High TDS Deducted by Bank? How to File Form 13 Online to Get Your TDS Rate Lowered

Why Banks Deduct High TDS (And How Form 13 Stops It)

If you’ve ever checked your fixed deposit interest only to find that your bank has already deducted 10% or even 20% as TDS, you’re certainly not the only one. Every year, countless taxpayers across India, including resident individuals, HUFs, and NRIs, end up with more tax deducted than they are actually required to pay. The result is money that remains locked away until they file their income tax return and receive a refund. The most effective way to prevent this cash flow trap is to file Form 13 online through the TRACES portal.

As per the Income Tax Act, by filing Form 13 online through the TRACES portal under Section 197, eligible taxpayers can apply for a lower or even nil TDS certificate. Once approved, the certificate instructs the deductor, whether it is your bank, employer, tenant, or any other payer, to deduct tax at a rate that better reflects your actual tax liability instead of the standard TDS rate.

In this guide, you’ll learn how Form 13 works, who can apply, the documents you’ll need, the complete filing process on the TRACES portal, what happens after you submit your application, and how to deal with revisions or rejections if they arise.

At A Glance: File Form 13 Online

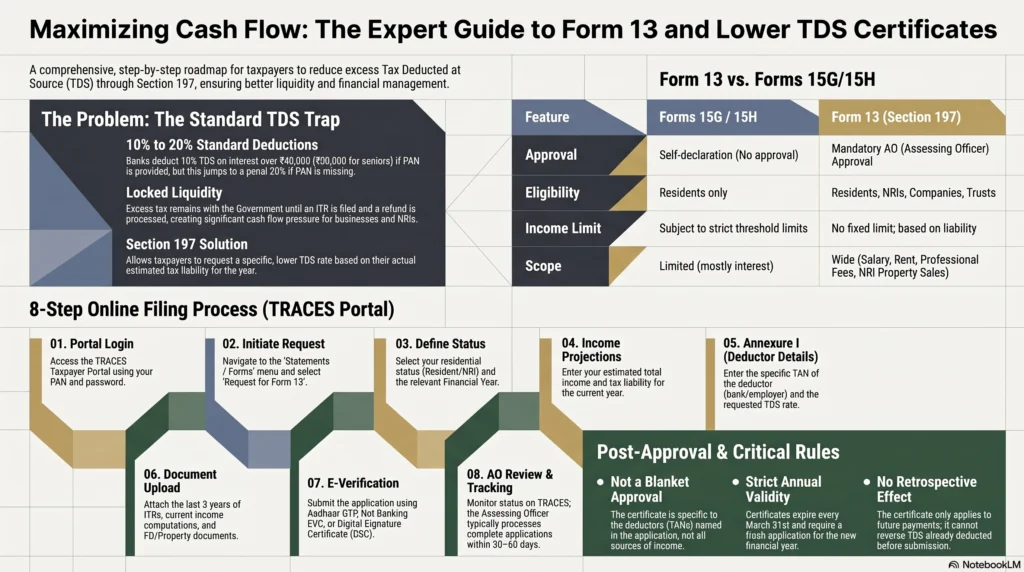

- The Core Issue: Prevent banks from locking up your cash flow with standard 10%–20% TDS deductions.

- The Solution: File Form 13 under Section 197 to get a lower or Nil TDS certificate aligned with your actual tax liability.

- Broad Eligibility: Unlike Forms 15G/15H, Form 13 requires Assessing Officer approval and is open to NRIs, companies, and trusts.

- Key Requirements: You must have a TRACES portal account, the deductor’s exact TAN, and accurate current-year income estimates.

- 100% Online Process: Submit digitally via TRACES by uploading supporting documents (ITRs, FD receipts) and completing e-verification.

- Strict Validity: Certificates are valid only for the current financial year and cannot reverse TDS that has already been deducted.

The Core Problem: Why Banks Deduct High TDS on Your Income

The Mechanics of TDS on Fixed Deposits and Bank Interest

Tax Deducted at Source (TDS) is a system built into the Income Tax Act, 1961, to ensure taxes are collected at the time income is paid. Instead of paying you the full amount, the person or organisation making the payment, whether it’s a bank, employer, tenant, or contractor, deducts tax first and deposits it with the Income Tax Department on your behalf. This deduction happens either when the income is credited to your account or when it is actually paid, whichever comes first. As explained by ClearTax, the recipient receives the balance amount after the tax has been deducted and deposited.

When it comes to interest earned on fixed deposits, recurring deposits, savings accounts, and similar investments, Section 194A of the Income Tax Act governs TDS. Banks generally deduct TDS at 10% once the interest earned crosses ₹40,000 in a financial year, or ₹50,000 in the case of senior citizens. The applicable thresholds and rates are explained in detail in this guide. This standard 10% rate applies when your PAN has been correctly furnished to the bank.

Why Your Bank Might Deduct 20% TDS Instead of 10%

If your bank is deducting TDS at 20% instead of 10%, the most common reason is that your PAN has not been submitted or updated in its records. Under Section 206AA of the Income Tax Act, banks are legally required to deduct tax at the higher of the applicable rate, the prescribed rate, or 20% when a valid PAN is unavailable. They have no discretion to apply a lower rate, even if your actual tax liability is much lower.

Even when your PAN details are up to date, and TDS is deducted at the standard 10%, the amount withheld may still exceed the tax you ultimately owe. Take the example of a retired individual earning ₹3 lakh in interest income across multiple banks. The banks may deduct ₹30,000 as TDS during the year. However, after considering the basic exemption limit, eligible deductions under Section 80C, and other available tax benefits, the person’s final tax liability could be negligible or even nil. In such cases, the excess tax remains with the Income Tax Department until the taxpayer files an income tax return and the refund is processed.

This isn’t a challenge faced only by retirees. Small business owners, professionals, partnership firms, landlords, and many other taxpayers regularly find themselves in a similar situation, where standard TDS deductions create unnecessary pressure on their cash flow.

The Cash Flow Impact of High TDS on Individuals and Businesses

The biggest downside of excess TDS is not the tax itself, but the temporary loss of access to your own money. As explained in this guide , taxpayers cannot recover excess TDS immediately. They must wait until they file their income tax return after the financial year ends, and then wait again for the Income Tax Department to process the refund. If the refund amount is substantial, processing can sometimes take even longer due to additional verification.

For businesses and professionals, this can have a much bigger financial impact. Contractors waiting for project payments, landlords relying on rental income, and NRIs selling property may see a significant portion of their money tied up as TDS. For example, an NRI selling a property worth ₹1.5 crore may have an actual taxable capital gain of only ₹40 lakh. Even so, TDS could exceed ₹22 lakh on the sale consideration, while the actual tax liability may be only around ₹5 to ₹6 lakh. As highlighted by the NRI Tax Service, the difference remains locked with the Income Tax Department until the refund is issued, reducing liquidity and creating an avoidable financial burden.

Decoding Section 197 of the Income Tax Act

What is Section 197 and How Does It Protect Taxpayers?

Section 197 of the Income Tax Act, 1961, gives taxpayers an opportunity to avoid having more TDS deducted than they are actually liable to pay. Instead of accepting the standard TDS rate and waiting for a refund later, eligible taxpayers can apply to the Income Tax Department for permission to have tax deducted at a lower rate or not deducted at all. As explained in this guide, the Assessing Officer reviews the applicant’s estimated income and expected tax liability before deciding whether to issue a lower or nil TDS certificate. Once the certificate is granted, the deductor, whether it’s a bank, employer, tenant, buyer, or another payer, must deduct TDS according to the rate mentioned in the certificate.

The scope of Section 197 extends well beyond bank interest. It covers several categories of income where TDS is commonly deducted, including salary under Section 192, interest on securities under Section 193, dividends under Section 194, bank and fixed deposit interest under Section 194A, contractor payments under Section 194C, insurance commission under Section 194D, lottery commission under Section 194G, commission or brokerage under Section 194H, rent under Section 194I, professional and technical fees under Section 194J, income from mutual fund units under Section 194K, compensation on compulsory acquisition under Section 194LA, payments under Sections 194BB, 194LBC, 194M and 194-O, as well as payments made to non-residents under Section 195. This makes Form 13 useful for a wide range of taxpayers, not just individuals earning interest from fixed deposits.

The Legal Basis for Requesting a Lower TDS Certificate

A certificate issued under Section 197 is commonly known as a lower deduction certificate or nil deduction certificate. Once it has been issued, it serves as a formal legal direction to the deductor. After you submit the certificate to your bank, employer, tenant, or any other deductor, they are authorised to deduct tax only at the rate specified in the certificate, provided they follow its conditions and quote the certificate number in their TDS filings.

As explained by India Filings, the Central Board of Direct Taxes introduced mandatory electronic filing of Form 13 through Notification No. 8/2018 dated 31 December 2018. Since then, both the application process and the certificate itself have been handled through the TRACES portal. The certificate is generated electronically, so there is no requirement for a physical signature. Both the taxpayer and the deductor can download it directly from the portal.

The reason Section 197 exists is straightforward. Standard TDS rates are designed to ensure tax collection, not to reflect every taxpayer’s individual financial position. A senior citizen may have enough deductions and exemptions to owe little or no tax despite earning significant interest income. Likewise, an NRI selling property may have taxable capital gains that are far lower than the property’s sale value after accounting for acquisition cost, improvements, and indexation. Section 197 helps bridge this gap by allowing TDS to be aligned with the taxpayer’s estimated liability before the deduction takes place, instead of relying on the refund process later.

Difference Between Section 197 (Form 13) and Form 15G/15H

Many taxpayers confuse Form 13 with Forms 15G and 15H, but they serve different purposes.

Forms 15G and 15H are self-declarations that resident individuals and HUFs can submit directly to their bank or deductor when they expect their income to remain below the taxable threshold. Form 15G is meant for individuals below 60 years of age, while Form 15H is available to senior citizens. Since these are self-declarations, approval from the Income Tax Department is not required. However, they come with strict eligibility conditions. Form 15G can only be used if the applicant’s total income falls within the prescribed limits, and both forms are restricted to specific TDS provisions. As noted in this guide, NRIs cannot use either Form 15G or Form 15H.

Form 13 follows a different route altogether. It requires a formal application to the Assessing Officer, along with supporting documents and an estimate of your income and tax liability. The certificate is issued only after the department is satisfied that a lower or nil TDS rate is justified.

This also makes Form 13 much more versatile. It applies to residents as well as NRIs, and it can be used by companies, LLPs, partnership firms, trusts, and other entities that are not eligible to submit Forms 15G or 15H. It also covers a much wider range of income categories and can be used even when self-declaration is not legally permitted.

| Feature | Form 15G / 15H | Form 13 (Section 197) |

| Who can file | Resident individuals and HUFs | Residents, NRIs, companies, LLPs, firms, trusts, and other entities |

| Approval required | No. Self-declaration | Yes. Approval from the Assessing Officer is mandatory |

| Income threshold | Subject to prescribed eligibility conditions | No fixed income limit. Based on estimated tax liability |

| TDS sections covered | Limited, mainly Section 194A | Covers multiple TDS provisions, including Section 195 |

| NRI eligibility | Not permitted | Permitted |

| Filing method | Submitted directly to the deductor | Filed online through the TRACES portal |

What is Form 13 and Who is Eligible to File It?

Understanding the Purpose of Income Tax Form 13

Form 13 is the prescribed application under Section 197 of the Income Tax Act for taxpayers who want tax to be deducted at a lower rate, or not deducted at all, because their actual tax liability is lower than the standard TDS rate. As explained here, it is neither a tax return nor a self-declaration. Instead, it is a formal request asking the Assessing Officer to review your estimated income, tax liability, and compliance history before deciding whether lower TDS should be allowed.

If the Assessing Officer is satisfied that your request is justified, a certificate is issued specifying either the reduced TDS rate or the maximum amount up to which tax need not be deducted. The certificate is generated electronically through the TRACES portal and can be downloaded by both the taxpayer and the deductor.

One important point to remember is that a Form 13 certificate is issued for specific deductors. It is not a blanket approval covering every source of income. For example, if you have fixed deposits with three different banks and want lower TDS on the interest from each one, you’ll need to include all three banks, along with their respective TANs, in your application.

Eligibility Criteria for Resident Individuals and HUFs

Resident individuals and Hindu Undivided Families (HUFs) can apply for Form 13 if they expect their actual tax liability for the financial year to be lower than the TDS that would normally be deducted. There is no fixed income ceiling that determines eligibility. What matters is whether the standard TDS exceeds the tax you are genuinely expected to pay.

This situation can arise in several ways. A salaried employee may be eligible because of substantial deductions and exemptions. A pensioner may fall below the taxable limit after considering the available reliefs. A self-employed professional or business owner may have losses or deductions that significantly reduce the final tax liability. In all these cases, applying for lower TDS can help avoid unnecessary deductions during the year.

The Assessing Officer considers several factors before granting approval, including your income tax returns from previous years, overall income pattern, advance tax payments, and the income estimate submitted with the application. As explained by TaxBuddy, taxpayers under both the old and the new tax regime can apply. The deciding factor is the estimated tax payable, not the regime they have chosen.

Eligibility for NRIs, Companies, and Other Entities

Form 13 is equally valuable for NRIs, companies, LLPs, partnership firms, trusts, and other entities that face TDS deductions exceeding their actual tax liability.

For NRIs, one of the most common situations involves the sale of property in India. Under Section 195, TDS is deducted on payments made to non-residents. Even when the actual taxable capital gain is relatively small after accounting for the property’s purchase cost, improvements, and indexation, the TDS deducted can still be substantial. As discussed at https://nriway.in/blog/lower-tds-certificate-for-nris-form-13, obtaining a lower TDS certificate through Form 13 can significantly reduce the amount blocked until the income tax refund is processed.

The same principle applies to companies, Limited Liability Partnerships, partnership firms, Associations of Persons (AOPs), Bodies of Individuals (BOIs), trusts, and other entities. If the expected tax liability is lower than the TDS that would otherwise be deducted, they can seek relief by applying for a lower or nil deduction certificate under Section 197.

Qualifying Income Types (Interest, Salary, Rent, NRI Property Sale)

Form 13 is not restricted to bank interest. It can be used for a wide variety of income streams where TDS is applicable. Some of the most common examples include:

- Fixed deposit interest and other bank interest under Section 194A.

- Salary income under Section 192 where the employer’s estimated TDS exceeds the employee’s actual liability.

- Rental income under Section 194I where tenants are required to deduct TDS on eligible payments.

- Professional and technical fees under Section 194J for consultants, doctors, lawyers, and other professionals.

- Commission or brokerage under Section 194H.

- Payments to contractors under Section 194C.

- Dividends under Section 194.

- Income received by NRIs, including property sale proceeds, rental income, interest from NRO accounts, and capital gains under Section 195.

The Income Tax Department also provides guidance on certificates for lower or nil TDS.

Essential Prerequisites Before Filing Form 13 Online

Mandatory TRACES Portal Registration

Before you can apply for a lower or nil TDS certificate, you must be registered on the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal. The entire Form 13 process, from submitting the application to tracking its status and downloading the certificate, is handled online through https://www.tdscpc.gov.in.

If you haven’t registered yet, the process is straightforward. Visit the portal, click Login, select Register as New User, choose Taxpayer, and complete the registration using your PAN and the required personal details. Detailed registration instructions are also provided by the Income Tax Department.

If you’re an NRI applying for a lower TDS certificate, make sure your PAN is active and properly linked to your TRACES account before starting the application.

Gathering TAN Details of the Deducting Banks

One of the most important details you’ll need is the TAN (Tax Deduction Account Number) of every deductor from whom you’re seeking lower TDS. Since the certificate issued under Section 197 is deductor-specific, it cannot be issued without the correct TAN.

For bank interest, this means obtaining the TAN of the specific bank branch where your fixed deposit or account is held. It’s important not to confuse the TAN with the branch’s IFSC code, as they serve entirely different purposes.

You can usually find the TAN by:

- Asking your bank branch directly.

- Referring to an earlier Form 16A issued by the bank.

- Using the TAN search facility on https://www.incometax.gov.in.

As highlighted by TaxBuddy, incorrect or missing TAN details are among the most common reasons why Form 13 applications are delayed or rejected. Taking a few extra minutes to verify these details can save considerable time later.

Estimating Current Year Income and Final Tax Liability

The success of your Form 13 application depends largely on how accurately you estimate your income and tax liability for the current financial year.

You’ll need to prepare a realistic estimate of income from every applicable source, including salary, bank interest, rental income, business profits, professional receipts, and capital gains. After that, calculate your expected tax liability after considering all eligible deductions, exemptions, and tax benefits.

The objective is simple. If the TDS likely to be deducted during the year is higher than your estimated tax liability, you have a valid basis for applying under Section 197.

Your estimates should also be backed by credible financial records. The Assessing Officer compares your projections with income tax returns filed in previous years, so any major variation should be supported by proper documentation. For example, if your income has fallen because you’ve retired, closed a business, changed jobs, or your fixed deposits have matured, be prepared to provide evidence supporting those changes. Well-documented applications are generally processed more smoothly than those based on unsupported estimates.

E-Verification Setup (Aadhaar OTP, Net Banking, or DSC)

A Form 13 application is not complete until it has been electronically verified.

TRACES currently allows applicants to verify their submission using one of the following methods:

- Aadhaar OTP, provided your PAN is linked with Aadhaar and your mobile number is registered with Aadhaar.

- Electronic Verification Code (EVC) through net banking.

- Digital Signature Certificate (DSC).

As noted in this guide, companies, LLPs, and professionals often prefer using a DSC because it provides a seamless verification process. Individual taxpayers, on the other hand, generally find Aadhaar OTP or net banking verification more convenient.

Whichever method you choose, it’s worth checking that everything is set up before you begin filing. Ensuring your Aadhaar-PAN linkage is active or that your DSC is valid can help you avoid unnecessary delays when you’re ready to submit the application.

Comprehensive Document Checklist for Form 13 Application

Submitting a well-prepared application can make a significant difference to how quickly your Form 13 request is processed. The Assessing Officer bases the decision largely on the documents you provide, so missing, incomplete, or inconsistent records often lead to queries, delays, or even rejection.

Personal and Identity Documents

Start by gathering the basic identity documents required for your application. These generally include:

- PAN card of the applicant.

- Aadhaar card, particularly if you plan to complete e-verification using Aadhaar OTP.

- Passport, if you’re applying as an NRI.

- For companies, LLPs, or partnership firms, the Certificate of Incorporation or Registration, along with the PAN of the entity and its directors or partners.

Having these documents ready before you begin filing will make the application process much smoother.

Income Tax Returns (ITR) and Assessment Orders of Past Years

One of the first things the Assessing Officer reviews is your tax compliance history. In most cases, you’ll be expected to submit copies of your Income Tax Returns for the previous three assessment years, along with the corresponding ITR acknowledgements (ITR-V). As outlined in this guide, these documents help establish your income pattern and filing history.

If you’ve received assessment orders under Sections 143(1), 143(3), or 144 for any of those years, it’s advisable to include them as well. They provide additional evidence of your tax compliance and may help the Assessing Officer evaluate your application more efficiently.

Applicants who haven’t filed returns regularly or have pending assessments should be prepared for closer scrutiny during the review process.

Current Year Estimated Profit and Loss or Income Computation

A key part of your application is demonstrating what you expect to earn during the current financial year and how that translates into your estimated tax liability.

The supporting documents will depend on the nature of your income:

- Salaried individuals should ideally provide recent salary slips and, where available, a projected Form 16.

- Self-employed professionals and business owners should prepare an estimated Profit and Loss account or an income statement for the current year.

- NRI applicants should include a detailed income computation covering expected income in India, capital gains calculations where applicable, any available DTAA (Double Taxation Avoidance Agreement) benefits, and the resulting estimated tax liability.

Supporting records such as bank statements, rental agreements, FD receipts, investment statements, or property sale agreements can strengthen the application by substantiating the figures you’ve declared.

Specific Documents Required for Bank Interest and Fixed Deposits

If your primary objective is to reduce TDS on fixed deposit or bank interest, you’ll also need documents that specifically support your interest income.

These typically include:

- Fixed deposit certificates or FD advice issued by your bank.

- Interest statements for the previous three financial years, wherever available.

- TAN details of every bank branch from which you’re seeking lower TDS.

- Bank passbooks or account statements showing interest credits.

- Form 26AS or the Annual Information Statement (AIS), reflecting any TDS already deducted during the current financial year.

A complete checklist of supporting documents, including additional annexure requirements, is available in this guide.

Providing clear, legible, and consistent documentation from the outset greatly improves the likelihood of a faster review and reduces the chances of the Assessing Officer requesting further clarification.

Step-by-Step Guide: How to File Form 13 Online on TRACES

Once you’ve completed the prerequisites and gathered the required documents, you’re ready to file Form 13 online. The entire process is completed through the TRACES portal, so there’s no need to submit any physical paperwork. If you’d like to see the official format before you begin, a draft of Form 13 is available here.

Step 1: Log in to the TRACES Taxpayer Portal

Visit https://www.tdscpc.gov.in and log in using your PAN as the User ID, your password, and the CAPTCHA displayed on the screen. Make sure you’re signing in as a Taxpayer, not as a Deductor or Tax Professional.

Once you’ve logged in successfully, you’ll be taken to the taxpayer dashboard, where you’ll find various services related to TDS, including the option to file Form 13.

Step 2: Navigate to the Form 13 Request

From the dashboard, open the Statements / Forms menu and select Request for Form 13.

This will launch the online application form where you’ll enter your details and upload the required documents. As explained by India Filings, the portal guides applicants through the filing process section by section, making it easier to complete the application accurately.

Step 3: Select Your Residential Status and Financial Year

The first part of the application requires some basic information about your request. You’ll need to specify:

- Your residential status, such as Resident, Non-Resident, or Not Ordinarily Resident.

- The financial year for which you’re applying for the lower or nil TDS certificate.

- Whether you’re requesting a lower TDS rate or a nil deduction certificate.

Take extra care while selecting your residential status. For example, if you’re an NRI but mistakenly choose “Resident,” the information submitted will be incorrect and may create complications during processing or affect the validity of the certificate. Additional guidance on the TRACES interface is available here.

Step 4: Enter Your Basic Details

Many personal details are automatically pulled from the PAN database, including your name, date of birth or incorporation, and address. You’ll still need to review the information carefully and provide or confirm additional details such as:

- Registered email address.

- Mobile number.

- PAN.

- Category of applicant, such as Individual, HUF, Company, LLP, or another entity.

NRI applicants may also be asked to provide details such as their country of residence and passport number. Ensure your contact information is accurate, as the Assessing Officer may use these details to communicate if additional clarification is needed.

Step 5: Provide Your Estimated Income and Tax Liability

This is one of the most important sections of the application because it forms the basis of your request for lower TDS.

You’ll be asked to enter:

- Your estimated total income for the current financial year.

- Your estimated tax liability on that income.

- Advance tax already paid, if any.

- TDS already deducted during the year, as reflected in Form 26AS or the Annual Information Statement (AIS).

- Any self-assessment tax paid.

The Assessing Officer relies heavily on these figures when deciding whether a lower deduction certificate should be issued. As explained by TaxBuddy, it’s essential that the information entered matches the supporting documents you upload.

Step 6: Complete Annexure I

Annexure I is where you provide deductor-specific information. Since a Form 13 certificate is issued separately for each deductor, you’ll need to enter these details individually.

For every deductor, you’ll typically need to provide:

- TAN of the deductor.

- Name and address of the deductor.

- Nature of income, such as interest, rent, or professional fees.

- Applicable TDS section, for example, Section 194A for fixed deposit interest.

- Estimated income expected from that deductor during the financial year.

- The lower TDS rate you’re requesting, or the amount up to which no TDS should be deducted.

If you’re seeking lower TDS from multiple bank branches, you’ll need a separate Annexure I entry for each branch’s TAN.

Be especially careful while entering TAN details and selecting the correct TDS section. Errors here are one of the most common reasons applications are delayed or rejected. As noted in this guide, the certificate applies only to the deductors specifically named in the application.

Step 7: Upload the Required Supporting Documents

After completing the form, you’ll be prompted to upload supporting documents.

Depending on your circumstances, these may include:

- PAN card.

- ITR acknowledgements for the previous three years.

- Current year’s estimated income computation.

- Estimated Profit and Loss account or income statement.

- Fixed deposit certificates or interest statements.

- Property sale agreement and capital gains computation for NRI property transactions.

- Advance tax challans, where applicable.

- Chartered Accountant’s certificate of estimated income, particularly for businesses and many NRI applications.

Most documents are accepted in PDF or JPEG format, subject to file size limits. Before uploading, ensure every document is complete, clearly readable, and consistent with the information you’ve entered in the application. Incomplete or poor-quality uploads frequently lead to additional queries from the Assessing Officer.

Step 8: Review, Verify, and Submit

Before submitting your application, the TRACES portal provides a final summary for review.

Take a few minutes to verify:

- All deductor TANs.

- Estimated income and tax calculations.

- The list of uploaded documents.

- Contact details and applicant information.

Once you’ve confirmed everything is accurate, complete the application using your preferred e-verification method, whether that’s Aadhaar OTP, EVC through net banking, or a Digital Signature Certificate.

After successful verification, the portal generates an acknowledgement number. Keep this number safe, as you’ll need it to track the status of your application and respond to any future communication from the Income Tax Department. As outlined in this guide, the application is then forwarded electronically to your jurisdictional TDS Assessing Officer for review.

Tracking, Processing, and Approvals

Submitting Form 13 is only the first step. Once your application reaches the Income Tax Department, it goes through a review process before a lower or nil TDS certificate is issued. Understanding what happens at this stage can help you respond promptly if additional information is requested and avoid unnecessary delays.

How the Assessing Officer (AO) Evaluates Your Application

After your application is submitted, it is forwarded to your jurisdictional Assessing Officer (AO). The AO reviews several aspects of your application before making a decision.

Some of the key factors considered include:

- Whether your estimated income is reasonable when compared with the income reported in your income tax returns over the past three years.

- Whether your estimated tax liability genuinely supports a lower or nil TDS deduction.

- Whether you have paid any applicable advance tax.

- Whether there are any outstanding tax demands or compliance issues against your PAN.

As explained here, the AO may also look at your overall tax compliance history and consider whether similar applications have been made in previous years.

Based on this review, the AO may:

- Approve the TDS rate you’ve requested.

- Approve a different lower TDS rate.

- Reject the application if the evidence provided does not justify the request.

If approved, the certificate is generated electronically through the TRACES portal. Since it is system-generated, no physical signature is required.

Checking Your Form 13 Application Status Online

You don’t have to wait for an email or letter to know what’s happening with your application. The TRACES portal allows you to track its progress at every stage.

Simply log in to your account, open the Statements / Forms section, and select the option to check the status of your Form 13 application.

The application typically moves through the following stages:

- Submitted

- Forwarded to AO

- Under Processing

- Clarification Required

- Approved

- Rejected

It’s a good idea to check the status regularly, especially during the first few weeks after submission, so you can respond quickly if the department requests additional information.

You can also find related updates and taxpayer services on the Income Tax Department’s portal.

Handling Queries and Requests for Additional Information from the AO

Not every application is approved immediately. If the Assessing Officer needs more information, your application status will change to indicate that clarification is required.

The AO may ask for:

- Additional supporting documents.

- Clarification regarding your estimated income.

- A revised income computation.

- Explanations for differences between your current estimates and previous tax returns.

These requests can usually be answered online through the TRACES portal by uploading the required documents and providing the necessary explanations.

Responding promptly is important. Ignoring or delaying a response may result in your application being rejected or closed without any further action. As highlighted in this guide, timely and complete responses generally improve the chances of obtaining approval.

Standard Timelines for Issuance of the Certificate

The Income Tax Act does not prescribe a fixed deadline for processing Form 13 applications. However, in practice, applications that are complete and supported by proper documentation are often processed within 30 to 60 days.

Timing also plays an important role.

If you apply early in the financial year, ideally in April or May, there’s a better chance of receiving the certificate before significant income is credited and TDS begins accumulating. Waiting until the latter part of the financial year may reduce the practical benefit, since a large portion of the tax may already have been deducted by then.

For NRIs involved in property transactions, planning ahead is particularly important. As explained in this guide , the application should ideally be submitted well before the property sale is completed. Once TDS has been deducted without a lower deduction certificate in place, the excess amount cannot be refunded by the buyer or deductor. It can only be claimed later by filing an income tax return and waiting for the refund to be processed.

What to Do Once the Lower TDS Certificate is Issued

Receiving approval for your Form 13 application is only part of the process. To actually benefit from the lower or nil TDS rate, you’ll need to download the certificate and ensure it reaches the relevant deductor. Here’s what you should do next.

Downloading the Certificate from TRACES

Once your application is approved, the lower TDS certificate becomes available for download through the TRACES portal under the Statements / Forms section. As explained by India Filings, both you and the deductor named in the application can access the certificate through your respective TRACES accounts.

The certificate contains important details, including:

- Certificate number.

- Name and PAN of the applicant.

- Name and TAN of the deductor.

- Nature of the income covered.

- Relevant TDS section.

- Approved TDS rate or the maximum amount eligible for nil deduction.

- Certificate validity period.

Before sharing the certificate with the deductor, take a moment to review these details and make sure everything is accurate.

Submitting the Certificate to Your Bank

After downloading the certificate, the next step is to provide it to the bank or any other deductor named in the certificate. Many banks now accept the certificate digitally through email, while others may ask you to submit it through your relationship manager or at the branch.

Once the deductor receives a valid certificate, they are legally required to deduct TDS at the rate specified in it and quote the certificate number in their TDS returns.

Keep in mind that the certificate only affects future payments. If TDS was deducted before the certificate was submitted, the bank cannot refund or reverse those deductions. Instead, that tax will continue to appear as credit in your Form 26AS and can be adjusted against your final tax liability when you file your income tax return.

To avoid unnecessary deductions, it’s always a good idea to submit the certificate to the deductor as soon as you receive it.

Validity Period and Expiry Rules of the Certificate

A lower or nil TDS certificate issued under Section 197 does not remain valid indefinitely. It is generally issued for a specific financial year or, in some cases, for a shorter period determined by the Assessing Officer.

As explained in this guide, unless the certificate specifically states otherwise, it is usually valid from the date of issue until 31 March of the relevant financial year. The Assessing Officer also has the authority to specify a shorter validity period or cancel the certificate if circumstances warrant.

The certificate does not renew automatically. If you expect to continue receiving income that attracts TDS, such as fixed deposit interest, rental income, professional fees, or similar payments, you’ll need to submit a fresh Form 13 application for the next financial year.

Applying early each year helps ensure that the new certificate is in place before fresh TDS deductions begin.

Common Reasons for Form 13 Rejection and How to Avoid Them

Even if you’re eligible for a lower or nil TDS certificate, approval isn’t automatic. The Assessing Officer reviews every application carefully, and inaccuracies or missing information can result in delays or rejection. Knowing the common pitfalls beforehand can improve your chances of getting your application approved the first time.

Mismatch Between Estimated Income and Past Tax Records

One of the most common reasons for rejection is a significant mismatch between the income you’ve projected for the current financial year and the income reported in your previous tax returns.

For example, if your ITRs over the last three years consistently show an annual income of around ₹15 lakh, but your Form 13 application estimates only ₹3 lakh without any explanation, the Assessing Officer is likely to question the figures. Simply stating a lower income is rarely enough.

If your income has genuinely fallen because you’ve retired, changed jobs, shut down a business, or experienced other major financial changes, support your application with relevant documents. Depending on your situation, this could include a retirement letter, employment termination letter, business closure documents, medical records, or any other evidence that explains the decline.

Similarly, if you’re claiming substantial deductions that significantly reduce your tax liability, make sure they’re backed by proper documentation. Unsupported estimates often invite additional scrutiny and may delay the approval process.

Incorrect or Missing TAN Details

Since a Form 13 certificate is issued for specific deductors, entering the correct TAN is essential.

If you provide the wrong TAN in Annexure I, the certificate may be issued for the wrong deductor or become unusable for the intended one. In that situation, the actual bank or deductor will continue deducting TDS at the normal rate because it isn’t covered by the certificate.

Before submitting your application, verify every TAN carefully. You can:

- Confirm the TAN directly with the bank or deductor.

- Check a previously issued Form 16A.

- Use the TAN search facility available on https://www.incometax.gov.in.

Taking a few minutes to verify these details can prevent unnecessary delays and save you from filing corrections later.

Not Responding to Queries from the Assessing Officer

During the review process, the Assessing Officer may ask for additional documents or clarification before making a decision. Receiving such a query doesn’t mean your application will be rejected. In many cases, it’s simply part of the verification process.

However, failing to respond within the prescribed time can lead to the application being rejected or closed without further action.

After filing Form 13, make it a habit to check your TRACES account regularly for updates. If you’ve authorised a Chartered Accountant or tax consultant to handle the application, ensure they also have access to monitor the portal and respond promptly to any departmental communication.

Providing complete and timely responses not only helps keep your application moving but also improves the likelihood of receiving the lower or nil TDS certificate without unnecessary delays.

Filing Revisions for Form 13 on TRACES

Sometimes, after submitting Form 13, you may realise that certain information needs to be corrected. In other cases, your financial situation may change while the application is still being processed. The TRACES portal allows revisions in specific circumstances, but what you can change depends largely on the stage your application has reached.

When Can You File a Revision Request?

A revision request is generally permitted if there’s a genuine change in your estimated income or you’ve discovered an error in the original application after submission.

As explained by TaxBuddy, revisions are usually allowed while the application is still under processing and before the Assessing Officer has issued the certificate. During this stage, the department can still consider updated information before making a final decision.

If the certificate has already been issued, revisions become much more limited, so it’s always best to review your application carefully before submitting it.

What Can Be Changed in a Revision?

The type of changes you can make depends on whether the certificate has been issued.

Before the certificate is issued

If your application is still awaiting approval, you can generally request changes such as:

- Email address or mobile number.

- Residential or correspondence address.

- Estimated income figures.

- Details of the deductor.

- The lower TDS rate or nil deduction being requested.

If you’re revising financial information, it’s a good idea to upload updated supporting documents along with the revised application. This helps the Assessing Officer understand why the changes were made and reduces the likelihood of further queries.

After the certificate is issued

Once the lower TDS certificate has been generated, only limited corrections are usually allowed. These are generally restricted to basic contact information, such as your email address or mobile number.

The key financial details approved by the Assessing Officer, including:

- The TDS rate.

- Estimated income.

- Deductor’s TAN.

- Nature of income covered.

cannot normally be changed after the certificate has been issued.

If there’s a major change in your financial circumstances after approval, it may be more appropriate to seek professional advice to determine whether a fresh application is required for the current year or whether the issue should be addressed in the following financial year’s Form 13 application.

Situations Where Revisions Are Not Allowed

The revision facility is intended to correct genuine errors or update information while an application is being processed. It cannot be used to fundamentally alter an approved certificate.

For example, revision requests are generally not accepted if they attempt to:

- Change an approved lower TDS rate to a nil deduction after the certificate has already been issued.

- Add new deductors who weren’t included in the original application.

- Change the nature of income, such as replacing professional income with capital gains.

- Expand the scope of an existing certificate beyond what was originally approved by the Assessing Officer.

In situations like these, a fresh Form 13 application is usually required because the Assessing Officer must evaluate the new facts independently.

Using the revision process only for legitimate corrections helps avoid unnecessary complications and supports smoother processing of future Form 13 applications.

Frequently Asked Questions (FAQ): File Form 13 Online

Yes, you can file Form 13 online on the TRACES portal at any time during the financial year. However, the lower TDS certificate only applies to future interest credits. It cannot reverse tax that the bank has already deducted. To recover the excess tax, you must claim the 20% TDS as a refund when filing your annual Income Tax Return (ITR).

Forms 15G and 15H are mere self-declarations submitted directly to the bank, available only to resident individuals whose total income falls below the taxable threshold. In contrast, Form 13 (Section 197) requires formal Assessing Officer approval, has no strict income ceiling, and is mandatory for NRIs, companies, LLPs, and trusts seeking a lower deduction rate.

Absolutely. A valid, active PAN is mandatory for both residents and NRIs to register on the TRACES portal and submit the Form 13 application. Without a PAN, banks are legally bound under Section 206AA to deduct TDS at a penal rate of 20%, and no lower deduction certificate can be issued.

While there is no fixed statutory deadline, approval typically takes 30 to 60 days provided your application is complete. To prevent rejection or delays, ensure your current estimated income aligns logically with past ITRs and always enter the correct TAN (Tax Deduction Account Number) for your specific bank branch.

The certificate is strictly valid only for the current financial year, automatically expiring on March 31st. Because it does not auto-renew, taxpayers must submit a fresh Form 13 application annually to continue benefiting from a lower TDS rate.

Can I file Form 13 in the middle of the financial year if TDS has already been deducted?

Yes. You can submit Form 13 at any time during the financial year. However, the certificate only applies to future payments made after it has been approved and submitted to the deductor. Any TDS deducted before that cannot be reversed by the bank or other deductor. Instead, the deducted amount will appear in your Form 26AS and can be adjusted against your final tax liability when you file your income tax return.

Is Form 13 available under the new tax regime?

Yes. Section 197 is available regardless of whether you’ve opted for the old or the new tax regime under Section 115BAC. As long as your estimated tax liability is lower than the TDS that would normally be deducted, you can apply for a lower or nil TDS certificate.

How long is a lower TDS certificate valid?

A lower TDS certificate is generally valid from the date it is issued until 31 March of the relevant financial year, unless the Assessing Officer specifies a shorter validity period or cancels it earlier. It does not renew automatically, so if you expect to receive similar income in the following financial year, you’ll need to submit a fresh Form 13 application.

Do NRIs need an Indian PAN to apply for Form 13?

Yes. A valid PAN is mandatory for filing Form 13 through the TRACES portal. Without a PAN, you won’t be able to register on TRACES or complete the application process. NRIs who don’t already have one should apply for a PAN before seeking a lower TDS certificate.

What should I do if my bank continues deducting TDS after I submit the certificate?

Once you’ve provided a valid lower TDS certificate, the bank is legally required to deduct tax according to the rate specified in the certificate. If it continues deducting TDS at the higher rate, you should first contact the bank’s branch or grievance officer and request that the deduction be corrected.

If the issue remains unresolved, you can escalate the matter by submitting a written complaint to your jurisdictional Assessing Officer as well as the Assessing Officer linked to the bank’s TAN. Any excess TDS deducted will still be reflected in your Form 26AS and can be claimed as a refund when you file your income tax return.

Disclaimer

This article is for informational purposes and does not constitute legal or tax advice. Tax rules and portal procedures are subject to change. Taxpayers are advised to consult a qualified Chartered Accountant or tax professional for advice specific to their situation. The applicable TDS portal is https://www.tdscpc.gov.in and the income tax e-filing portal is https://www.incometax.gov.in.

Leave a Reply