Salary Payment Rules in India (2026): 7th Day Deadline, 48-Hour FnF & 50% Wage Rule Explained

India’s labour law landscape is undergoing its most consequential overhaul since Independence, which has led to significant changes in the salary payment rules in India. With the Government of India having notified the four Labour Codes effective November 21, 2025, employers across every sector now face binding new rules on when salaries must be paid, how exit settlements must be processed, and how salary structures must be composed. Three rules in particular stand out for their operational and financial impact: the 7th Day salary payment deadline, the 48-hour Full and Final Settlement requirement, and the 50% Wage Rule governing salary composition. This guide explains all three in detail, with compliance timelines, industry impacts, and an actionable checklist for 2026 and beyond.

At a Glance: India’s 2026 Salary Payment & Wage Rules

The Big Shift

India’s labour law overhaul is now in force. As of November 21, 2025, 29 legacy laws have been consolidated into 4 Labour Codes, fundamentally reshaping payroll compliance for all employers.Salary Deadline: 7th or 10th Day Rule

Under the Code on Wages (Section 17):

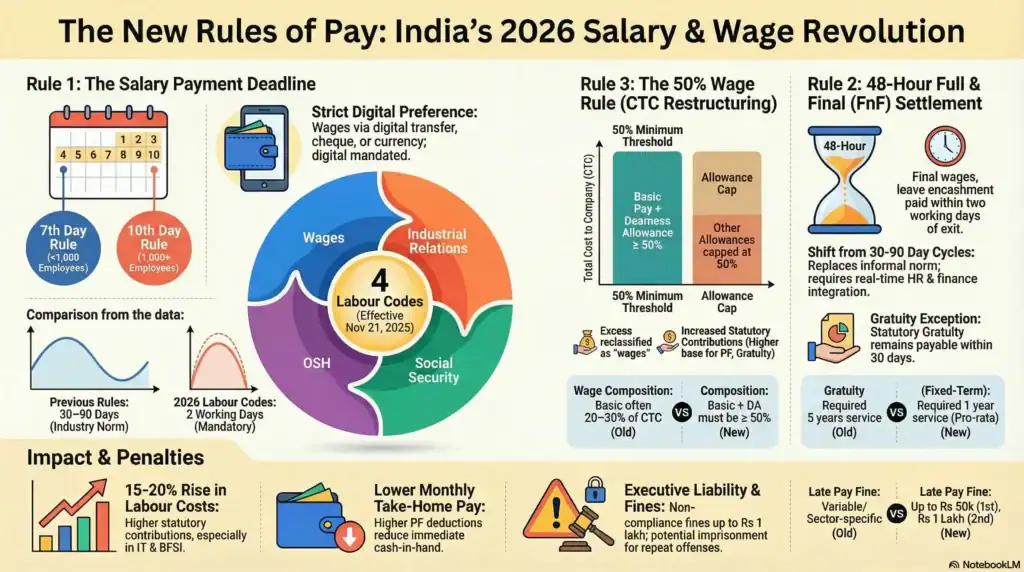

- Companies with fewer than 1,000 employees must pay salaries by the 7th of the following month

- Companies with 1,000 or more employees must pay by the 10th

There are no longer any sector-based exemptions.48-Hour FnF Settlement Rule

All Full and Final (FnF) settlements, including unpaid salary and leave encashment, must be completed within two working days of an employee’s exit (resignation, termination, or retrenchment).The 50% Wage Rule (CTC Restructuring)

- Basic Pay and Dearness Allowance (DA) must constitute at least 50% of total CTC

- Allowances are capped at 50%

This standardizes salary structures across industries.Financial Impact on Employers and Employees

- Employer contributions (PF and gratuity) are expected to increase by 15–20%

- Employees may see lower monthly take-home pay, offset by higher long-term benefits

Compliance: Immediate Action Required

To avoid penalties and executive liability, employers should:

- Audit and restructure CTC components

- Implement real-time FnF processing systems

- Ensure digital compliance via the Shram Suvidha Portal

What Are the New Salary Payment Rules Under India’s Labour Codes (2026)?

From 29 Labour Laws to 4 Labour Codes: What Changed?

For decades, Indian employers navigated a complex web of 29 central labour statutes, each with different definitions, thresholds, and compliance requirements. The consolidation of these laws into four comprehensive Codes represents a structural reset. The four Labour Codes are: the Code on Wages 2019, the Industrial Relations Code 2020, the Code on Social Security 2020, and the Occupational Safety, Health and Working Conditions (OSH) Code 2020. Together, they cover every aspect of the employment relationship from hiring to exit, wage payment to social security, and workplace safety to dispute resolution.

As noted by the Government of India, this consolidation is described as the biggest labour reform in independent India. The Code on Wages 2019 is the most directly relevant to salary payment rules. It governs the definition of wages, payment timelines, and penalties for non-compliance for all employees regardless of salary level, expanding coverage far beyond the earlier Payment of Wages Act 1936, which applied only to workers earning up to a specified wage ceiling.

Why Salary Payment Rules Matter for Employers in 2026?

The new rules matter because they affect virtually every registered employer in India. The Code on Wages applies to establishments employing two or more workers, meaning startups, SMEs, large corporates, and public sector undertakings all fall within its scope. Analysis of the Labour Codes shows that sweeping changes to employment relationships that require immediate legal and operational attention from businesses operating in India have been introduced.

For HR and payroll teams, the implications are concrete: salary payment cycles must be reconfigured, salary structures must be audited and redesigned, exit processing workflows must be accelerated dramatically, and statutory contribution calculations will change substantially due to the redefinition of wages. The financial impact extends beyond payroll operations to balance sheets, as higher wage bases increase provident fund and gratuity liabilities.

Labour Codes Implementation Timeline & Current Status (2025-2026)

The four Labour Codes were passed by Parliament between 2019 and 2020. All four received Presidential assent, and the central government notified the rules under each Code. According to a detailed update from EY India, the four Labour Codes were made effective across the country from November 21, 2025. The Press Information Bureau of India confirmed this in its official release, describing the notification as simplifying and streamlining India’s labour law framework.

DLA Piper’s global employment team documented the notification in detail, noting that while the central rules are now operative, the practical rollout requires state governments to notify their own complementary rules on concurrent subjects. Several large states had already pre-notified their draft rules; full state-level compliance is expected to be consolidated through 2026.

7th Day Salary Payment Rule Explained Under Code on Wages

Legal Provision: Section 17 Salary Payment Deadline Explained

Section 17 of the Code on Wages 2019 is the operative provision on wage payment timelines. It specifies that wages must be paid before the expiry of the 7th day after the last day of the wage period for establishments employing fewer than 1,000 workers. For larger establishments employing 1,000 or more workers, wages must be paid before the expiry of the 10th day after the last day of the wage period. This detailed reading of the Code’s provisions covers the wage period definitions and payment obligations in full.

This rule applies uniformly across all industries and ownership structures, replacing the fragmented timelines that previously existed under the Payment of Wages Act 1936 and the Minimum Wages Act 1948. The Code also mandates that wages be paid in current coin, currency notes, by cheque, or through digital transfer to the worker’s bank account, with digital payment being the strongly preferred and increasingly mandated mode. A detailed guideline of the payroll deadline schedules for 2026 is available at Wisemonk.

Old vs New Salary Payment Deadlines in India

Under the Payment of Wages Act 1936, wages had to be paid by the 7th day of the following month for establishments employing fewer than 1,000 persons, and by the 10th day for larger establishments. The Code on Wages 2019 broadly retains this structure but makes it universal and unambiguous. The critical change is the elimination of the wage ceiling that previously limited the Payment of Wages Act’s coverage to lower-paid workers. Under the new Code, all employees, including senior managers and executives, are covered, creating uniform compliance obligations regardless of pay level.

Previously, many large IT companies and professional services firms operated on flexible payment cycles that could extend beyond the 10th of the month. Under the new framework, any delay beyond the stipulated deadline constitutes a violation, regardless of employer size or industry. This guide by TopSource documents the detailed impact of this change on payroll processing.

Salary Payment Timelines by Wage Type (Daily, Weekly, Monthly)

The Code on Wages establishes different payment windows depending on the wage period agreed between the employer and the worker. For daily wage workers, payment must be made at the end of the work shift or within 24 hours of the end of the working day in most cases. For weekly wage periods, payment must be completed within two working days of the end of the working week. For fortnightly wage periods, the deadline is within two working days of the end of the fortnight. For monthly-waged employees, the 7th-day or 10th-day rule applies as described above.

Employers may not impose wage periods longer than one month on any category of worker. This is particularly relevant for contractual and gig arrangements where some employers have historically adopted irregular or extended payment cycles. The explainer by Wisemonk provides further guidance on payroll calendars and compliance dates for 2026.

Industry-Wise Applicability of Salary Deadlines (IT, Startups, Manufacturing)

The salary payment deadline applies across all industries without sectoral exemptions. The IT and software services sector, which has historically operated on mid-month or end-of-month payroll cycles stretching into the second week of the following month, now needs to ensure compliance with the 7th or 10th day deadline.

NASSCOM, the industry body for the Indian IT sector, submitted detailed feedback on the draft labour code rules on behalf of its members, raising several operational concerns about implementation timelines and definitions.

Manufacturing establishments with large contract labour workforces and daily wage workers already operate within tighter payment windows and may find less operational disruption. A detailed analysis of contract staffing operations in 2026, including the implications for staffing agencies and their clients in this guide by Votltech HR Services. Startups and smaller tech companies should note that the Code applies from the point of hiring the second employee, making early compliance essential.

Penalties for Late Salary Payment Under Labour Codes

Non-payment or delayed payment of wages under the Code on Wages 2019 attracts significant financial penalties. For a first offence, the employer is liable to a fine of up to Rs 50,000. For a second or subsequent offence within five years, the penalty increases to up to Rs 1 lakh, and the employer may also face imprisonment of up to three months. Officers responsible for payroll who are shown to have authorised or permitted the default may be personally liable.

The compliance obligations and penalty structure under the Code are respectively detailed in these guides by Complinity and Bharat Payroll. In addition to statutory penalties, aggrieved employees may file claims for the unpaid wages along with interest at prescribed rates for the period of delay.

48-Hour Full and Final Settlement Rule (FnF) Explained

What Is Full and Final Settlement (FnF) in India?

Full and Final Settlement refers to the complete closure of all financial obligations between an employer and a departing employee. This includes payment of outstanding salary for the worked period up to the date of exit, encashment of earned but unused leave, payment of gratuity where applicable, processing of provident fund transfers or withdrawal, payment of any contractual bonuses or incentives due, and deduction of any amounts lawfully owed by the employee, such as advances or notice pay in lieu.

Until the Labour Codes, FnF was governed primarily by individual employment contracts and informal industry practice. There was no universal statutory deadline for completing the settlement. Delays of 30, 60, or even 90 days were common, creating serious financial hardship for departing employees and leading to frequent disputes.

Section 17(2): 48-Hour FnF Rule Explained

The Code on Wages 2019, under Section 17(2), mandates that where an employee is removed, dismissed, retrenched, resigns, or becomes unemployed due to the closure of the establishment, the final wage payment must be made within two working days of the date of such separation. This provision effectively creates a 48-hour FnF window, though the precise count is in working days rather than calendar hours. The implications of this rule for payroll processing are explored in detail in this guide and at Topsource.

This is a transformative change. Previously, most large employers operated on FnF cycles of 30 to 90 days, often citing the need to verify notice period compliance, recover company assets, complete tax calculations, and process PF and gratuity paperwork. The 48-hour window compresses this entire process into a near-real-time operation, requiring significant investment in HR systems and process redesign.

Do Weekends and Holidays Count in the 48-Hour FnF Rule?

The Code specifies two working days, not two calendar days. This distinction matters for exits that happen on Fridays or immediately before public holidays. In such cases, the 48-hour working-day window may extend across a weekend or holiday, but the obligation to pay within two working days remains binding. Employers cannot claim weekends or gazetted holidays as extensions beyond what the working-day calculation already accommodates.

Gratuity vs FnF Settlement: Key Legal Differences

Gratuity is a statutory retirement benefit governed separately under the Code on Social Security 2020, payable to employees who have completed five or more years of continuous service (or one year for fixed-term employees under the new Code). Gratuity is calculated as 15 days’ wages for each completed year of service, using the last drawn basic wages plus dearness allowance. The Code on Social Security specifies that gratuity must be paid within 30 days of it becoming payable, a separate and longer timeline from the 48-hour FnF rule.

FnF, by contrast, encompasses salary arrears and leave encashment that must be paid within two working days. Employers should structure their FnF workflows to process the two-day components (salary, leave encashment) separately from gratuity processing, if necessary, to avoid the entire settlement being blocked by gratuity calculation delays. The comprehensive Guide to the Labour Codes published by Cyril Amarchand Mangaldas covers these distinctions in authoritative detail.

Payroll and Exit Management Impact of 48-Hour FnF Rule

The 48-hour FnF rule is widely recognised as the single most disruptive operational requirement of the new Codes for HR departments. Manual payroll systems that process FnF on monthly payroll runs cannot comply. Employers need automated payroll systems capable of processing ad-hoc FnF transactions in real time, with integrated leave management, salary processing, and statutory compliance modules.

The case for payroll automation in the context of the new Labour Codes is made in this explainer. Managed payroll service providers such as those at Paysquare are actively building 48-hour FnF processing capabilities into their service offerings.

50% Wage Rule Explained: Salary Structure Changes in India

Definition of ‘Wages’ Under Code on Wages 2019

The Code on Wages 2019 introduces a precise statutory definition of wages that is different from the common understanding of basic salary. Under Section 2(y), wages mean all remuneration, whether by way of salaries, allowances, or otherwise, expressed in terms of money, and include basic pay, dearness allowance, and retaining allowance, if any.

The definition explicitly excludes a wide range of components, including house rent allowance, conveyance allowance, travel allowance, special allowances not included in the basic pay definition, bonuses not forming part of the remuneration, gratuity, PF contributions by the employer, and retrenchment compensation.

A thorough explanation of this definition and its implications is available at Complinity. PwC India provides a practitioner-level analysis of how the wage definition interacts with salary structuring and compliance.

50% Wage Threshold Rule: What It Means for Employers

The proviso to Section 2(y) of the Code on Wages 2019 states that if the total of exclusions (allowances not forming part of wages) in any wage period exceeds 50% of total remuneration, the excess shall be deemed remuneration and shall be treated as wages. In practical terms, this means that at least 50% of an employee’s total monthly CTC must consist of wages as defined above (basic + DA). Allowances and exclusions cannot together exceed 50% of the total pay package.

The impact on Indian salary structures, where basic pay has historically been kept low (sometimes as little as 20 to 30% of CTC) to minimise PF and gratuity contributions while maximising take-home through allowances, is substantial.

Allowance Restructuring and Salary Reclassification Impact

Indian employers, particularly in the IT, BFSI, and professional services sectors, have for decades structured salary packages with high proportions of special allowances, performance pay, meal vouchers, communication reimbursements, and other components that fall outside the statutory wage definition. A typical mid-career IT professional might have a basic salary of 25% of CTC, with the rest split across HRA, special allowances, and variable pay. Under the 50% rule, this structure would need to be reconfigured so that wages constitute at least 50% of the package.

Where current structures violate the threshold, employers must either increase the basic wages component or have certain allowances reclassified and treated as wages, with knock-on effects for PF and gratuity calculations. The Topsource analysis walks through the restructuring implications. The Dezshira advisory firm covers these compliance nuances in its guide.

Impact on PF, Gratuity, and Bonus Calculations

The most significant downstream effect of the 50% wage rule is on statutory contribution calculations. Provident Fund contributions under the Employees’ Provident Funds and Miscellaneous Provisions Act are calculated at 12% of basic wages and DA for both employer and employee. When basic wages increase to at least 50% of CTC under the new definition, the PF contribution base rises proportionally, increasing the cash outflow for both parties.

Similarly, gratuity is calculated at 15 days’ basic wages plus DA per year of service. A higher wage base directly increases the gratuity liability an employer must eventually fund. KPMG, in its detailed analysis estimates that employers in high-allowance-ratio sectors could see total labour costs increase by 15 to 20% after full compliance with the 50% wage rule. The earlier KPMG flash alert tracks the evolving compliance landscape.

Does the 50% Wage Rule Reduce Take-Home Salary?

For employees, the immediate effect of the 50% wage rule is a reduction in net take-home salary, even if the gross CTC remains unchanged. Higher basic wages mean higher mandatory PF deductions (12% of the increased basic), which reduces the monthly pay credited to the bank account. While the employee ultimately receives the PF corpus at retirement or on exit, the monthly cash shortfall can be significant. An employee on Rs 1 lakh CTC with basic restructured from Rs 25,000 to Rs 50,000 would see their own PF deduction rise from Rs 1,800 to Rs 6,000 per month.

Employees in lower income brackets may find the take-home reduction more acute, while those nearing retirement may welcome the larger PF accumulation.

Financial Impact of New Salary Rules on Employers in India

Labour Cost Increase: 15-20% Impact Explained

The combined effect of the 50% wage rule on PF contributions, gratuity funding, and bonus calculations can increase total labour costs by 15 to 20% for employers in sectors with historically low basic pay ratios. KPMG has flagged this range in its GMS flash alert coverage. For a company with a payroll of Rs 100 crore annually, this could translate to an additional Rs 15 to 20 crore in annual labour costs once the new rules are fully implemented. The scale of the increase depends on the current basic-to-CTC ratio across the workforce.

Balance Sheet Impact Under Ind AS 19 (Gratuity Liability)

Under Indian Accounting Standard 19 (Ind AS 19), which governs the accounting treatment of employee benefits, gratuity is classified as a defined benefit obligation. Any increase in the wage base that feeds into the gratuity calculation must be reflected in the actuarial valuation of the liability. For listed companies and large private firms, the restatement of gratuity liability following the 50% wage rule will create a one-time charge to the P&L or Other Comprehensive Income, depending on the accounting policy adopted. Finance teams should initiate revised actuarial valuations well ahead of notification dates.

Gratuity Rules for Fixed-Term Employees Under Labour Codes

One of the more significant and less-discussed changes in the Code on Social Security 2020 is the extension of gratuity eligibility to fixed-term contract employees after just one year of continuous service, compared to the five years required for permanent employees. As contract and project-based hiring grows, particularly in the IT, consulting, and infrastructure sectors, this provision creates a new gratuity liability for categories of workers previously excluded. The DLA Piper briefing covers this change in its analysis of the Code on Social Security.

Tax Implications of Salary Restructuring in India

Salary restructuring under the 50% wage rule has tax implications for employees. HRA exemption under Section 10(13A) of the Income Tax Act is calculated as the least of three values, one of which is the actual HRA received. If HRA as a proportion of CTC falls to comply with the 50% wage rule, the HRA exemption available to employees in metro cities may be reduced. PwC India’s Labour Codes resource and the Union Budget 2026 update together provide context for the interplay between the Labour Codes and income tax planning.

Industry-Wise Impact of Labour Code Salary Rules

IT Sector and Startups: Maximum Impact Areas

The Indian IT and software services sector faces the highest structural disruption from the 50% wage rule. The industry has historically maintained very low basic pay ratios, sometimes in the range of 20 to 35% of CTC, to minimise statutory contributions and maximise take-home for employees who generally prefer this structure. NASSCOM has actively engaged with the government on the operational implications and related policy forums. Startups, particularly those with lean HR functions and complex ESOPs or variable pay structures, will need specialist legal and payroll advisory support to restructure compensation frameworks in compliance with the new rules.

Manufacturing and Contract Labour Compliance Impact

Manufacturing establishments and heavy industry, where wages are traditionally structured with a significant basic pay and DA component as per industry-level wage settlements, may face less disruption from the 50% wage rule. However, the 7th day payment deadline and the 48-hour FnF rule for contract workers present operational challenges in large factories with hundreds or thousands of contract workers on daily or weekly wage cycles. Compliance frameworks for contract staffing in 2026 are addressed in this guide at Voltech.

Gig and Platform Workers: Social Security Changes

The Code on Social Security 2020 includes, for the first time, a statutory framework for the social security of platform workers and gig workers employed through app-based platforms such as delivery, mobility, and home services aggregators. Platform aggregators above a specified size are required to contribute to a social security fund for their gig workers, covering health insurance, life insurance, and, in due course, provident fund-type benefits. The full implications for gig economy operators and workers are analysed in this guide.

Women Workforce Rules: Night Shift and Safety Compliance

The OSH Code 2020 introduces important provisions related to women workers, particularly around night shifts. Employers wishing to deploy women employees during night hours must obtain their consent, provide safe transportation to and from the workplace, and ensure adequate CCTV surveillance and other safety measures. These requirements add compliance costs but are designed to expand workforce participation by making night-shift employment safer and more accessible for women. Mandatory health checkup requirements under the new Labour Codes, including provisions benefiting women workers, are outlined in this guide.

Penalties and Compliance Risks Under Salary Payment Rules

Financial Penalties and Interest for Non-Compliance

The Code on Wages 2019 prescribes a tiered penalty structure. For violations related to non-payment, underpayment, or delayed payment of wages, the penalty for a first offence is a fine of up to Rs 50,000. For a second or subsequent offence within five years, the fine increases to up to Rs 1 lakh. Additionally, employers may be required to pay the unpaid or delayed wages along with interest at a rate to be notified. The full penalty structure and compliance guide are detailed in these guides by Bharat Payroll and Complinity.

Legal Consequences for Employers and HR Liability

Beyond financial penalties, repeated or egregious violations of the salary payment rules can attract criminal proceedings, including imprisonment of up to three months for responsible officers of the employer. Directors and HR heads who are shown to have been responsible for the default may face personal liability. The Jan Vishwas (Amendment of Provisions) Bill 2025, which decriminalised a range of minor regulatory offences across 16 central acts, has not decriminalised wilful wage theft or systematic non-payment of wages, which remain criminal matters.

Inspector-cum-Facilitator Mechanism Explained

One of the structural innovations in the Labour Codes is the replacement of the traditional Labour Inspector with an Inspector-cum-Facilitator. Under this model, officials must first act in a facilitative capacity, helping employers understand their obligations and correct non-compliant practices before invoking penal powers. Web-based inspections, randomised inspection allocation, and digital filing of inspection reports are also mandated to reduce opportunities for rent-seeking. The Government of India has explained this reform. Employers who engage proactively with compliance and maintain digital records are better positioned in the event of an inspection.

Digital Compliance, Wage Registers, and Filing Requirements

The Codes mandate the maintenance of wage registers, muster rolls, and other records in digital form and their submission through the Shram Suvidha Portal. Annual returns, previously filed separately under each of the 29 laws, are now consolidated into a single integrated filing. The India Briefing analysis details the new unified registration system for employers and the digital compliance architecture.

Employer Compliance Checklist for Labour Codes (2026)

Payroll Audit Checklist for 50% Wage Rule Compliance

The first step for every employer is a comprehensive payroll audit to calculate the current basic-to-CTC ratio for every employee, identify those whose current wage structure violates the 50% threshold, and model the PF, gratuity, and tax impact of restructuring. An authoritative payroll audit checklist for this exercise is available in this guide by Actax Corporate Strategies. The audit should also cover contract workers, fixed-term employees, and workers engaged through staffing agencies.

Upgrading HR and Payroll Systems for Compliance

Compliance with the 7th-day payment deadline and the 48-hour FnF rule requires payroll systems capable of processing both scheduled and off-cycle transactions in near real time. Employers still operating on legacy manual or spreadsheet-based payroll should prioritise migrating to compliant automated systems. The payroll compliance automation case is made in this analysis. Cloud-based HR and payroll platforms with built-in statutory compliance updates are recommended. An overview of payroll compliance for 2026 is available in this guide.

Implementing 48-Hour FnF Exit Processes

To achieve 48-hour FnF capability, employers need to redesign their exit management workflows end-to-end. This includes integrating leave management with payroll for automatic leave encashment calculation, setting up digital asset return and clearance checklists, enabling finance to process ad-hoc bank transfers outside the regular payroll cycle, and pre-computing gratuity eligibility so it can be triggered instantly on exit notification. The LoopHealth HR compliance checklist provides a structured walkthrough of the process changes required.

Reviewing Employment Contracts and Worker Classification

Employment contracts must be reviewed and updated to reflect the new wage definitions, payment timelines, and exit obligations. Special attention is needed for contracts with fixed-term workers to reflect the new gratuity eligibility and FnF obligations. Misclassification of workers as independent contractors to avoid Labour Code coverage is a growing risk area. The bizhrs.com compliance checklist and the myndsolution quick guide cover the contract review requirements in detail.

Digital Record-Keeping and Labour Law Filings

Employers must ensure their wage registers, attendance records, and FnF settlement documentation are maintained digitally and are accessible for inspection via the Shram Suvidha system. Annual integrated returns must be filed on time. The India Stack’s digital infrastructure, including its role in enabling digital compliance for labour laws is plays a key role here. The Direct Benefit Transfer infrastructure, used increasingly for wage disbursement to blue-collar workers, is explained in this guide.

When Will Salary Payment Rules Come Into Effect in India?

Labour Codes Rollout Timeline (2025–2026)

The four Labour Codes were made effective centrally from November 21, 2025, as confirmed by EY. Enforcement at the establishment level is now in effect for all employers covered by the central notification. For establishments in states where state-specific rules have also been notified, full legal enforcement is operative. Employers are advised to treat January 1, 2026, onwards as the definitive compliance start date and build their implementation plans accordingly.

State-Wise Labour Code Implementation Status

Labour is a concurrent subject under the Indian Constitution, meaning both central and state governments can legislate on it. The Labour Codes require both central and state rules to be operative for full implementation. Several states, including Uttar Pradesh, Madhya Pradesh, Rajasthan, Haryana, and Karnataka, had pre-notified draft rules. NASSCOM’s policy engagement tracker tracks the state-wise status of Labour Code rule notifications relevant to the IT and services sector. Employers with multi-state operations should monitor each state’s notification status separately.

What Employers Should Do Before State Notification?

Even in states where rules have not yet been fully notified, employers are advised to begin compliance preparations immediately. Running a payroll structure audit, modelling the financial impact, upgrading HR systems, and training HR and finance teams all take time and should not be deferred until the last moment. The Wire’s coverage summarises the key changes employers should be preparing for in 2026, regardless of state notification status.

Frequently Asked Questions (FAQ): Salary Payment Rules in India (2026)

The Code on Wages, 2019, standardizes the definition of wages to prevent artificially low basic pay structures.

Under this rule:

Basic Pay + Dearness Allowance (DA) + Retaining Allowance ≥ 50% of total CTC

If allowances (HRA, conveyance, special allowances) exceed 50%, the excess is added back to wages for calculating PF and gratuity

This ensures higher contributions toward statutory benefits and prevents wage structuring loopholes.

In many cases, yes.

Because the wage base must be at least 50% of CTC:

EPF contributions increase (since they are calculated on basic wages)

This leads to a reduction in monthly take-home pay

However, the trade-off is:

Higher retirement savings (PF corpus)

Increased gratuity benefits

Yes, this is now mandatory.

Under Section 17(2) of the Code on Wages:

Employers must complete Full and Final (FnF) settlement within 2 working days

Applies to resignation, termination, and retrenchment

This replaces the earlier industry norm of 30–45 day settlement cycles, making payroll compliance significantly stricter.

The new framework expands gratuity eligibility for Fixed-Term Employees (FTEs).

Earlier: Minimum 5 years of continuous service required

Now: Pro-rata gratuity after just 1 year of service

This change, introduced under the Code on Social Security, improves benefits for contract and short-term workers.

No. The law follows a tiered salary payment deadline:

Fewer than 1,000 employees → Salary by the 7th of the following month

1,000 or more employees → Salary by the 10th

This distinction accounts for larger payroll processing requirements.

Not for all employees.

Under the OSH&WC Code, 2020:

Employers must provide free annual health checkups

Applicable to employees above 40 years in specified establishments

This expands compliance beyond wages to include employee health and preventive care.

Salary Payment Rules and Payroll Compliance in India (2026)

The new salary payment rules under India’s four Labour Codes represent a genuine paradigm shift in the country’s employment law architecture. The 7th day payment deadline, the 48-hour FnF rule, and the 50% wage requirement are not marginal tweaks to existing law; they are structural changes that require employers to rethink their payroll operations, salary architectures, and HR systems from the ground up.

The financial stakes are substantial. KPMG’s analysis points to a potential 15 to 20% increase in labour costs for high-allowance-ratio employers. Balance sheet gratuity liabilities will require restatement. Take-home salaries may decline for a significant portion of the workforce as PF deductions rise.

Against these challenges, the regulatory environment also offers new protections: gig workers get social security coverage, women workers get enhanced night shift protections, and the Inspector-cum-Facilitator model reduces arbitrary enforcement.

For employers, the window for proactive preparation is open now. Payroll audits, salary restructuring, system upgrades, contract reviews, and employee communications should all be completed before enforcement actions begin. Resources such as the LoopHealth compliance checklist and the Cyril Amarchand Mangaldas guide provide detailed guidance. The Shram Suvidha portal is the central registration and compliance filing platform.

India’s payroll compliance era has changed permanently. The employers who adapt early, invest in the right systems, and engage proactively with the new regulatory framework will find that the Labour Codes ultimately create a more predictable, transparent, and professionally managed employment ecosystem, one that serves workers, employers, and the broader economy well.

Leave a Reply