The ₹10 Lakh Mistake: Complete Guide to Declaring Foreign Assets (Schedule FA) in ITR 2026

The New Era of Global Tax Transparency

India’s middle class didn’t just “go global” overnight, but it sort of drifted there, quietly at first. One person starts buying US stocks through Vested or Stockal. Someone else gets RSUs from a parent company listed on Nasdaq. Freelancers begin accepting USD through Payoneer, maybe without thinking twice about where that money technically “lives.” And then crypto happened, sitting on foreign exchanges, slightly out of sight, slightly out of mind. Put all of that together, and suddenly, a very large number of Indians have financial footprints that stretch well beyond India. Not dramatically. Just enough to matter. Herein, the Schedule FA becomes crucial.

Policymakers noticed. They usually do, eventually.

That’s where the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, or just the Black Money Act, comes in. It wasn’t designed only for the obvious cases of hidden offshore wealth. It also catches the far more common situation: regular taxpayers who simply didn’t realise they were supposed to report something. The law kicked in from 1 July 2015 (Assessment Year 2016–17), and its scope is wider than most people assume at first glance.

And then there’s the part that makes people slightly uneasy when they first hear it—the data sharing.

Under FATCA (Foreign Account Tax Compliance Act), US financial institutions report accounts held by Indian residents. Under the Common Reporting Standard (CRS), more than 100 countries, UK, Singapore, UAE, Canada, Australia, and so on, do the same. Information flows in automatically and quietly, every year.

So, by the time you sit down to file your ITR, there’s a decent chance the Income Tax Department already has a version of your foreign financial life sitting in its system.

This changes the tone of the whole exercise.

This isn’t really about “whether to disclose” anymore. That choice, if it ever existed is mostly gone. What remains is making sure you do it correctly, because the penalties for getting it wrong aren’t mild, and “I didn’t know” doesn’t travel very far as an argument.

At a Glance: Foreign Asset Disclosure in India

Short on time? Here is a quick summary of the core rules for reporting foreign assets and income in your 2026 ITR:

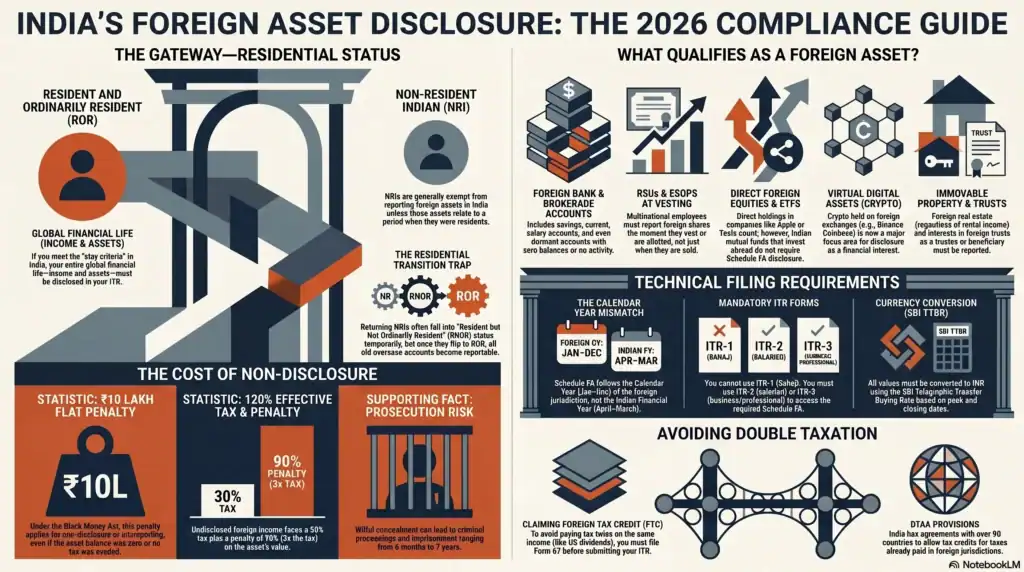

- Who Must File: Mandatory for all Resident and Ordinarily Resident (ROR) taxpayers. NRIs are generally exempt from foreign asset reporting.

- What Counts as a Foreign Asset: Overseas bank accounts, vested RSUs/ESOPs, US stocks/ETFs, foreign real estate, and crypto held on foreign exchanges.

- The Penalty Risk: Failing to report an asset in Schedule FA can trigger a flat ₹10 Lakh penalty under the Black Money Act—even if no tax was evaded or the account balance was zero.

- The Right Form: You must use ITR-2 or ITR-3. Filing ITR-1 means you are completely skipping your Schedule FA obligations.

- The Timeline Trap: Unlike standard Indian taxes (April–March), foreign assets in Schedule FA must be reported based on the foreign jurisdiction’s Calendar Year (Jan–Dec).

- Avoiding Double Tax: If foreign taxes were already deducted (e.g., on US dividends), you must file Form 67 before submitting your ITR to claim Foreign Tax Credit (FTC) under the DTAA.

Who Is Required to File Schedule FA in ITR?

Understanding Residential Status (The Deciding Factor)

If there’s one thing that quietly determines almost everything in this space, it’s your residential status under the Income Tax Act, 1961. Not your passport, not where your salary comes from, but how many days you’ve physically spent in India, and a bit of your recent history.

India splits taxpayers into three buckets. Sounds simple. In practice, people get this wrong more often than you’d expect.

Resident and Ordinarily Resident (ROR)

This is the category where the rules really tighten. If you’ve spent enough days in India (182 days in a year, or the slightly trickier 365+60-day combination), and you’ve been around long enough in previous years, you fall into ROR. And once you’re here, your entire global financial life comes into view, at least from a tax perspective. Income from anywhere in the world is taxable, and all foreign assets must be disclosed in Schedule FA. There is no real wiggle room.

Resident but Not Ordinarily Resident (RNOR)

This one usually catches returning NRIs. You’re technically a resident again, but the law gives you a kind of soft landing. Foreign income isn’t taxed (in most cases), and disclosure requirements are lighter. It’s a temporary phase, though. You don’t stay RNOR forever, and when it flips to ROR, things change quickly.

Non-Resident Indian (NRI)

If you don’t meet the stay criteria, you’re an NRI. In that case, India is only interested in income that arises within its borders. Your overseas assets? Generally, outside the reporting net. At least while you remain non-resident.

There’s a line from this guide that puts it plainly, almost bluntly: “Understanding residency status is critical. It determines your disclosure obligations.”

It’s one of those statements that sounds obvious, until you realise how many filings go wrong right here.

Is It Mandatory for NRIs to Declare Foreign Assets in India?

Short answer: No.

Longer answer—still no, but with a few traps around the edges.

NRIs are not required to disclose foreign bank accounts, overseas investments, or foreign income in Indian tax returns just because those assets exist. That part is actually straightforward.

Where things get messy is in practice. A surprising number of NRIs end up filing returns as residents—sometimes due to bad advice, sometimes because the ITR portal nudges them that way, sometimes just habit. And once you file as a resident, the system assumes you should have disclosed foreign assets. That’s where unintended exposure begins.

There is one important caveat: if you earn income in India, say, rent from a property, you still need to file an ITR. But even then, your foreign assets remain outside Schedule FA requirements.

Also worth noting (and this is relatively new territory): the Foreign Assets of Small Taxpayers Disclosure Scheme, 2026. As outlined here, it can apply even to people who are now NRIs if the assets or income relate to a time when they were residents. So, the timeline matters, not just your current status.

Legal Owner vs. Beneficial Owner vs. Beneficiary

This is where the law gets a bit philosophical.

It’s not enough to ask, “Is this asset in my name?” The tax rules go further.

- Legal owner: The name on the paperwork. Straightforward.

- Beneficial owner: The person who actually funded the asset, even if it’s held in someone else’s name.

- Beneficiary: Someone who benefits economically, even if they didn’t fund it and don’t legally own it.

And yes, all three categories can trigger disclosure requirements.

Even beneficiaries may need to report, unless a specific exemption applies (for example, if the income is already taxed in the hands of the legal or beneficial owner under the Fifth Proviso to Section 139(1)).

There’s another wrinkle people often miss: signing authority.

Even if the money isn’t yours, say, you’re authorised to operate a company’s foreign account, you may still need to disclose that authority in Schedule FA.

It’s one of those areas where the instinct is to think, “This doesn’t really count as mine.”

But the law isn’t asking about instinct. It’s asking about the connection.

What Qualifies as a Foreign Asset? The Complete List

Do I Need to Declare Foreign Bank Accounts to Indian Tax Authorities?

Yes—no ambiguity here.

If you’re an ROR, pretty much any foreign bank account you’ve touched counts. Savings, current, salary accounts, even fixed deposits. That old student account you opened in the UK and forgot about? Still counts. The USD balance sitting idle in a brokerage account? That too.

We’re talking about:

- A savings account with something like Barclays from your time abroad

- A brokerage-linked cash account (say, Charles Schwab)

- Custodian accounts holding your US stocks or ETFs

The rule is simple, even if it feels excessive: disclose it regardless of balance, activity, or income.

There is one detail people latch onto: the ₹5 lakh threshold under the Black Money Act. If your aggregate foreign account balances never exceeded that during the year, the ₹10 lakh penalty may not apply.

But, and this is where people slip, that’s a penalty relief, not a reporting exemption. You still have to disclose. Skipping it because “the amount is small” is not a safe interpretation.

Are Foreign RSUs and ESOPs Considered Foreign Assets?

Yes, and this is where a lot of salaried professionals get caught off guard.

If you work for a multinational and receive RSUs or ESOPs from a foreign parent entity, those shares become reportable the moment they vest or are allotted. Not when you sell them and not when you transfer the money. At vesting.

What usually happens is this:

- The employer does everything right—taxes the perquisite, deducts TDS, and shows it in your Form 16

- You report the salary income correctly

And then you forget to disclose the actual shares in Schedule FA.

That mismatch? It’s one of the more common triggers for automated notices.

The tax treatment itself has two stages:

- At vesting/exercise:

The fair market value becomes salary income. Already taxed. - At sale:

Any gain beyond that FMV is taxed as capital gains.

And yes, even ESPPs fall into this. If you’re getting discounted shares from a foreign entity, they belong in Schedule FA.

Foreign Equity, Mutual Funds, and ETFs

If you’re directly investing in foreign markets, buying Apple, Tesla, or ETFs through an overseas broker, those holdings need to be disclosed.

This includes:

- Direct stock investments

- Foreign mutual funds

- Foreign-listed ETFs

But here’s a small distinction that trips people up:

If you’re investing in an Indian mutual fund that itself invests abroad, that does not count as a foreign asset for Schedule FA.

So, the question to ask is: Do I directly hold the foreign asset?

If yes → disclose.

If it’s wrapped inside an Indian fund → you’re fine.

Immovable Property and Real Estate Abroad

This one’s more obvious, but still worth stating plainly.

Own property outside India? It goes into Schedule FA.

Doesn’t matter if it’s:

- A holiday home in Portugal

- A rental apartment in Dubai

- Land in the US that’s just sitting there

Even if it generates zero income. Even if it’s locked and unused. The disclosure requirement doesn’t depend on activity, but it depends on ownership.

Do I Need to Declare Foreign Crypto Accounts to Indian Tax Authorities?

Yes, and this has become a major focus area recently.

If your crypto sits on foreign exchanges like Binance, Coinbase, or Kraken, it’s treated as a foreign asset.

Since the Finance Act 2022 formalised taxation for Virtual Digital Assets (VDAs), the expectation is clear:

- 30% tax on gains

- 1% TDS

- And yes, Schedule FA disclosure if held abroad

Typically, these are reported under “financial interest” or the catch-all “other capital asset” category.

The compliance push here isn’t theoretical either. The department has been actively flagging such cases .

Crypto used to feel a bit outside the system. It doesn’t anymore.

Cash Value Insurance, Trusts, and Endowments

This is the quiet corner where people genuinely don’t realise they have a reporting obligation.

We’re talking about:

- Foreign life insurance policies with a surrender value

- Annuity contracts

- Interests in foreign trusts (as trustee, settlor, or beneficiary)

- Stakes in foreign companies or foundations

These don’t show up in obvious ways—no trading apps, no monthly statements you casually check. Which is exactly why they’re often missed.

And yet, these are the cases that tend to trigger notices later, especially for people who’ve lived abroad and returned, or inherited assets without fully understanding what came with them.

How Are Foreign Assets Taxed in India?

Taxation on Foreign Dividend Income

If you’re earning dividends from foreign companies, say, US stocks quietly paying you every quarter that income doesn’t get any special treatment in India.

It’s taxed as “income from other sources.” Which sounds harmless, but really just means: it’s added to your total income and taxed at your slab rate.

So, if you’re already in a higher bracket, those dividends are taxed right up there with your salary. There are no concessional rates and no soft landing.

There is a small saving grace, though. Many countries (like the US) withhold tax at source before the money even reaches you. Under DTAA, you can usually claim credit for that, but we’ll get to that in the next section.

Still, the first time someone realises their “passive” dividend income is taxed like regular income, it’s not always a pleasant moment.

Capital Gains Tax on Sale of Foreign Assets

This part tends to surprise people, even those who’ve been investing for a while.

Foreign stocks are treated as unlisted assets in India. Not because they’re obscure, but because they’re not listed on an Indian exchange.

That classification changes everything:

- Long-Term Capital Gains (LTCG):

You only get long-term status after 24 months (not 12 like Indian equities) - Tax rate for LTCG:

20% with indexation - Short-Term Capital Gains (STCG):

Taxed at your slab rate

So yes, holding a US stock for, say, 14 months doesn’t get you any preferential treatment. It’s still short-term in India’s eyes.

For RSUs and ESOPs, there’s an extra layer:

- Your cost of acquisition isn’t zero

- It’s the fair market value at vesting, which was already taxed as salary

This detail matters. Miss it, and you might end up overpaying tax or worse, reporting it incorrectly.

Tax Treatment of Rent from Foreign Property

Owning property abroad sounds glamorous until tax season rolls around.

Rental income from a foreign property is taxed in India under “Income from House Property.” Same category as Indian real estate and the same general structure.

That means:

- You can claim the standard 30% deduction on the net annual value

- The remaining income is taxed at your slab rate

But there’s a bit of friction when it comes to taxes paid abroad. Not everything translates neatly. Municipal taxes, local deductions, they don’t always map cleanly into Indian rules.

So, in practice, you often end up relying on DTAA provisions to avoid being taxed twice on the same rental income.

And this is usually where people realise: owning property in another country isn’t just about exchange rates and rental yield. It’s also about navigating two tax systems that don’t always speak the same language.

Avoiding Double Taxation: DTAA and FTC

How Does the Double Taxation Avoidance Agreement (DTAA) Work?

At its core, DTAA is trying to solve a very human frustration: “Why am I paying tax twice on the same income?”

Because without it, that’s exactly what would happen.

Say you earn dividend income from the US. The US taxes it first (since the company is based there). Then India steps in (since you’re a resident here) and says, “We tax your global income.” Suddenly, the same money is taxed in two places.

DTAA steps in as a kind of referee.

India has signed these agreements with over 90 countries, and they basically decide who gets to tax what and how much.

Take the India–US example:

- The US taxes dividends, but usually at a reduced treaty rate (often 15% for individuals)

- India still taxes the income, but allows you to adjust for what you’ve already paid

So, you don’t escape tax, but you avoid paying it twice in full.

There are two ways DTAAs handle this:

- Exemption method – India simply doesn’t tax certain foreign income (rare in practice)

- Credit method – You pay tax in both places, but get a credit in India for the tax already paid abroad

Most of the time, you’re dealing with the credit method.

Claiming Foreign Tax Credit (FTC) via Form 67

This is where things stop being conceptual and become procedural.

You don’t automatically get DTAA relief. You have to claim it properly, and that hinges on one form: Form 67.

Miss this, and the system basically ignores your foreign tax payment. There will be no credit, and you have to pay full tax in India.

The process itself isn’t complicated, but the timing matters more than people expect:

- Go to the Income Tax portal: https://www.incometax.gov.in

- Find and open Form 67

- Enter details:

- Country where income was earned

- Type of income

- Tax paid abroad (converted to INR)

- Relevant DTAA article

- Submit Form 67

- Only then file your ITR

That ordering is not optional. If you file your ITR first and remember Form 67 later, things get messy.

Also, and this is easy to overlook, you need to reflect the credit again in your ITR under Schedule TR. Think of it as the summary layer, while Form 67 is the detailed backup.

There’s a slightly annoying truth about all this:

Even when you’ve already paid tax abroad, you still have to prove it properly to get relief in India. The system doesn’t assume fairness, but you have to document it.

Step-by-Step Guide to Filling Schedule FA in Your ITR

Which ITR Form Should You Choose for Foreign Assets?

This is one of those mistakes that feels small but isn’t.

If you have foreign assets and you’re filing ITR-1 (Sahaj) or ITR-4 (Sugam), you’re already off track. Those forms simply don’t have Schedule FA, Schedule FSI, or Schedule TR. So even if everything else is correct, the filing is technically incomplete.

The correct forms are:

- ITR-2 → Most salaried individuals with foreign assets (RSUs, stocks, etc.)

- ITR-3 → If you have business or professional income (freelancers, consultants, etc.)

It sounds obvious when written out. But in practice, people pick ITR-1 because it’s quicker, cleaner, and then unknowingly skip disclosure altogether.

The Calendar Year vs. Financial Year Mismatch

This part trips up even careful filers.

India runs on a financial year (April–March). But Schedule FA? It doesn’t care. It follows a calendar year (January–December), at least for most countries like the US.

So, when you’re filing for FY 2025–26 (AY 2026–27), your US assets need to be reported for:

January 1, 2025 → December 31, 2025

Not April to March. Not “whatever matches your ITR.”

And honestly, this is where small inconsistencies creep in. This includes numbers not aligning across schedules and income not matching asset balances. Nothing dramatic, just enough to trigger a system flag.

How to Convert Foreign Currency to INR for ITR?

Currency conversion sounds straightforward until you realise there isn’t just one rate you can use everywhere.

The rules require using SBI Telegraphic Transfer Buying Rates (TTBR), and the rate depends on what exactly you’re reporting:

- Peak balance: Rate on the date the peak occurred

- Investment cost: Rate on the date you bought the asset

- Closing balance: Rate as of December 31

- Income (dividends, interest): Typically, the closing rate of the year

So yes, you might end up using multiple exchange rates within the same asset entry.

And all values need to be shown in:

- Original foreign currency

- INR equivalent

You can pull these rates from SBI or RBI’s FLAIR portal. It’s a bit tedious. No real shortcut here.

Completing the Schedule FA Entries

Once you actually start filling Schedule FA, it becomes more structured, almost mechanical.

For each asset, you’ll need to provide:

- Type of asset

(bank account, custodian account, equity interest, immovable property, etc.) - Country + country code

- Address of the asset/account

- Account number or identifier

- Peak value during the year

(in foreign currency + INR) - Closing balance as of December 31

(again, both currencies) - Income generated

(interest, dividends, etc.) - Whether that income has been taxed in your ITR

(and under which head)

What Is the Penalty for Not Declaring Foreign Assets in India?

The Flat Rs. 10 Lakh Penalty under the Black Money Act

There’s a number that shows up again and again in this space: ₹10 lakh.

And it’s not a sliding scale. Not “up to.” Just flat.

Under Section 42 of the Black Money Act, this penalty kicks in in two very specific situations:

- You don’t file an ITR at all, despite having foreign assets or income

- You file an ITR but leave out (or misreport) foreign assets

That second one is what catches most people. Not intentional concealment, but just incomplete disclosure.

What tends to surprise people is this: the penalty applies even if there’s no additional tax due.

So even if your foreign account earned zero income, or your stock just sat there, the act of not reporting it can still trigger the penalty.

It’s less about tax evasion, more about non-disclosure.

Tax and Penalty on Undisclosed Foreign Income

If things move beyond simple non-reporting, say, the department actually identifies undisclosed income or assets during assessment, the situation escalates quickly.

- Tax: 30% on the value of the undisclosed asset/income

- Penalty: Up to 90% of that tax

Put together, you’re looking at a potential 120% effective hit on the asset’s value in extreme cases.

That’s not a rounding error, that’s painful.

There’s a reason schemes like the 2026 disclosure scheme exist . They’re essentially an acknowledgment that the standard route under the Act is harsh enough that people need an off-ramp.

Prosecution and Imprisonment Risks

And then there’s the part most people prefer not to think about.

The Black Money Act isn’t just financial; it has criminal provisions.

- Imprisonment can range from 6 months to 7 years

- Applicable in cases of wilful concealment or failure to disclose

What makes it more uncomfortable is how the law is structured. In certain proceedings, there’s a presumption that undisclosed foreign assets represent untaxed income, meaning the burden shifts to you to prove otherwise.

It’s not something that comes up for routine errors. But it exists, and that alone changes how seriously people tend to take compliance once they’re aware of it.

Is There a Minimum Threshold to Escape the Penalty?

This is where a lot of half-information floats around.

Yes, there is a ₹5 lakh threshold, but it’s narrower than people think.

- It applies only to foreign bank/depository/custodian accounts

- If the aggregate peak balance stays below ₹5 lakhs, the ₹10 lakh penalty may not apply

But two important caveats:

- It does not apply to other assets

(stocks, ESOPs, property, crypto, trusts—none of these get this relief) - It does not remove the disclosure requirement

So even if your account had, say, ₹2 lakhs sitting in it, you still need to report it. The threshold only protects you from the penalty, not from the obligation.

This is one of those areas where people hear the first half (“₹5 lakh threshold”) and miss the second half entirely.

There’s a pattern across all of this, if you zoom out a bit:

The law isn’t just trying to tax foreign assets, it’s trying to make sure they’re visible.

And once you look at it that way, the severity of the penalties starts to make more sense. Thery are not pleasant, but consistent.

Special Case Studies for High-Risk Taxpayers

The Returning NRI Scenario

This one comes up more often than you’d think.

Someone spends years abroad, US, UK, maybe the Middle East, builds up a perfectly normal financial life there. Bank accounts, retirement funds, maybe a rental property, a few investments. Nothing unusual.

Then they move back to India.

For the first couple of years, they might fall under RNOR status, which softens the tax impact. But eventually, almost quietly, they transition into ROR status.

And that’s the moment everything changes.

Suddenly, all those foreign assets that never needed to be reported in India , now do.

- A US 401(k) account

- A UK ISA

- Brokerage accounts holding stocks

- Maybe even a dormant bank account from years ago

All of it now belongs in Schedule FA.

The tricky part is psychological, not technical. People think: “I’ve had these for years. Nothing new happened this year.”

But from a tax perspective, something did happen—their residential status changed.

And for those who realise a bit late (which happens), the Foreign Assets of Small Taxpayers Disclosure Scheme 2026 offers a structured way to clean things up.

It’s not uncommon for people to only fully understand their exposure a year or two after returning. By then, it’s less about perfect compliance and more about fixing the gap carefully.

The Start-Up Employee with Foreign ESOPs

If you’ve worked at an Indian startup with a foreign parent company, this scenario probably feels familiar.

At first, ESOPs or RSUs feel like a future problem and something abstract. You get the grant letter, maybe glance at it, and move on.

Then vesting starts.

And suddenly, there are multiple layers:

- Grant: Nothing to report. No tax. Easy.

- Vesting: Tax hits as salary. TDS deducted. Everything looks handled.

- Holding the shares: This is where Schedule FA quietly enters the picture

- Sale: Capital gains come into play

The common mistake? Stopping at step 2.

People assume: “Tax has already been deducted, so I’m covered.”

But the asset itself, the shares, still need to be disclosed separately.

That gap between income reporting and asset disclosure is exactly what triggers notices.

There’s also a timing nuance:

The shares don’t just disappear from Schedule FA the moment you sell them. Depending on the reporting cycle, they may still need to show up for that year.

It’s one of those areas where everything is technically documented, you just have to connect the dots across forms.

The Freelancer Receiving Payments via PayPal/Payoneer

This one’s a bit more subtle.

Freelancers-developers, writers, designers-working with international clients often receive payments through platforms like PayPal, Payoneer, Wise, or direct foreign bank transfers.

From a work perspective, it feels simple: you do the job, you get paid.

From a tax perspective it depends on how the money flows.

If the platform maintains a foreign currency balance in your name (which PayPal/Payoneer often do), that can qualify as a foreign account, meaning Schedule FA disclosure applies.

If the money is immediately swept into your Indian account, the balance abroad may be minimal, but the account itself still exists, and that’s enough to trigger reporting.

Meanwhile, the income itself needs to be reported as business or professional income, converted to INR properly.

This category has been getting more attention from the tax department, especially where:

- Foreign remittances (via Form 15CA/CB)

- Don’t line up cleanly with reported income in the ITR

It’s not always intentional. Sometimes it’s just fragmented understanding, income reported, but the underlying account forgotten.

If there’s a thread connecting all these cases, it’s this: People don’t usually get into trouble because they’re hiding something. It’s more often because they didn’t realise how many separate obligations sit around the same asset or income.

Frequently Asked Questions (FAQs) About Foreign Asset Disclosures in India

If you omit a foreign asset in Schedule FA, you could face a flat ₹10 lakh penalty under the Black Money Act. However, if you realize the mistake before the revised return deadline (December 31 of the assessment year), you can file a revised ITR to include the missing disclosure and generally avoid the penalty.

Yes. Schedule FA disclosure is mandatory for all Resident and Ordinarily Resident (ROR) taxpayers, regardless of the account’s balance or activity. Even if your overseas student account is dormant, or your foreign brokerage account holds zero cash, it must still be reported to the Income Tax Department.

No. ITR-1 does not contain Schedule FA. If you hold any foreign assets—including vested RSUs, ESPPs, direct US stocks, or crypto on a foreign exchange—you are legally required to file either ITR-2 or ITR-3. Filing ITR-1 when you have foreign assets means your tax return is technically incomplete.

This is a very common misconception. The ₹5 lakh threshold only provides relief from the ₹10 lakh penalty under the Black Money Act, and it strictly applies only to foreign bank accounts. It does not exempt you from the requirement to report the asset, nor does it apply to stocks, ESOPs, mutual funds, or real estate.

Yes. Through the Foreign Account Tax Compliance Act (FATCA) with the US and the Common Reporting Standard (CRS) globally, India receives automated financial data from over 100 countries. If your overseas account is linked to your Indian KYC, PAN, or passport, the tax department likely already has the data matching your profile.

Quick Reference: Foreign Asset Disclosure & Taxation Rules in India (2026)

| Foreign Asset Category | ITR Disclosure (Schedule FA) | Indian Tax Treatment & Rates | ITR Reporting Period | Penalties & Thresholds (Black Money Act) |

| Overseas Bank Accounts (Savings, Depository, Checking) | Mandatory for all ROR taxpayers, even if dormant or holding a zero balance. | Interest taxed as ‘Income from Other Sources’ at your applicable slab rate. | Calendar Year (Jan–Dec) | ₹10 Lakh flat penalty. Exemption: No penalty if aggregate peak balance is under ₹5 Lakhs (but reporting remains mandatory). |

| Foreign RSUs & ESOPs (MNC Employees) | Mandatory the moment they are vested or allotted to you. | 1. At Vesting: Taxed as Salary (Fair Market Value). 2. At Sale: Taxed as Capital Gains. | Calendar Year (Jan–Dec) | ₹10 Lakh penalty. No minimum threshold relief. Risk of prosecution for concealment. |

| US Stocks, Foreign Equity & ETFs | Mandatory for direct holdings. (Excludes Indian Mutual Funds that invest abroad). | Treated as unlisted assets. LTCG: 20% with indexation (after 24 months). STCG: Slab rate. Dividends taxed at slab rate. | Calendar Year (Jan–Dec) | ₹10 Lakh penalty. No minimum threshold relief. |

| Foreign Real Estate / Immovable Property | Mandatory regardless of personal usage or if it generates zero income. | Rental income taxed under ‘House Property’ (allows standard 30% deduction). | Calendar Year (Jan–Dec) | ₹10 Lakh penalty. Imprisonment risks (6 months to 7 years) for wilful concealment. |

| Crypto on Foreign Exchanges (Binance, Coinbase, etc.) | Mandatory under ‘Financial Interest’ or ‘Other Capital Asset’ in Schedule FA. | 30% flat tax on gains + 1% TDS. | Calendar Year (Jan–Dec) | ₹10 Lakh penalty. No minimum threshold relief. |

| Foreign Life Insurance & Trusts | Mandatory if the policy has a surrender value, or if you are a trustee/beneficiary. | Treated as global income and taxed at applicable slab rates. | Calendar Year (Jan–Dec) | ₹10 Lakh penalty. No minimum threshold relief. Highly scrutinized category. |

Conclusion and Compliance Checklist

If there’s one idea that quietly runs through everything we’ve covered, it’s this:

when it comes to foreign assets, over-disclosure is almost always safer than under-disclosure.

There’s no real downside to being thorough. The system doesn’t penalise you for saying too much. But saying too little, or saying it incorrectly, can get expensive very quickly.

Over the past decade, India’s approach to foreign asset reporting has shifted from reactive to almost anticipatory. Between FATCA, CRS, and increasingly sharp data matching, the odds of something slipping through unnoticed are lower than they used to be. Not zero, but low enough that it’s not a bet worth making.

At the same time, the introduction of the Foreign Assets of Small Taxpayers Disclosure Scheme (Finance Bill 2026) signals something else: the government knows that many people didn’t deliberately hide anything, they just didn’t fully understand the rules. There’s now a path to correct that. But ideally, you don’t need that path at all.

5-Point Final Compliance Checklist Before Submitting Your ITR

1. Confirm your residential status.

This is where everything begins. Don’t rely on assumptions like “I live here now” or “I was abroad last year.” Actually, calculate your days. The difference between ROR, RNOR, and NRI isn’t cosmetic, but it completely changes your obligations.

2. Select the right ITR form.

If you’re an ROR with foreign assets or income, it has to be ITR-2 or ITR-3. Filing ITR-1 might feel simpler, but it quietly skips the very schedules you’re required to fill.

3. Complete Schedule FA for all foreign assets.

Use the calendar year (Jan–Dec) where applicable, not the financial year. Convert values using SBI TTBR rates at the correct dates. And include everything—not just what feels “significant.” Small accounts, dormant holdings, ESOPs, crypto on foreign exchanges, it all counts.

4. Report foreign income in Schedule FSI.

Interest, dividends, capital gains, rental income—each needs to be disclosed properly, country-wise, and under the correct income head.

5. File Form 67 before submitting the ITR (if claiming FTC).

This step is easy to miss and surprisingly unforgiving. If you’ve paid tax abroad and want credit for it in India, Form 67 must come before your ITR. Not after, not “later.”

A Note on Professional Guidance

This entire area sits at a slightly uncomfortable intersection—income tax law, the Black Money Act, FEMA rules, RBI reporting, and DTAAs. Each one has its own logic, and they don’t always align neatly.

So, while it’s absolutely possible to handle this yourself, there’s a strong case for involving a Chartered Accountant with international tax experience, especially if:

- You’ve recently returned to India

- You hold multiple foreign assets

- You’re dealing with RSUs, ESOPs, or foreign income streams

Sometimes it’s less about complexity and more about avoiding that one small oversight that turns into a notice later.

In the end, this isn’t really about perfection. It’s about visibility and consistency.

Because once something is properly disclosed, it stops being a risk.

Disclaimer

This article is for general informational purposes only and should not be construed as legal or tax advice. Tax laws are subject to change; consult a qualified Chartered Accountant for advice specific to your situation

Discussion (1)

Leave a Reply