Tax Year under Income Tax Act 2025: Replaces Assessment and Previous Year

Income Tax Act 2025 and the Shift to a Unified Tax Year

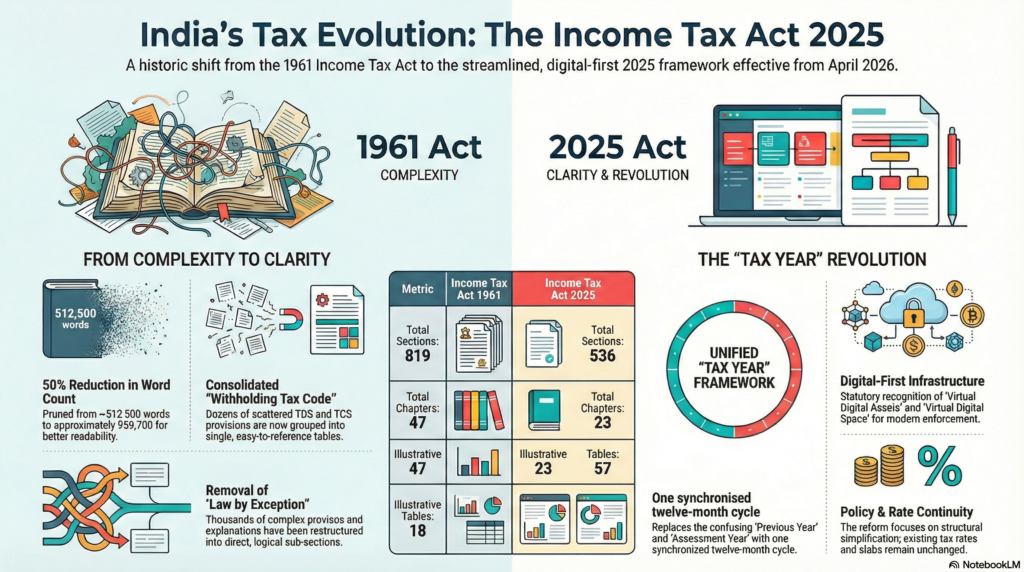

For more than six decades, Indian taxpayers have lived with the Income Tax Act, 1961, a law that began its life fairly lean but slowly, almost quietly, grew into something massive. Over 4,000 amendments later, it now runs to about 5.12 lakh words, a scale that has been widely acknowledged in professional and media analyses.

That kind of growth doesn’t happen without consequences. For taxpayers, it meant confusion. For professionals, constant reinterpretation. For administrators, a law that was technically sound but increasingly hard to operate smoothly. Even official government material has admitted that the 1961 Act had become cluttered and difficult to navigate in practice.

The Income Tax Act, 2025, notified to come into force from April 1, 2026, is meant to be a structural reset, not a cosmetic edit. Its notification in the Gazette of India makes clear that this is a full repeal-and-replace exercise, not another round of patchwork amendments.

At the centre of this overhaul sits a change that sounds almost too simple to matter: the introduction of a unified “Tax Year.” Yet this single shift addresses one of the most persistent pain points in Indian tax compliance, the coexistence of the “Previous Year” and the “Assessment Year.”

For years, taxpayers have earned income in one year and reported it in another, a structure that required mental bookkeeping even before actual bookkeeping began. You earned income in one period, but the law spoke to you in the language of a different year altogether. The Income Tax Act, 2025, collapses this duality into a single timeline, a move that has been repeatedly highlighted in legislative tracking and policy reviews

This change is also part of a broader policy narrative. Policymakers have described the new Act as a stepping stone toward Viksit Bharat 2047, a developed India by the centenary of independence. That framing may sound aspirational, but the mechanics underneath are practical: fewer concepts, clearer timelines, and less room for basic misunderstanding.

In this series of sections, we will unpack what the Tax Year actually means, why it was introduced, and how it changes everyday tax compliance. Whether you are a salaried employee filing a straightforward return or a professional advising clients, this shift will touch your workflow. And it’s worth understanding properly, before April 1, 2026, arrives.

Why the Income Tax Act 2025 Replaces Assessment Year and Previous Year

To really understand why the Tax Year matters, you have to step back and look at what the Income Tax Act, 1961 had become over time. It didn’t start off unwieldy. In fact, in its early years, it was relatively compact and navigable. But decades of economic change, judicial interpretation, policy experimentation, and political compromise slowly transformed it into something far denser.

Every Union Budget brought amendments. Court rulings demanded clarifications. New business models, especially digital ones, forced fresh provisions. Each change made sense in isolation. Together, they created a statute that crossed 800 sections and expanded to more than 5.12 lakh words, a scale that even official government documents have openly acknowledged as excessive.

Professional bodies were not quiet about this either. The Institute of Chartered Accountants of India (ICAI), among others, repeatedly pointed out that the Act had become difficult to apply consistently, especially for smaller taxpayers and first-time filers. When even trained professionals need frequent updates just to keep track of what changed last year, something is clearly off.

This concern was formally echoed during the legislative review process. The Parliamentary Select Committee examining the Income Tax Bill, 2025 noted that the 1961 Act had become cluttered and hard to navigate, even for seasoned practitioners, and that simplification, not incremental amendment, was the only realistic solution.

The Dual-Year Confusion: Previous Year vs Assessment Year Explained

Among all the layers of complexity, one feature consistently confused taxpayers more than any other: the coexistence of the Previous Year and the Assessment Year.

Under the old framework, income earned between April 1 and March 31 was classified as income of a particular Financial Year (also called the Previous Year). But the tax return for that income was filed in the following year, known as the Assessment Year. For example, income earned in FY 2025-26 was assessed in AY 2026-27, a structure explained repeatedly in taxpayer guides and explainer articles over the years.

For experienced taxpayers, this was eventually manageable. For newcomers, it was a recurring source of confusion. A common question was almost always the same: Why is the year I’m filing for different from the year I earned the income? The terminology felt abstract, and the logic was not immediately obvious.

Historically, the reasoning was administrative. The tax department needed time after the financial year ended to collect returns, verify information, and conduct assessments. But that justification started to lose force in a world where returns are filed electronically, processed algorithmically, and assessed through faceless systems. As of recent years, over 99% of returns are e-filed, a fact repeatedly highlighted in official releases and budget documents (see CBDT and PIB communications.

The Tax Year concept directly addresses this mismatch between how the system evolved and how the law continued to speak. By replacing the dual-year structure with a single primary reference point, the Income Tax Act, 2025 removes a layer of mental translation that never really added value for the taxpayer.

Instead of earning income in one year and mentally shifting gears to file in another, the law now speaks in one timeline. The filing still happens later, but the conceptual anchor-the Tax Year-remains the same. That small change does a surprising amount of heavy lifting when it comes to clarity.

What Is the Tax Year? Definition Under Section 3 of the Income Tax Act 2025

With all the background noise stripped away, the definition of the Tax Year itself is almost startlingly simple. Under Section 3 of the Income Tax Act, 2025, a “Tax Year” is defined as a period of 12 months beginning on April 1 and ending on March 31. There is no parallel terminology and no secondary labels doing quiet work in the background. This definition appears clearly in the text of the Bill and its accompanying explanations.

In practical terms, this means:

• Tax Year 2026-27 runs from April 1, 2026, to March 31, 2027

• Tax Year 2027-28 runs from April 1, 2027, to March 31, 2028

What changes is not the calendar itself, we were already living from April to March, but the role that this period plays in the law. The Tax Year is now the single reference point for both earning income and determining the tax rates applicable to that income. This alignment has been highlighted repeatedly in professional analyses, including PwC’s summaries of significant developments under the new Act.

Under the old system, there was a subtle but important disconnect. You earned income in the Previous Year, but the tax rates that applied were technically those enacted for the Assessment Year. For most taxpayers, this distinction lived quietly in the background, but it mattered when rates changed, deductions were tweaked, or transitional provisions applied. The Tax Year removes that disconnect by design.

Financial Year vs Assessment Year vs Tax Year: Key Differences

The contrast between the old and new systems becomes clearer when placed side by side.

Under the Income Tax Act, 1961, the structure looked like this:

• The Financial Year (FY) ran from April 1 to March 31 and represented the period during which income was earned.

• The Previous Year was effectively the same period, but only for tax terminology purposes.

• The Assessment Year (AY) was the year immediately following the Financial Year, during which that income was assessed and taxed.

This layered terminology has been explained countless times in taxpayer education material over the years.

Under the Income Tax Act, 2025, the framework is flatter:

• The Tax Year (April 1 to March 31) is the period during which income is earned and the period whose rates apply to that income.

• The Subsequent Tax Year is simply the next Tax Year, during which the return is filed.

This shift has been illustrated in multiple side-by-side comparisons published by tax platforms and advisory firms.

The practical benefit here is cognitive. Instead of translating between FY and AY every time you file, you think in one timeline: I earned income in Tax Year X, and I will file for it in the following Tax Year. It’s not dramatic. It’s just cleaner, and in compliance work, clean usually means fewer mistakes.

Charging Section Simplified: How the Tax Year Aligns the Basis of Charge

The real-world impact of the Tax Year concept becomes clearest when you look at the charging provision, the part of the law that actually gives the government the authority to levy income tax. Under the Income Tax Act, 1961, this role was played by Section 4, a provision that many professionals quietly dreaded. It packed references to both the Previous Year and the Assessment Year into a single, dense paragraph, often requiring multiple readings to fully decode. This criticism has appeared repeatedly in legal and professional commentary over the years.

The Income Tax Act, 2025, takes a markedly different approach. The charging section has been rewritten into five short, self-contained subsections. Instead of cross-referencing multiple temporal concepts, the law now states its core principle plainly: income tax is charged on the total income of every person for each Tax Year at the rates enacted for that Tax Year. That’s the entire logic, laid out without legal gymnastics.

This rewrite has been widely noted as one of the most meaningful drafting improvements in the new Act. By removing layered terminology from the charging section itself, the law eliminates confusion right at the entry point. Legal firms and policy analysts have described this as a move toward predictability and readability rather than just formal compliance.

Accounting Alignment: Accrual and Matching Principles Under the Tax Year

Beyond readability, this change carries deeper significance for businesses and accountants. Tax law has always had an uneasy relationship with accounting principles, especially accrual accounting. Under accrual concepts, income is recognised when it is earned, not when it is received, and expenses are matched to the revenues they help generate within the same period.

The old dual-year framework disrupted this alignment. Income earned in one year was taxed using rates and rules framed for another year, which introduced a conceptual mismatch. It was small on paper, but meaningful in practice when planning transactions or closing books. Professional advisories have flagged this misalignment for years, particularly in corporate and audit contexts.

By anchoring taxation squarely to the Tax Year in which income is earned, the 2025 Act brings tax computation closer to how financial statements are actually prepared. EY’s alerts on the new Bill explicitly highlight this convergence between tax timing and accounting recognition.

For businesses, this means fewer mental adjustments when moving from books to returns. You earn income in Tax Year 2026-27, apply Tax Year 2026-27 rates, and file in the next year. The path is linear, not zigzagged. It doesn’t eliminate complexity altogether-tax never does- but it removes a layer of unnecessary translation that had outlived its usefulness.

Short Tax Years and Special Scenarios Under Income Tax Act 2025

Tax law rarely has the luxury of dealing only in neat, twelve-month blocks. Businesses don’t always start on April 1, income streams don’t always exist for a full year, and sometimes operations simply stop midstream. The drafters of the Income Tax Act, 2025, seem to have acknowledged this reality upfront, which is where the idea of short Tax Years comes in.

Rather than forcing every taxpayer into a rigid April-to-March mold, the new Act allows a Tax Year to be shorter than twelve months in specific, clearly defined situations. This approach has been discussed at length in practitioner analyses that focus on operational practicality rather than theory.

Short Tax Years: New Businesses, Mid-Year Income, and Closure Cases

A Tax Year can be shorter than the standard twelve months in the following scenarios:

• New Business Setups:

If you set up a business partway through the year, say on October 15, 2026, your first Tax Year begins on that date and ends on March 31, 2027. This initial period, even though it spans only a few months, is treated as a complete Tax Year for compliance purposes. The following year then resets to the normal April-to-March cycle. This treatment has been highlighted as particularly helpful for startups and newly incorporated entities.

• Mid-Year Income Sources:

Not all income sources exist from day one. If, for instance, you begin earning rental income from a property in July 2026, the Tax Year for that specific source starts in July and runs until March 31, 2027. You’re not forced to artificially stretch that income backward to April just to satisfy a definition. This source-specific flexibility is one of the quieter but more thoughtful features of the new framework.

• Ceasing Entities:

When a business or profession shuts down before March 31, say on September 30, 2026, the Tax Year for that entity ends on the date of cessation. The period from April 1, 2026, to September 30, 2026, becomes the relevant Tax Year. This avoids the awkwardness of keeping a “ghost year” alive for tax purposes after operations have genuinely ended.

The common thread across these scenarios is practicality. The Tax Year concept isn’t treated as a rigid box but as a flexible container that adjusts to real economic activity. Analysts have noted that this design choice helps preserve the simplicity of the new system without forcing artificial compliance burdens on businesses whose timelines don’t fit the textbook calendar.

In other words, the law recognises that while simplicity is the goal, realism still matters. And in tax compliance, that balance is harder to strike than it sounds.

Filing Returns Under the Tax Year System: Deadlines and ITR-U Changes

Once the conceptual dust settles, most taxpayers land on a very practical question: Alright, but when do I actually file my return now? The Income Tax Act, 2025, answers this without reinventing the wheel, though the terminology does change.

The new law takes effect from April 1, 2026. That makes Tax Year 2026–27 (April 1, 2026, to March 31, 2027) the first year governed entirely by the new framework. Returns for this Tax Year will be filed during Tax Year 2027–28, referred to in the Act as the Subsequent Tax Year. This sequencing has been confirmed in official government communications and press notes issued alongside the Bill.

What Is the Subsequent Tax Year? New Filing Terminology Explained

The phrase Subsequent Tax Year sounds new, but its function will feel familiar. It simply means the Tax Year immediately following the one in which the income is earned. In practical terms, it does what the Assessment Year used to do, serve as the window for filing returns, processing them, and carrying out any scrutiny, but without the conceptual baggage of a second, parallel year.

This change in language has been explained directly in the FAQs released by the Income Tax Department, which emphasise that filing mechanics remain broadly the same even though the labels have been simplified. The idea is to make the timeline easier to explain, especially to individual taxpayers who file once a year and move on.

Income Tax Return Deadlines Under the New Tax Year Framework

While the terminology shifts, the familiar staggered filing structure remains largely intact:

• Salaried Individuals (ITR-1 and ITR-2): July 31 of the Subsequent Tax Year

• Non-Audit Businesses: August 31 of the Subsequent Tax Year

• Audit-Required Cases: October 31 of the Subsequent Tax Year

So, income earned during Tax Year 2026–27 will generally be reported by July 31, August 31, or October 31 of Tax Year 2027–28, depending on the category. This continuity has been highlighted in taxpayer-focused explainers to reassure filers that deadlines themselves are not being radically reshuffled.

Updated Return (ITR-U) Under Income Tax Act 2025: 48-Month Window

One of the more taxpayer-friendly changes introduced by the 2025 Act is the expansion of the time limit for filing an Updated Return (ITR-U). Under the new regime, taxpayers have up to 48 months from the end of the relevant Tax Year to correct errors or omissions in a filed return.

What’s more significant is what can now be corrected. The Act allows taxpayers to reduce previously reported losses in an updated return, something that was not permitted earlier. This is particularly relevant for businesses that may have overstated losses due to accounting errors or later clarifications in law. The practical implications of this change have been widely reported in mainstream financial media.

Taken together, the longer window and added flexibility signal a shift in tone. The system appears to be moving, at least incrementally, toward correction and voluntary compliance rather than immediate penalty. It’s not a free pass, but it does acknowledge that mistakes happen, especially in a complex tax environment.

Section 536 Explained: Repeal, Saving Clause, and Transition to the Tax Year

Replacing a tax law that has been in force for more than sixty years isn’t something you can do with a clean overnight switch. There are pending assessments, ongoing appeals, carried-forward losses, and unresolved disputes, all tied to the old regime. The Income Tax Act, 2025, addresses this reality through Section 536, commonly referred to as the Repeal and Saving clause.

At a structural level, Section 536 performs a delicate balancing act. On the one hand, it formally repeals the Income Tax Act, 1961, with effect from April 1, 2026. On the other hand, it ensures that this repeal does not erase rights, obligations, or proceedings that arose under the old law. This approach has been explained in detail in expert commentary analysing how amendments and proceedings will continue during the transition phase.

Repeal and Saving Clause: Carried-Forward Losses and Pending Assessments

Section 536 achieves several important objectives at once:

• Formal Repeal:

The Income Tax Act, 1961, stands repealed from April 1, 2026, making way for the new Act in full.

• Saving Existing Rights and Liabilities:

Any rights, obligations, penalties, or liabilities that arose under the 1961 Act continue to be governed by that law, even after repeal. In other words, repeal does not mean amnesty.

• Carried-Forward Losses:

Losses incurred under the old regime, such as those from Financial Year 2024-25 (Assessment Year 2025–26) can still be carried forward and set off in future years, despite the shift to the Tax Year system. This continuity has been explicitly confirmed in comparative analyses of the two Acts.

• Pending Assessments and Appeals:

Any assessment, reassessment, appeal, or legal proceeding relating to periods before April 1, 2026, will continue under the 1961 Act, as if it had not been repealed. This avoids legal uncertainty and jurisdictional confusion.

AY 2026–27 vs Tax Year 2026–27: Which Law Applies?

One issue that caused early confusion when the new Act was announced was the apparent overlap between Assessment Year 2026–27 and Tax Year 2026–27. On paper, both refer to the same calendar period, April 1, 2026, to March 31, 2027. So which law applies?

The answer is: both, but for different purposes.

• Assessment Year 2026–27 relates to income earned during Financial Year 2025–26 and is governed entirely by the Income Tax Act, 1961. Filing, scrutiny, and appeals for that income all happen under the old law.

• Tax Year 2026–27, under the new Act, refers to income earned during April 1, 2026, to March 31, 2027, which will be taxed according to the Income Tax Act, 2025.

This dual activity during the same calendar period has been clarified in multiple professional explainers to reassure taxpayers that there is no legal conflict or double taxation risk.

A simple way to think about it is this: during April 2026 to March 2027, you are simultaneously closing the past under the old law and living the present under the new one. One process looks backward; the other moves forward. They share dates, but not substance.

Structural Simplifications in Income Tax Act 2025 Beyond the Tax Year

The introduction of the Tax Year is the most visible change, but it’s really just the tip of a larger design shift. The Income Tax Act, 2025 reflects a broader drafting philosophy, one that prioritises consolidation, digital readiness, and language that doesn’t actively fight the reader. These changes don’t always make headlines, but in day-to-day compliance, they may end up mattering just as much.

TDS and TCS Consolidation: From 69 Sections to 13

Under the 1961 Act, provisions relating to Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) were scattered across 69 different sections. Each section dealt with a specific payment type-salary, rent, interest, professional fees-forcing taxpayers and deductors to constantly jump between provisions. This fragmentation was a long-standing pain point, particularly for businesses handling multiple kinds of payments.

The 2025 Act consolidates these provisions into just 13 sections, primarily grouped under Section 393. Instead of narrative-heavy drafting, the law now relies more on structured tables that clearly spell out who needs to deduct or collect tax, at what rate, and under what conditions. This shift has been analysed in detail by tax publishers and practitioners, who see it as a move toward usability rather than mere formal compliance.

The difference is subtle but important. Instead of interpreting dense prose, deductors can now scan a table and understand their obligation at a glance. For large organisations dealing with dozens of TDS categories, that clarity adds up quickly.

Digital Economy Recognition Under the Income Tax Act 2025

Another notable shift is the Act’s explicit recognition of income arising from the virtual digital space. The 1961 Act, drafted long before cloud computing and platform economies, struggled to keep pace with digital business models. Concepts like online marketplaces, cloud servers, and social media monetisation were often retrofitted into provisions never designed for them.

The 2025 Act addresses this head-on by acknowledging that income can be generated through digital infrastructure, email servers, cloud storage, digital platforms, and that such presence can have tax implications. This change has been highlighted in policy and consulting firm analyses as a necessary update for a digital-first economy.

It’s not just a definitional tweak. By formally recognising virtual spaces, the law creates clearer hooks for jurisdiction, compliance, and enforcement in an economy where physical presence is no longer the default.

Plain Language Drafting: Simplifying Legal Terminology

Perhaps the most understated reform is linguistic. The drafting committee made a conscious effort to remove archaic legal phrases, expressions like “without prejudice to the generality of the foregoing” or “notwithstanding anything contained hereinbefore.” These phrases may be familiar to lawyers, but for most readers, they obscure more than they clarify.

The 2025 Act still reads like a statute; it’s not pretending to be a blog post, but the sentences are shorter, the structure is cleaner, and the logical flow is easier to follow. This plain-language push has been noted in multiple expert commentaries as a step toward accessibility without sacrificing legal precision.

Taken together, these structural simplifications suggest that the Tax Year reform isn’t an isolated fix. It’s part of a larger attempt to make the law navigable for the people who actually have to use it, not just those trained to interpret it.

Global Alignment and Investor Impact of the Unified Tax Year

India’s move to a unified Tax Year isn’t happening in isolation. Tax systems don’t evolve in a vacuum, and policymakers were clearly looking outward while drafting the Income Tax Act, 2025. One of the recurring themes in official explanations and expert commentary is alignment, with global norms, with investor expectations, and with how modern economies actually function.

Most OECD countries already operate on a single-year tax concept. The United Kingdom, Australia, and Canada all tax income within one coherent annual frame, without the conceptual split between earning and assessment that characterised India’s earlier system. While the UK’s tax year famously runs from April 6 to April 5 (a historical oddity), the underlying logic is simple: income earned in a tax year is taxed in that same tax year. This comparison has been repeatedly drawn in professional analyses discussing India’s reform direction.

By adopting a similar framework, India sends a signal, especially to multinational corporations and foreign investors, that its tax system is moving toward predictability. Investor confidence is closely tied to clarity. When timelines are intuitive and terminology is consistent, it becomes easier to model tax costs, plan investments, and assess risk. This point has been emphasised in several consulting and policy firm notes reviewing the broader impact of the 2025 Act.

Trust-Based Governance and Faceless Compliance Systems

The Tax Year reform also fits neatly into India’s longer-running push toward trust-based governance. Over the last few years, the income tax ecosystem has shifted dramatically toward digitisation. As per official data releases, more than 99% of income tax returns are now filed electronically, with the majority processed through faceless assessment systems that minimise direct interaction between taxpayers and tax officers.

Simplification plays a crucial supporting role here. A faceless, digital system only works well when the underlying rules are easy to follow. When taxpayers can understand what year applies, which rates apply, and when to file without decoding layered terminology, voluntary compliance becomes more realistic. This, in turn, allows the tax administration to focus its resources on genuinely complex or high-risk cases rather than routine clarifications.

Several expert reviews of the new Act point out that clarity and reduced human interface go hand in hand. The Tax Year concept, while modest on the surface, reinforces a system where compliance is driven more by understanding than by enforcement pressure.

In that sense, the reform is as much about behaviour as it is about structure. A clearer system nudges taxpayers toward compliance, not through fear or complexity, but through predictability.

Preparing for the Income Tax Act 2025 Tax Year Transition

The shift from the Income Tax Act, 1961, to the Income Tax Act, 2025, is more than a routine legislative update. It’s a structural reset, one that tries to correct decades of accumulated complexity rather than layering one more amendment on top. The introduction of the unified Tax Year sits at the center of this change, collapsing the long-standing duality of “Previous Year” and “Assessment Year” into a single, more intuitive framework.

For taxpayers, the direction of travel is clear. The future of Indian taxation is meant to be simpler, more transparent, and closer to global standards. That intent has been reiterated across official statements, explanatory memoranda, and expert commentary since the Bill was introduced.

Still, simplicity on paper doesn’t mean taxpayers can afford to be passive. The transition period, especially the overlap year beginning April 1, 2026, will require attention and planning.

Actionable Steps for Taxpayers and Practitioners Before April 1, 2026

- Update Your Accounting Systems

Businesses and professionals should ensure that their accounting and compliance software reflects the new Tax Year terminology. Most major software providers have already announced updates aligned with the 2025 Act, as noted in industry briefings and professional updates. - Review Your Record-Keeping Practices

With the expanded 48-month window for filing updated returns (ITR-U), accurate and retrievable records matter more than ever. Digital record-keeping is no longer optional, it’s foundational to managing corrections and revisions efficiently, a point repeatedly stressed in expert analyses of the new regime. - Stay Informed About CBDT Notifications

The Central Board of Direct Taxes (CBDT) will continue to issue rules, circulars, and clarifications to operationalise the Act. Keeping track of these updates through official channels is essential, particularly during the first few years of implementation. - Educate Your Team

For businesses, the shift from Assessment Year to Tax Year affects more than return filing. TDS compliance, payroll processing, budgeting cycles, and internal reporting all touch tax timelines. Ensuring that finance and HR teams understand the new language and logic will reduce friction during the transition. - Plan for the Transition Year

During Tax Year 2026–27, taxpayers will be doing two things at once: filing returns for FY 2025–26 under the old law, while simultaneously earning income under the new Tax Year framework. This overlap is manageable, but only if compliance calendars are planned carefully, a point highlighted in several expert transition guides.

Final Outlook: A Stepping Stone to Viksit Bharat

Policymakers have repeatedly described the Income Tax Act, 2025, as a stepping stone toward Viksit Bharat 2047, a vision of India as a fully developed nation by the centenary of its independence. Tax reform may not sound inspirational, but it’s foundational. A system that people can understand is a system they are more likely to comply with.

When small business owners can grasp their tax obligations without decoding dense legal language, when salaried employees can file returns without second-guessing which year applies, and when the administration can process compliance digitally without excessive manual intervention that’s when reform starts to show real dividends.

The Tax Year is more than a change in terminology. It represents a quiet recalibration of the relationship between the taxpayer and the state, one built on clarity, predictability, and a measure of trust. It won’t be perfect. No reform ever is. But it does move the system in a direction that feels more rational than ritualistic.

April 1, 2026 marks the beginning of Tax Year 2026–27.

The countdown isn’t symbolic anymore. It’s practical.

Leave a Reply