Uncovering the 2026 Labour Codes’ Hidden Costs: Beyond the 50% Wage Rule

Navigating the 2026 Labour Codes: Understanding the True Operational and Financial Impact

Ask almost any HR leader, CFO, or payroll consultant in India about the biggest change introduced by the 2026 Labour Codes, and the answer is usually the same: “basic pay must now be 50% of CTC.” That single provision has come to dominate conversations around the reforms. It is the headline point in payroll webinars, the focus of LinkedIn explainers, and often the first thing employers discuss when preparing for compliance. The core issue here is the 2026 Labour Codes’ hidden costs.

What receives far less attention is everything that follows once basic pay increases. It is not just another figure on a salary slip. A higher basic salary has a cascading effect across several areas of workforce costs. Employers may see larger provident fund contributions, higher gratuity liabilities, increased overtime payouts, tighter exit settlement obligations, gig worker related levies, and additional spending on welfare infrastructure. Taken together, these changes can have a much bigger financial impact than the widely discussed 50% wage rule itself.

This article explores those less visible costs by examining the Code on Wages 2019, the Code on Social Security 2020, the Industrial Relations Code 2020, and the Occupational Safety, Health and Working Conditions (OSH) Code 2020. All four codes came into central force on 21 November 2025, while the central rules under each were notified on 8 May 2026. At the same time, individual states continue to roll out their own rules and implementation timelines, creating a compliance landscape that employers must monitor closely.

At A Glance: 2026 Labour Codes’ Hidden Costs

· Beyond the 50% Wage Rule: The mandate requiring basic pay to be at least 50% of CTC triggers a cascade of hidden operational costs that extend far beyond simple payroll restructuring.

· Surging Statutory Liabilities: Expanding the statutory wage base directly inflates employer provident fund (EPF) contributions and accelerates gratuity accruals, demanding immediate cash-flow reforecasting.

· The 48-Hour F&F Mandate: Employers must now process full and final (F&F) exit settlements within two working days, necessitating urgent HRMS and payroll automation to avoid severe legal penalties.

· Gig Economy Compliance: Digital platforms and aggregators face a newly enforced 1-2% turnover levy to fund mandatory social security benefits for gig and platform workers.

· Strategic CTC Restructuring: Superficial renaming of allowances will fail compliance tests; businesses must conduct thorough salary audits and financial scenario modeling to successfully navigate the 2026 Labour Codes.

The New Baseline: Understanding the 2026 Labour Code Consolidation

The Shift from 29 Acts to 4 Unified Codes

For decades, navigating India’s labour law framework meant dealing with a patchwork of 29 separate central legislations. Each law had its own definitions, compliance requirements, thresholds, and enforcement mechanisms. Even fundamental terms such as “wages” and “worker” were interpreted differently depending on the statute. Employers often found themselves managing overlapping obligations under laws like the Factories Act, the Payment of Wages Act, the Industrial Disputes Act, the EPF Act, and many others.

The 2026 labour law reforms aim to simplify this landscape by bringing those fragmented laws under four unified labour codes:

| Code | Core subject matter |

| Code on Wages, 2019 | Minimum wages, timely payment, bonus, equal remuneration |

| Industrial Relations Code, 2020 | Trade unions, standing orders, lay-off, retrenchment, disputes |

| Code on Social Security, 2020 | Provident fund, ESI, gratuity, maternity benefit, gig and platform workers |

| OSH Code, 2020 | Working hours, safety, welfare facilities, women’s night-shift work |

Although the four labour codes came into effect at the central level on 21 November 2025, the Central Rules that operationalise them were notified only on 8 May 2026. These include the Code on Wages (Central) Rules 2026, Social Security (Central) Rules 2026, Industrial Relations (Central) Rules 2026, and the OSH (Central) Rules 2026.

It is equally important to understand that these Central Rules do not apply to every employer in the country. They primarily govern establishments where the Central Government is the “appropriate government,” including railways, mines, ports, banks, insurance companies, telecom operators, central public sector undertakings, and certain multi-state establishments. Most factories, commercial establishments, plantations, and private employers will instead be governed by rules notified by their respective state governments. Since states have progressed at different speeds, compliance requirements may still vary across jurisdictions.

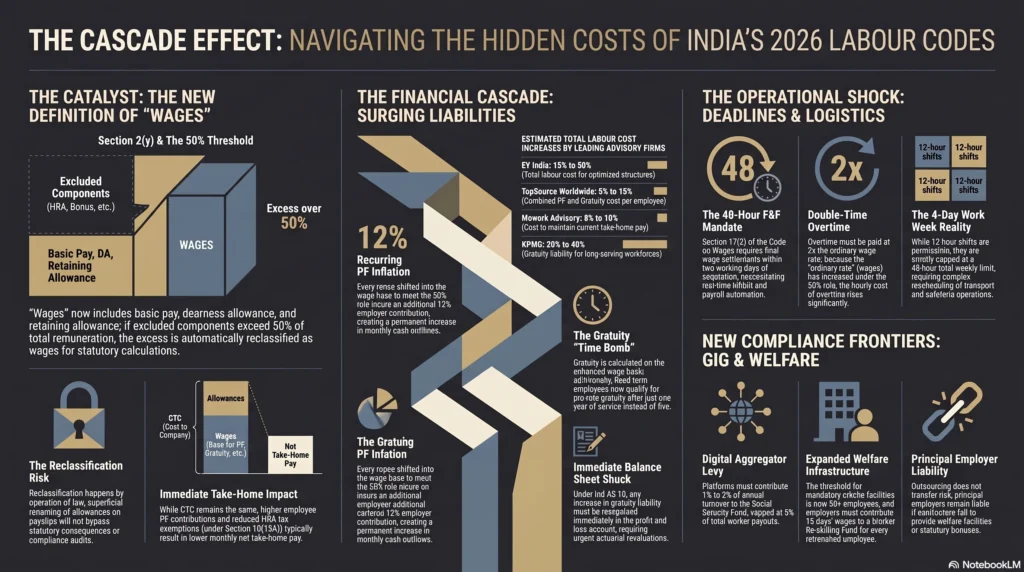

The New Definition of “Wages” Under Section 2(y)

Much of the financial impact discussed in this article can be traced back to a single change in how the law defines “wages.” Section 2(y) of the Code on Wages, 2019 introduces a standard definition that is mirrored in Section 2(88) of the Code on Social Security, Section 2(zq) of the Industrial Relations Code, and Section 2(zzj) of the OSH Code.

Under this definition, wages include basic pay, dearness allowance, and retaining allowance. At the same time, certain components remain outside the definition, including house rent allowance (HRA), conveyance allowance, bonus, overtime, commission, the employer’s provident fund contribution, and gratuity.

The real significance lies in the proviso attached to this definition. If the excluded components make up more than 50% of an employee’s total remuneration during any wage period, the amount exceeding that threshold is automatically treated as “wages” for statutory calculations. This affects provident fund contributions, gratuity, bonus, ESI, and other statutory benefits.

This is not a choice available to employers. The reclassification happens by operation of law, regardless of how individual salary components are described on the payslip. Simply renaming allowances or restructuring salary heads cannot avoid the statutory consequences.

Why the Focus is Disproportionately on the 50% Basic Pay Rule

The 50% wage rule has become the most talked about aspect of the labour codes because it is the change employees notice immediately. A higher basic salary is visible on every monthly payslip, making it easy to understand and discuss. By comparison, changes such as increased gratuity provisioning or higher employer contributions are less visible, even though they can significantly affect an organisation’s long-term costs.

In reality, the increase in basic pay is only the starting point. It triggers a series of financial and operational consequences that extend well beyond payroll restructuring. Higher provident fund contributions, increased gratuity liabilities, stricter 48-hour exit settlement timelines, revised overtime calculations, gig worker related obligations, and expanded welfare infrastructure requirements all add to the overall cost of compliance. These are recurring commitments that employers must plan for over time, making them far more significant than the headline change alone.

Unpacking the 50% Wage Rule and Its Direct Impact on Payroll

The Mathematics of CTC Restructuring

The impact of the 50% wage rule becomes much clearer when you look at the numbers. Consider an employee with a monthly CTC of ₹90,000. Traditionally, many employers structured salaries by keeping the basic pay relatively low while allocating a larger share to various allowances. This approach helped optimise statutory contributions without changing the overall cost to the company.

| Component | Pre-Code Structure | Post-Code (Compliant) Structure |

| Basic + DA (“wages”) | ₹27,000 (30%) | ₹45,000 (50%) |

| Allowances (HRA, special, conveyance) | ₹63,000 (70%) | ₹45,000 (50%) |

| Employer PF @ 12% of wages | ₹3,240/month | ₹5,400/month |

| Employee PF @ 12% of wages | ₹3,240/month | ₹5,400/month |

| Net monthly take-home impact | — | ₹2,160 lower, all else equal |

At first glance, an additional employer PF contribution of ₹2,160 a month may not appear particularly significant. Scale that across a workforce of several hundred employees, however, and the increase becomes a meaningful addition to annual payroll costs. It is one of the reasons many organisations are reassessing salary structures well before implementation deadlines.

Payroll teams also need to account for another important detail. Wage periods for daily-rated employees and overtime calculations continue to be based on the conventional 26 working day month. Although this is separate from the 50% wage rule itself, payroll systems and calculation engines must be updated to reflect both changes accurately.

Allowances, Exclusions, and the Reclassification Risk

The law is designed to prevent superficial salary restructuring. Simply renaming a salary component without changing the overall pay structure will not achieve compliance. What matters is the substance of the salary composition, not the label assigned to each component.

If excluded components continue to account for more than 50% of an employee’s total remuneration, the excess is automatically added back into wages for statutory calculations, regardless of how those components are described on the payslip.

There are also important distinctions within the exclusions themselves. Bonus continues to remain outside the definition of wages under Section 26 of the Code on Wages, even if it represents a substantial portion of an employee’s compensation. Other components, including overtime, conveyance allowance, and special allowances, do not receive the same treatment once the 50% threshold is crossed.

This is why labour law advisers consistently caution employers against relying on cosmetic changes. Renaming salary heads without genuinely rebalancing the ratio between basic pay and allowances can still leave an organisation non-compliant, despite the time and effort spent on restructuring .

The Immediate Hit to Employee Take-Home Pay

While employers often focus on the increase in their own statutory contributions, employees usually notice a different consequence first. Because employee provident fund contributions increase alongside the employer’s contribution, the monthly amount credited to their bank account falls, even though the overall CTC remains unchanged.

There is another consequence that is easy to overlook. House Rent Allowance exemption under Section 10(13A) of the Income Tax Act is calculated partly on the actual HRA an employee receives. When HRA is reduced to accommodate a higher basic salary, the available tax exemption may also decrease. For employees, particularly those living in metropolitan cities where HRA exemptions can make a noticeable difference, this can reduce post-tax income even further. It is an effect that often receives little attention during the initial rollout of revised salary structures, making clear employee communication especially important.

The Hidden Balance Sheet Shock: Escalating Provident Fund Liabilities

How a Higher Basic Pay Inflates Employer EPF Contributions

One of the most immediate financial consequences of the new wage definition is the increase in provident fund contributions. Both the employer and the employee contribute 12% of statutory wages. As the wage base expands under the 50% rule, so does the amount payable every month. Every rupee that shifts from an excluded allowance into the statutory wage base results in an additional 12% employer contribution for as long as that employee remains on the payroll.

The legislation also blocks one of the most obvious ways employers might try to offset the additional expense. Section 124 of the Code on Social Security expressly prevents organisations from reducing other components of an employee’s compensation simply to compensate for higher statutory contributions. In practical terms, businesses are expected to absorb the increase rather than restructure salaries in a way that undermines the intent of the law.

The Cash Flow Implications of Uncapped PF Liabilities

Provident fund obligations affect cash flow differently from gratuity. Gratuity is generally a long-term liability that becomes payable when an employee leaves or retires. Provident fund contributions, by contrast, require monthly cash outflows. The impact begins as soon as the revised salary structure takes effect and continues every payroll cycle thereafter.

There is also very little room for delay. Under Section 127 of the Code on Social Security, employers who miss EPF or ESI remittance deadlines are liable to pay simple interest at 12% per annum on delayed contributions. This provision was formally notified through the Central Rules issued on 8 May 2026. What might begin as a temporary cash flow challenge can therefore become an ongoing statutory cost if payroll compliance slips.

Because these higher contributions apply across the workforce rather than only to employees leaving the organisation, provident fund costs are usually the first increase finance teams see reflected in monthly cash flow forecasts. Unlike one-off employee exits or retirement payments, this is a recurring obligation that becomes part of routine payroll expenditure.

Budgeting for Employer Statutory Cost Increases Without Altering CTC

The overall increase in labour costs depends largely on how salaries were structured before the reforms. Organisations that historically relied heavily on allowances are likely to experience the biggest adjustments. While estimates differ across advisory firms, they generally fall within a similar range.

| Source | Estimated increase | What it measures |

| EY India analysis | 15 to 20% | Total labour cost for aggressively optimised salary structures |

| TopSource Worldwide | 5 to 15% | Combined provident fund and gratuity cost per employee |

| Mewurk payroll advisory | Approximately 8 to 10% | Employer cost of maintaining current take-home pay |

| KPMG commentary | 20 to 40% | Increase in gratuity liability for long-serving workforces |

Industries such as IT services, BFSI, and sales-led organisations are expected to feel the greatest impact. These sectors have traditionally maintained relatively low basic salaries while allocating a larger share of compensation to allowances. As a result, they often require the most significant restructuring to meet the new wage threshold.

The Gratuity Time Bomb: Accelerated Accrual and Expanded Eligibility

Calculating the 15-Day Wage Rule on a 50% Enhanced Base

Gratuity obligations are also set to rise under the revised wage framework. Section 53 of the Code on Social Security continues to calculate gratuity as 15 days’ wages for every completed year of service, using the employee’s last drawn basic pay and dearness allowance as the basis.

Although gratuity itself remains excluded from the statutory definition of wages for the purposes of the 50% calculation, the amount ultimately payable increases whenever the underlying basic salary increases. Since the formula is directly linked to basic pay and dearness allowance, a larger wage base translates into higher gratuity obligations over time.

From an accounting perspective, employers generally estimate gratuity provisioning at roughly 4.81% of basic pay each month, based on the statutory formula of 15 days divided by a 26 working day month and spread across 12 months. Increasing the basic salary from 30% to 50% of CTC therefore raises the monthly gratuity accrual proportionately, even though the actual payment may not be made until years later.

The Financial Impact of One-Year Gratuity for Fixed-Term Employees

The reforms also expand the number of employees who qualify for gratuity. Under the earlier framework, gratuity generally became payable only after five years of continuous service. The Code on Social Security changes this position by allowing fixed-term employees to receive pro rata gratuity after completing just one year of service.

For organisations that rely heavily on project-based or fixed-term hiring, this represents a significant shift in employment costs. A category of workers that previously generated little or no gratuity liability now creates a statutory benefit obligation.

The final Central Rules notified on 8 May 2026 also resolved an earlier uncertainty. The Industrial Relations Code had already specified a one-year eligibility requirement for fixed-term employees, while earlier draft rules under the Code on Social Security did not clearly prescribe a minimum period of service. The final rules aligned both codes by confirming a one-year threshold, removing ambiguity around eligibility.

Retrospective Liability vs. Prospective Accounting for Gratuity Provisions

One point that offers employers some certainty is that the revised gratuity calculation operates prospectively. The higher wage base applies only from 21 November 2025 onward and does not require organisations to recalculate gratuity for service completed before that date.

That said, the accounting impact is far from gradual. The Institute of Chartered Accountants of India has clarified that any increase in gratuity liability arising from the labour codes must be recognised in the profit and loss account when preparing interim financial statements for the period ending 31 December 2025. Employers cannot spread or defer the additional expense over future reporting periods.

Under Ind AS 19, gratuity is treated as a defined benefit obligation. Any statutory change that increases this liability requires an immediate actuarial revaluation, with the resulting impact recognised in the profit and loss account or Other Comprehensive Income during the year the change takes effect. For finance teams, delaying actuarial assessments until the end of the financial year can lead to unexpected adjustments that affect reported earnings and financial planning.

Operational Hurdles: The 48-Hour Full and Final (F&F) Settlement Mandate

The Logistical Nightmare of Two-Day Exit Settlements

One of the most demanding operational changes introduced by the new labour framework is the timeline for full and final settlements. Under Section 17(2) of the Code on Wages, employers are required to pay an employee’s final wages within two working days of resignation, dismissal, retrenchment, or any other form of separation.

For many organisations, this represents a major departure from long-standing practice. Traditionally, full and final settlements were often completed over 30 to 90 days, allowing enough time to recover company assets, reconcile leave balances, verify reimbursements, and process payments through the regular monthly payroll cycle.

It is also important to distinguish wages from gratuity. Gratuity continues to follow its own statutory timeline of 30 days under the Code on Social Security and is not covered by the 48-hour settlement requirement. As a result, payroll teams must establish separate workflows that allow wages, leave encashment, and other final dues to be processed immediately, without waiting for gratuity calculations to be completed.

Upgrading Payroll and HRMS Systems to Meet Settlement Deadlines

Meeting a two working day deadline is not simply a matter of revising company policy. It requires payroll and HR systems that can process employee exits almost in real time.

Leave balances need to be updated continuously instead of being reconciled at the end of each month. Notice pay adjustments, gratuity eligibility, and other exit-related calculations should be triggered automatically when an employee’s separation is recorded. Finance teams also need the ability to process off-cycle payments without waiting for the next scheduled payroll run.

Organisations that still rely on spreadsheets or legacy payroll software may find compliance particularly difficult. Even a small delay in calculating an employee’s leave encashment or verifying a payroll component can cause the settlement timeline to exceed the statutory limit.

Financial Penalties and Compliance Risks for Delayed F&F Payouts

The consequences of missing the settlement deadline extend beyond administrative inconvenience. Section 54 of the Code on Wages prescribes escalating penalties for delayed or non-payment of wages. A first offence can attract a fine of up to ₹50,000. Repeat offences within five years may result in fines of up to ₹1 lakh, imprisonment of up to three months, or both. Responsibility can also extend personally to the individual overseeing payroll compliance.

For businesses handling dozens or even hundreds of employee exits every year, the challenge is not an isolated compliance issue. A payroll process that consistently misses the two working day deadline creates repeated exposure to statutory penalties, making efficient exit management a business necessity rather than an administrative improvement.

Working Hours, Overtime, and the 4-Day Work Week Illusion

The Reality of 12-Hour Shifts and 48-Hour Weekly Caps

The idea of a four day work week has attracted widespread attention since the labour codes were announced. However, the legal framework is more nuanced than many headlines suggest.

The final Code on Wages Rules continue to recognise an eight hour standard working day, in line with the Occupational Safety, Health and Working Conditions Code. Employers may organise work into four longer shifts, but only if the total working time remains within the 48 hour weekly limit and mandatory rest breaks are observed.

State level rules illustrate how these arrangements are expected to operate in practice. For example, exemptions issued under Haryana’s Shops and Establishments framework require employers to comply with a 48 hour weekly limit, daily working hour restrictions, overtime at twice the ordinary wage rate, and mandatory rest intervals after every six hours of work.

This means a four day work week does not reduce the total number of hours employees work. Instead, it redistributes those hours across fewer days. For employers, that often means redesigning shift schedules, transport arrangements, cafeteria operations, security coverage, and supervisory staffing. These operational adjustments can involve significant planning and expense, even though they rarely feature in discussions about flexible work schedules.

Double-Time Overtime Rules on an Increased Wage Base

Overtime costs are also likely to increase under the revised wage structure. Section 27 of the Occupational Safety, Health and Working Conditions Code requires employers to pay at least twice the ordinary rate of wages for overtime work.

While guidance differs slightly on when overtime begins, with some sources referring to work beyond eight hours a day and others referencing nine hours or 48 hours a week, there is broad agreement on one point. Overtime must be compensated at double the applicable wage rate, not at a lower multiplier.

Because overtime calculations are based on the revised statutory definition of wages, a higher basic salary also increases the hourly overtime rate. Industries such as manufacturing, logistics, warehousing, and other shift-based operations are therefore likely to experience a noticeable rise in overtime costs alongside their higher provident fund and gratuity obligations.

Tracking and Automating Attendance for Compliance Accuracy

These requirements place greater emphasis on accurate attendance records than ever before. The Occupational Safety, Health and Working Conditions Code encourages the use of digitised registers, electronic wage records, and digital compliance systems, making accurate attendance data an essential part of payroll administration rather than an optional convenience.

For many employers, this means investing in biometric attendance systems or integrated digital platforms that connect attendance directly with payroll calculations. Automating these processes not only helps ensure overtime is calculated correctly but also creates a reliable audit trail. That documentation can prove invaluable during inspections by an Inspector-cum-Facilitator or when responding to employee grievances relating to working hours, overtime, or wage payments.

Social Security and the Gig Economy Transition

Mandatory Contributions to the Social Security Fund for Aggregators

One of the most significant changes introduced by the new labour framework is the formal recognition of gig workers, platform workers, and aggregators within India’s social security system. For the first time, businesses operating ride-hailing services, food delivery platforms, and similar digital marketplaces are required to contribute between 1% and 2% of their annual turnover to a Social Security Fund. The contribution is subject to an upper limit of 5% of the total amount paid to gig and platform workers.

The objective is to make social security benefits more portable. Instead of being tied to a single platform, benefits such as life and disability insurance, health and maternity cover, and old age protection are linked to workers through Aadhaar-enabled Universal Account Numbers and e-Shram registration. This allows eligible workers to retain their benefits even when they move between different platforms.

The Central Rules notified in May 2026 also introduced a minimum age requirement for accessing these benefits. As a result, aggregators need to incorporate age verification into their onboarding and worker registration processes to ensure compliance from the outset.

Expanding Employee State Insurance (ESI) Thresholds via New Wage Definitions

The revised definition of wages affects more than just provident fund and gratuity. Employee State Insurance calculations are also based on statutory wages, meaning the 50% reclassification can alter ESI eligibility and contribution calculations for many employees.

Alongside these structural changes, the revised Social Security Rules also enhance certain employee benefits. The maximum funeral expense benefit available under the ESI scheme has increased from ₹15,000 to ₹20,000, while the medical bonus payable as part of maternity benefits has doubled from ₹7,500 to ₹15,000.

Employers that provide supplementary maternity or insurance benefits should review their internal policies to ensure they remain aligned with the revised statutory framework.

The Cost of Compliance for Platform-Based Business Models

For platform businesses, compliance extends well beyond registering with the appropriate authorities. The new framework introduces ongoing operational responsibilities that require continuous monitoring and reporting.

Businesses must establish systems to calculate turnover-linked contributions accurately, maintain worker registrations on government portals, and verify age eligibility before workers can access social security benefits, as required under the final rules.

Unlike conventional payroll expenses that generally increase as employee numbers grow, the aggregator contribution is linked to business turnover. As revenue expands, so does the contribution, even if the size of the registered gig workforce remains relatively stable. This makes compliance costs an ongoing part of business growth rather than a one-time regulatory adjustment.

Infrastructure and Welfare: The Overlooked Compliance Expenditures

Mandatory Annual Health Check-ups and Safety Standards

Not every change under the final labour rules resulted in additional costs. In some areas, the government narrowed earlier proposals before notifying the final framework.

Draft Occupational Safety, Health and Working Conditions Rules had proposed mandatory annual health check-ups for workers over the age of 40 across factories, mines, docks, and construction establishments, with examinations to be completed within 120 days of the start of each calendar year. The final rules significantly reduced this requirement. Mandatory annual health check-ups now apply only to dock workers and employees engaged in building and construction work, while the earlier 120-day deadline has been removed altogether.

This distinction matters from a budgeting perspective. Employers that had planned large-scale factory health screening programmes based on earlier draft rules may need to revisit those assumptions. Construction and dock employers, however, should continue treating annual health check-ups as an ongoing compliance obligation.

The final rules also require establishments employing 500 or more workers to constitute a safety committee. At the same time, the Central Government retains the authority to revise this threshold for specific industries or categories of establishments in the future

The Financial Burden of Crèche Facilities and Principal Employer Responsibilities

The revised labour framework also broadens access to workplace childcare facilities. Establishments employing 50 or more workers are now required to provide crèche facilities, lowering the threshold that applied under several of the earlier labour laws that have since been consolidated.

The final Social Security Rules further strengthen maternity-related protections, including provisions relating to crèche facilities and safeguards against dismissal during pregnancy.

The responsibilities of principal employers have also become more explicit. Where contract labour is engaged, the principal employer may still be held responsible if the contractor fails to provide mandatory welfare facilities or defaults on statutory bonus payments owed to contract workers. In other words, outsourcing labour does not automatically transfer compliance obligations. Employers must actively monitor contractor compliance rather than assume responsibility ends once work is outsourced.

Reskilling Funds and Retrenchment Cost Amplifications

Retrenchment now carries an additional financial obligation. Under the revised framework, employers must contribute an amount equal to 15 days of a retrenched employee’s last drawn wages to the Worker Re-skilling Fund. This requirement was formally brought into operation through the Central Rules notified on 8 May 2026.

Because the contribution is calculated using last drawn wages, any increase in the statutory wage base under the 50% rule also increases the amount payable into the fund. As a result, workforce restructuring exercises now carry higher statutory costs than they would have under earlier salary structures.

Construction sector employers also need to account for another recurring obligation. Building and construction projects continue to attract a welfare cess of 1% of construction costs, with the proceeds supporting welfare schemes for construction workers. While separate from payroll, it remains an important compliance cost that should be factored into project budgets alongside the broader labour code changes.

Strategic Restructuring: How Employers Can Mitigate the Financial Blow

Conducting a Comprehensive CTC Audit Across All Departments

The first step in managing the financial impact of the new labour codes is understanding where your organisation stands today. That means carrying out a detailed CTC audit across every department rather than applying a one-size-fits-all approach. Permanent employees, fixed-term employees, and contract or agency workers should all be assessed separately because each group creates different statutory obligations and long-term cost implications.

A thorough audit should identify which employee groups currently fall below the 50% wage threshold and measure the extent of the gap. This allows organisations to target restructuring where it is actually needed instead of implementing broad salary revisions across the entire workforce. In many cases, functions such as sales and IT, where compensation has traditionally relied heavily on allowances, will require more extensive restructuring than manufacturing or operations roles that already have relatively higher basic pay.

Scenario Modeling: Reducing Allowances vs. Increasing Total CTC

Once the compliance gap has been identified, employers face a strategic decision. They can either accommodate the higher statutory costs within the existing CTC by reducing allowances, or increase overall CTC to preserve employees’ current take-home pay while meeting the statutory wage requirement.

Whichever path is chosen, careful financial modelling is essential. Labour law advisers repeatedly caution organisations against several common mistakes that can make restructuring more expensive or leave them non-compliant:

- Renaming allowances without genuinely increasing the proportion of basic pay.

- Failing to calculate the 50% threshold correctly for employees with variable compensation or significant ESOP components.

- Applying a standard salary template across every role instead of modelling different employee groups separately.

- Looking only at provident fund costs while overlooking the combined impact on gratuity, taxation, and other statutory liabilities.

- Finalising salary changes before reviewing the financial implications with finance, payroll, and actuarial teams.

Taking the time to model multiple scenarios before implementation can help employers strike a balance between compliance, employee expectations, and long-term cost control.

Modernizing Contracts and Vendor Agreements

Salary restructuring is only one part of the transition. Employment documentation also needs to be updated to reflect the revised legal framework.

Appointment letters, employment agreements, HR policies, and staffing vendor contracts should all be reviewed to ensure they incorporate the new wage definitions, revised gratuity provisions, and accelerated full and final settlement timelines. The final Occupational Safety, Health and Working Conditions Rules also introduce a standardised appointment letter format that captures key employee details such as name, date of birth, Aadhaar number, designation, and the nature of employment.

Employers that engage contract labour should review vendor arrangements particularly carefully. The labour codes place restrictions on using contract labour for core business activities. At the same time, the revised Occupational Safety, Health and Working Conditions Rules simplify contractor licensing by allowing a single licence for contractors operating across multiple states instead of requiring separate licences in each state.

Although this reduces administrative complexity, organisations will still need to revisit existing contracts to ensure they reflect the updated legal requirements.

Effective Employee Communication Strategies to Manage Expectation Drops

Even a well-planned salary restructuring can create unnecessary friction if employees are not told what is changing and why.

For many employees, the most noticeable outcome of the new wage structure is a lower monthly take-home salary. Without context, that reduction can easily be interpreted as a pay cut rather than the result of increased provident fund contributions and higher long-term retirement benefits.

Clear communication can make a significant difference. Employers should explain the legal changes, outline how the revised salary structure affects statutory benefits, and illustrate the long-term impact in practical financial terms rather than relying on technical legal language. A transparent communication strategy helps reduce confusion, employee grievances, and unnecessary attrition during what is already a significant organisational transition.

Transitioning Successfully into India’s 2026 Labour Framework

Moving from Legacy Payroll to Automated Compliance Systems

A recurring theme across the new labour codes is the growing importance of automation. Many of the new obligations simply cannot be managed efficiently through manual processes or month-end spreadsheets.

Requirements such as two working day full and final settlements, automated gratuity calculations, electronic appointment letters, digital wage registers, and attendance systems that feed directly into overtime calculations all depend on payroll and HR platforms capable of processing information in real time.

Compliance reporting is also becoming more centralised. Registers, statutory returns, and inspection processes are increasingly being managed through integrated digital portals. Randomised, technology-driven inspection allocation is gradually replacing the discretionary inspection model that characterised the earlier labour law framework, making accurate digital records more important than ever.

Frequently Asked Questions: 2026 Labour Codes’ Hidden Costs

The rule mandates that basic pay plus dearness allowance must comprise at least 50% of an employee’s total compensation (CTC). If excluded allowances exceed 50%, the excess amount is automatically reclassified as wages, directly inflating statutory compliance costs.

Because provident fund (EPF) contributions are calculated on the statutory wage base, pushing basic pay to 50% of CTC automatically increases the monthly 12% employer match. This creates a permanent, recurring increase in monthly cash outflows across the entire workforce.

Since gratuity is tied to last-drawn basic pay, a higher wage base significantly accelerates long-term gratuity accruals. Furthermore, fixed-term employees now qualify for pro-rata gratuity after just one year of service, instead of the traditional five-year threshold.

Section 17(2) requires final wages to be paid within two working days of an employee’s exit. To avoid steep statutory penalties, businesses must transition from legacy payroll spreadsheets to real-time HRMS automation that instantly reconciles leave encashments and notice pay.

Platform-based business models must now contribute 1% to 2% of their annual turnover to a dedicated Social Security Fund for gig workers, subject to a 5% cap of total worker payouts. This obligation is tied to overall revenue growth rather than headcount.

Employers should execute a comprehensive departmental CTC audit and use financial scenario modeling to rebalance allowances within existing CTCs, while updating employment contracts to match the final notified state-specific rules.

Aligning Finance, HR, and Legal Teams for State-by-State Notifications

One of the biggest practical challenges facing employers is that implementation is not happening uniformly across the country. The applicable rules depend on which authority is considered the “appropriate government” for a particular establishment. That determination is based on the nature of the business and its regulatory framework rather than simply the location of the company’s head office.

The pace of implementation also differs from state to state. Some states, including Gujarat and Arunachal Pradesh, have already notified rules under all four labour codes. Others, such as Uttar Pradesh and Punjab, have implemented only certain rules while continuing to consult on others. States like West Bengal are still in the consultation stage for portions of the framework.

For organisations operating across multiple states, this means there is no single national implementation timeline. Instead of treating compliance as a one-time project, employers should establish a shared tracking mechanism involving finance, HR, legal, and payroll teams. Regular reviews of state-level notifications will help ensure the organisation remains compliant as implementation continues to evolve across different jurisdictions.

Disclaimer

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Labour Code rules are being notified progressively by individual states, and specific obligations can vary by establishment type, sector, and location. Employers should consult a qualified labour law practitioner or com

Leave a Reply