PPF vs. EPF vs. NPS in 2026: The Complete Guide to Indian Retirement Funds

Navigating India’s 2026 Retirement Landscape: The Strategic Roles of PPF, EPF, and NPS

The Public Provident Fund, better known as PPF, has held a special place in Indian households for decades. Ask almost any middle-class family about long-term savings, and chances are PPF comes up somewhere in the conversation. And honestly, it makes sense. It’s backed by the Government of India, carries virtually no credit risk, and offers a combination that’s increasingly rare in personal finance: safety, predictability, and tax efficiency. This guide provides you with a deep dive into the topic of PPF vs EPF vs NPS in 2026.

In a market full of noise, stocks running hot one year, debt products looking shaky the next, PPF remains steady. Maybe not exciting, but dependable. And when you’re planning for retirement, dependability matters more than flashiness.

At a Glance: PPF vs. EPF vs. NPS (2026 Quick Comparison)

Short on time? Here is the executive summary of India’s top three retirement funds to help you structure your long-term wealth strategy:

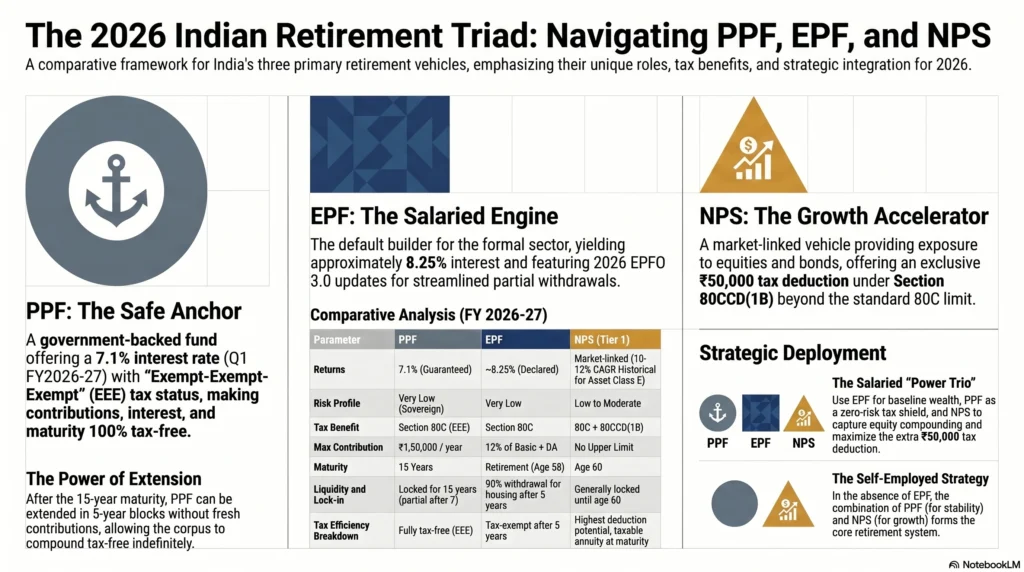

- Public Provident Fund (PPF) – The Safe Anchor: Offers a sovereign-backed, guaranteed 7.1% interest rate (Q1 FY2026-27). With a 15-year lock-in, it boasts the coveted “Exempt-Exempt-Exempt” (EEE) tax status, meaning your contributions, accumulated interest, and final maturity corpus are 100% tax-free.

- Employees’ Provident Fund (EPF) – The Salaried Engine: The default wealth-builder for formal sector employees, combining employer and employee contributions (historically yielding ~8.25%). It remains tax-exempt if held for 5 continuous years. The 2026 EPFO 3.0 updates have streamlined partial withdrawals for housing, education, and medical needs.

- National Pension System (NPS) – The Growth Accelerator: A market-linked, highly regulated pension vehicle offering exposure to equity and corporate bonds. NPS Tier 1 provides an exclusive ₹50,000 tax deduction under Section 80CCD(1B)—over and above the standard 80C limit. Funds are locked until age 60, after which up to 60% can be withdrawn tax-free as a lump sum (or via Systematic Lump Sum Withdrawal), with the remaining 40% routed to a mandatory annuity.

The Strategist’s Takeaway: Do not view these as competing products. A robust 2026 retirement portfolio leverages EPF for automated baseline wealth, PPF as a zero-risk tax shield, and NPS to capture equity-driven compounding and maximum tax efficiency.

PPF Interest Rate 2026: Latest Updates

As of Q1 FY2026–27 (April to June 2026), the PPF interest rate stands at 7.1% per annum, compounded annually. The government reviews PPF rates every quarter, although interestingly, this rate has stayed unchanged since April 2020. That kind of stability is rare, especially for an instrument that still offers government-backed returns.

One detail many investors miss, sometimes until it’s too late, is how PPF interest is calculated. Interest is based on the lowest balance between the 5th and the last day of each month. Sounds technical, but it has a practical consequence: if you’re making your yearly contribution, it’s smart to deposit before the 5th of April. Miss that window by even a day, and you lose a month’s worth of interest on that contribution. Not catastrophic, maybe—but over 15–20 years, those small misses stack up.

For the latest rate notifications and government circulars, you can use these guides by Bajaj Finserv and AngelOne, which carry timely reminders on annual deposit deadlines.

Another reason PPF continues to attract long-term investors? It’s EEE (Exempt-Exempt-Exempt) tax status. Your contributions qualify under Section 80C, the interest earned stays tax-free, and your maturity amount isn’t taxed either. For someone in a higher tax bracket, that often makes the real post-tax return far more attractive than a fixed deposit that looks better on paper but gets chipped away by taxes.

Step-by-Step: How to Open a PPF Account Online in SBI YONO App

Opening a PPF account used to mean paperwork, branch visits, and the kind of waiting that somehow always felt longer than it actually was. That’s changed. In 2026, if you already have an SBI savings account and your KYC is in place, the whole process can usually be done from your phone in just a few minutes.

For many investors, especially first-timers, that convenience removes a big mental barrier. Starting is often the hardest part.

Here’s how the process works on SBI’s YONO app. (If you want a full checklist of supporting documents before you begin, refer to this guide.

Step 1: Download and log in to the SBI YONO app using your registered mobile number and internet banking credentials. Before you begin, make sure your SBI savings account is active, KYC-compliant, and linked to your Aadhaar and PAN where applicable.

Step 2: Once inside the app, head to “Investments” → “PPF” → “Open PPF Account.” The navigation is fairly straightforward, though depending on app updates, menu placement can shift a little.

Step 3: Choose whether you’re opening the account in your own name or as a guardian for a minor. A lot of parents use PPF as a long-term wealth-building tool for children, but it’s worth remembering: by law, an individual can hold only one PPF account in their own name.

Step 4: Fill in your PAN details, Aadhaar information, nominee details, and other basic account information. A surprising number of people skip the nominee section, thinking they’ll “do it later.” Some do. Many don’t. And that can create avoidable complications down the road.

Step 5: Set your contribution preference. You can invest anywhere between ₹500 and ₹1,50,000 per financial year, either as a lump sum or through instalments (up to 12 contributions annually). Many investors choose to automate this using a Standing Instruction (SI), which frankly removes a lot of procrastination from the equation.

Step 6: Complete the e-sign process using Aadhaar OTP verification. Once verified, your PPF account number is generated, and your digital passbook becomes available inside the app.

If you prefer the old-school route, or just like speaking to a human before locking money away for 15 years, you can still open a PPF account by visiting an SBI branch, a post office, or any other authorised bank and submitting the PPF-1 form with your KYC documents.

If you’re still deciding which bank suits your broader banking needs, Scripbox maintains a useful guide.

A small observation most seasoned investors eventually make: where you open your PPF account matters less than whether you consistently fund it. The account itself does the heavy lifting. Discipline does the rest.

Using a PPF Calculator for 15 Years (1.5 Lakh Annual Investment)

One of the biggest reasons investors stay loyal to PPF, sometimes for decades, is simple: you know what you’re getting into.

There’s no guessing. No market panic. No waking up to a red portfolio because some global event rattled equities overnight. PPF doesn’t promise drama. It promises consistency. And for long-term retirement planning, that kind of predictability has real value.

If you invest the maximum allowed ₹1,50,000 every year and continue doing that for the full 15-year lock-in period, here’s what the numbers look like at the current 7.1% annual interest rate:

| Year | Annual Investment (₹) | Total Investment (₹) | Interest Earned (₹) | Closing Balance (₹) |

| 1 | 1,50,000 | 1,50,000 | 10,650 | 1,60,650 |

| 5 | 1,50,000 | 7,50,000 | 1,19,186 | 8,69,186 |

| 10 | 1,50,000 | 15,00,000 | 5,39,447 | 20,39,447 |

| 15 | 1,50,000 | 22,50,000 | 18,18,209 | 40,68,209 |

So over 15 years, you have contributed ₹22.5 lakh out of your own pocket. By the end of the term, that grows to roughly ₹40.68 lakh—and importantly, that maturity amount remains completely tax-free under current PPF rules.

That’s where the real magic of compounding starts to become visible. You’re not just saving money anymore; your money starts doing a decent amount of the lifting for you. Nearly ₹18.2 lakh of the final corpus comes purely from accumulated interest. Quiet growth, year after year. Nothing flashy. But very hard to ignore.

If you want to test different contribution amounts, timelines, or compare PPF against other retirement products, you can run your own projections using the calculators available here.

And here’s something many first-time investors overlook: the real power of PPF often starts after year 15, not before it.

Once the original maturity period ends, you don’t have to withdraw the money. You can extend the account in blocks of five years, either with fresh contributions or without adding a single rupee more. That means your existing corpus can continue compounding, tax-free, into your 50s, 60s, or even beyond.

That’s when PPF quietly shifts from being a savings product to becoming a serious retirement asset.

PPF Premature Withdrawal Rules & Extensions Explained

PPF is built for patience. That’s really the point of the product. It’s designed to reward people who can think in decades instead of months, which, admittedly, is easier said than done when life starts throwing expensive surprises your way.

Still, life doesn’t always wait for a 15-year lock-in to finish. Medical emergencies happen. Education costs show up faster than expected. Sometimes priorities change. That’s why PPF does offer limited flexibility, but the rules matter, and they’re worth understanding before you ever need them.

The withdrawal framework below draws from the official rules explained in here.

Partial Withdrawals (After Year 7)

You become eligible for partial withdrawals starting from the 7th financial year after opening your account.

There’s a catch, actually, two.

You can make only one withdrawal per financial year, and the amount you can withdraw isn’t simply “whatever is in the account.” Instead, the maximum permitted amount is the lower of:

- 50% of the account balance at the end of the 4th year preceding the withdrawal year, or

- 50% of the balance at the end of the immediately preceding year

Yes, it’s a bit bureaucratic. Very PPF. But once you understand the formula, planning becomes easier.

Premature Account Closure (After 5 Years)

If you need to close your PPF account before maturity, premature closure is allowed, but only after 5 completed financial years, and only for specific reasons.

These include:

- Treatment of a life-threatening illness involving the account holder or dependent family members

- Higher education expenses for the account holder or minor children

- Change in residential status, such as becoming an NRI

Premature closure comes with a cost: the applicable interest rate is reduced by 1% for the period your account was active.

That penalty may not sound huge at first glance, but over several years, it can noticeably reduce your final corpus.

Loan Against PPF (Years 3–6)

This is one feature that often surprises people.

Between the 3rd and 6th year of your account, you may be eligible to take a loan against your PPF balance instead of withdrawing from it.

The loan amount can be up to 25% of the balance at the end of the 2nd financial year immediately preceding your loan application.

The interest charged is currently PPF rate + 1%.

For investors who need short-term liquidity but don’t want to disturb long-term compounding, this can be a smarter move than breaking other investments.

What Happens After 15 Years?

This is where PPF quietly becomes far more powerful than many people realise.

At maturity, you have three options:

Option 1: Withdraw the entire corpus and close the account. Clean, simple, done.

Option 2: Extend the account for another 5 years without making fresh contributions. Your existing balance continues earning interest, currently 7.1%, without requiring additional capital.

Option 3: Extend for another 5 years with fresh contributions, continuing to invest up to ₹1.5 lakh annually while retaining all associated tax benefits.

And honestly? Option 2 is probably one of the most underrated wealth-building features in Indian finance.

By that stage, your corpus is usually large enough that compounding itself starts doing the heavy lifting. No fresh money. No extra effort. Just time, quietly working in the background.

For updated deposit limits and budget-related changes to PPF rules, you can refer to this guide.

EPF Withdrawal & UAN Guide 2026: How to Check Your PF Balance & Claim Online

For millions of salaried employees in India, the Employees’ Provident Fund (EPF) isn’t just another deduction on a payslip, it’s often the single largest retirement asset they build during their working years.

At first, most people barely pay attention to it. The contribution gets deducted automatically, the employer adds their share, and life moves on. Then one day, usually after a job switch, a home purchase plan, or the first serious retirement calculation, you look at your EPF balance and realise something: this quiet little account has been doing serious work in the background.

That’s the real strength of EPF. It combines employee contributions, employer contributions, government-declared interest, and tax advantages into a structure that compounds steadily over decades.

But there’s a catch: if you don’t understand how to manage it, especially your UAN (Universal Account Number),, you can end up with fragmented accounts, KYC issues, delayed withdrawals, or missing service records.

And honestly, those problems tend to show up at the worst possible time—when you actually need the money.

PF Balance Check Online: UAN Number, Missed Call & Passbook Download

Your Universal Account Number (UAN) is essentially your financial identity inside the EPFO ecosystem. Think of it as the permanent thread connecting all your PF accounts across different employers.

Change jobs five times? Your UAN stays the same.

Move cities? Same UAN.

Switch industries entirely? Still the same UAN.

That continuity matters because your retirement history, contribution records, transfers, claims, and KYC details all sit under that number.

How to Activate Your UAN

If you haven’t activated your UAN yet, the process starts on the EPFO member portal.

You’ll need:

- Your UAN (usually provided by your employer)

- Your registered mobile number

- Aadhaar-linked personal details

Once activation is complete, you get access to your full EPF dashboard, passbooks, transfer requests, withdrawal claims, profile updates, nomination details, basically everything.

It’s one of those things that takes a few minutes to set up but can save hours of frustration later.

Multiple Ways to Check Your PF Balance

EPFO has made balance checking easier over the years, and thankfully, you’re no longer tied to one method.

1. EPFO Member Passbook Portal

This is the most detailed option.

Log in at https://passbook.epfindia.gov.in/MemberPassBook/Login using your UAN and password to download your passbook.

You’ll see:

- Monthly employee contributions

- Employer contributions

- Interest credits

- Transfers from old employers

- Any withdrawal history

If you’ve switched jobs multiple times, this is usually the first place to check whether all your service history has carried forward correctly.

2. Missed Call Service

Sometimes you just want a quick balance update without logging in.

Give a missed call to 9966044425 from your UAN-registered mobile number.

Within minutes, you’ll receive an SMS with your latest PF balance.

Simple. Old-school. Still works.

3. UMANG App

The government’s unified mobile platform, available at https://umang.gov.in, also integrates EPF services.

From the app, you can:

- Check balances

- Track withdrawal claims

- Access passbooks

- Update certain account details

For people who prefer mobile access over web portals, this usually feels smoother.

4. SMS Service

Send “EPFOHO UAN ENG” to 7738299899 from your registered mobile number.

You’ll receive your balance details via SMS.

You can also change the language code at the end depending on your preferred language.

A small thing, but useful.

Keep Your KYC Updated

Here’s where a lot of EPF withdrawal delays begin: incomplete KYC.

If your Aadhaar, PAN, or bank account details don’t match your EPFO records, claims can get delayed or rejected outright.

So before you ever think about withdrawing, transferring, or merging accounts, make sure your KYC is updated.

Detailed guides are available here.

It’s not glamorous paperwork. Nobody enjoys doing it.

But when retirement money, or even emergency withdrawals, are involved, clean records matter more than most people realise.

EPF Withdrawal Rules 2026: Home Purchase, Construction & Tax Implications

If there’s one part of EPF that employees tend to pay attention to a little later than they should, it’s withdrawal rules.

Most people know money is being deducted every month. Fewer know when they can access it, how much they can withdraw, or what tax consequences might quietly follow if they get the timing wrong.

And in 2026, EPF rules have become more flexible, but also a little more layered.

One of the biggest developments this year has been the rollout of EPFO 3.0, a major modernization push that introduces ATM-based and UPI-linked PF withdrawals for eligible claims. For a system long associated with paperwork, employer approvals, and delayed processing, this is a pretty meaningful shift.

Detailed coverage of this update is available here.

Here’s what actually matters for members in 2026.

Full Withdrawal

You can withdraw your entire EPF balance under the following situations:

- Upon retirement, generally at 58 years of age

- After 2 months of continuous unemployment

There’s also an important flexibility built in.

If you remain unemployed for 1 month, you may withdraw up to 75% of your corpus, while the remaining balance stays invested.

That’s useful because job transitions don’t always go as planned. Sometimes what’s meant to be a two-week break quietly turns into three months.

Having partial access to your EPF can act as a financial buffer during those in-between phases.

Partial Withdrawal for Home Purchase or Construction

This is one of the most commonly used EPF withdrawal provisions, and understandably so.

After completing 5 years of EPF membership, members can withdraw up to 90% of their PF balance for:

- Buying a residential property

- Constructing a home

- Repaying certain housing-related obligations

The property must be registered in your name, or jointly with your spouse.

An important detail many employees miss: your 5-year eligibility period can include service across multiple employers, as long as your EPF accounts were properly transferred.

Which is exactly why merging old accounts matters.

Partial Withdrawal for Medical Emergencies

Life has a way of ignoring financial timelines.

For serious medical needs, EPF allows withdrawals of up to:

- 6 times your monthly basic salary plus dearness allowance, or

- Your employee contribution with accumulated interest, whichever is lower

This can be used for hospitalization and specified treatment scenarios.

In practical terms, it often becomes emergency liquidity without forcing families to break fixed deposits, liquidate mutual funds, or borrow at high interest rates.

Partial Withdrawal for Marriage or Education

After completing 7 years of service, EPF members may withdraw up to 50% of their employee share plus interest for:

- Marriage expenses

- Higher education costs

This applies to your own needs, as well as eligible family members in specified situations.

Not every life milestone needs debt. Sometimes your own long-term savings can quietly support the big moments.

Tax Implications of EPF Withdrawals

This is where mistakes can get expensive.

If you withdraw EPF funds before completing 5 continuous years of service, the withdrawal may attract Tax Deducted at Source (TDS).

Current rates include:

- 10% TDS if PAN is available

- 20% TDS if PAN is not submitted

Detailed tax reference in this guide

However, if you complete 5 continuous years of service, EPF withdrawals are generally fully tax-exempt.

That 5-year rule matters a lot.

And there’s another tax angle higher-income employees should know.

If your annual employee EPF contribution exceeds ₹2.5 lakh, the interest earned on the excess contribution becomes taxable in the year it accrues.

This rule has remained in force under the new Income Tax Act 2025.

Other Important 2026 Updates

EPFO has also extended its mid-de-linking facility in 2026, allowing members to de-link PF accounts from previous employers in specific scenarios—especially where employment records or legacy account mappings create complications.

Detailed guidance is available here:

And for a broader overview of EPFO changes, including dormant account activation, pension updates, and revised processing workflows, this summary is useful.

At the end of the day, EPF isn’t just a retirement bucket. For many employees, it quietly doubles as an emergency reserve, a housing support mechanism, and sometimes even a bridge between jobs.

The trick is knowing when to touch it and when not to.

Online EPF Management: Form 15G, Merging Accounts & Correcting Details

Managing your EPF used to feel unnecessarily complicated. Too many portals, too many forms, too many moments where you’d wonder whether your request had actually gone through or just disappeared into some administrative black hole.

Thankfully, things are better now. Not perfect, but definitely better.

In 2026, most EPF account management tasks can be handled online, which means fewer branch visits, less back-and-forth with HR, and a lot more control sitting directly with the employee.

Still, the system works best when your records are clean. That’s really the theme here.

Submitting Form 15G Online

If you’re planning to withdraw from your EPF and your total taxable income falls below the basic exemption limit, Form 15G can help you avoid unnecessary TDS deductions.

A lot of employees discover this only after tax has already been deducted which is frustrating, because by then you’re dealing with refund claims instead of prevention.

In 2026, Form 15G can be submitted fully online through the EPFO member portal.

Before filing, make sure:

- Your PAN is linked and verified

- Your bank details are updated

- Your Aadhaar KYC is complete

- Your withdrawal eligibility conditions are already met

It’s a small form, but if you’re eligible, it can make a noticeable difference in cash flow during withdrawal.

Merging Multiple PF Accounts

If you’ve changed jobs even a couple of times, there’s a decent chance you’ve accumulated multiple EPF member IDs.

That’s normal.

What’s not ideal is leaving them scattered.

Every job switch can create a fresh EPF member account under the same UAN unless the old balance is properly transferred. If those accounts remain unmerged, you can run into:

- Incomplete service history

- Tax complications during withdrawal

- Confusion around the 5-year continuous service rule

- Delays in claims processing

To merge your accounts:

- Log in to the EPFO member portal

- Navigate to “Online Services” → “One Member – One EPF Account (Transfer Request)”

- Verify your previous employment details

- Submit the transfer request

In many cases, your previous employer may need to approve the transfer.

It can take some time, sometimes longer than expected, but it’s worth doing. Clean consolidation now prevents administrative headaches later.

And honestly, few things are more annoying than discovering an old PF balance from seven years ago while trying to plan retirement.

Correcting EPF Details

Name mismatches. Wrong dates of birth. Aadhaar spelling differences. PAN mismatches.

Tiny errors on paper surprisingly big problems in practice.

These issues often don’t surface until you file a claim, update KYC, or attempt a withdrawal. That’s when people realize their EPF profile doesn’t match their official documents.

If your account is Aadhaar-verified, many basic corrections, such as name or date of birth updates, can now be initiated directly from the EPFO member portal.

For major corrections, especially where employer records need verification, you may need to submit a Joint Declaration Form, available on the official EPFO forms page:

A practical rule a lot of experienced employees follow: every time you switch jobs, spend ten minutes checking your EPF profile.

It feels unnecessary until one day it saves you weeks.

NPS Tier 1 vs Tier 2 (2026): Maximize Your Retirement Corpus & Section 80CCD(1B) Tax Benefits

If PPF is the steady, predictable workhorse of retirement planning and EPF is the default wealth-builder for salaried employees, then NPS sits in a different lane altogether.

It’s more flexible. More market-linked. A little less emotionally comforting for conservative investors, maybe. But over long-time horizons? Potentially far more powerful.

That’s exactly why the National Pension System has become increasingly relevant in 2026, especially for professionals, business owners, freelancers, and higher-income taxpayers who want something beyond traditional fixed-return instruments.

Unlike PPF or EPF, NPS gives you exposure to equity, corporate bonds, government securities, and alternative assets, all under a retirement-focused framework regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

Operational oversight comes through the NPS Trust and Central Recordkeeping Agencies like Protean eGov Technologies.

And honestly, that structure matters. Retirement investing works best when the system behind it feels boring, regulated, and hard to break.

NPS Tier 1 vs Tier 2 Account: Key Differences Explained

Before investing in NPS, you need to understand one thing clearly: Tier 1 and Tier 2 are not the same product.

They share the same ecosystem, but they serve very different purposes.

The comparison below draws from detailed analyses in this guide:

| Feature | NPS Tier 1 | NPS Tier 2 |

| Purpose | Mandatory retirement account | Voluntary investment account |

| Minimum Contribution | ₹500 per contribution; ₹1,000/year | ₹250 per contribution |

| Withdrawals | Restricted until age 60 | Anytime |

| Tax Deduction | Eligible | Generally not available |

| Asset Allocation | Active or Auto | Active or Auto |

| PRAN | Required | Requires active Tier 1 |

At first glance, Tier 2 looks more attractive. more flexible, no lock-in, easier access.

But the real reason most investors choose Tier 1 is tax efficiency.

The Real Tax Advantage: Section 80CCD(1B)

This is where NPS quietly separates itself from almost every other retirement product in India.

Tier 1 contributions qualify for the additional Section 80CCD(1B) deduction of ₹50,000—over and above the standard ₹1.5 lakh Section 80C limit.

That “extra” ₹50,000 often becomes the deciding factor for tax-conscious investors.

For someone in the 30% tax bracket (plus cess), that can translate into roughly ₹15,600 in annual tax savings.

Not a theoretical benefit. Real money saved every year.

Detailed breakdowns are available here:

Over a 20–25 year career, that annual tax advantage alone can compound into something meaningful.

So What About Tier 2?

Tier 2 is different.

Think of it less as a retirement account and more as a low-cost investment wrapper.

It gives you:

- Exposure to the same pension fund managers

- Extremely low expense ratios

- Flexible entry and exit

- No long lock-in period

What it generally doesn’t give most investors is a tax deduction.

(There’s a limited exception for certain government employees.)

That means for most individuals, Tier 2 works better as:

- Medium-term investing

- Parking surplus funds

- Tactical debt/equity allocation

- Building liquidity outside retirement lock-ins

In other words: Tier 1 is where the retirement strategy lives.

Tier 2 is where flexibility lives.

And depending on your goals, both can have a place, but they shouldn’t be confused.

The biggest mistake new investors make with NPS isn’t choosing the wrong fund.

It’s choosing the right fund inside the wrong account type.

How to Open an NPS Account Online Through Aadhaar eKYC

Opening an NPS account in 2026 is dramatically easier than it used to be.

A few years ago, pension products still carried that old-world reputation—forms, signatures, branch visits, courier documents, follow-up calls. A bit of friction at every step. These days? If your Aadhaar, PAN, and bank details are in order, you can usually get started from your laptop or even your phone in less time than it takes to finish a cup of coffee.

That shift matters, because with retirement investing, the hardest part often isn’t choosing the product.

It’s starting.

Thankfully, the eNPS ecosystem has made that first step much smoother.

Route 1: Opening Through Protean CRA

One of the most common routes is through Protean eGov Technologies, which operates one of the official Central Recordkeeping Agency platforms for NPS.

Visit:

Once you’re there:

Step 1: Click on “New Registration.”

Step 2: Select “Individual Subscriber.”

Step 3: Choose your preferred KYC method:

- Aadhaar OTP verification

- Aadhaar Offline KYC

Most people prefer OTP verification simply because it’s faster.

Step 4: Fill in your personal details, including:

- Full name

- Date of birth

- Address

- PAN details

- Mobile number

- Email ID

- Nominee information

This is also where you’ll enter your bank account details—which becomes important later for withdrawals, exits, or pension payouts.

Step 5: Choose your Pension Fund Manager (PFM) and asset allocation strategy.

This is where NPS becomes more personalized.

You can either:

- Select Active Choice, where you manually allocate across equity, corporate bonds, government securities, and alternative assets

- Or choose Auto Choice, where allocations adjust automatically as you age

For first-time investors who don’t want to actively rebalance portfolios every few years, Auto Choice often feels like the easier starting point.

Step 6: Upload your signature and photograph if required.

Step 7: Make the minimum contribution of ₹500 online.

Once the payment goes through, your Permanent Retirement Account Number (PRAN) is generated.

That PRAN becomes your lifelong NPS identity.

And yes, keep it somewhere safe. Future you will thank you.

Route 2: Through NSDL eNPS Portal

You can also register through:

The process is broadly similar—same Aadhaar-based onboarding, same PRAN generation, same paperless experience.

Some investors use whichever interface feels smoother. Others simply go through whichever portal their employer or bank recommends.

Either route works.

Opening NPS Through Your Bank

If you already bank with institutions like State Bank of India, HDFC Bank, ICICI Bank, or Axis Bank, there’s a good chance you can open your NPS account directly through net banking.

Official portals include:

https://www.icici.bank.in/personal-banking/investments/government-schemes/nps-national-pension-system

https://www.hdfcpension.com/nps-recent-changes/

Bank-based onboarding often feels easier for people who already have KYC verified through existing accounts.

For login and account access guidance, refer to this guide.

Important 2026 Updates

NPS has also seen some notable infrastructure upgrades in 2026.

One of the biggest is Protean CRA’s Multiple NAV framework, effective April 1, 2026:

In plain English? It improves pricing accuracy across different transaction types, making the accounting process fairer for subscribers.

Another practical improvement: NPS contributions can now be made through UPI and Bharat Bill Payment System (BBPS).

Her is the official circular.

That might sound like a small operational tweak, but it matters.

Because the easier it becomes to contribute regularly the more likely people actually will.

And with retirement planning, consistency usually beats complexity.

Every single time.

NPS Returns Calculator (60 Years) & Choosing a Pension Fund Manager

This is where NPS starts to feel very different from PPF or EPF.

With those products, the return is largely known in advance. With NPS? Not quite.

NPS is market-linked, which means your final corpus depends on three things more than anything else:

- How early you start

- How consistently you contribute

- And who manages your money

That last part, your Pension Fund Manager (PFM), often gets overlooked by first-time investors. Understandably. Most people are busy figuring out tax deductions, PRAN registration, and whether to choose Active or Auto allocation. Fund manager selection feels like something they’ll “look into later.”

Sometimes later becomes 10 years.

And by then, compounding has already picked a direction.

What Kind of Returns Has NPS Historically Delivered?

Unlike fixed-return retirement products, NPS returns vary depending on the asset class you choose.

Historically, long-term performance has broadly looked like this:

- Asset Class E (Equity): Around 10–12% CAGR over 10-year periods among top-performing schemes

- Asset Class C (Corporate Bonds): Roughly 8–9% CAGR

- Asset Class G (Government Securities): Typically, 7–8% CAGR

These figures are drawn from here.

Of course, past returns don’t guarantee future performance. Markets have a way of humbling anyone who forgets that.

Still, over long investment horizons—20, 25, 30 years—equity exposure has historically done a lot of heavy lifting.

Sample NPS Corpus Projection

Let’s make this more real.

Imagine you’re 30 years old and contribute ₹10,000 every month into NPS until age 60.

That’s a 30-year investment horizon.

Assuming a blended annual return of 9%, here’s what the numbers roughly look like:

- Total Contribution: ₹36,00,000

- Estimated Corpus at Age 60: ~₹1.84 crore

- Mandatory Annuity Purchase (40%): ~₹73.6 lakh

- Lump Sum Withdrawal (60%): ~₹1.10 crore

That’s the power of time more than anything else.

Not genius stock-picking. Not timing the market.

Just consistency.

If you want to run your own numbers with different ages, contribution levels, or expected returns, you can use the calculator here.

And honestly, if you’re serious about retirement planning, running your own projections once a year is one of the smartest habits you can build.

Choosing a Pension Fund Manager

India currently has several PFRDA-approved pension fund managers, and while all operate under the same regulatory framework, performance can differ over time.

Among the stronger performers in the Scheme E (Equity – Tier I) category in early 2026 are:

- SBI Pension Funds

- HDFC Pension Management

- ICICI Prudential Pension Fund

- UTI Retirement Solutions

Historical NAV and scheme data can be reviewed here.

Protean’s comparative analysis tools are also useful:

One underappreciated feature of NPS: you can switch your PFM once every year at no cost.

That flexibility matters.

If your chosen fund consistently trails its peer group—not for one quarter, not for one noisy market cycle, but over several years—you’re not locked in forever.

Active Choice vs Auto Choice

This decision shapes your risk profile more than your PFM selection.

Active Choice gives you control.

You decide how much goes into:

- Equity (E)

- Corporate Bonds (C)

- Government Securities (G)

- Alternative Assets (A)

That’s great if you actually enjoy portfolio management.

Most people say they do.

Fewer actually revisit allocations consistently.

Then there’s Auto Choice.

Here, the system gradually reduces equity exposure as you age—more growth when you’re younger, more stability as retirement gets closer.

For investors who don’t want to actively rebalance every few years, this is often the more realistic choice.

There’s also the Balanced Life Cycle Fund, detailed here:

It maintains a moderate equity allocation, striking a middle ground between growth and stability.

And honestly? Retirement investing doesn’t usually fail because people chose the wrong fund.

It usually fails because they stop contributing.

Or start too late.

Everything else comes second.

NPS Maturity, Annuities & Premature Withdrawal Rules

This is usually the point where people realize something important about NPS:

Building the retirement corpus is only half the story.

The other half? Knowing how you can actually access it.

And this is where NPS feels a little different from most investment products. It isn’t designed to simply let you build wealth and walk away whenever you want. It’s built with a specific goal—retirement income. Which means the exit rules are structured to keep that long-term purpose intact.

Sometimes that feels restrictive. Sometimes it’s exactly the discipline people need.

Either way, if you’re investing in NPS, you need to understand how maturity, withdrawals, annuities, and early exits actually work—before retirement sneaks up on you.

What Happens at Maturity (Age 60)?

Once you reach 60 years of age—or your official superannuation age—you become eligible to exit your NPS Tier 1 account.

At that stage, current rules require:

- At least 40% of your total corpus must be used to purchase an annuity from a PFRDA-registered Annuity Service Provider (ASP)

- The remaining 60% can be withdrawn as a lump sum, and under current tax rules, this portion is tax-free

That structure exists for one reason: to ensure at least part of your retirement savings turns into a steady income stream instead of being withdrawn and spent all at once.

And honestly… that’s not always a bad design.

If your total NPS corpus is below ₹5 lakh, the annuity requirement does not apply, and you can withdraw the entire amount as a lump sum.

Official exit rules and regulations are available here:

Can You Continue Beyond Age 60?

Yes, and a lot of investors still don’t realize this.

NPS contributions can continue up to age 75.

That gives working professionals, consultants, business owners, or anyone delaying retirement the flexibility to keep building their corpus even after the traditional retirement age.

For people earning later in life, which is increasingly common, that extension can be genuinely valuable.

Systematic Lump Sum Withdrawal (SLW)

One of the more practical upgrades to NPS in recent years is the introduction of Systematic Lump Sum Withdrawal (SLW).

Instead of withdrawing your 60% lump sum all at once, you now have the option to withdraw it gradually:

- Monthly

- Quarterly

- Half-yearly

- Annually

Here is the official circular.

For retirees who don’t want a massive idle bank balance or who simply prefer controlled cash flow—this can be a very practical feature.

Sometimes retirement isn’t about having all the money at once.

Sometimes it’s about making sure the money behaves.

Partial Withdrawals Before Age 60

Life happens long before retirement.

That’s why NPS allows limited partial withdrawals after 3 years of PRAN activation.

You may withdraw up to 25% of your own contributions (not employer contributions, not returns) for specific purposes such as:

- Higher education of children

- Marriage of children

- Purchase or construction of your first home

- Treatment of critical illness

- Skill development or self-improvement programs

A maximum of 3 partial withdrawals is permitted during your NPS tenure.

Here is the official master circular.

It’s flexible, but clearly designed to prevent casual dipping into retirement savings.

Which, honestly, is probably wise.

What If You Exit Before 60?

This is where NPS becomes stricter.

If you decide to exit before age 60, and you’ve been an NPS subscriber for more than 10 years, the rules become tougher:

- At least 80% of your corpus must be used to buy an annuity

- Only 20% can be withdrawn as a lump sum

If your corpus is below ₹2.5 lakh, full withdrawal may be permitted without the annuity requirement.

Here is the detailed withdrawal guide

That heavier annuity requirement exists for a reason, it discourages investors from treating NPS like a short-term savings account.

Because it isn’t.

And it was never meant to be.

Choosing an Annuity Provider

When it’s time to convert part of your corpus into pension income, you’ll need to purchase an annuity from a PFRDA-approved provider, such as:

- Life Insurance Corporation of India (LIC)

- SBI Life Insurance

- HDFC Life Insurance

Operational instructions for ASPs are available here.

You’ll usually choose between options like:

- Lifetime annuity

- Joint life annuity

- Annuity with return of purchase price

- Increasing annuity options

And here’s the trade-off most retirees eventually face:

If you want your nominees to receive the corpus later, your monthly pension usually comes down.

If you want the highest monthly pension today, the death benefits often reduce.

There’s no universally “best” option here.

Just trade-offs. Real ones.

And one more thing many investors miss: annuity income is fully taxable according to your income tax slab.

That makes it the one clearly taxable leg inside an otherwise tax-efficient NPS structure.

For retirees managing life certificates digitally, the Jeevan Pramaan platform remains a useful tool:

No branch visits. No paper chasing. Just digital verification.

A small improvement, but for pensioners, sometimes small improvements matter a lot.

Frequently Asked Questions: PPF vs. EPF vs. NPS in 2026

There is no single “best” fund; a balanced strategy is ideal. PPF offers guaranteed, tax-free 7.1% returns. EPF is the default for salaried wealth with historical yields of ~8.25%. NPS is the growth engine, offering market-linked equity upside and exclusive tax deductions.

Under Section 80CCD(1B), you can claim an additional tax deduction of ₹50,000 for NPS Tier 1 contributions. This is over and above the ₹1.5 lakh limit available under Section 80C, making it a critical tool for high-tax-bracket earners.

With the rollout of EPFO 3.0, eligible members can now initiate instant, UPI-linked withdrawals for specified amounts. For full withdrawals, you must still use the Unified Portal or UMANG app, provided your UAN is Aadhaar-linked and KYC-compliant.

After the initial 15-year maturity, you can extend your PPF account in blocks of 5 years indefinitely. You have two options: extension with fresh contributions (retaining tax benefits) or extension without further deposits (where the balance continues to earn tax-free interest).

As of 2026, you can withdraw up to 60% of your NPS corpus tax-free as a lump sum upon reaching age 60. The remaining 40% must be used to purchase an annuity, which provides a regular pension taxable as per your income slab.

While the UAN is the primary key, you can check your balance via the EPFO SMS service or missed call facility (9966044425) from your registered mobile number, or by using the UMANG app.

| Feature | Public Provident Fund (PPF) | Employees’ Provident Fund (EPF) | National Pension System (NPS) |

| Primary USP | Sovereign Safety + 100% Tax-Free | Automated Workplace Wealth | Market-Linked Equity Upside |

| 2026 Returns | 7.1% (Guaranteed/Fixed) | ~8.25% (Historical Yield) | 8% – 12% (Market-Linked) |

| Tax Status | EEE (Exempt-Exempt-Exempt) | Exempt (Conditions apply) | EEE-ish (60% Lump sum tax-free) |

| Max Investment | ₹1.5 Lakh / Year | ₹2.5 Lakh (Tax-free interest cap) | No limit (₹50k extra 80CCD) |

| Lock-in Period | 15 Years | Until Retirement / Job Loss | Until Age 60 |

| Withdrawal Rule | Partial after 7th year | Housing/Medical (EPFO 3.0) | 25% of own contribution |

| Digital Access | SBI YONO / Net Banking | EPFO 3.0 / UMANG App | Protean eNPS / BBPS |

| Best For… | Conservative Investors | Salaried Employees | Aggressive Growth / High Tax Bracket |

| Risk Level | Negligible (Government) | Very Low | Low to Moderate |

Building a Bulletproof Retirement Strategy with PPF, EPF, and NPS in 2026

If there’s one mistake people make with retirement planning in India, it’s looking for the perfect product.

The perfect fund. The perfect tax hack. The perfect return.

Usually, that’s the wrong question.

Because in reality, retirement security is rarely built by one product doing everything. It’s usually built by multiple tools doing different jobs—quietly, consistently, over a long stretch of time.

And in India, that trio often comes down to PPF, EPF, and NPS.

Each one solves a different problem.

Public Provident Fund (PPF) gives you stability, sovereign safety, and one of the cleanest tax structures available under the EEE framework. It’s the kind of product that doesn’t make headlines—but 20 years later, you’re glad you kept funding it.

Employees’ Provident Fund (EPF), for salaried employees, often becomes the invisible engine of long-term wealth. Month after month, salary after salary, it compounds in the background. Not glamorous. Very effective.

And National Pension System (NPS) brings something the other two don’t: market-linked upside, deeper tax flexibility, and the potential to build a significantly larger retirement corpus over long horizons.

The smartest retirement plans usually don’t choose one.

They combine all three.

For Salaried Employees: The Power Trio

If you’re working in the formal sector, your retirement framework is already partially built.

Start with EPF.

Your employer’s contribution is one of the few forms of “free money” most professionals ever receive. Don’t underestimate it.

Then layer PPF on top as your low-risk, tax-free debt anchor. Funding your PPF early in the financial year, especially each April, can quietly improve long-term compounding more than most people realise.

Then use NPS Tier 1 strategically, especially to capture the additional Section 80CCD(1B) deduction of ₹50,000.

That extra tax deduction, year after year, adds up.

Not dramatically at first.

Then suddenly… very dramatically.

For Self-Employed Professionals and Freelancers

No employer means no EPF.

That doesn’t mean weaker retirement planning, it just means you have to build the system yourself.

For many self-employed individuals, PPF + NPS becomes the core combination.

PPF provides stability and tax-free accumulation.

NPS provides growth potential, tax deductions, and market participation that fixed-return products alone often can’t deliver over 25–30 years.

And honestly, if your income is irregular—as freelance income often is—automation matters even more than product selection.

Consistency beats intensity.

Almost every time.

For Higher-Income Earners

If you’re earning above ₹10 lakh annually, tax efficiency starts mattering in a different way.

The new tax regime has changed how many investors think about Section 80C.

But NPS still holds real relevance, especially through employer contributions under Section 80CCD(2), which remain deductible under both tax regimes.

For many high-income professionals, this quietly becomes one of the most efficient retirement tax strategies still available.

Not flashy.

Very effective.

The 2026 Snapshot

Here’s the simplest way to think about the three:

| Parameter | PPF | EPF | NPS (Tier 1) |

| Returns | 7.1% (guaranteed) | 8.25% (declared) | Market-linked |

| Risk | Very Low | Very Low | Low to Moderate |

| Tax Benefits | Section 80C | Section 80C | Section 80C + 80CCD(1B) |

| Liquidity | Low | Moderate | Low |

| Best For | Stability | Salaried wealth-building | Long-term growth |

Comparative frameworks and retirement analyses can be explored here:

And for ongoing regulatory updates, official circulars, and account management resources:

NPS Trust – https://npstrust.org.in/circulars

Employees’ Provident Fund Organisation – https://www.epfindia.gov.in

Platforms like PensionBox (https://pensionbox.in/) also offer consolidated retirement tracking tools.

In the end, retirement planning usually comes down to a few boring habits:

Start early.

Contribute regularly.

Review once a year.

Don’t panic when markets wobble.

Don’t stop when life gets busy.

That’s it.

No secret formula. No miracle product.

Just time, discipline, and a system that keeps working even when you’re not thinking about it.

Disclaimer

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Interest rates, tax rules, and regulatory conditions mentioned are as of May 2026 and are subject to change. Please consult a SEBI-registered investment advisor or a qualified chartered accountant before making investment decisions.

Discussion (4)

Leave a Reply