Income Tax Act 2025: Key Changes Effective 1 April 2026

A Historic Shift in India’s Taxation Framework

For more than 60 years, India’s direct tax system rested on a single legislative foundation: the Income-tax Act, 1961. Over time, that statute became far more than a book of rules. It shaped how income was classified, how businesses were structured, how professionals built careers, and how citizens understood their financial obligations to the state. Its terminology entered everyday language. Before the introduction of the Income Tax Act 2025, sections were quoted by number alone. Entire advisory practices grew around navigating its complexity.

Yet the Act was also a product of its time. It was drafted for an economy that was smaller, slower, and far less interconnected. Over the decades, it was amended repeatedly to respond to new realities-liberalisation, globalisation, digitalisation, and the rise of entirely new forms of income. Each amendment addressed an immediate need, but collectively they produced a statute that was dense, layered, and increasingly difficult to read as a coherent whole.

That long legislative chapter is now ending. The Income Tax Act, 2025, replaces the Income-tax Act, 1961, in its entirety. This is not a selective clean-up or a consolidation exercise. It is a deliberate attempt to rethink how income taxation should function in a modern, high-volume, technology-driven economy. Instead of building on the old structure, the new law starts fresh, retaining policy intent where necessary but reworking language, structure, and administration from the ground up.

The Income Tax (No. 2) Bill, 2025, has already received parliamentary approval and will come into force on April 1, 2026. From that date onward, all assessments, filings, enforcement actions, and dispute resolution processes will be governed by the new statute. The full text of the law, as notified in the official gazette, makes it clear that this is not a cosmetic rewrite. Provisions have been renumbered, long-standing concepts reframed, and procedural mechanics redesigned to align with how compliance actually works today.

The government’s stated objectives behind this reform have been consistent across budget speeches, explanatory memoranda, and parliamentary debates. The emphasis is on simplifying tax law, reducing unnecessary litigation, improving certainty, and lowering the cost of compliance for both taxpayers and administrators. When Finance Minister Nirmala Sitharaman introduced the Bill in the Lok Sabha, coverage by the national media highlighted her description of the new Act as a move toward a “trust-based, technology-driven tax administration.” That framing is central to understanding the philosophy of the law.

This shift matters because the profile of India’s taxpayers has changed dramatically. The income-tax system is no longer dealing with a relatively small, formal segment of the population. More than 140 million individuals now file income-tax returns. The taxpayer base includes salaried employees, freelancers, gig workers, consultants, small traders, start-up founders, and investors in digital assets. Many of these taxpayers engage with the system without regular professional support and rely heavily on online platforms and simplified guidance.

Under these conditions, a law built around dense cross-references, multiple provisos, and layered explanations creates friction. Even when taxpayers want to comply, understanding what applies to them can be difficult. The Income Tax Act, 2025, attempts to respond to this reality directly. Its language is more straightforward, its structure more linear, and its assumptions are grounded in widespread voluntary compliance rather than constant enforcement pressure.

At the same time, simplification does not mean dilution. The new law strengthens the state’s ability to track income flows in a digital economy. It recognises that modern income is often fragmented across platforms, accounts, and jurisdictions, and it equips tax authorities with tools to address that complexity. The balance the Act seeks to strike is clear: make compliance easier for honest taxpayers, while improving the system’s ability to detect and address deliberate non-compliance.

This guide is intended to unpack the Income Tax Act, 2025, in practical terms. Rather than treating it as a purely technical or legal document, it focuses on how the new framework will operate in real life once April 2026 arrives. It examines what has changed, why those changes matter, and how different groups-individual taxpayers, businesses, professionals, and students-should prepare for the transition.

Each section looks at a specific dimension of the new law, from structural redesign and terminology changes to personal taxation, administrative simplification, digital asset regulation, and professional transition timelines. The objective is not to overwhelm, but to provide clarity so that readers can understand not just what the law says, but what it means for them in practice.

Structural Overhaul in the Income Tax Act 2025

Fewer Sections and Consolidated Provisions

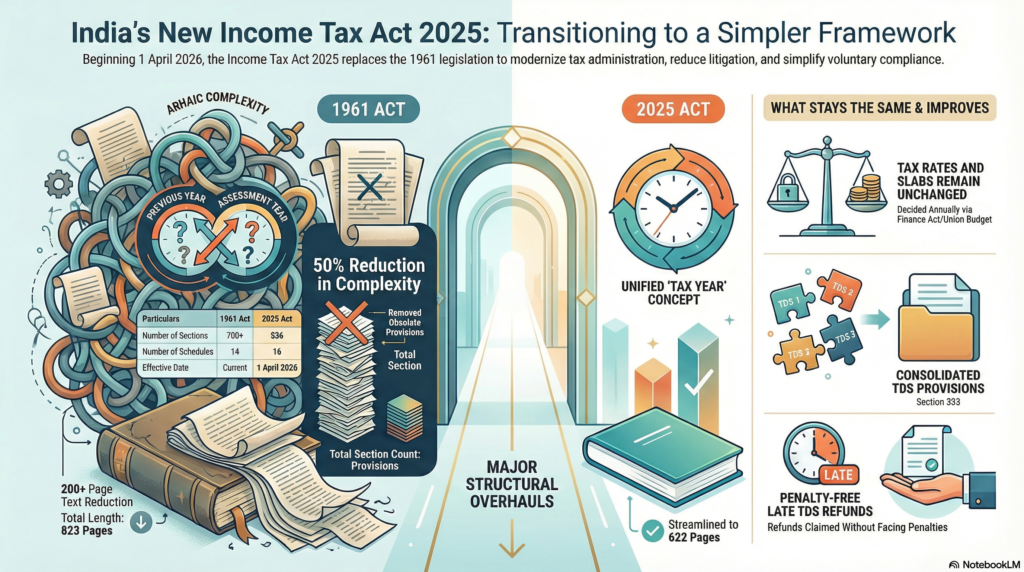

One of the first things that stands out when reading the Income Tax Act, 2025, is how much lighter and more deliberate it feels compared to its predecessor. This is not a matter of formatting or presentation alone. The new law is almost half the length of the Income-tax Act, 1961, a change that reflects years of accumulated frustration with a statute that had grown dense through constant amendment rather than intentional redesign.

Under the earlier framework, complexity was often the by-product of necessity. Each Finance Act responded to emerging economic realities-new financial instruments, new business structures, new compliance priorities. Over time, however, these responses stacked on top of one another. Provisions were inserted rather than rewritten. Explanations were added instead of simplifying the core language. Entire sections became dependent on chains of provisos that only made sense when read together.

The Income Tax Act, 2025, takes a different approach. Instead of attempting to preserve every legacy formulation, it strips the law back to its essentials and rebuilds it in a more linear, readable form. The reduction in length does not signal fewer obligations or weaker enforcement. Rather, it reflects the removal of duplication, outdated references, and explanatory clutter that no longer serve a practical purpose.

This structural rethink becomes clearer when viewed numerically. The Income-tax Act, 1961, eventually expanded to well over 700 sections. Many of these provisions overlapped in scope, addressed similar transactions, or existed largely to clarify the effect of earlier amendments. The new framework brings this down to 536 sections. As noted in detailed commentary published by Taxmann, this reduction was achieved by consolidating related provisions and rewriting them in direct, operational language rather than legal shorthand.

Also Read: India DBT Reforms: ₹3.48 Lakh Crore Savings and 0.91 WEI Score Explained (2026)

Sequential Numbering and Improved Readability

Equally important is how the new Act is meant to be read. The old law often required readers to jump across chapters and explanations to understand a single obligation. Definitions were scattered. Exceptions were buried in footnote-style provisos. The 2025 Act aims to ensure that most provisions can be understood on their own, without constant cross-referencing. This matters not only for individual taxpayers, but also for professionals, administrators, and software systems that rely on predictable statutory logic.

Another significant change is the abandonment of alphabet-heavy section numbering. Under the 1961 Act, provisions such as 80C, 80CCD(1), and 80CCD(1B) became familiar to professionals but intimidating to non-specialists. For taxpayers without regular advisory support, remembering which variant applied often felt like a test of memory rather than understanding. The new Act replaces this system with simple sequential numbering across the statute.

This change may appear cosmetic, but its practical impact is substantial. Most taxpayers now interact with the law through digital portals, automated return-filing systems, and online guidance. Sequential numbering improves searchability, reduces misinterpretation, and lowers the cognitive barrier to engaging with the statute directly. It also simplifies updates to compliance software, which previously had to accommodate multiple lettered subsections and overlapping references.

The policy intent behind this redesign is explicitly stated in the Budget Memorandum accompanying the Bill. The government draws a direct connection between clearer drafting, reduced compliance costs, and lower litigation. Ambiguity has historically been one of the biggest drivers of tax disputes. When provisions are difficult to interpret, even good-faith compliance can result in disagreements over meaning rather than substance.

By tightening language and structure, the new Act attempts to reduce interpretational friction. This does not eliminate disputes entirely-no tax system can- but it shifts the focus away from semantic arguments and toward substantive issues of income recognition and disclosure. Over time, this is expected to ease pressure on appellate forums and reduce the volume of litigation that arises purely from unclear drafting.

There is also an administrative dimension to this overhaul. Tax authorities operate under the same statute as taxpayers. Clearer provisions reduce discretion at the implementation stage, leading to more uniform application across jurisdictions. This consistency is particularly important in a faceless and digitised tax administration, where automated systems rely on precise statutory triggers rather than subjective judgment.

In effect, the structural overhaul of the Income Tax Act, 2025, is not about making the law shorter for its own sake. It is about making the law usable—by taxpayers trying to comply, by professionals advising clients, and by administrators enforcing it at scale. Whether this objective is fully realised will depend on implementation, but the legislative intent is unmistakable.

Unified Tax Year Reform Under the Income Tax Act 2025

Replacing Previous Year and Assessment Year

For decades, one of the least intuitive features of India’s income-tax system was the distinction between the “Previous Year” and the “Assessment Year.” While the logic behind this separation was well understood by tax professionals, it routinely confused individual taxpayers. Income was earned in one year, assessed in another, and referred to in notices and forms using terminology that did not always align with how people thought about their finances.

This confusion was not merely academic. Taxpayers often struggled to identify which year applied when responding to notices, planning investments, or even checking whether a particular provision was in force for a given transaction. The need to mentally map income years to assessment years added an unnecessary layer of complexity to an already demanding compliance process.

The Income Tax Act, 2025, addresses this long-standing issue by replacing the dual-year framework with a single, unified concept: the Tax Year. Under the new law, the Tax Year is defined as the twelve-month financial period beginning on April 1 and ending on March 31, during which income is earned. There is no parallel label, no secondary definition, and no interpretational gap. Income belongs to the year in which it is earned.

Practical Impact on Filing and Planning

This change does not alter the underlying mechanics of compliance. Returns are still filed after the close of the financial year, and assessments continue to take place later. What changes is how these stages are described. The year in which returns are filed, assessments are completed, and notices are issued is now referred to as the Succeeding Tax Year. The practical time gap remains intact, but the language is cleaner and more intuitive.

To illustrate how this works in practice, income earned between April 1, 2026, and March 31, 202,7 will fall under Tax Year 2026–27. The return for that income will be filed during the Succeeding Tax Year, 2027–28. For taxpayers accustomed to aligning their finances with the financial year, this approach feels more natural and eliminates the need for constant translation between concepts.

The benefits of this change extend beyond individual understanding. From an administrative perspective, a unified Tax Year simplifies the design of forms, notices, and digital interfaces. It reduces the scope for mismatches and clerical errors, particularly in automated systems where incorrect year selection has historically been a common cause of defects and follow-up communication.

This realignment also improves tax planning clarity. When provisions, rates, and exemptions are tied directly to the year in which income is earned, taxpayers can make more informed decisions without worrying about transitional overlaps. This is especially relevant during periods of legislative change, where confusion about applicability dates often leads to disputes or inadvertent non-compliance.

For professionals, the unified Tax Year reduces explanatory friction with clients. Concepts that once required careful clarification can now be explained in straightforward terms. This does not diminish the need for professional advice, but it allows that advice to focus on substantive planning rather than decoding terminology.

In effect, the move to a unified Tax Year reflects a broader design philosophy of the Income Tax Act, 2025. The law seeks to align statutory language with how taxpayers naturally think about time, income, and compliance. While the change may appear modest on paper, its cumulative impact on clarity, communication, and ease of compliance is likely to be significant.

Personal Tax Changes Under Income Tax Act 2025

Clause 202 and the Default Tax Regime

One of the most consequential changes introduced by the Income Tax Act, 2025, is the formal elevation of the New Tax Regime as the default system for individual taxpayers and Hindu Undivided Families. What was initially introduced as an optional alternative has now been repositioned as the standard framework. This shift is not accidental. It reflects a deliberate policy choice to move India’s personal income-tax system away from exemption-heavy complexity toward a structure based on lower rates and simpler compliance.

Clause 202 anchors this transition. By placing the default regime at the centre of personal taxation, the Act signals that the government no longer expects the average taxpayer to navigate a dense web of deductions, exemptions, and conditional benefits. Instead, the emphasis is on predictability, ease of filing, and reduced documentation. The law is designed on the assumption that simplicity itself is a form of relief.

The Clause 202 tax slabs applicable from Tax Year 2026–27 establish a gradual progression of rates. Income up to ₹3,00,000 attracts no tax. Income between ₹3,00,001 and ₹7,00,000 is taxed at 5%. This is followed by a 10% rate on income up to ₹10,00,000, 15% on income up to ₹12,00,000, 20% on income up to ₹15,00,000, and 30% on income exceeding that threshold. Read in isolation, these slabs appear familiar. Their real impact becomes evident when considered alongside the revised rebate and deduction framework.

The enhanced Section 87A rebate plays a central role in reshaping tax outcomes for middle-income earners. Under the new Act, resident individuals with total income up to ₹12 lakh effectively face zero tax liability under the default regime. This is not a symbolic benefit. It materially changes the tax position of a wide segment of salaried and self-employed taxpayers who previously paid tax despite relatively modest incomes.

For salaried individuals, the impact is even more pronounced due to the increased standard deduction of ₹75,000. This raises the effective zero-tax threshold to ₹12.75 lakh. In practical terms, a salaried employee earning up to this amount can discharge their entire tax liability without claiming a single exemption or deduction beyond the standard allowance. This represents a marked departure from the earlier approach, where tax planning often revolved around investment-linked deductions and employer-specific allowances.

Illustrative calculations published by ClearTax demonstrate how these provisions operate in real-world scenarios. In many cases, taxpayers with incomes slightly above the zero-tax threshold still benefit from a smoother marginal tax curve compared to the old regime. The result is less volatility in take-home income as earnings rise.

Importantly, the option to choose the old regime has not been eliminated. Taxpayers who continue to benefit from deductions related to housing loans, insurance premiums, provident fund contributions, or specific exemptions may still find the older structure advantageous. However, the burden of choice now shifts in practice. The default position is simplicity, and opting out requires an affirmative decision.

This design choice carries behavioural implications. Over time, fewer taxpayers may feel compelled to engage in tax-driven financial planning solely to minimise liability. Instead, investment decisions can be guided more by financial goals than by deduction eligibility. From an administrative standpoint, this also reduces the volume of documentation and verification required during assessments.

The dominance of the default regime reflects a broader philosophical shift in personal taxation. Rather than incentivising specific behaviours through a complex lattice of deductions, the Income Tax Act, 2025, prioritises transparency and ease. Whether this approach ultimately broadens the tax base or reshapes household savings patterns will become clearer over time, but its immediate effect on compliance simplicity is undeniable.

Administrative Reforms Under the Income Tax Act 2025

TDS Consolidation Under Section 393

For employers, banks, financial institutions, and businesses that routinely deduct tax at source, the Income Tax Act, 2025, introduces one of its most operationally significant reforms through the consolidation of TDS provisions under Section 393. While this change does not alter the underlying tax policy or applicable rates, it fundamentally improves how deductors interact with the law on a day-to-day basis.

Under the Income-tax Act, 1961, TDS obligations were scattered across a wide range of sections. Each category of payment—salary, interest, professional fees, commission, rent, contractual payments—was governed by its own provision, often with separate thresholds, exceptions, and explanatory notes. For deductors handling multiple payment streams, compliance involved constant cross-referencing and the risk of overlooking a relevant condition or update.

The new Act addresses this fragmentation by bringing all TDS-related provisions into a single consolidated section. Section 393 functions as a unified framework that sets out the principles, applicability, and operational mechanics of tax deduction at source. While specific rates and thresholds continue to be notified through schedules and rules, the statutory backbone is now located in one place.

Crucially, the government has chosen not to disrupt existing practice during the transition. The TDS rates FY 2025-26 remain unchanged. This ensures that deductors are not required to recalibrate systems or renegotiate contracts purely because of the legislative rewrite. Stability during the shift to a new statute reduces the risk of compliance errors in the first year of implementation.

The real benefit of consolidation lies in accessibility. Employers processing payroll, companies paying professional fees, and banks crediting interest income often operate under strict timelines. When TDS provisions are scattered, even minor ambiguities can delay processing or trigger conservative over-deduction to avoid penalties. A single, coherent statutory framework reduces this friction and improves confidence in compliance decisions.

From an organisational perspective, this change also simplifies internal training and controls. Compliance teams can rely on a central provision rather than maintaining fragmented reference materials. Over time, this reduces dependency on ad hoc interpretations and minimises variation in how TDS rules are applied across branches or departments.

According to KPMG’s India Tax Highlights, large organisations managing diverse payment obligations are likely to see measurable reductions in time spent on TDS compliance. These efficiency gains may appear incremental on a monthly basis, but over an entire financial year, they translate into lower administrative costs and fewer disputes arising from inadvertent non-compliance.

The consolidation also supports the broader move toward automated and faceless tax administration. When statutory logic is centralised and consistent, it is easier to embed into payroll software, banking systems, and compliance platforms. This reduces manual intervention and the scope for human error, both of which have historically contributed to mismatches between deductors’ filings and recipients’ returns.

It is important to note that consolidation does not dilute responsibility. Deductors remain accountable for the timely deduction, deposit, and reporting of TDS. Penalties for failure to comply continue to apply. What changes is the ease with which deductors can identify their obligations and meet them accurately.

In effect, Section 393 reflects the broader philosophy of the Income Tax Act, 2025. Rather than changing what is taxed or how much is collected, the law focuses on making compliance more straightforward. For entities that interact with the tax system at scale, this shift from fragmentation to coherence may prove to be one of the most practically beneficial reforms in the new statute.

Digital Asset Taxation and Enforcement Framework

Expanded Definition of Virtual Digital Assets

The rapid rise of cryptocurrencies, tokenised instruments, and blockchain-based transactions has posed a challenge for tax systems across the world. Income and wealth that once moved through easily traceable banking channels can now be stored, transferred, and traded across decentralised networks with minimal friction. The Income Tax Act, 2025, responds to this reality by explicitly bringing Virtual Digital Assets within a clearer and more comprehensive statutory framework.

The new Act expands the definition of Virtual Digital Assets to expressly include cryptocurrencies, non-fungible tokens, and any asset recorded, transferred, or stored using cryptographic methods or distributed ledger technology. By spelling this out in the statute itself, the law removes lingering ambiguity about whether newer digital instruments fall within the tax net. For taxpayers, this clarity reduces interpretational risk. For the administration, it closes gaps that previously allowed arguments over classification rather than disclosure.

While the scope of what constitutes a Virtual Digital Asset has been clarified, the tax treatment remains deliberately stringent. Transfers of such assets continue to attract a flat 30% tax on crypto transfers, with no allowance for deductions other than the cost of acquisition. Losses arising from these transactions cannot be set off against other income or carried forward. This approach reflects the government’s continued caution toward speculative digital assets, even as it acknowledges their growing role in investment portfolios.

From a compliance standpoint, this continuity is significant. Taxpayers already engaged in digital asset transactions are not being asked to relearn the tax outcome. Instead, they are being placed within a firmer statutory framework that leaves little room for interpretational manoeuvring. The message is clear: participation in digital markets does not place income outside the scope of taxation.

Clause 247 and Access to Virtual Digital Space

The most debated aspect of the new digital framework, however, lies not in rates but in enforcement powers. Clause 247 introduces the concept of access to the “Virtual Digital Space” during tax investigations. This term is defined broadly enough to include emails, cloud storage accounts, digital wallets, online trading accounts, and other electronically stored data. In effect, it recognises that modern financial records often exist entirely in digital form.

Legal commentary and professional analysis, including discussion in regulatory bulletins, have raised concerns about the breadth of this power. Critics argue that the definition of virtual digital space is wide enough to potentially capture personal communications and data unrelated to tax matters. The fear is not theoretical. In a digital-first environment, financial and personal data often coexist on the same platforms.

Supporters of the provision counter that traditional search and seizure tools are no longer adequate in a world where wealth can be concealed behind passwords and encrypted wallets. From this perspective, access to digital records is not an expansion of power so much as a necessary adaptation. Without it, enforcement risks falling behind the realities of how income and assets are held.

The Act attempts to balance these competing concerns through procedural safeguards. Authorisation for such searches is required from senior officers, and the powers are framed within existing investigative protocols. However, as with many enforcement provisions, the real test will lie in how these powers are exercised in practice. Judicial interpretation and administrative guidance will play a critical role in defining the boundaries between legitimate investigation and intrusion into privacy.

For taxpayers engaged in digital asset activity, this section of the Act underscores the importance of record-keeping and transparency. Informal practices that may have seemed acceptable in the early days of cryptocurrency trading carry a higher risk under a regime that explicitly recognises and regulates digital spaces. Clear documentation, accurate reporting, and awareness of compliance obligations become essential.

In a broader sense, the treatment of Virtual Digital Assets under the Income Tax Act, 2025 reflects a dual intent. The law seeks to modernise oversight mechanisms to keep pace with technological change, while also signalling restraint by maintaining a consistent tax policy rather than reacting with frequent rate or rule changes. How effectively this balance is maintained will shape taxpayer confidence in the digital tax framework over the coming years.

Compliance Philosophy Shift in the Income Tax Act 2025

Decriminalisation and Trust-Based Governance

One of the most significant, though less immediately visible, shifts introduced by the Income Tax Act, 2025 lies in how the law treats non-compliance. Rather than focusing solely on rates, slabs, or procedural mechanics, the new Act re-examines the underlying philosophy of enforcement. In doing so, it marks a clear move away from a punitive default approach toward one grounded in proportionality and trust.

Under the earlier framework, a wide range of procedural and technical lapses carried the risk of criminal prosecution. Delays in filing certain documents, failures to maintain prescribed records, or non-responsiveness to notices could, in some circumstances, expose taxpayers to criminal liability. While such provisions were intended as deterrents, in practice, they often created anxiety and adversarial engagement, particularly for small businesses and individual taxpayers acting in good faith.

The Income Tax Act, 2025, draws a clearer line between deliberate evasion and procedural error. Technical and compliance-related defaults are now primarily addressed through financial penalties rather than imprisonment. Criminal sanctions are reserved for cases involving wilful evasion, fraud, or intentional concealment of income. This distinction reshapes the tone of enforcement. It recognises that errors can arise from complexity or misunderstanding rather than intent.

This change has practical implications for taxpayer behaviour. When the consequence of a mistake is correction and penalty rather than prosecution, taxpayers are more likely to engage proactively with the system. The fear-driven compliance that characterised parts of the earlier regime is replaced with an expectation of cooperation. Over time, this can improve disclosure quality and reduce the volume of disputes that arise from defensive filing practices.

The move toward decriminalisation aligns with the broader idea of trust-based governance, a theme that runs through several aspects of the new Act. The assumption is that most taxpayers seek to comply if the rules are clear and the consequences proportionate. Enforcement resources can then be focused on cases where there is evidence of intentional wrongdoing rather than spread thin across minor lapses.

Professional analysis from EY India suggests that this approach could lead to a reduction in adversarial proceedings and an improvement in long-term compliance behaviour. By lowering the stakes for genuine mistakes, the system encourages early correction and voluntary disclosure.

This philosophical shift is reinforced by the continued expansion of faceless tax administration. Assessments, appeals, and penalty proceedings increasingly take place through digital platforms, reducing discretionary interaction between taxpayers and tax officers. When combined with clearer statutory language, this reduces the perception of arbitrary enforcement and improves consistency across cases.

The updated return mechanism under Section 267 fits squarely within this framework. Taxpayers are given an extended window to revise returns and correct omissions or errors without immediately triggering punitive consequences. This reinforces the idea that the system values accuracy and cooperation over punishment for honest mistakes.

It is important to note that trust-based governance does not imply leniency toward evasion. The Act strengthens investigative and data-matching capabilities, particularly in a digital economy. The difference lies in how the law distinguishes between error and intent. Where non-compliance is deliberate, enforcement remains firm. Where it is inadvertent, the response is corrective.

Taken together, these changes represent a meaningful recalibration of the taxpayer–state relationship. The Income Tax Act, 2025, signals that compliance is a shared responsibility rather than a contest of avoidance and enforcement. Whether this cultural shift fully takes root will depend on consistent application, but the legislative intent is clear.

Professional and Student Transition to the New Tax Law

ICAI Timeline for CA Examinations

A legislative overhaul of this magnitude inevitably raises concerns among students and professionals whose education, examinations, and day-to-day practice are closely tied to the existing legal framework. Recognising this, the Institute of Chartered Accountants of India has adopted a measured and structured approach to the transition from the Income-tax Act, 1961, to the Income Tax Act, 2025. The objective is to ensure continuity, fairness, and adequate preparation time rather than abrupt disruption.

The official guidance issued by ICAI provides much-needed clarity on how and when the new law will be introduced into the Chartered Accountancy examination syllabus. Under this framework, all CA examinations conducted up to January 2027, including the November 2026 attempt, will continue to be based on the Income-tax Act, 1961. This decision acknowledges that many students are already well advanced in their preparation and should not be forced to pivot mid-stream.

This transition window is particularly important given the scale of change involved. The new Act is not merely a renumbered version of the old law. Its structure, terminology, and conceptual organisation differ in material ways. Introducing it too quickly into examinations could have created confusion and placed students at an unfair disadvantage.

The first examinations to be conducted under the Income Tax Act, 2025, will be the May/June 2027 attempts. From that point onward, CA Intermediate and CA Final candidates will be examined on the new law through the revised Paper 3A Income-tax Law syllabus. This timeline provides a buffer of roughly sixteen months from the Act’s effective date of April 1, 2026, allowing sufficient time for updated study material, practice manuals, and revision resources to be developed and absorbed.

For coaching institutions, authors, and publishers, this phased approach enables orderly curriculum updates rather than rushed revisions. For students, it allows preparation to proceed with certainty, without the risk of last-minute syllabus changes or overlapping applicability.

Practising Chartered Accountants face a different, though related, transition. The statutory authority to conduct tax audits continues to rest exclusively with CAs, and this position remains unchanged under the new Act. What will evolve is the application of the law in practice. Professionals will need to familiarise themselves with new section numbers, revised terminology, and altered procedural flows.

While the initial learning curve may be steep, many professionals anticipate that the simplified structure and clearer drafting will reduce effort over time. Tasks that previously required extensive cross-referencing may become more straightforward once familiarity sets in. This has implications not only for efficiency, but also for how professionals communicate tax concepts to clients.

The ICAI transition plan also reflects an awareness of the profession’s role in stabilising the system during periods of change. By ensuring that future professionals are examined under a clear and settled framework, the Institute supports consistent interpretation and application of the law in its early years.

Overall, the approach taken toward student and professional transition underscores the broader philosophy of the Income Tax Act, 2025. Reform is being implemented with an emphasis on predictability and preparedness rather than shock. For those entering the profession and those already practising, the transition period offers time to adapt, learn, and ultimately benefit from a more coherent statutory framework.

What the Income Tax Act 2025 Means for India’s Tax Future

The Income Tax Act, 2025, is more than a routine legislative update. It represents a deliberate reset in how taxation is conceptualised, communicated, and enforced in India. By replacing a statute that had grown layered over six decades, the government has signalled that complexity is no longer an acceptable by-product of tax administration. Clarity, predictability, and usability are now treated as core design principles rather than secondary considerations.

At a structural level, the reduction to 536 sections, the elimination of alphabet-heavy numbering, and the adoption of clearer drafting standards address long-standing pain points for both taxpayers and professionals. These changes may not alter tax liability on their own, but they materially affect how easily obligations can be understood and met. When the law itself is easier to navigate, compliance becomes less intimidating and disputes rooted in interpretation become less frequent.

The introduction of the unified Tax Year further reinforces this shift toward intuitive design. By aligning statutory language with how taxpayers naturally think about income and time, the new framework removes an unnecessary cognitive barrier that existed for decades. This alignment may appear modest in isolation, but across millions of taxpayers and interactions, it has the potential to significantly reduce confusion and error.

For individual taxpayers, the dominance of the default tax regime reshapes the personal taxation landscape. The combination of lower rates, an enhanced Section 87A rebate, and a higher standard deduction simplifies filing for a large segment of the population. While the option to choose the old regime remains, the policy signal is clear: simplicity is no longer the alternative—it is the norm. Over time, this may also influence how households approach savings and investments, shifting the focus away from tax-driven decisions.

From an administrative and business perspective, consolidation of provisions such as TDS under Section 393 reflects a practical understanding of compliance at scale. When obligations are easier to locate and apply, the risk of inadvertent error declines. This benefits not only deductors but also the tax system as a whole by reducing mismatches, notices, and avoidable disputes.

The Act’s treatment of Virtual Digital Assets and its expanded enforcement powers illustrate a parallel priority: keeping pace with how income and wealth are created in a digital economy. While concerns around privacy and scope are legitimate, the statutory recognition of digital spaces acknowledges that traditional tools are no longer sufficient. The balance between effective enforcement and individual rights will evolve through implementation and judicial interpretation, but the direction of travel is unmistakable.

Perhaps the most significant shift lies in the law’s compliance philosophy. The move toward decriminalisation and trust-based governance marks a change in tone as much as in substance. By distinguishing between deliberate evasion and procedural error, the Act encourages engagement rather than avoidance. Faceless administration, extended correction windows, and proportional penalties together reshape the taxpayer–state relationship from one of suspicion to one of conditional trust.

As India advances toward its long-term development vision, articulated through initiatives such as Viksit Bharat @2047 and reinforced in official communications, the Income Tax Act, 2025, stands out as a foundational reform. A modern economy requires a tax system that is not only effective in revenue collection but also credible, comprehensible, and fair in its operation.

The transition period leading up to April 1, 2026, offers taxpayers, businesses, students, and professionals a valuable window to familiarise themselves with the new framework. Those who invest time now in understanding its structure and intent are likely to find compliance smoother and planning more predictable in the years ahead.

Ultimately, the success of the Income Tax Act, 2025, will not be measured solely by revenue outcomes. It will be judged by whether it reduces friction, builds trust, and supports economic participation at scale. In that sense, the Act is not just a change in law, but a statement about how the Indian state intends to interact with its taxpayers in the decades leading up to 2047 and beyond.

[…] Income Tax Act, 2025, notified to come into force from April 1, 2026, is meant to be a structural reset, not a cosmetic […]