ITR 2026 Filing: Investment Taxation Under the Income Tax Act 2025 Guide

Income Tax Act 2025: Transitioning from the 1961 Framework

The Income Tax Act 2025 marks one of the biggest overhauls in India’s direct tax system in more than 60 years. Effective from April 1, 2026, it replaces the long-standing Income Tax Act of 1961 and introduces a framework that is cleaner, more structured, and far easier to navigate, at least on paper. For investors, though, the changes go well beyond simplified language. Whether you’re salaried, self-employed, retired, or managing investments as an NRI, the new law changes how you approach tax planning, compliance, and ultimately, your ITR 2026 filing.

This guide is built to help you make sense of what actually matters. We’ll walk through the key investment-related changes under the new framework, from the revised 12.5% long-term capital gains tax on equity, to the split treatment of debt mutual funds, to how fixed deposit interest is taxed, and where capital losses can still work in your favour.

If you’re filing your Income Tax Return for Assessment Year (AY) 2026–27, covering income earned during FY 2025–26, you’re effectively filing during the transition into the Income Tax Act 2025 regime. And that transition isn’t just a legal technicality. It affects how gains are calculated, how exemptions are claimed, how losses are carried forward, and even how foreign income may need to be reported. In other words, understanding the new framework now can save a lot of confusion later.

ITR 2026 at a Glance: Key Policy & Tax Changes

If you are preparing your investment portfolio for the upcoming filing season, these are the core statutory changes and transition rules you must apply:

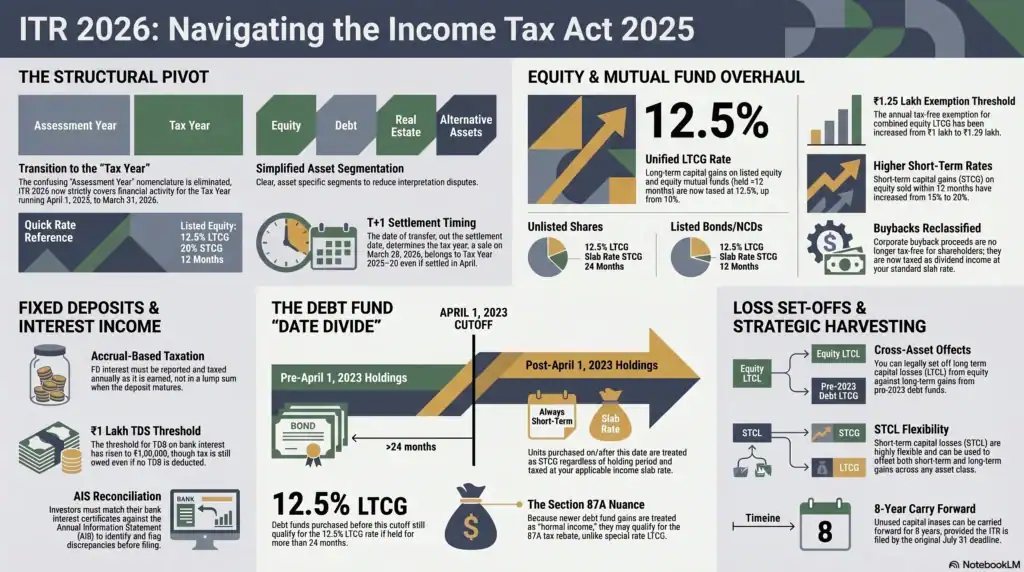

- The End of the “Assessment Year”: The Income Tax Act 2025 eliminates the confusing two-year nomenclature. ITR 2026 strictly covers your financial activity for the new Tax Year running from April 1, 2025, to March 31, 2026.

- Equity LTCG Raised to 12.5%: Long-term capital gains on listed equity and equity mutual funds are now taxed at a flat 12.5%. However, the tax-free exemption limit has been increased to ₹1.25 lakh per financial year.

- The Debt Fund Divide: Your debt mutual fund taxation depends entirely on the purchase date. Investments made before April 1, 2023, qualify for 12.5% LTCG. Investments made on or after April 1, 2023, are taxed purely as short-term capital gains (STCG) at your applicable slab rate.

- Buybacks Taxed as Dividends: Under the amended rules, corporate buyback proceeds are no longer tax-free in the hands of the shareholder. They are now taxed as dividend income at your standard slab rate, while the acquisition cost is treated as a capital loss.

- FD Interest on Accrual: Fixed deposit interest must be reported and taxed annually as it accrues, not when it matures. Ensure your AIS (Annual Information Statement) matches your bank’s yearly interest certificate to avoid TDS mismatches.

- Cross-Asset Set-Offs: Strategic tax harvesting is highly effective. You can legally set off long-term capital losses (LTCL) from equity against long-term capital gains (LTCG) from pre-2023 debt funds.

The Structural Shift: Transitioning from the 1961 Act to the 2025 Framework

For decades, India’s Income Tax Act of 1961 was the backbone of direct taxation, but it also became increasingly difficult to work with. Over the years, layers of amendments, provisos, explanations, and cross-references turned it into something even experienced chartered accountants sometimes had to untangle twice. By the time it crossed 800 sections and countless interpretive notes, the law had become functional, yes, but hardly intuitive.

That’s where the Income Tax Act 2025 steps in.

Introduced as the Income Tax Bill 2025 during the Union Budget session and set to take effect from April 1, 2026, the new legislation aims to simplify not just language, but structure. Chapters have been reorganised, definitions cleaned up, and compliance provisions made easier to trace. The overhaul isn’t simply an old law wearing a new label. The changes include revised tax slabs, updated deduction thresholds, rationalised TDS provisions, and a much more streamlined capital gains framework.

For investors, though, the most meaningful shift isn’t necessarily the slab revision; it’s the way capital gains rules have been restructured. Under the new act, tax treatment for equity, debt instruments, real estate, and alternative assets is laid out in clearer, asset-specific segments. In practical terms, that reduces interpretation disputes and makes compliance more straightforward. The trade-off? Taxpayers who were used to navigating the old section references now have to relearn where everything lives.

Defining the “Tax Year” vs. “Assessment Year” for 2026 Filings

If there was one concept that routinely confused taxpayers under the old system, it was the distinction between the “previous year” and the “assessment year.” Income earned during one financial period would be taxed in the following assessment year, which is technically correct, but often confusing in practice.

The Income Tax Act 2025 finally addresses that.

As highlighted in this analysis, the old terminology has been replaced with a simpler concept: the tax year. From April 1, 2026 onward, your tax year aligns directly with your financial year, April 1 to March 31. There is no separate terminology and no unnecessary mental gymnastics.

For the purposes of ITR 2026, this means income earned between April 1, 2025, and March 31, 2026, falls into the relevant tax period and must generally be reported by July 31, 2026, unless the Income Tax Department issues an extension at its official portal.

For capital gains, timing still matters. The date of transfer, not necessarily the settlement date, is what determines which tax year the gain belongs to. So, if you sold listed equity units on March 28, 2026, that gain belongs to Tax Year 2025–26, even if the settlement happened on March 31 under the T+1 cycle. That small detail can matter a lot when you’re matching broker statements against your AIS.

The Legislative Intent: Why the 2025 Act Rewrote Capital Gains

The capital gains rewrite didn’t happen overnight. In many ways, the July 2024 Union Budget laid the groundwork.

Before those changes, India’s capital gains system had become messy. Different asset classes had different holding periods. Equity and debt were taxed differently. Indexation is applied in some cases but not others. Surcharge rates varied depending on the asset. Even seasoned investors often needed spreadsheets just to model post-tax outcomes.

That complexity is exactly what the 2025 Act tries to fix.

As discussed in this mutual fund taxation guide, the July 2024 Budget introduced several structural changes that now sit at the heart of the new law.

Among the biggest:

- A unified 12.5% LTCG rate across most major asset classes

- A higher ₹1.25 lakh annual exemption for equity LTCG

- Removal of indexation benefits in most standard cases

- A revised 20% STCG rate for listed equity and equity-oriented mutual funds

These changes, analysed in greater depth by tax experts, signal a broader policy shift: less complexity, fewer exceptions, and a tax framework designed to be more predictable, even if, for some investors, not always cheaper.

Equity Taxation: Navigating the 12.5% LTCG Regime

For equity investors, whether you invest through direct stocks or equity mutual funds, one of the biggest tax changes in ITR 2026 is the revised treatment of long-term capital gains.

Under the Income Tax Act 2025, gains from listed equity shares and equity-oriented mutual funds held for more than 12 months now attract a flat 12.5% long-term capital gains (LTCG) tax. That’s an increase from the earlier 10% rate under Section 112A of the 1961 Act. On the flip side, the exemption threshold has also been raised from ₹1 lakh to ₹1.25 lakh per financial year. Short-term capital gains (STCG), applicable where equity is sold within 12 months, are now taxed at 20%, up from the earlier 15%.

These updated rates are reflected in the detailed breakdown available in this guide, which confirms both the revised LTCG and STCG rates for equity-oriented investments.

The ₹1.25 Lakh Exemption: Practical Calculation Examples

One point investors often misunderstand is how this exemption actually works.

The ₹1.25 lakh exemption applies per taxpayer, per financial year, and it applies to the combined total of long-term gains from listed equity shares, equity mutual funds, and units of business trusts. It does not apply separately across different investments, brokers, or fund houses. Think of it as one common pool.

Here’s what that looks like in practice:

Example 1 — Gains Below the Exemption Limit

Suppose you redeem equity mutual fund units and book an LTCG of ₹1.20 lakh during FY 2025–26. Since your gains remain below the ₹1.25 lakh threshold, your tax liability is nil.

This interpretation is supported by the example discussed in this analysis, which confirms that no tax is payable when annual equity LTCG stays below the exemption limit.

Example 2 — Gains Above the Exemption Limit

Now, assume your total equity LTCG is ₹3.50 lakh.

Your taxable gain would be:

₹3.50 lakh – ₹1.25 lakh = ₹2.25 lakh

Tax calculation:

₹2.25 lakh × 12.5% = ₹28,125

Health and Education Cess @ 4% = ₹1,125

Total tax payable = ₹29,250

Example 3 — Both STCG and LTCG in the Same Year

Let’s say you have:

- ₹2 lakh LTCG from equity mutual funds

- ₹80,000 STCG from shares sold within 12 months

Your tax works out as:

LTCG = (₹2 lakh – ₹1.25 lakh) × 12.5% = ₹9,375

STCG = ₹80,000 × 20% = ₹16,000

Total tax before cess = ₹25,375

A small but important detail: if your annual LTCG is below ₹1.25 lakh, the unused exemption doesn’t carry forward. It expires at the end of the year.

That’s why many investors use tax harvesting before March 31, booking gains within the exempt limit, then re-entering the position to reset the acquisition cost for future tax planning.

Grandfathering Rules & Section 112A FMV Calculations for Pre-2018 Units

Investments made before January 31, 2018, still benefit from the grandfathering provisions originally introduced in the Finance Act 2018, provisions that continue under the Income Tax Act 2025.

The intent here is simple: gains that accumulated before the reintroduction of the LTCG tax should not be taxed retroactively.

For equity shares or equity mutual fund units bought before January 31, 2018, your cost of acquisition is determined using this rule:

The cost is deemed to be the higher of:

- The actual purchase cost, or

- The lower of:

- Fair Market Value (FMV) as of January 31, 2018

- Sale price on the date of transfer

Sounds technical, but in practice, it protects older gains from being unfairly taxed.

Example:

You purchased units in 2014 at ₹50 each.

NAV on January 31, 2018 = ₹120

Sale price in December 2025 = ₹180

Calculation:

- Lower of FMV (₹120) and sale price (₹180) = ₹120

- Higher of actual cost (₹50) and ₹120 = ₹120

So your deemed acquisition cost becomes ₹120.

Taxable LTCG per unit:

₹180 – ₹120 = ₹60

To verify historical purchase data, you can download your CAS from CDSL using this guide https://www.finnovate.in/learn/blog/how-to-download-your-cdsl-cas-statement or from NSDL with the process described here.

When filing ITR-2, these gains must be disclosed under Schedule 112A, where ISIN-level reporting, acquisition details, FMV, and sale consideration are all captured.

Bonus Issues, Rights Issues, and Buyback Reporting Standards

Corporate actions often create confusion during tax filing, especially when investors assume all units are taxed the same way.

They’re not.

Bonus Shares

Under the Income Tax Act 2025, the cost of acquisition for bonus shares continues to be treated as zero.

So, if you received 100 bonus shares and later sold them at ₹200 each after the qualifying holding period, your full sale value—₹20,000—becomes your capital gain (subject, of course, to the broader ₹1.25 lakh exemption framework).

Rights Issue Shares

For rights shares, the acquisition cost is the amount actually paid during the rights issue. The holding period begins from the date of allotment and not the announcement date.

Buybacks

This is where things changed significantly.

Until recently, companies undertaking buybacks paid Buyback Distribution Tax (BDT), and shareholders typically didn’t face direct tax on proceeds.

That changed under the Finance Act 2024, effective October 1, 2024.

Now, under the revised rules incorporated into the Income Tax Act 2025:

- Buyback proceeds received by shareholders are taxed as dividend income

- The applicable tax is based on your slab rate

- The original acquisition cost may be treated as a capital loss, which can potentially be set off against other capital gains

This is a major shift in reporting and tax treatment, particularly for high-volume investors.

For fund-level corporate action references, AMFI data remains available here.

The Debt Fund Landscape: Taxation Without Indexation

Debt mutual fund taxation has changed more in the last few years than many investors realise. What used to be a fairly straightforward category, especially for long-term investors looking for tax efficiency, now operates under a split framework that depends heavily on when you made the investment.

Under the Income Tax Act 2025, the changes introduced from April 1, 2023, are now fully embedded into the law. So, if you’re filing ITR 2026, the first question isn’t just what fund do you own? It’s when did you buy it?

That single date can dramatically change your tax outcome.

Specified Mutual Funds: Why the April 1, 2023, Cutoff Matters

Debt funds that invest less than 35% in domestic equity are classified as specified mutual funds, and their taxation now follows a two-category system based entirely on the date of purchase.

Category 1 — Investments Made Before April 1, 2023

If you invested in a qualifying debt fund before April 1, 2023, those units still retain long-term capital gains treatment after a holding period of two years.

Once eligible for LTCG classification, gains are taxed at a flat 12.5%, without indexation.

This treatment has been discussed in detail in this article, which confirms that pre-April 2023 debt fund investments continue to qualify for long-term taxation after the required holding period.

For long-term investors, this older tax treatment still offers a meaningful advantage, especially in higher tax brackets.

Category 2 — Investments Made On or After April 1, 2023

This is where the landscape changed sharply.

For debt fund investments made on or after April 1, 2023, the law no longer provides LTCG treatment regardless of how long you stay invested.

You could hold the fund for three years, five years, or even 10. The gains are still treated as short-term capital gains, added to your normal income, and taxed at your applicable slab rate.

That means:

- No preferential LTCG rate

- No indexation

- No separate capital gains tax benefit

For investors in the 30% tax bracket, that’s a very different outcome compared to older holdings.

To put it simply:

A debt fund purchased in March 2023 and sold after three years may qualify for 12.5% LTCG tax.

An identical debt fund purchased in May 2023 and held for the exact same period may be taxed at 30%, depending on your slab.

Same product. Same holding period. Completely different tax result.

That’s why purchase-date tracking matters more than ever.

A Budget 2025 Twist: The Section 87A Rebate Angle

Interestingly, Budget 2025 introduced a nuance that caught many investors off guard.

As highlighted by InCred Premier, gains from debt mutual funds purchased after April 2023, because they’re treated as normal income, may potentially qualify for the Section 87A rebate, assuming your total taxable income remains within the applicable threshold under the new tax regime.

That creates an unusual scenario.

In some lower-income cases, newer debt fund investments may actually produce a lower effective tax burden than older debt fund investments taxed at the special 12.5% rate because special-rate income typically doesn’t qualify for the rebate.

A little counterintuitive, honestly. But tax law often is.

Reporting in Your ITR

For filing purposes:

- Pre-April 2023 debt fund LTCG is reported under Schedule CG in the long-term capital gains section and taxed at 12.5%.

- Post-April 2023 debt fund gains are treated as short-term gains and flow into your normal income computation, typically through Schedule CG-STCG, depending on the return form.

Getting this classification wrong can distort your tax liability and potentially trigger AIS mismatches later.

Target Maturity Funds vs. Fixed Deposits: Post-Tax Yield Comparisons

One of the more practical decisions investors face in 2026 is whether debt funds, especially target maturity funds (TMFs), still offer better after-tax outcomes compared to fixed deposits.

The answer? It depends on both your tax bracket and your purchase date.

Scenario 1 — Higher-Bracket Investor (30% Slab) with Pre-April 2023 TMF

Assume:

- TMF return = 7.2% CAGR over 3 years

- Tax = 12.5% LTCG

- Effective post-tax return ≈ 6.3%

Compare that to:

- Bank FD return = 7.0%

- Tax = 30% slab rate

- Effective post-tax return ≈ 4.9%

That’s a gap of roughly 140 basis points in favour of the TMF.

For high-bracket investors holding older debt fund units, the tax edge is still very real.

Scenario 2 — Lower-Bracket Investor (10% Slab) with Post-April 2023 TMF

Now assume:

- TMF return = 7.2%

- Tax = 10% slab rate (treated as normal income)

- Effective post-tax return ≈ 6.5%

Compared with:

- FD return = 7.0%

- Tax = 10% slab rate

- Effective post-tax return ≈ 6.3%

In this case, the difference narrows significantly.

As discussed in the Economic Times analysis, the debt fund versus FD decision now depends much more on tax profile, holding horizon, and liquidity needs than it did a few years ago.

The HDFC Life guide offers further perspective on how these rule changes have reshaped debt investing for conservative portfolios.

Bottom line? Debt funds haven’t disappeared as a tax planning tool, but the automatic tax advantage they once carried definitely has. Investors now need to be far more intentional about when they invest, how long they stay invested, and what bracket they’re likely to fall into when they eventually redeem.

Fixed Deposits (FDs) and Interest Income Strategies

From a tax perspective, fixed deposit income is often seen as straightforward. There’s no holding-period calculation, no grandfathering rules, no special exemption thresholds. Interest earned from FDs is simply taxed as normal income under Income from Other Sources, a treatment that continues under the Income Tax Act 2025.

Simple in theory.

In practice? This is still one of the most commonly misreported categories in ITR filings.

Most mistakes happen for two reasons: taxpayers either misunderstand when FD interest becomes taxable, or they assume that if the bank hasn’t deducted TDS, there’s nothing to report. Both assumptions can cause trouble later.

Accrual vs. Receipt Basis: Avoiding Double Taxation

One of the most important concepts in FD taxation is that interest is taxed on an accrual basis, not a receipt basis.

That means the tax department doesn’t care only about when you receive the money. What matters is when the income was actually earned.

Here’s what that looks like in practice:

Suppose you invest ₹5 lakh in a 3-year fixed deposit on April 1, 2023, earning 7.5% annually, compounded once a year.

Even though the FD matures in March 2026—and the total interest may only be paid then—you still need to report the accrued interest each financial year.

That would roughly look like:

- FY 2023–24 → ~₹37,500

- FY 2024–25 → ~₹40,312

- FY 2025–26 → ~₹43,336

A lot of taxpayers make the mistake of reporting the full maturity amount only in the final year. It feels logical, maybe even intuitive—but from a tax perspective, it’s incorrect.

Worse, it can lead to double taxation issues if the bank reports TDS differently across years.

The safer approach is simple:

Get the bank’s annual interest certificate, break the interest year by year, and report it accordingly.

For slab-based tax calculations, the Income Tax Department’s official calculator remains available.

The updated slab structure under the Income Tax Act 2025, as outlined here, also changes the tax outcome for many FD investors. Under the revised regime:

- Nil tax up to ₹4 lakh

- 5% between ₹4–8 lakh

- 10% between ₹8–12 lakh

- Higher slabs thereafter

- Peak rate remains 30% above ₹24 lakh

For some investors, especially retirees or conservative savers relying on interest income, these revised slabs could materially affect post-tax returns.

TDS Threshold Changes: What “No TDS” Actually Means

Another change investors need to be aware of is the revised TDS threshold on interest income.

Under the Income Tax Act 2025, the threshold for TDS deduction on bank and post office interest has reportedly increased from ₹40,000 to ₹1,00,000 per year.

That sounds like good news and operationally, it often is.

But here’s the catch:

No TDS does not mean no tax.

If your annual FD interest is below ₹1 lakh, the bank may not deduct tax at source, but you’re still legally required to declare that income and pay tax if your total income exceeds the applicable exemption limit.

This is one of those areas where taxpayers trip over a small assumption and then get a notice months later.

No TDS simply means no tax has been collected yet. It doesn’t mean the income disappears.

Resolving TDS Discrepancies: Matching Form 26AS with your AIS

Before filing ITR 2026, every FD investor should reconcile two documents:

- Form 26AS

- AIS (Annual Information Statement)

Both are available through the Income Tax Department’s e-filing portal.

Of the two, AIS is usually more comprehensive. It pulls information from banks, brokers, mutual fund registrars, and other reporting entities.

That makes it incredibly useful, but also a source of occasional mismatches.

Here are some of the most common scenarios:

Scenario 1 — TDS Deducted by the Bank but Missing in Form 26AS

If your bank deducted TDS but the credit doesn’t show up in Form 26AS, it usually means one of two things:

- The bank hasn’t deposited the TDS yet, or

- Their TDS return wasn’t filed correctly

In that case, raise the issue with the bank first.

If it isn’t resolved, you can flag the discrepancy through the AIS feedback portal.

Importantly, don’t hold back your ITR just because of this mismatch. Report the income correctly and claim the TDS based on available documentation.

Scenario 2 — Form 26AS and AIS Show Different Values

Sometimes both systems show data, but the numbers don’t line up.

This usually happens because AIS updates more frequently and pulls from multiple sources.

If the difference is small and explainable, submit feedback in AIS and move on.

If the gap is large, investigate immediately. In some cases, banks have incorrectly mapped PAN details, and fixing it early saves a lot of back-and-forth later.

Scenario 3 — Interest Shows Up in AIS, But No TDS Was Deducted

This is often completely normal, especially if annual interest remains below the ₹1 lakh threshold.

But you still need to calculate the tax liability yourself.

If the tax payable crosses the advance tax limits and isn’t paid on time, interest under Sections 234B and 234C may apply.

At a glance, fixed deposits still look like the simplest investment from a tax perspective. But once accrual rules, TDS thresholds, and AIS matching come into play, they demand a little more attention than most investors expect. Ignore the paperwork, and even the safest investment can create unnecessary compliance headaches.

Strategic Loss Set-Offs and Carry Forward Rules in 2026

Capital losses rarely feel good in the moment. Nobody enjoys looking at red numbers in a portfolio. But from a tax perspective, losses can actually become one of the most valuable planning tools available if you understand how to use them properly.

The Income Tax Act 2025 largely preserves the loss set-off framework from the old 1961 law, while making some aspects easier to interpret. For investors filing ITR 2026, understanding these rules can make a noticeable difference to your final tax outgo.

And in some cases, the tax saved from smart loss utilisation can be more meaningful than chasing an extra half-percent of portfolio return.

Cross-Asset Offsets: Can Equity Losses Offset Debt Gains?

One of the most common questions investors ask is whether losses in one asset class can be used against gains in another.

The short answer: yes, but the type of loss matters.

Under the 2025 framework, capital loss set-off follows a strict hierarchy:

Short-Term Capital Loss (STCL)

Short-term capital losses are the most flexible.

They can be adjusted against:

- Short-Term Capital Gains (STCG) from any capital asset

- Long-Term Capital Gains (LTCG) from any capital asset

That means a short-term loss from equity, debt funds, listed shares, bonds, or even certain alternative assets may potentially be used across categories.

That flexibility makes STCL one of the most useful tools in year-end tax planning.

Long-Term Capital Loss (LTCL)

Long-term losses are more restricted.

They can only be set off against:

- Long-Term Capital Gains (LTCG)

They cannot be adjusted against short-term gains.

So, if you book a long-term loss on an equity mutual fund, you can’t use it against short-term gains from swing trading or short-duration debt fund redemptions.

That distinction trips up a lot of investors.

Real-World Example: Equity Loss vs Debt Fund Gain

Suppose you’ve booked:

- ₹50,000 long-term capital loss on equity mutual funds

- ₹3.20 lakh long-term capital gain on a debt mutual fund purchased before April 1, 2023

Since both fall under LTCG treatment, the equity loss can be used to reduce the debt fund gain.

Your taxable LTCG becomes:

₹3.20 lakh – ₹50,000 = ₹2.70 lakh

That directly lowers your tax liability under the 12.5% LTCG regime.

Cross-asset adjustment is fully permitted here.

Similarly, if you had a short-term loss in equity, that could also offset short-term gains from debt funds taxed at slab rates.

As illustrated in the case study, separate gain categories still need to be computed independently before applying exemptions and offsets.

For example:

A taxpayer with:

- ₹1.20 lakh equity LTCG

- ₹30,000 equity STCG

Would see:

- LTCG fully exempt (within ₹1.25 lakh limit)

- STCG is taxed separately at 20%

Same year. Same portfolio. Different tax treatment.

That’s why classification matters almost as much as the gain itself.

Carry Forward of Unadjusted Capital Losses

Not every loss can be fully utilised in the same year.

If you don’t have enough gains to absorb your losses, the unused portion can be carried forward for up to 8 years.

Under the Income Tax Act 2025, this terminology aligns with the new “tax year” structure, but the practical rule remains unchanged.

That means:

- Losses booked in FY 2025–26 can potentially be carried forward through the next 8 tax years

- Those losses can be used whenever eligible gains arise in future years

But, and this part is critical, the benefit is available only if you file your ITR on time.

Late filing can cost you the right to carry forward capital losses entirely.

Even if you made no taxable gains during the year, even if your entire portfolio was negative, filing still matters.

This is one of those quiet rules that doesn’t get much attention until someone misses it.

Unlisted Shares and Alternative Assets Under the New Act

Not all investments follow the same holding period rules.

Under the Income Tax Act 2025:

- Listed equity → LTCG after 12 months

- Unlisted equity / private shares → LTCG after 24 months

- Certain bonds and alternative assets may also follow the 24-month threshold

For unlisted shares:

- LTCG tax rate = 12.5% (without indexation)

- STCG = Taxed at slab rates

This is particularly relevant for:

- Startup investors

- ESOP holders in private companies

- Angel investors

- Pre-IPO participants

- AIF investors

Alternative Investment Funds (AIFs), regulated by SEBI, continue to have layered tax treatment depending on fund structure.

More on AIF registration and compliance can be found in this guide.

For investors using sale proceeds to claim exemptions under Section 54 or 54F, the capital gains account scheme remains relevant. Information is available here.

ICICI Bank’s updated implementation, effective January 1, 2026, is also referenced in this article.

Bonds, NCDs, and Corporate Restructuring Cases

Debt securities such as listed bonds and NCDs follow their own holding rules:

- Listed bonds → LTCG after 12 months

- Unlisted bonds → LTCG after 24 months

Once classified as long-term, gains are taxed at 12.5% under the new regime.

Another area investors often miss? Corporate restructuring.

If you receive shares or bonds through:

- Demergers

- Mergers

- Scheme of arrangement

- Corporate spin-offs

Your original acquisition cost and holding period may carry over into the new securities.

That can significantly affect your capital gains calculation later.

Historical guidance on cost splitting after demergers is available here.

The takeaway here is simple: losses are not just damage control. Used correctly, they become a strategy. But only if records are clean, classifications are accurate, and returns are filed on time. Miss one of those pieces, and what could have been a tax advantage quietly disappears.

NRI Taxation & Global Implications for ITR 2026

For Non-Resident Indians (NRIs), filing taxes in India has always involved a few extra layers—TDS at source, foreign documentation, treaty benefits, repatriation rules, and in some cases, a fair bit of back-and-forth with banks, brokers, or tax advisors.

The Income Tax Act 2025 attempts to simplify parts of this framework, but the core compliance obligations for NRIs remain very much in place.

If you’re an NRI investing in Indian equities, mutual funds, debt instruments, real estate, or unlisted shares, ITR 2026 isn’t just about calculating gains; it’s also about ensuring taxes are deducted correctly, treaty benefits are claimed properly, and repatriation rules are followed without triggering avoidable delays.

TDS Rate Charts and Repatriation Tax Clearance Certificates

Under the Income Tax Act 2025, tax is typically deducted at source when NRIs realise capital gains on Indian investments.

Broadly, the TDS rates continue along these lines:

| Asset Class | LTCG TDS Rate | STCG TDS Rate |

| Listed equity / equity mutual funds | 12.5% | 20% |

| Debt mutual funds (pre-April 2023 investments) | 12.5% | Slab rate (often 30%) |

| Debt mutual funds (post-April 2023 investments) | Slab rate | Slab rate |

| Immovable property | 12.5% | Slab rate |

| Unlisted shares | 12.5% | 30% |

These rates may also attract:

- Surcharge (depending on income level)

- Health & Education Cess @ 4%

So while the headline LTCG rate may look like 12.5%, the effective tax incidence can move closer to 14–15% in higher-income cases.

A useful breakdown of recent cross-border tax developments is available in Deloitte’s analysis.

DTAA Benefits: Avoiding Double Taxation

One of the biggest advantages available to NRIs is access to India’s Double Taxation Avoidance Agreements (DTAAs).

India has tax treaties with multiple jurisdictions, including:

United Arab Emirates, United States, United Kingdom, Singapore, Canada, and Mauritius.

Depending on your country of residence and the nature of your investment income, treaty benefits may reduce tax on:

- Capital gains

- Dividend income

- Interest income

But treaty benefits don’t apply automatically.

To claim them, NRIs generally need:

- A Tax Residency Certificate (TRC) from their country of residence

- Form 10F

- A self-declaration confirming beneficial ownership and treaty eligibility

And yes, missing even one of these documents can delay or block treaty relief.

Also worth noting: treaty provisions can change over time. The India–Mauritius treaty, for example, saw major revisions in 2016, affecting how certain capital gains are taxed.

So historical assumptions don’t always hold.

Lower Deduction Certificate (LDC): Reducing Excess TDS

One of the biggest pain points for NRIs, especially in large transactions, is excessive tax deduction upfront.

Say you’re selling:

- A property in India

- A large block of unlisted shares

- A startup stake

- High-value inherited assets

In many cases, the buyer is legally required to deduct TDS at the full applicable rate.

That’s where the Lower Deduction Certificate (LDC) becomes useful.

If your actual tax liability is expected to be lower than the default TDS rate, you can apply to the Income Tax Department for an LDC here.

Once approved, the buyer can deduct tax at the lower certified rate instead of the standard rate.

For high-value transactions, which can make a very real difference to cash flow.

Repatriation and Tax Clearance

After selling Indian investments, many NRIs eventually want to move funds abroad.

That’s where tax compliance overlaps with FEMA rules.

Under current regulations:

Funds held in an NRO (Non-Resident Ordinary) account can generally be repatriated up to USD 1 million per financial year, subject to documentation.

That documentation usually includes:

- Form 15CA

- Form 15CB (certified by a Chartered Accountant)

Funds held in an NRE (Non-Resident External) account generally enjoy fewer restrictions when repatriated.

For capital gains reinvestment—especially where exemptions under Sections 54 or 54F are being claimed—the Capital Gains Account Scheme (CGAS) remains relevant.

Some designated banks continue to offer these accounts, including ICICI Bank, whose NRI capital gains scheme details are available here.

The Practical Reality for NRIs in ITR 2026

For resident investors, ITR filing is often about getting the numbers right.

For NRIs, it’s usually about getting both the numbers and the paperwork right.

A gain may be calculated perfectly—but if:

- Treaty documents are missing

- TDS was deducted incorrectly

- Repatriation certificates weren’t filed

- Residential status was classified incorrectly

the compliance burden can quickly snowball.

The Income Tax Act 2025 does make the language cleaner. But for cross-border investors, the system still rewards one thing above all else:

Documentation. Clean, early, and complete.

Frequently Asked Questions: ITR 2026 & Income Tax Act 2025

Yes. The 12.5% Long-Term Capital Gains (LTCG) rate on listed equity and equity-oriented mutual funds applies to gains realized in FY 2025-26. You must pay this flat rate on aggregate long-term gains exceeding the new ₹1.25 lakh annual exemption limit when filing your return by July 2026.

Taxation depends strictly on your investment date. Debt funds purchased before April 1, 2023, qualify for the 12.5% LTCG rate if held for over 24 months. However, units purchased on or after April 1, 2023, are classified as Short-Term Capital Assets and are taxed at your applicable income tax slab rate, regardless of your holding period.

To claim grandfathering benefits for equity purchased before January 31, 2018, you must use Schedule 112A in the ITR-2 form. You are required to input the specific ISIN, actual cost of acquisition, and the Fair Market Value (FMV) as of January 31, 2018. The e-filing portal automatically computes the tax-exempt portion based on these inputs.

Yes. The statutory TDS threshold for bank interest has been raised to ₹1,00,000, meaning banks will not deduct tax on amounts below this limit. However, you are still legally required to declare this interest on an accrual basis every financial year under “Income from Other Sources” and pay tax according to your specific slab rate.

Yes. Under the capital loss set-off rules, a Short-Term Capital Loss (STCL) from any asset class can be set off against both Short-Term and Long-Term Capital Gains. However, a Long-Term Capital Loss (LTCL) can only be set off against other Long-Term Capital Gains.

| Asset Class (Investment Type) | Holding Period for Long-Term Status | Long-Term Capital Gains (LTCG) Rate | Short-Term Capital Gains (STCG) Rate | Exemption Limit & Thresholds | Key Tax Treatment & Strategic Notes |

| Listed Equity & Equity Mutual Funds | More than 12 months | 12.5% | 20% | ₹1.25 lakh per financial year | Exemption raised from ₹1 lakh. Grandfathering rules apply for units bought before Jan 31, 2018. Indexation removed. |

| Debt Mutual Funds (Purchased before April 1, 2023) | More than 24 months | 12.5% | Applicable slab rate | Nil | Qualifies for special LTCG rate without indexation. Capital losses can be strategically set off against other LTCG. |

| Debt Mutual Funds (Purchased on or after April 1, 2023) | N/A (Always Short-Term) | N/A | Applicable slab rate | Section 87A rebate (if eligible) | Treated purely as STCG regardless of holding period. Added to normal income. No indexation benefits. |

| Unlisted Equity / Private Shares | More than 24 months | 12.5% | Applicable slab rate | Nil | Long-term gains taxed at 12.5% without indexation. Highly relevant for startup ESOPs and angel investors. |

| Listed Bonds and NCDs | More than 12 months | 12.5% | Applicable slab rate | Nil | Qualify for beneficial LTCG treatment much faster (12 months) under the new regulatory framework. |

| Fixed Deposits (FDs) | N/A | N/A | Applicable slab rate | ₹1,00,000 for TDS deduction | Interest is taxed annually on an accrual basis, not maturity. TDS threshold increased significantly to ₹1 lakh. |

| Corporate Buybacks | N/A | N/A | Applicable slab rate | Nil | Proceeds now taxed as dividend income at standard slab rates. Original acquisition cost is treated as a capital loss. |

Adapting Your Portfolio for the 2026 Filing Season

The Income Tax Act 2025 isn’t just a statutory rewrite. For investors, it marks a real shift in how wealth is taxed, reported, and planned for in India.

Between revised capital gains rates, changes to debt fund taxation, updated rebate mechanics, and a cleaner compliance framework, ITR 2026 will likely feel different, even for seasoned taxpayers who’ve been filing returns for years.

And maybe that’s the bigger point here.

This isn’t simply about learning a few new tax rates. It’s about adjusting your investment decisions to a framework where post-tax returns matter just as much as headline returns.

The investors who handle this transition best probably won’t be the ones reacting in July while filing their returns. More likely, it’ll be the ones who plan before March 31, 2026, while there’s still time to act.

Immediate Action Items: Tax Harvesting and Portfolio Rebalancing Before March 31

1. Equity Tax Harvesting

If your unrealised long-term capital gains in equity mutual funds or listed shares remain below the ₹1.25 lakh exemption threshold, this may be the right time to review whether tax harvesting makes sense.

By booking gains before March 31, 2026, and, where suitable, re-entering the position, you may reset your acquisition cost at a higher base, potentially reducing future LTCG exposure.

Of course, tax planning shouldn’t distort your asset allocation. That’s where working with a qualified advisor can help. A useful perspective on that is available in this guide.

2. Loss Harvesting

Not every losing investment needs to be sold, but if you’re already considering portfolio clean-up, realised losses can become valuable tax assets.

Remember:

- STCL can offset both STCG and LTCG

- LTCL can offset LTCG only

Unused losses may be carried forward for up to 8 years, provided your return is filed within the due date.

That one deadline matters more than many investors realise.

3. Debt Fund Category Review

If you hold debt mutual funds, go back and check your transaction dates.

Seriously, don’t assume you remember.

The difference between a purchase made on March 31, 2023 and one made on April 2, 2023 can completely change the tax treatment.

Pre-April 2023 units may still qualify for 12.5% LTCG treatment after the holding requirement is met.

Post-April 2023 units? Those gains generally flow into your normal income and are taxed at slab rates.

A quick review here could influence whether you stay invested, redeem, or rebalance.

4. FD Interest and Advance Tax Review

If you hold fixed deposits across multiple banks, now’s a good time to consolidate your annual accrued interest figures.

Not maturity values. Not rough estimates.

Actual accrued interest.

Make sure:

- Bank certificates match your records

- AIS entries are accurate

- Advance tax (if applicable) is paid before the March 15 deadline

Ignoring this often leads to avoidable interest under Sections 234B and 234C.

5. Review Exit Load Timelines

Before redeeming mutual funds purely for tax reasons, double-check whether an exit load still applies.

Sometimes investors save tax on paper, and quietly lose that advantage through redemption charges.

A practical overview of exit load considerations is available here.

Small details like this can quietly reshape your actual post-tax return.

Final Document Checklist: Aligning Your AIS, Form 26AS, and Capital Gain Statements

Before filing ITR 2026, gather and reconcile the following:

From Your Bank(s)

- Annual Interest Certificate for all fixed deposits

- Form 16A, where TDS was deducted

- Savings account interest statements

From Mutual Fund Registrars (CAMS / KFintech)

- Capital Gains Statement for FY 2025–26

- Consolidated Account Statement (CAS)

CAS downloads remain available through:

- https://www.finnovate.in/learn/blog/how-to-download-your-cdsl-cas-statement

- https://www.finnovate.in/learn/blog/how-to-download-nsdl-cas-statement

For SIP investors, ensure each instalment is reflected separately, because every SIP purchase carries its own holding period.

From Your Broker

If you invest in direct equity, obtain:

- Capital Gains Report

- Detailed transaction statements

- ISIN-level data for Schedule 112A

Platforms like Zerodha provide reporting facility, with tax integrations also available via https://zerodha.quicko.com/.

From the Income Tax Department

Before submitting your return, reconcile:

- AIS (Annual Information Statement)

- Form 26AS

Accessible through:

https://incometaxindiaefiling.gov.in

Cross-check:

- Every TDS entry

- Every capital gains disclosure

- Every reported interest entry

And if something looks off—submit feedback before it turns into a notice later.

For NRIs

Additional documentation may include:

- Tax Residency Certificate (TRC)

- Form 10F

- Form 15CA / 15CB for repatriation

Cross-border investing always demands one extra layer of discipline.

Final Thought

The move to the Income Tax Act 2025 is more than a compliance update—it’s a good excuse, maybe even a necessary one, to step back and look at your portfolio through a different lens.

Not just what am I earning?

But:

What am I actually keeping after tax?

That’s usually where smarter investing begins.

And in a tax regime that’s becoming cleaner—but not necessarily simpler in practice—that question may matter more than ever.

For ongoing updates, Finance Bill changes, and CBDT circulars, official communications remain available here.

Discalimer

The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of [Your Website Name]. This content is provided for general information and entertainment purposes only. While we endeavor to provide accurate and helpful insights, the information here is provided “as is” and should not be treated as professional advice. Readers are encouraged to use their own judgment and discretion before applying any tips, strategies, or recommendations found in this post to their personal or professional lives.

Discussion (1)

Leave a Reply