How the New Income Tax Law Impacts Salaried Employees in 2026

Why the New Income Tax Rules 2026 Matter for Your Paycheck

April 1, 2026, isn’t just another neat line on the calendar where one financial year quietly hands over to the next. It’s a bit more structural than that. This is the day the Income Tax Act, 2025, actually kicks in, replacing a law that’s been around long enough to feel almost permanent, 65 years, give or take. Alongside it, the Income Tax Rules, 2026, step in for the 1962 rulebook, wrapping up what the government is calling a once-in-a-generation clean-up of how direct taxes work in India.

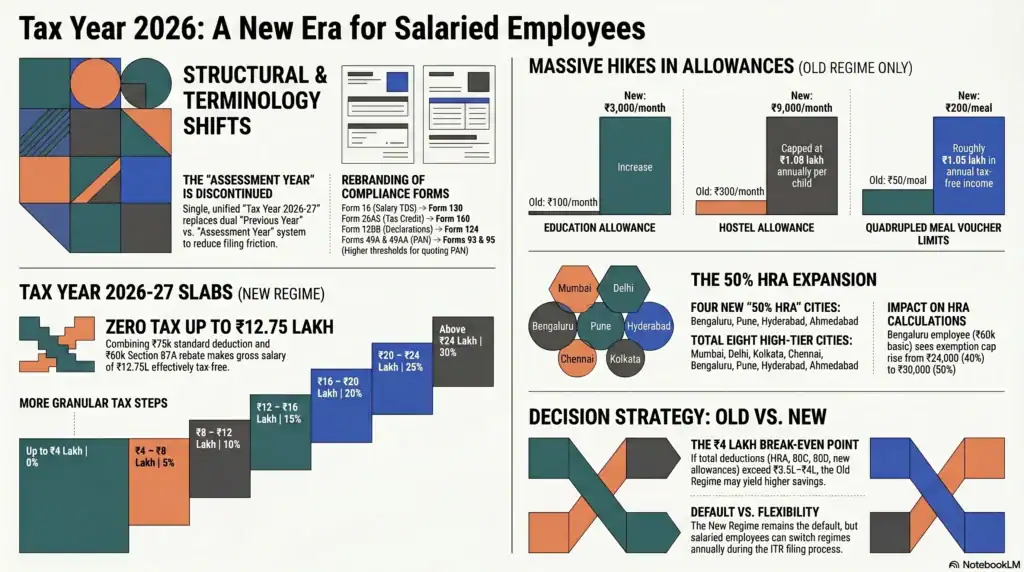

If you’re salaried, this isn’t one of those changes you can ignore and hope payroll “just handles it.” It touches everything—your payslip structure, the forms you’re used to, even the way your final tax number gets calculated. Form 16? Gone. Now it’s Form 130. The whole “assessment year vs previous year” confusion? Scrapped in favour of a single “tax year.” And then there are the more tangible bits, cities like Bengaluru, Pune, and Hyderabad suddenly getting a 50% HRA benefit, education allowance limits shooting up dramatically, and meal vouchers actually becoming meaningful again.

On balance, most of this leans positive for salaried taxpayers. A lot of allowances that had basically turned into token numbers, stuck somewhere in the early 2000s while costs kept rising, have been reset to something closer to reality. The effective zero-tax threshold still sits around ₹12.75 lakh under the new regime, which is not insignificant. And even though the form names and structure might feel unfamiliar at first glance, the compliance side is actually cleaner than what we’ve been dealing with. Less clutter, fewer oddly worded provisions.

What this guide tries to do, without overcomplicating things, is walk you through the parts that actually matter. Slabs, allowances, what you need to tell HR (and when), and where you might be leaving money on the table if you don’t adjust early. Think of it less as a technical manual and more as a practical map for Tax Year 2026–27.

At a Glance: The 2026 Income Tax Overhaul for Salaried Employees

If you only have two minutes, here are the critical changes coming into effect on April 1, 2026 under the new Income Tax Act 2025:

- The “Assessment Year” is Dead: Say goodbye to confusing timelines. Everything now falls under a single, unified Tax Year 2026-27.

- Zero Tax up to ₹12.75 Lakh (New Regime): Under the default new tax regime, a gross salary of up to ₹12.75 lakh is effectively tax-free when combining the ₹75,000 standard deduction and the Section 87A rebate.

- Form 16 is Officially Replaced: Your employer will no longer issue Form 16. It has been replaced by Form 130. Additionally, Form 26AS is now Form 168, and investment declarations shift to Form 124.

- Massive Hikes to Old Regime Allowances: Deductions have been aggressively updated for inflation. The children’s education allowance jumps from ₹100 to ₹3,000 per month, hostel allowance rises to ₹9,000 per month, and tax-free meal vouchers increase to ₹200 per meal.

- New 50% HRA Cities Added: Rents have changed, and the rules finally caught up. Bengaluru, Pune, Hyderabad, and Ahmedabad are now eligible for the higher 50% HRA exemption limit.

- The Old Regime is Making a Comeback: Because the new massive allowance hikes are only available under the old regime, employees claiming HRA and education limits may find the old tax regime gives them a lower tax bill in 2026.

Key Changes in the Income Tax Act 2025 (Effective April 2026)

How The New Income Tax Act 2025 Impacts Salary

At first glance, you might expect a brand-new tax law to flip everything upside down. It doesn’t, at least not in the way people fear. Your salary isn’t suddenly being taxed under some alien logic. The broad structure stays put. But under the surface, quite a few knobs have been adjusted.

What’s changed, really, is how things are calculated and presented. Perquisites are being valued differently, allowance limits have been nudged, some quite dramatically, and the forms that decide your final taxable income look unfamiliar now. The law itself reads cleaner too. Less of that dense, layered legal language. More tables and more formulas. It feels intentional, almost like someone finally tried to make it readable.

For most salaried folks, the impact shows up in three very specific, very practical places.

First, there are allowances. A lot of them were stuck in time, numbers that might have made sense in the 90s but felt almost symbolic today. Those have now been reset to levels that actually reflect current costs. You’ll notice the difference, especially if your salary structure leans on these components.

Second, compliance. The familiar paperwork-Form 16, Form 12BB-has been replaced. Not radically different in purpose, but different enough to throw you off the first time you see them.

And third, HRA. This one’s subtle but important. The system now acknowledges that cities like Bengaluru or Hyderabad aren’t exactly “cheap rent” zones anymore. The classification has finally caught up with how people actually live and pay rent.

What hasn’t changed is just as important. Salary income is still taxed the way you’d expect. The old vs new regime choice is still there. Core deductions, think Section 80C, haven’t disappeared or been reinvented.

So no, you’re not dealing with a completely new philosophy of taxation. It’s more like someone took the old rulebook, rewrote it in clearer language, updated the numbers, and trimmed the excess. Same game, cleaner rules.

When Does The New Income Tax Act 2025 Apply?

This part is refreshingly straightforward with no hidden twists.

The Income Tax Act, 2025, applies to income earned from April 1, 2026, onward, which lines up with Tax Year 2026–27. Even though the law was technically approved back in 2025, there was a deliberate pause before switching it on. That gap wasn’t accidental. It gave everyone-companies, payroll teams, tax officials, even software vendors-a bit of breathing room to get their systems in order before the new rules actually started biting.

Alongside the Act, the Central Board of Direct Taxes (CBDT) rolled out the Income Tax Rules, 2026. These replace the old 1962 rules entirely. What’s interesting is that drafts were shared publicly beforehand, feedback was invited, and suggestions floated around. Not something taxpayers usually notice, but it does explain why the rollout feels relatively coordinated.

In practical terms, though, it boils down to something very simple:

If your employer pays you salary from April 2026 onward, it’s governed by the new Act.

Which also means your company’s backend, payroll software, TDS calculations, and investment declaration forms should already reflect these changes. Ideally, this all happens quietly in the background, and you don’t have to think about it.

But if something looks off, higher TDS than expected, outdated forms, weird calculations, it’s worth raising it early with HR or finance. Waiting till filing season usually turns a small mismatch into a mildly annoying cleanup exercise.

Tax Year 2026-27 Explained: What Is The Difference Between Tax Year And Assessment Year?

This is one of those changes that doesn’t affect how much tax you pay, but quietly fixes a long-standing confusion that almost everyone has tripped over at some point.

Under the old system, you had this two-layer naming setup. You earned income in one year (called the “previous year”), and then filed taxes for it in another (called the “assessment year”). So, income from FY 2025–26 became AY 2026–27. Technically, it’s logical. But in practice? People constantly mixed it up, especially when filling out forms or dealing with banks.

The new law just removes that extra layer.

Now, if you earn income between April 1, 2026, and March 31, 2027, it all sits neatly under Tax Year 2026–27. That’s the label you’ll see everywhere—returns, notices, documents. No second name to keep track of and no mental translation required.

It’s mostly a language fix, to be honest. The timing of things hasn’t changed. You’ll still pay taxes, file returns, and deal with TDS pretty much on the same schedule as before. But the way it’s described is simpler, and that alone reduces a surprising amount of friction.

For salaried employees, the impact shows up in small but noticeable ways. Your Form 130 (the new Form 16), your ITR forms, even bank paperwork—they’ll all start using “Tax Year 2026–27.” Over time, institutions will adjust fully. For now, there might be a short phase where both terms float around.

If you need a quick mental shortcut:

Tax Year 2026–27 = what used to be called AY 2026–27. That’s really it. No deeper complication hiding underneath.

Differences Between Income Tax Act 1961 and 2025

The Income Tax Act of 1961 had a history. A lot of it. Over six decades, the law picked up amendments, court rulings, clarifications, layer after layer, until reading it felt a bit like walking through an old house where every room had been extended at a different time. Functional, yes. But not always intuitive.

By the end, it wasn’t just long, but it was dense. Sections stacked with provisos, explanations sitting on top of earlier explanations. You could get to the right answer, but not always quickly.

The 2025 Act doesn’t throw that system away, but it reorganises it. Think of it as a rewrite rather than a reinvention. The same core ideas are still there, but the presentation is cleaner. Instead of long-winded clauses, you’ll see more tables, clearer formulas, and fewer “if this, then that, except when” type constructions.

A few structural shifts stand out.

For one, the old “previous year vs assessment year” distinction is gone and replaced by the single tax year concept we just talked about. Then there’s consolidation: fewer forms, more streamlined compliance. And importantly, a lot of the financial thresholds—allowances, perquisites—have been updated to reflect what things actually cost today, not what they cost decades ago.

But here’s the part that’s easy to miss if you just skim headlines:

This is not a philosophical shift in taxation.

You still pay tax the same way. Employers still deduct TDS. Deductions, rebates, filing obligations—they all continue in familiar form. What’s changed is the packaging, the language and the thresholds. The paperwork you use to interact with the system.

So, if you’re a salaried employee, you’re not learning a new game, but you’re just adjusting to a cleaner version of the old one. Slightly less cluttered and a bit more aligned with reality.

Income Tax Slab Rates FY 2026-27 (New Tax Regime)

Is Salary Up To 12 Lakhs Tax-Free In 2026?

Short answer: yes, but only if you look at it the right way.

A salaried employee earning up to ₹12 lakh annually ends up paying zero tax under the new regime for Tax Year 2026–27, thanks to the Section 87A rebate. That rebate goes up to ₹60,000, which neatly cancels out whatever tax gets calculated on that income. So, on paper, there is tax. In reality, it disappears by the time you’re done computing.

Now here’s where it gets slightly more interesting. Once you factor in the ₹75,000 standard deduction, the “zero tax” ceiling quietly stretches to about ₹12.75 lakh in gross salary. It’s one of those details people miss, and then feel mildly annoyed about later.

So, someone earning ₹12.75 lakh, with no other income, lands at ₹12 lakh taxable income after the deduction, qualifies fully for the rebate, and walks away with zero tax liability. It’s clean and almost suspiciously neat math.

As for the slab structure itself, it’s more granular now. Less of those big jumps and more gradual steps:

- Up to ₹4 lakh: no tax

- ₹4–8 lakh: 5%

- ₹8–12 lakh: 10%

- ₹12–16 lakh: 15%

- ₹16–20 lakh: 20%

- ₹20–24 lakh: 25%

- Above ₹24 lakh: 30%

The idea seems fairly clear: ease the burden a bit in the middle ranges, where most salaried people actually sit. Not revolutionary, but definitely more refined than before.

Section 87A Rebate New Tax Regime 2026-27

This rebate is doing a lot of heavy lifting.

Under the new framework, if your total income doesn’t cross ₹12 lakh, you can claim a rebate of up to ₹60,000. It’s applied after calculating tax as per slabs—so it’s not a deduction, more like a final adjustment that wipes out your liability.

But there’s a catch, and a slightly unforgiving one.

The rebate is all or nothing. If your income is ₹12 lakh, you’re fine. ₹12,00,001? The rebate disappears completely. No gradual phase-out, no partial benefit. It’s just gone. That one-rupee jump can feel oddly expensive if you’re not planning around it.

Also, it doesn’t apply to certain types of income—like long-term capital gains taxed at special rates. But for a typical salaried employee without those extras, it works exactly as expected: it zeroes out your tax up to ₹12 lakh.

Has The Standard Deduction Changed For Salaried Employees for FY 2026-27?

No change here, and that’s not a bad thing.

The ₹75,000 standard deduction under the new regime stays exactly as it is. No bills, no proofs, and no awkward last-minute document hunts. It just quietly reduces your taxable income before anything else is calculated.

Under the old regime, it’s still ₹50,000. That ₹25,000 gap between the two regimes might not sound huge at first, but it does tilt the scales, especially for people who don’t have a long list of deductions to claim.

In a way, this higher standard deduction is part of what makes the new regime feel simpler. Fewer moving parts, fewer decisions to optimise.

Maximum Tax-Free Income 2026 Salaried

If you’re trying to pin down the exact number:

₹12.75 lakh is the effective maximum tax-free salary under the new regime.

That comes from ₹12 lakh (rebate ceiling) plus ₹75,000 (standard deduction). It’s a tidy combination, and for many people, it’s the number that actually matters more than the slabs themselves.

The old regime, on the other hand, doesn’t offer a clean, single threshold like this. You can reach zero tax at higher incomes, but only if you stack enough deductions: 80C, HRA, insurance, and so on. It’s doable, but it takes planning and paperwork.

The new regime, by comparison, feels almost passive. Less effort, but also fewer levers to pull.

Massive Hikes in Allowances: Is the Old Regime Making a Comeback?

If there’s one part of the new rules that actually feels like a shift, not just a cleanup, it’s this.

For years, a lot of allowances existed in name only. The numbers hadn’t kept up with reality. You’d see them in your CTC breakup, but the tax benefit was so tiny it barely moved the needle. Almost symbolic, like a leftover from an older version of the economy.

That’s changed now, and quite aggressively.

The Income Tax Rules, 2026, have gone back and revised these limits across the board. Not small tweaks, but meaningful jumps. The kind you actually notice in your take-home, not just in theory.

Some of the increases are honestly a bit startling when you see them side by side.

- Children’s education allowance: from ₹100 to ₹3,000 per month per child

- Hostel allowance: from ₹300 to ₹9,000 per month per child

- Meal vouchers: from ₹50 to ₹200 per meal

That’s not incremental, but that’s a reset.

And this is where things get slightly ironic. All these allowances? They only matter under the old tax regime. The new regime doesn’t let you claim them at all.

So suddenly, the old regime, which many people had mentally moved on from, starts looking relevant again. Not for everyone, but definitely for employees whose salary structure includes these components in a meaningful way.

Does this mean the old regime is making a full comeback?

Not exactly.

But it does mean the gap between old and new isn’t as one-sided as it looked a year ago. The decision now depends much more on how your salary is structured, not just how much you earn.

Expansion Of 50% HRA Exemption Cities List 2026

HRA rules themselves haven’t changed, but where they apply has, and that makes a bigger difference than it sounds.

Under the old regime, the HRA exemption is calculated as the lowest of three values:

- actual HRA received

- rent paid minus 10% of the basic salary

- a percentage of your basic salary based on your city

For years, only four cities—Delhi, Mumbai, Kolkata, and Chennai—qualified for the higher 50% threshold. Everywhere else, it was capped at 40%, even if rents told a completely different story.

That mismatch has finally been addressed.

Ahmedabad, Bengaluru, Hyderabad, and Pune have now been added to the 50% category. Which, frankly, feels overdue. Anyone who’s paid rent in these cities over the last decade probably saw this coming.

The updated list, eight cities in total, lines up much better with where housing is actually expensive in India today. It’s less about labels like “metro” and more about the real cost of living.

Is Bengaluru Eligible For 50% HRA in 2026?

Yes, very much so.

Bengaluru is now officially part of the 50% HRA category under the new rules. So, if your basic salary is ₹60,000 per month, the city-based component in the HRA calculation jumps from ₹24,000 (40%) to ₹30,000 (50%).

Now, whether you fully benefit depends on which of the three conditions becomes the limiting factor, but this change removes a pretty common bottleneck for many employees.

And realistically, given how rents have climbed in areas like Whitefield or HSR, this isn’t just a technical tweak. For a lot of people paying ₹25,000–₹40,000 in rent, it directly increases the exemption they can claim.

HRA Exemption Rules For Pune and Hyderabad 2026

Pune and Hyderabad follow the same upgrade; they’re now treated like top-tier cities for HRA purposes.

So instead of being stuck at 40%, employees in these cities can use the 50% salary benchmark while calculating exemption.

Let’s make that concrete.

If someone in Pune has a basic salary of ₹50,000 per month, the city-based limit moves from ₹20,000 to ₹25,000. That extra ₹5,000 per month doesn’t automatically become tax-free, but it raises the ceiling, which can matter depending on rent levels.

If your rent is high enough, this higher cap actually comes into play. If not, the “rent minus 10% of salary” condition still takes over. Either way, the system now has more room to reflect reality instead of cutting off too early.

Calculate HRA Under New Rules 2026

The formula itself hasn’t changed, which is helpful because it’s already complicated enough.

You still calculate HRA exemption as the lowest of:

- actual HRA received

- rent paid minus 10% of basic salary

- 50% or 40% of basic salary (depending on city)

The only update is that the 50% rule now applies to eight cities instead of four.

https://kpmg.com/xx/en/our-insights/gms-flash-alert/2026/flash-alert-2026-051.html

A quick example makes this clearer.

Say you’re in Hyderabad:

- Basic salary: ₹60,000/month

- HRA received: ₹28,000

- Rent paid: ₹25,000

Now calculate:

- Condition 1: ₹28,000

- Condition 2: ₹25,000 – ₹6,000 = ₹19,000

- Condition 3: 50% of ₹60,000 = ₹30,000

The exemption is the lowest—₹19,000 per month. The remaining ₹9,000 becomes taxable.

Interestingly, even with the higher 50% cap, in this case it doesn’t change the final number. The rent condition is still the limiting factor. But in other scenarios, especially where rent is higher, it absolutely can.

Children Education Allowance Tax Exemption 2026

This is one of those changes where you almost do a double-take the first time you see the numbers.

For years, the children’s education allowance sat at ₹100 per month per child. Not a typo—₹100. It hadn’t kept pace with reality for so long that most people stopped factoring it into their tax planning altogether.

Now, under the Income Tax Rules, 2026, that limit has been raised to ₹3,000 per month per child (for up to two children). That’s a thirty-fold increase. Suddenly, something that used to be negligible actually matters.

How Much Education Allowance Is Tax-Free In 2026?

If you run the numbers, it adds up fairly quickly.

For two children, you can now claim:

₹3,000 × 2 × 12 months = ₹72,000 per year as tax-free income.

Compare that to the earlier ₹2,400 per year ceiling, and the difference isn’t subtle anymore. It’s the kind of gap that can actually shift your old vs new regime calculation.

And in practical terms, this aligns better with reality. School fees in most cities aren’t anywhere near ₹100 per month, but they’re often ₹10,000, ₹20,000, sometimes more. This doesn’t cover everything, of course, but at least it’s no longer symbolic.

One important detail, though:

This exemption is available only under the old tax regime.

So, if you’re considering switching (or staying) in the old regime specifically because of this, you need to factor in the full ₹72,000 benefit when comparing options, not just look at slabs in isolation.

Also worth noting—your employer has to actually structure this as part of your salary. If it’s not in your CTC, you don’t get the benefit automatically.

Hostel Allowance Exemption Limit 2026

If the education allowance jump felt big, the hostel allowance revision is on another level.

Earlier, the exemption sat at ₹300 per month per child. Again, one of those numbers that had clearly outlived its relevance. Under the new rules, it’s been raised to ₹9,000 per month per child, for up to two children.

That means an employee can now claim up to ₹18,000 per month, ₹2,16,000 annually, as tax-free hostel allowance. Compared to the earlier ₹7,200 per year, it’s not even the same conversation anymore.

And realistically, this starts to resemble actual hostel costs, especially in bigger cities or university hubs where accommodation isn’t cheap.

But just like the education allowance, there’s a boundary you can’t ignore: this benefit exists only under the old tax regime.

So, if you’re someone whose salary includes hostel allowance, and your kids are actually staying in hostels, the math tilts more strongly toward the old regime than it did before. Not automatically, but noticeably.

In fact, for two children, the additional tax-free component compared to the old limits is over ₹2 lakh per year. That’s not a rounding error, but it’s the kind of number that can swing your entire tax decision if everything else is roughly balanced.

Meal Voucher Tax Exemption 2026 Limit

This one’s quieter, but still meaningful in day-to-day terms.

The exemption for meals provided by your employer has gone from ₹50 per meal to ₹200 per meal. On paper, that’s just a fourfold increase. In practice, it changes how useful meal benefits actually feel.

If you assume two meals a day over roughly 22 working days, the monthly exempt amount jumps from about ₹2,200 to ₹8,800. Over a year, that’s ₹1,05,600 instead of ₹26,400.

It’s not life-changing money, but it’s steady, recurring, and, importantly, tax-free under the old regime.

There’s another small but useful tweak alongside this: The tax-free limit for gifts, vouchers, and tokens from employers has increased from ₹5,000 to ₹15,000 per year.

So, those Diwali vouchers or occasional rewards? A larger portion of them now stays outside your taxable income.

Again, same pattern: these benefits strengthen the case for the old regime, but only if your salary structure actually includes them.

Old vs New Tax Regime 2026 Salaried: The Ultimate Decision

Up until recently, the comparison between old and new tax regimes felt almost predictable. For many people, the new regime was the easy default—simpler, cleaner, fewer calculations.

That’s no longer universally true.

With the sharp increase in allowance exemptions, the old regime has quietly become more competitive again. Not across the board, but enough that you can’t just assume one is better without running the numbers. The HRA changes, the education and hostel allowances, even meal benefits, they all stack up if your salary structure supports them.

So, the decision now isn’t just about income level. It’s about composition. Two people earning the same salary could land on completely different answers depending on how their CTC is structured.

Is Old Tax Regime Better In 2026 With New Allowances?

For certain employees, yes, it can be.

If your salary includes a meaningful HRA component (especially in one of the eight 50% cities), plus education allowance, hostel allowance, and meal benefits, the old regime starts looking a lot more attractive than it did even a year ago.

Take someone in Bengaluru, for example. They benefit from the higher HRA threshold and from the revised allowance limits. That combination can reduce taxable income quite significantly, sometimes enough to outweigh the simpler slabs of the new regime.

But, and this is important, this doesn’t apply to everyone.

If your salary is mostly fixed pay, with minimal allowances, and you’re not heavily investing under Section 80C, the new regime still holds its ground. The ₹75,000 standard deduction and the effective zero-tax threshold up to ₹12.75 lakh make it very appealing for a large chunk of salaried employees.

Also, remember: the new regime is still the default. If you haven’t actively opted otherwise, your employer is probably deducting TDS based on it.

Should I Choose Old or New Tax Regime For 15 Lakhs Salary?

This is where things get slightly less intuitive.

At ₹15 lakh annual salary, you’re right in the zone where the choice genuinely depends on details.

Under the new regime:

- Income after ₹75,000 standard deduction: ₹14.25 lakh

- Tax liability: roughly ₹1.42 lakh (before cess)

It’s straightforward. No planning required, no documentation stress.

Under the old regime, though, the outcome can shift quite a bit.

Let’s say:

- You claim HRA (especially in a 50% city)

- You invest ₹1.5 lakh under Section 80C

- You take the ₹50,000 standard deduction

- You claim ₹25,000 under Section 80D

You’re already looking at ₹3.75–₹4 lakh in deductions. Add in the revised allowances, and your taxable income drops further. At that point, the old regime often ends up giving you a lower tax bill than the new one.

There’s a rough “break-even” zone here, usually somewhere around ₹3.5–₹4 lakh in total deductions and exemptions. Cross that, and the old regime tends to win. Stay below it, and the new regime is usually simpler and cheaper.

Tax Saving Tips For Salaried Employees 2026

This part depends entirely on which regime you’re leaning toward.

Under the new regime, there isn’t much to optimise, and that’s kind of the point.

Your main levers are:

- ensuring the ₹75,000 standard deduction is applied correctly

- checking that employer-provided perks (meals, gifts, etc.) are taxed using the updated limits

It’s less about strategy, more about accuracy.

Under the old regime, though, it’s a different story.

Here, you actually have room to optimise:

- max out Section 80C (₹1.5 lakh)

- claim full HRA—especially with the expanded 50% city list

- use the higher education and hostel allowance limits

- claim health insurance under Section 80D

If your salary includes these components, you can reduce taxable income by ₹4–₹5 lakh or more. That’s where the old regime starts to pull ahead.

Can Salaried Employees Switch Tax Regimes Every Year?

Yes, and this flexibility is more useful than it sounds.

If you don’t have business income, you can switch between old and new regimes every year when filing your return. The choice you make at the start of the year (for TDS purposes) isn’t final—it just affects your monthly cash flow.

So even if your employer deducts TDS under the new regime, you can still choose the old regime later when filing, and claim a refund if excess tax was deducted.

That said, it’s still worth choosing carefully upfront. Getting it right early means better cash flow through the year instead of waiting for a refund later.

One small update here: your investment declaration is now made via Form 124 (instead of Form 12BB). That’s the document your employer uses to decide how much TDS to deduct.

If you have business income, though, the flexibility is limited, you don’t get to switch back and forth every year.

The End of Form 16: Navigating 2026 Tax Compliance

What Happened To Form 16 In 2026?

For most salaried people, Form 16 wasn’t just another document; it was the document. The one you downloaded, forwarded to your CA (or stared at yourself), and used for everything from filing returns to applying for loans.

That’s now changed.

Form 16 has been discontinued under the Income Tax Rules, 2026 and replaced with Form 130. Same purpose, different name, but the emotional adjustment might take a bit longer than the technical one.

Functionally, nothing dramatic has shifted. Form 130 still tells the same story—your salary, deductions, and TDS paid. It’s still your primary proof of income and tax compliance.

But here’s where it might get slightly awkward, at least for a while.

Banks, landlords, visa offices—they’ve all been conditioned for years to ask for “Form 16.” That habit won’t disappear overnight. So, there may be moments where you submit Form 130 and have to explain, briefly, that it’s the new equivalent.

A small friction point. Temporary, but real.

What Is Form 130 In Income Tax?

At its core, Form 130 is just the updated version of what Form 16 used to be, a TDS certificate issued by your employer.

It includes:

- total salary paid

- allowances and perquisites

- deductions applied

- total TDS deducted

So far, familiar territory.

What’s slightly new is the structure. Form 130 has three parts instead of two, with an additional annexure, mainly to accommodate cases like senior citizens receiving a pension or interest income from the same employer. For most salaried employees, this extra detail will just sit there quietly unless it’s relevant.

If you’ve changed jobs during the year, nothing changes in how you handle it. Each employer issues their own Form 130, and you combine them when filing your return, same as before.

Deadlines for issuing the form also remain aligned with the old system. So while the name has changed, the rhythm hasn’t.

Form 26AS New Name: Form 168 Explained

Another rename, this time for something slightly more behind-the-scenes.

Form 26AS, which many people checked (or at least intended to check) before filing returns, is now called Form 168.

It still does the same job: a consolidated view of your taxes, TDS from salary, TDS from other sources, advance tax, and even certain high-value transactions reported by banks or financial institutions.

Nothing fundamentally new here. Just a different label.

But it’s still important, arguably more than most people treat it. This is the document that confirms whether the tax your employer says they deducted has actually been deposited with the government.

If there’s a mismatch between your ITR and Form 168, that’s when notices tend to show up. Quietly at first, then less quietly.

Changes In PAN Quoting Requirements 2026

This is a smaller change, but one that shows up in everyday transactions.

The thresholds for when you need to quote your PAN, while buying a vehicle, making large deposits, paying hotels or restaurants, have been increased. It’s basically an acknowledgment that transaction values have gone up over time, and the old limits were starting to feel outdated.

There’s also a change in the forms used for PAN applications.

Form 49A and 49AA are out. They’ve been replaced by Form 93 and Form 95. And for non-residents (or those not ordinarily resident), there’s an added requirement, passport details, and citizenship information.

For most salaried employees, this won’t come up often. But if you’re moving abroad, returning from an assignment, or dealing with cross-border paperwork, it’s something to keep in mind.

New IT Returns Filing Deadline 2026

Some things, thankfully, stay exactly the same.

The deadline for filing income tax returns for salaried individuals (who don’t need an audit) continues to be July 31 of the following year.

So, for Tax Year 2026–27, the due date is July 31, 2027. No surprises there.

What will change is the form you use to file. New ITR forms under the 2025 Act are expected, and the old ones won’t apply anymore.

So sometime before filing season, it’s worth checking the income tax portal, not something most people do proactively, but useful this time around.

Preparing for the 2026 Tax Year: Next Steps

For most salaried employees, this transition isn’t something that forces immediate, drastic changes. Your tax liability doesn’t suddenly behave differently overnight. But there are a few quiet adjustments that can make a noticeable difference, especially if you catch them early.

The first thing worth doing, maybe sooner than you’d usually bother, is reviewing your salary structure with your employer.

This matters more than it used to.

If your CTC includes components like education allowance, hostel allowance, or meal benefits, there’s a good chance they’re still sitting at old limits in your payroll system. These don’t always auto-update. And if they don’t, you’re effectively leaving tax-free money on the table until you claim it later as a refund, which is fine, but not ideal.

A quick conversation with HR can sometimes translate into higher take-home pay throughout the year, not just a correction at filing time.

The second step is more specific, but important if it applies to you.

If you live in Bengaluru, Hyderabad, Pune, or Ahmedabad and claim HRA under the old regime, your employer needs to treat your city as a 50% category now. If their system hasn’t caught up yet, your HRA exemption might be calculated too conservatively, leading to higher TDS.

Not a disaster, you can recover it later, but again, it’s better fixed early than reconciled later.

Frequently Asked Questions (FAQs): 2026 Income Tax Rules for Salaried Employees

Yes. Under the new tax regime for Tax Year 2026-27, a gross salary up to ₹12.75 lakh is effectively tax-free. This is achieved by combining the ₹75,000 standard deduction with the Section 87A rebate, which wipes out your tax liability.

Form 16 is officially discontinued under the Income Tax Rules 2026 and replaced by Form 130 (your new primary TDS certificate). Furthermore, Form 26AS is now Form 168, and employee investment declarations use Form 124.

The 50% HRA exemption limit has expanded to eight cities. Salaried employees in Bengaluru, Pune, Hyderabad, Ahmedabad, Delhi, Mumbai, Kolkata, and Chennai can now use the 50% basic salary cap.

These massive hikes are only available under the old tax regime:

Children’s Education Allowance: Increased to ₹3,000 per month per child (up to ₹72,000 annually for two).

Hostel Allowance: Increased to ₹9,000 per month per child (up to ₹2,16,000 annually for two).

If you have substantial allowances (like 50% HRA) and Section 80C investments, the old tax regime may offer a lower tax bill. If your deductions are minimal, the new tax regime remains the most cost-effective choice.

No. You automatically claim a ₹75,000 standard deduction under the new tax regime and ₹50,000 under the old tax regime without needing to submit proofs.

Yes. Employees without business income can switch between the old and new tax regimes annually when filing their Income Tax Return (ITR).

The Income Tax Act 2025 eliminated the confusing “Assessment Year” terminology. Income earned from April 2026 to March 2027 simply falls under a unified Tax Year 2026-27.

Differences Between Income Tax Act 1961 and 2025 (Comparison Table)

| Feature or Allowance | Old System Detail (Pre-2026) | New System Detail (Post-April 2026) | Tax Regime Eligibility | Key Changes and Impact | |

| Tax Slabs (General) | Broad steps (e.g., ₹3-6 lakh, ₹6-9 lakh) | ₹4-8L (5%), ₹8-12L (10%), ₹12-16L (15%), ₹16-20L (20%), ₹20-24L (25%), Above ₹24L (30%) | New Regime (Default) | More granular steps to ease the tax burden in the middle-income ranges. | |

| Tax Slab: 0% Rate | Up to ₹3 lakh | Up to ₹4 lakh | New Regime (Default) | Base exemption limit increased to ₹4 lakh under the refined granular slab structure. | |

| Effective Zero-Tax Threshold | Approx ₹7.5 lakh (New Regime) | ₹12.75 lakh | New Regime (Default) | Combines ₹75,000 standard deduction and ₹60,000 Section 87A rebate to exempt gross income up to ₹12.75 lakh. | |

| HRA 50% City List | 4 Cities (Delhi, Mumbai, Kolkata, Chennai) | 8 Cities (Added: Bengaluru, Pune, Hyderabad, Ahmedabad) | Old Regime Only | Expands 50% basic salary cap for HRA to reflect rising rents in tech hubs; directly lowers taxable income for many. | |

| Hostel Allowance | ₹300 per month per child | ₹9,000 per month per child | Old Regime Only | Massive hike to ₹2,16,000 annually for two children; makes the Old Regime more competitive for parents. | |

| Children’s Education Allowance | ₹100 per month per child | ₹3,000 per month per child | Old Regime Only | A 30-fold increase reflecting modern costs; allows up to ₹72,000 annual exemption for two kids. | |

| Meal Vouchers | ₹50 per meal | ₹200 per meal | Old Regime Only | Increases daily tax-free meal benefit; total annual benefit can reach ~₹1.05 lakh. | |

| Gift/Voucher Exemption | ₹5,000 per year | ₹15,000 per year | Old Regime Only | Triple the previous limit for tax-free rewards and tokens from employers. | |

| TDS Certificate for Salary | Form 16 | Form 130 | Both Regimes | Formal renaming of the primary income proof; remains the primary document for bank loans and visa processing. | |

| Consolidated Tax Statement | Form 26AS | Form 168 | Both Regimes | Renaming of the background document used to verify TDS deposits with the government. | |

| Investment Declaration Form | Form 12BB | Form 124 | Mainly Old Regime | Updated form for employees to declare investments and HRA details to employers for TDS purposes. | |

| Tax Filing Year Terminology | Assessment Year vs Previous Year | Single “Tax Year” | Both Regimes | Removes naming confusion; income earned in 2026-27 is simply filed under Tax Year 2026-27. |

Action Step: Updating Investment Declarations with HR

This is one of those small administrative changes that can quietly trip people up.

The old Form 12BB is gone. Investment declarations are now made through Form 124.

This is the form where you tell your employer everything that affects your TDS, investments, HRA details, deductions, and allowance claims. It’s not glamorous, but it directly shapes how much tax gets deducted from your salary each month.

If your company has already switched to Form 124, it’s worth filling it out carefully and updating amounts to reflect the new allowance limits. If they haven’t switched yet and are still using the old format, that’s something to flag.

Because officially, from April 1, 2026 onward, the new forms aren’t optional.

If you’re still undecided between old and new regimes, this is also the moment to pause and run the numbers properly. Not roughly, but properly. The gap between the two isn’t trivial anymore.

Tools from platforms like ClearTax or Bajaj Finserv can help, but even a basic side-by-side calculation using your actual salary structur will get you surprisingly far.

One last thing, small, but you’ll run into it sooner than you expect.

Form 130 is now your Form 16. So, when a bank, lender, or anyone else asks for Form 16, you’ll be handing over Form 130 instead. Same legal standing, but different name.

For a while, you might need to explain that. Maybe once, maybe a few times. Then it’ll become normal, and nobody will think twice about it.

And stepping back for a second, this whole shift, at its core, is less dramatic than it first appears.

It’s a cleanup, a modernization, and long-overdue adjustment to numbers that hadn’t aged well.

For salaried employees, the wins are fairly concrete: higher allowance exemptions, better alignment with real-world costs (especially housing), and a compliance system that’s a bit less cluttered than before.

The obligations are largely the same, and the timelines are familiar.

What really changes is awareness—knowing the new limits, spotting where your salary structure hasn’t caught up yet, and making sure your employer is applying the rules correctly. That’s where most of the upside sits in 2026.

Disclaimer

The content on this page is intended for informational and educational purposes only and should not be construed as professional financial, tax, or legal advice. India Policy Hub and its authors are not certified financial planners, registered investment advisors, or practicing Chartered Accountants (CAs). Tax laws, particularly regarding international assets and compliance, are complex and subject to change. Always consult a qualified professional or Chartered Accountant regarding your specific financial situation, tax liabilities, or legal compliance before making any financial decisions or submitting tax declarations.

Discussion (5)

Leave a Reply