What Is Direct Benefit Transfer (DBT) in India? A Complete Explainer of the JAM Trinity

How Direct Benefit Transfer Transformed Welfare Delivery in India

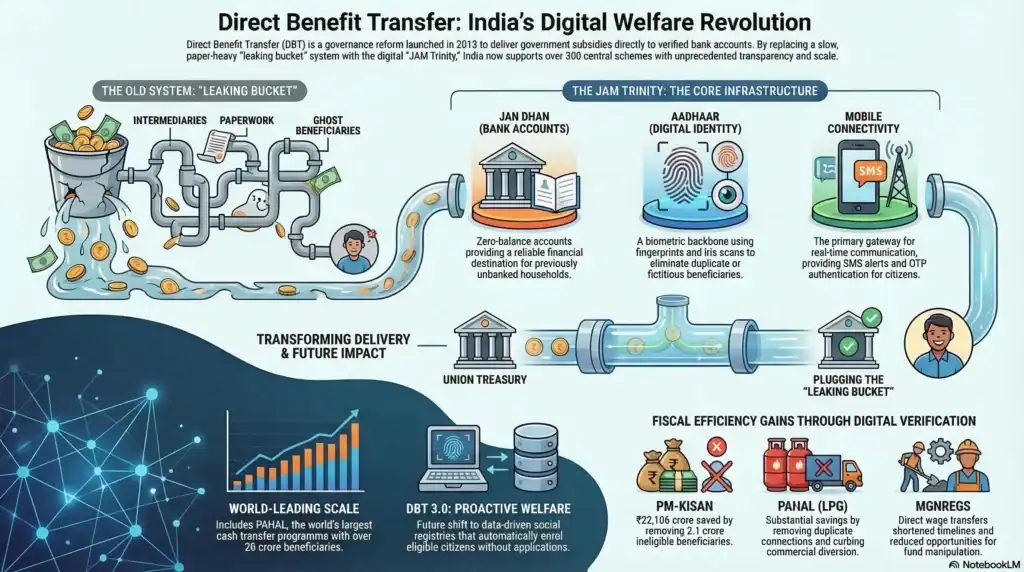

Direct Benefit Transfer (DBT) is widely considered one of the most transformative governance reforms undertaken in independent India. Introduced on 1 January 2013, DBT is a centrally administered initiative designed to ensure that government benefits, whether cash or in-kind, reach eligible citizens directly, without unnecessary delays or interference.

Instead of routing subsidies through layers of bureaucracy and intermediaries, the system sends funds straight into a beneficiary’s verified bank account. In principle, it replaces a slow, paper-heavy welfare pipeline with something closer to a direct digital transfer.

Before DBT came along, welfare delivery in India had a reputation for inefficiency. Economists sometimes described the system as a “leaking bucket.” The idea was simple: by the time a rupee allocated for welfare travelled through departments, local administrators, and distribution networks, only a fraction of its value might actually reach the intended beneficiary.

Money could disappear through administrative delays, duplicate identities, or outright diversion. DBT attempts to plug those leaks by creating a direct digital route through which benefits flow from the Union Government’s treasury to an Aadhaar-linked bank account, with far fewer opportunities for funds to get lost along the way.

Over the past decade, the system has expanded dramatically. Today, Direct Benefit Transfer (DBT) in India supports more than 316 central government schemes and over 2,000 state-level programmes, covering sectors ranging from agriculture and education to social security, labour, and health. The scale alone is striking. Institutions outside India have taken notice as well. The International Monetary Fund has described the digital infrastructure behind DBT as a “logistical marvel”, noting that no other welfare delivery mechanism currently operates at this scale. Similarly, the World Bank has highlighted DBT as a useful reference point for developing economies trying to modernise their own social protection systems.

At a Glance: India’s DBT & JAM Trinity (2026)

- What is Direct Benefit Transfer (DBT)?

A government reform that transfers subsidies directly into bank accounts using Aadhaar, eliminating intermediaries and ensuring faster, transparent welfare delivery.- What is the JAM Trinity?

The core infrastructure enabling DBT: Jan Dhan (bank accounts), Aadhaar (biometric identity), and Mobile (connectivity) for population-scale inclusion.- How much money has been transferred via DBT?

By January 2026, cumulative transfers exceeded ₹49.09 lakh crore, covering more than 450 central and 1,200 state welfare schemes.- What are the total savings from DBT?

By March 2026, DBT has generated savings of over ₹3.48 lakh crore by eliminating duplicate and “ghost” beneficiaries.- How many Jan Dhan accounts are active in 2026?

As of March 2026, there are 57.71 crore Jan Dhan accounts, forming the foundation of India’s financial inclusion ecosystem.

The JAM Trinity Explained: The Core Infrastructure Behind DBT

Jan Dhan Accounts: The Financial Gateway for DBT Payments

The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in August 2014, set out to tackle a very basic barrier: millions of Indians simply did not have a bank account. Without one, receiving a digital welfare payment was impossible, regardless of eligibility.

PMJDY addressed this gap by offering zero-balance, no-frills bank accounts, bringing previously unbanked households into the formal financial system. The scale of the effort is hard to overstate as it quickly grew into the largest financial inclusion programme in the world. In practical terms, these accounts became the final destination for DBT payments. Once a citizen has a Jan Dhan account, welfare funds have somewhere reliable to land.

Aadhaar Identity System: The Verification Backbone of DBT

Identity verification is the second piece of the puzzle. Managed by the Unique Identification Authority of India (UIDAI), Aadhaar assigns a 12-digit biometric identity number to residents of India. Within the DBT ecosystem, Aadhaar functions as a common identity layer that helps ensure benefits go to the right person.

Before digital identity systems were introduced, welfare programmes often struggled with duplicate or fictitious beneficiaries. Aadhaar’s biometric authentication, based on fingerprints or iris scans, helps governments confirm identities at the point of delivery and reduce those kinds of leakages.

Aadhaar also powers the Aadhaar Payment Bridge (APB), which acts as a routing mechanism that connects government payment instructions to the correct bank account. Citizens who want to verify whether their Aadhaar is linked to a bank account can check their seeding status through the official portal at myaadhaar.uidai.gov.in.

Mobile Connectivity: The Communication Layer of the DBT Ecosystem

The final pillar is mobile connectivity. While bank accounts and identity verification enable the actual transfer of funds, mobile phones provide the communication channel that keeps beneficiaries informed.

In many parts of India, especially rural areas, a mobile phone is the primary gateway to digital services. Even a basic feature phone can receive SMS alerts confirming that a subsidy has been credited, generate OTPs for authentication, or help users access scheme information. For beneficiaries who may live far from a bank branch, these small notifications can be surprisingly important: they provide proof that the money has arrived.

How the JAM Trinity Forms India’s Digital Public Infrastructure

What makes the JAM Trinity powerful is not any single component, but the way the three layers work together. Bank accounts provide the financial endpoint, Aadhaar confirms identity, and mobile networks connect citizens to the system in real time.

Taken together, these components form a core part of what policymakers and institutions such as NITI Aayog describe as India’s Digital Public Infrastructure (DPI), a set of interoperable platforms that handle identity, payments, and data exchange at a population scale.

The broader implications of the JAM Trinity have attracted attention well beyond India. Policy researchers frequently cite it as an example of how digital infrastructure can modernise welfare systems, and several countries across Africa, Southeast Asia, and Latin America are now exploring similar frameworks.

How Direct Benefit Transfer Works: PFMS, APB, and Payment Infrastructure

Public Financial Management System (PFMS): The Government Payment Engine

Behind the scenes of every DBT payment sits a financial platform that most citizens rarely hear about but depend on constantly: the Public Financial Management System (PFMS). This web-based system was developed by the Controller General of Accounts under the Ministry of Finance to track, manage, and disburse government funds with far greater precision than older paper-based systems ever allowed.

In simple terms, PFMS acts as the central command centre for government payments. Ministries initiate transfers through the system, which then routes funds directly to beneficiaries’ bank accounts. One important feature is what officials call “just-in-time” fund release. Instead of allocating large sums in advance where money might sit idle or be misused, PFMS releases funds only when they are actually due to be paid.

The platform connects to a vast banking network that includes more than 500 banks, covering commercial banks, regional rural banks, cooperative banks, and even India Post’s banking services. This broad integration is what allows DBT payments to reach beneficiaries living in remote villages just as reliably as those in major cities.

Aadhaar Payment Bridge (APB): Routing DBT Payments to Bank Accounts

While PFMS manages the release of funds, the Aadhaar Payment Bridge (APB) handles the routing of those payments. Operated by the National Payments Corporation of India (NPCI), the APB functions as a mapping system that connects an individual’s Aadhaar number to their preferred bank account.

Here’s how it works in practice. When a government department initiates a DBT payment, it does not necessarily need the beneficiary’s bank account details. Instead, it sends the Aadhaar number along with the payment amount to NPCI. The APB then checks its internal “mapper,” identifies the bank account linked to that Aadhaar number, and routes the funds accordingly, often within minutes.

For citizens who want to confirm whether their Aadhaar is properly linked to a bank account, NPCI provides a seeding portal where this status can be verified.

Cash Transfers vs In-Kind Transfers in the DBT System

DBT doesn’t operate in just one way; it supports two main types of benefit delivery.

The first is the cash transfer mode, where subsidy or support payments are deposited directly into a beneficiary’s bank account. Schemes like the PAHAL LPG subsidy, PM-KISAN income support for farmers, and MGNREGS wage payments fall into this category. In these cases, the beneficiary receives money and can decide how to spend it.

The second is in-kind transfer mode, which works a little differently. Instead of receiving cash, beneficiaries collect physical goods such as subsidised food grains under the Public Distribution System (PDS). At the point of distribution, Aadhaar authentication is used to verify identity. Once the biometric verification is successful, the system unlocks the entitlement stored in the government database.

Both methods rely on the same digital identity and payment infrastructure. The difference lies mainly in the final step: whether the benefit arrives as money in a bank account or as a physical good released after authentication.

Major Government Schemes Using Direct Benefit Transfer

PAHAL LPG Subsidy: The World’s Largest Cash Transfer Programme

One of the earliest and most widely cited examples of DBT in action is the PAHAL (Pratyaksha Hastaantarit Laabh) scheme for LPG subsidies. Often described as the largest direct cash transfer programme in the world, PAHAL fundamentally changed how cooking gas subsidies are delivered in India.

Before the reform, LPG cylinders were sold at subsidised prices. While the intention was to make cooking fuel affordable for households, the system had a major flaw: subsidised cylinders were frequently diverted into commercial markets where they could be sold at higher prices. This created a parallel market and significant leakage in the subsidy system.

PAHAL replaced the old model with a cleaner approach. Consumers now purchase LPG cylinders at the market price, and the subsidy amount is transferred directly into their bank account through DBT. This separation between the market price and the subsidy helped curb diversion while ensuring that legitimate consumers still receive the intended benefit.

The scheme expanded rapidly, eventually enrolling over 26 crore beneficiaries. According to PRS Legislative Research “Currently, there are a total of 27.16 crore LPG (domestic) connections in the country. Of these, 26.12 crore (94%) consumers are beneficiaries under the PAHAL scheme, and therefore, can avail LPG cylinders at subsidised rates.” The programme generated substantial savings in its early years by removing duplicate connections and curbing misuse.

PM-KISAN Income Support Scheme for Farmers

Another major programme running on DBT infrastructure is PM-KISAN (Pradhan Mantri Kisan Samman Nidhi). The scheme provides Rs. 6,000 annually to eligible small and marginal farmers, distributed in three instalments of Rs. 2,000 each and credited directly to Aadhaar-linked bank accounts.

While the individual payment may appear modest, its predictability is often what matters most. For many farmers, especially those managing small landholdings, a guaranteed inflow of funds during the agricultural cycle can help cover input costs such as seeds, fertilisers, or labour.

The programme has also demonstrated how digital verification can improve targeting. According to data released by PIB, Aadhaar-based verification helped identify and remove over 2.1 crore ineligible beneficiaries, including income-tax filers and government employees who did not meet eligibility criteria. The process reportedly saved Rs. 22,106 crore, which could then be redirected to genuine farming households.

MGNREGS Wage Payments Through DBT

The Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) is one of India’s largest social protection programmes, guaranteeing up to 100 days of wage employment per year for rural households.

Historically, wage payments under the scheme often faced delays and irregularities. Workers sometimes had to wait weeks, occasionally longer, to receive their wages, and in some cases, fake job cards were reportedly used to siphon funds.

The integration of DBT has reshaped how payments are made. Wages are now transferred directly into workers’ bank accounts via the Aadhaar Payment Bridge, shortening payment timelines and reducing opportunities for manipulation. Reports from the Comptroller and Auditor General (CAG) of India note improvements in transparency and record-keeping after the shift to digital wage payments, although they also highlight areas where administrative oversight still needs strengthening.

Social Security Pensions Under DBT

DBT has also transformed the way pensions are distributed under the National Social Assistance Programme (NSAP), which provides financial support to vulnerable groups such as the elderly, widows, and persons with disabilities.

Earlier, pension payments were often distributed as cash through local administrative channels, typically via gram panchayat officials. While this system worked in many places, it also left room for delays, deductions, or informal fees.

Direct bank transfers have simplified the process considerably. Pension amounts are now credited straight into beneficiaries’ accounts, making the payment process more predictable and easier to track.

According to observations from UNDP India, this shift has had broader social implications as well. Regular and transparent pension payments can contribute to greater financial stability for vulnerable households, often improving access to food, healthcare, and other basic needs while preserving a sense of dignity for recipients.

Social Impact of DBT: Women’s Empowerment and Financial Inclusion

Financial Independence and Household Bargaining Power

One of the most interesting and sometimes overlooked effects of DBT has been its impact on women’s economic independence. When welfare payments are deposited directly into a woman’s personal bank account, the dynamics within households can subtly begin to shift. Access to funds, even modest amounts, often translates into greater influence over how household money is spent.

Research consistently suggests that when women control financial resources, spending patterns tend to prioritise essentials such as food, education, and healthcare. The MoSPI Women and Men in India report highlights how financial inclusion, particularly through bank accounts opened under Jan Dhan, has expanded women’s access to the formal economy.

Academic research backs up these observations. A peer-reviewed study published on ScienceDirect found that direct cash transfers to women are associated with greater participation in household decision-making. Similarly, the Poverty Action Lab (J-PAL) has documented how the identity of the transfer recipient matters: when women receive welfare payments directly, funds are more likely to be directed toward children’s nutrition, schooling, and long-term household wellbeing.

State-Level Cash Transfer Schemes for Women

Several Indian states have taken the DBT infrastructure a step further by launching targeted cash transfer schemes specifically designed for women. In many ways, these programmes resemble a limited form of Universal Basic Income, at least for female beneficiaries.

Karnataka’s Gruha Lakshmi scheme and Madhya Pradesh’s Ladli Behna Yojana are two prominent examples. Both programmes use DBT systems to deposit regular payments directly into women’s bank accounts, providing a predictable source of income that households can rely on.

Early analyses suggest these schemes may have broader social effects beyond the immediate financial support. An SBI Research study on Ladli Behna reported improvements in financial literacy, savings behaviour, and overall self-reported wellbeing among beneficiaries.

At the same time, economists and fiscal analysts are watching these programmes closely. A PRS India analysis of state finances points out that large-scale cash transfer schemes can place significant pressure on state budgets. While politically popular and socially impactful, their long-term sustainability remains an ongoing policy debate.

Extending DBT to Tribal and Marginalised Communities

Delivering welfare benefits to geographically remote and historically marginalised communities has always been one of the most difficult challenges in public policy. In India, many Scheduled Tribe populations live in areas with limited administrative infrastructure and banking access.

DBT systems are increasingly being adapted to address this challenge. The DBT Tribal portal tracks welfare transfers specifically targeting tribal beneficiaries under schemes managed by the Ministry of Tribal Affairs.

Technology also plays a role in identifying underserved areas. Geospatial tools such as the NRSC’s Bhuvan Aadhaar platform help map settlements and track where welfare coverage may still be incomplete. By combining satellite data with administrative databases, policymakers can identify communities that have not yet been integrated into the DBT system.

Removing Intermediaries from Welfare Delivery

Perhaps one of the most visible changes brought by DBT is the removal of intermediaries who once stood between beneficiaries and welfare payments. In the past, local power structures- village-level officials, panchayat representatives, or distribution agents- sometimes controlled access to benefits.

While many of these actors performed legitimate administrative roles, the system also created opportunities for informal payments, delays, or selective distribution. Beneficiaries often had little transparency about how funds moved through the system.

DBT’s direct-to-bank-account model largely bypasses these intermediaries. Once eligibility is verified and a payment is approved, the transfer goes straight to the beneficiary. Studies by policy institutions such as CPR India and ORF suggest that this disintermediation has weakened certain local patronage networks that previously influenced welfare distribution.

That said, the shift has also had side effects. In some cases, the removal of intermediary roles has displaced informal employment linked to older welfare distribution systems, such as parts of the Public Distribution System supply chain. Like many governance reforms, the transition has brought both efficiency gains and new policy questions.

Challenges in Direct Benefit Transfer: Exclusion, Digital Divide, and Privacy

Exclusion Errors in Aadhaar Authentication

For all its efficiency gains, DBT is not immune to problems. One of the most frequently discussed issues is exclusion error, situations where eligible beneficiaries are unable to access benefits because the system fails to recognise or authenticate them.

A major source of this problem lies in biometric authentication. Aadhaar verification often relies on fingerprint scans, but in real-world conditions, fingerprints do not always scan reliably. Manual labourers, elderly individuals, or people whose fingerprints have worn down over time can sometimes struggle to authenticate successfully.

Research has flagged this concern. A study published in the American Economic Review documented authentication failure rates in certain contexts that raised questions about the reliability of biometric systems for vulnerable populations. Similarly, the CAG of India has reported instances where authentication failures led to the denial of Public Distribution System (PDS) rations for households that were otherwise eligible.

In theory, fallback mechanisms exist, but their implementation on the ground can vary widely.

The Digital Divide in Welfare Access

Another challenge is more structural: DBT relies heavily on digital infrastructure and digital literacy, both of which remain unevenly distributed across India.

Having a bank account and an Aadhaar number does not necessarily mean someone feels comfortable navigating digital processes. Tasks that appear simple -checking a payment status online, entering an OTP, or filing a grievance digitally -can become genuine obstacles for beneficiaries unfamiliar with digital interfaces.

This gap is particularly visible among older citizens and rural women, many of whom are first-time users of formal banking systems. Recognising this issue, the Ministry of Electronics and Information Technology (MeitY) has expanded digital literacy programmes such as DigiSakhi and the Common Service Centre network to provide assistance at the village level.

Still, the broader digital divide between urban and rural areas continues to shape how smoothly DBT functions in practice.

Last-Mile Banking and Cash Withdrawal Challenges

Even when a DBT payment successfully reaches a beneficiary’s bank account, another challenge may appear: accessing the money itself.

Large parts of rural India still lack easy access to bank branches or ATMs. Beneficiaries often rely on Business Correspondent (BC) agents or banking representatives who travel to villages with micro-ATM devices. These agents are essential to the last-mile banking ecosystem, but their availability and cash liquidity can be inconsistent.

In some cases, beneficiaries must wait for a BC agent to visit their village or travel long distances to withdraw funds. Issues such as dormant accounts, minimum-balance penalties, or insufficient cash at withdrawal points can add further friction to the process.

The Reserve Bank of India has issued multiple guidelines aimed at strengthening the BC network and improving last-mile banking infrastructure. Despite these efforts, the experience of accessing DBT payments still varies widely depending on location, infrastructure, and local banking capacity.

Privacy and Data Governance Concerns

Beyond operational challenges, DBT also raises deeper questions about data governance and privacy. The system relies on large interconnected databases that track identity, financial transactions, and welfare eligibility across multiple government platforms.

This integration brings clear benefits in terms of efficiency and fraud reduction, but it also means that the DBT ecosystem generates enormous volumes of personal data. UIDAI’s own governance documents acknowledge the tension between the advantages of biometric identity systems and the risks associated with storing and linking sensitive information at scale.

Policy researchers and civil society organisations continue to debate whether existing legal safeguards are strong enough to protect citizens from misuse of such data. Institutions such as CPR India have contributed to ongoing discussions about balancing technological efficiency with privacy protections.

In many ways, this debate reflects a broader policy dilemma: how to build highly efficient digital welfare systems without compromising citizens’ rights and data security.

The Future of DBT in India: DBT 2.0 and DBT 3.0

DBT 2.0: Digital Eligibility Verification Systems

The next stage in the evolution of Direct Benefit Transfer focuses on simplifying how eligibility is verified. Traditionally, applying for welfare schemes in India meant collecting and submitting a stack of documents such as income certificates, caste certificates, land ownership records, and more. Even small discrepancies between documents maintained by different departments could delay or derail an application.

DBT 2.0 aims to reduce this friction by shifting eligibility verification into the digital layer. Platforms such as DigiLocker, India’s official digital document repository, allow citizens to store verified versions of government-issued documents online. Combined with API Setu, a government API gateway that enables secure data exchange between departments, these systems allow eligibility checks to happen automatically.

In practice, this means a citizen may not need to physically submit documents at all. For example, a farmer applying for PM-KISAN could have land ownership verified directly through state land records. Similarly, a student applying for a scholarship might have their caste certificate validated through a digitally stored record in DigiLocker. By automating these cross-checks, DBT 2.0 attempts to eliminate bureaucratic delays and reduce the chances of eligible beneficiaries being excluded due to paperwork mismatches.

DBT 3.0: Proactive Welfare Through Social Registries

If DBT 2.0 focuses on simplifying applications, DBT 3.0 pushes the idea even further: a welfare system where citizens may not need to apply at all.

The concept centres around Social Registries, which are integrated databases that combine demographic, economic, and social information about households. By analysing this data, the system could automatically identify individuals who qualify for certain welfare programmes and enrol them without requiring a formal application.

In this model, the state becomes proactive rather than reactive. Instead of citizens navigating complex administrative processes, the system identifies eligibility and triggers benefits automatically. NITI Aayog has promoted the Social Registry approach as a way to ensure that eligible citizens are not excluded simply because they lack awareness of a scheme, face literacy barriers, or live far from government offices.

Of course, such a system would also raise important questions about data governance, privacy, and institutional accountability. But in theory, it represents a major shift in how welfare states function — from application-driven systems to data-driven, proactive governance.

Using DBT for Disaster Relief and Climate-Adaptive Welfare

Another emerging use of DBT infrastructure lies in disaster response and climate adaptation. As extreme weather events become more frequent, governments are exploring ways to deliver relief funds quickly to affected populations.

The existing DBT architecture-the pipeline connecting Aadhaar identity, PFMS fund management, and bank accounts- provides ready-made “rails” for rapid financial assistance. Instead of waiting weeks for administrative assessments, disaster relief payments could potentially be triggered automatically when certain environmental thresholds are reached.

Geospatial tools such as NRSC’s Bhuvan Aadhaar platform already help map agricultural regions and vulnerable settlements. When combined with satellite-based crop stress indicators and weather data, these tools could allow governments to identify affected farming communities and release financial support within hours.

If implemented effectively, this approach could transform how disaster relief works, shifting from slow, manual processes to near real-time financial assistance delivered directly to affected households.

Common Questions: India’s DBT & JAM Trinity (2026)

The JAM Trinity creates a direct digital pipeline for welfare delivery. Jan Dhan provides bank accounts, Aadhaar verifies beneficiary identity, and Mobile enables communication. This integration allows the government to bypass intermediaries and ensure 100% of the benefit reaches the intended recipient.

The DBT framework is built on three pillars:

Aadhaar Payment Bridge (APB): Uses Aadhaar numbers as financial addresses for bulk transfers.

Public Financial Management System (PFMS): Tracks fund flow from the treasury to the beneficiary.

Business Correspondents (BCs): “Bank Mitras” delivering last-mile banking services in underserved areas.

By March 2026, DBT savings have exceeded ₹3.48 lakh crore. These gains come from removing 5.2 crore fake ration cards and 4.1 crore duplicate LPG connections, effectively eliminating intermediary leakages and “ghost” beneficiaries.

As of March 2026, India has 57.71 crore Jan Dhan accounts. Notably, over 55% are held by women, and more than 66% are in rural areas, highlighting massive progress in gender-inclusive financial growth.

Yes. Beneficiaries receive SMS alerts on basic phones and withdraw funds using AEPS (Aadhaar Enabled Payment System) through local agents. This ensures last-mile access for citizens without requiring smartphones or private internet connections.

Why Direct Benefit Transfer Matters for India’s Welfare State

Direct Benefit Transfer is often discussed in technical terms — databases, payment rails, authentication layers. But step away from the architecture for a moment, and the idea becomes much simpler. At its core, DBT is an attempt to repair something that had quietly eroded over decades: trust between citizens and the state.

For a long time, welfare in India carried a certain unpredictability. Benefits might arrive late, be partially diverted, or depend on navigating local power structures. DBT tries to strip away some of that uncertainty by making the flow of welfare funds more transparent and more direct.

The change becomes most visible in ordinary moments. A farmer in rural Bihar receives an SMS confirming that Rs. 2,000 has landed in her account. A widow in Odisha withdraws her pension without needing to negotiate with a local intermediary or pay a small unofficial fee. These moments are small in isolation, but multiplied across millions of households, they begin to reshape how public welfare actually feels on the ground.

Scholars have tried to measure these shifts systematically. The IES paper by Tiwari and Kamila remains one of the more detailed academic assessments of DBT’s development. Their findings broadly echo the views expressed by institutions such as the IMF, the World Bank, and the UNDP: despite implementation challenges, DBT represents a meaningful structural improvement in India’s welfare delivery system.

That said, the journey is far from finished. The transition toward DBT 3.0 will demand continued investment in digital infrastructure, stronger safeguards for data governance, more responsive grievance redressal systems, and sustained efforts to build digital literacy, especially among citizens who remain on the margins of the digital economy.

For citizens who want to engage with the system directly, the DBT Bharat portal remains the most comprehensive public resource. Practical steps such as checking Aadhaar-bank linking status or locating the nearest Aadhaar enrolment centre can make a real difference in ensuring that eligible individuals are connected to the benefits intended for them.

In the end, DBT is not just about moving money more efficiently. It is about building a welfare system that works quietly, predictably, and fairly, something citizens can rely on without needing to fight for it every time.

[…] this infrastructure really showed its teeth, though, was in Direct Benefit Transfers […]