The 2026 Guide to PF Contribution Calculation Under New Labour Codes: A Complete Explainer

How the New Labour Code 2026 and 50% Wage Rule Impact Your Take-Home Salary

If you’re a salaried professional in India, 2026 PF calculation in the New Labour Code 2026 isn’t just an HR exercise—it’s going to directly impact your take-home pay.

The rollout of the four new Labour Codes is being talked about as a big reform (and it is), but most of the chatter stays oddly superficial. People mention longer working hours, maybe leave policies, and then move on. The real shift, though, the one that will actually nudge your finances every single month, sits inside something deceptively small: how “wages” are defined for Provident Fund deductions.

Right now, HR teams across the country are in a mild state of chaos—reworking salary structures, updating payroll systems, and double-checking compliance. Meanwhile, most employees haven’t quite caught on yet. There’s this assumption that if your CTC hasn’t changed, nothing really has. But that’s not how this plays out.

In many cases, your take-home salary is going to shrink a bit. Not dramatically, but enough to notice. That gap between what you expected to receive and what actually lands in your account, that’s what we might call the “PF Gap.” And closing that gap starts with understanding one rule that’s suddenly doing a lot of heavy lifting: the 50% Basic Pay Rule.

Here’s the core idea, stripped of jargon: the parts of your salary that don’t count as wages-things like HRA, conveyance, and those vague “special allowances”- can’t collectively be more than half of your total pay anymore. If they cross that 50% line, the extra portion gets pulled back into “wages” and becomes subject to PF deduction.

What this means in practice is pretty straightforward, even if companies try to dress it up differently: Basic Pay is no longer going to sit at that comfortable 25-35% range most people are used to. It’s often pushed up to at least 50% of your CTC.

And that one shift? It quietly changes everything. PF contributions go up, Take-home salary dips and long-term savings improve. A for short-term comfort maybe not so much.

This guide is here to unpack all of that without the usual HR fog. We’ll get into the legal logic behind the change, how the calculations actually work (not just in theory), a few real salary scenarios, and the ripple effects—gratuity, ESI, the works. There’s also a practical checklist at the end, because honestly, most people just want to know: what do I do now?

At a Glance: PF Calculation Under New Labour Code 2026

- The Core Shift: The New Labour Code 2026 introduces a mandatory 50% Basic Pay rule, fundamentally changing PF contribution calculations in India.

- How It Works: Under the new definition of wages, allowances cannot exceed 50% of your total salary. Any excess amount is automatically added to your wage base for EPF deductions.

- Employee Impact: Expect a slight drop in your monthly take-home salary, which is offset by a significant boost to your long-term retirement savings and future Gratuity payouts.

- Employer Action: HR professionals and business owners face higher provident fund liabilities and must urgently audit existing CTC structures to maintain payroll compliance.

Decoding the Legal Framework

The Four Labour Codes

For years-decades, really-India’s labour laws were a bit of a patchwork quilt. Twenty-nine different central laws, layered over time, each solving a specific problem but collectively becoming messy, hard to navigate, and harder to enforce.

So, the government decided to do something fairly ambitious: compress all of that into four broad codes. What we now have are the Code on Wages 2019, the Industrial Relations Code 2020, the Occupational Safety, Health and Working Conditions Code 2020, and the Code on Social Security 2020. On paper, it sounds clean. Almost elegant. One unified framework instead of a legal maze

But here’s the thing, most employees won’t feel all four of these equally. Some parts matter more if you’re in manufacturing, others if you’re in gig work, and some you’ll never directly notice.

For PF calculations, though, two of these codes quietly do most of the heavy lifting: the Code on Wages 2019 and the Code on Social Security 2020. The first one redraws the definition of “wages” which sounds technical but ends up affecting your salary structure. The second one takes that definition and applies it to things like EPF, ESI, and gratuity.

So, if you’re wondering why your PF numbers are changing, it’s not random. It’s these two codes working together behind the scenes.

Why the Government Redefined “Wages”

This part, honestly, has been coming for a while.

Over the years, companies got creative with salary structures. Not illegally, but strategically. Basic Pay was often kept low, somewhere around 25-35% of CTC, and the rest was padded with allowances: HRA, special allowance, conveyance, you name it.

It made sense from an employer’s perspective. Lower Basic Pay meant lower PF contributions, less statutory burden, and cleaner books.

But there was a catch. A big one, actually.

When employees retired, their EPF corpus, the thing that’s supposed to support them when their regular income stops ended up being much smaller than their overall earnings would suggest. You could spend decades earning a decent salary and still end up with a surprisingly modest retirement fund.

That gap? That’s what the government is trying to fix.

By tightening the definition of “wages” and imposing a 50% ceiling on exclusions, the system is essentially forcing salaries to be structured more realistically. Less hiding income in allowances, more of it flowing into the social security net.

Of course, this isn’t a painless fix. Employers pay more. Employees see lower take-home in the short term. Nobody loves that.

But zoom out a little, and you can see the intent: push more money into long-term savings, even if it stings a bit today.

The Definition of “Wages” Under 2026 Rules

Now, this is where things get a little technical, but it’s worth slowing down here, because this definition drives everything else.

Under the Code on Social Security 2020, “wages” is defined pretty broadly. It includes all forms of remuneration—salary, allowances, anything that can be expressed in money. But then it narrows things down with specifics.

At the core, three components are clearly inside the definition:

- Basic Pay

- Dearness Allowance (DA)

- Retaining Allowance (if applicable)

These form the foundation of your PF calculation.

Then there’s the exclusion list—the usual suspects:

- HRA

- Overtime

- Commission

- Conveyance allowance

- Other allowances that aren’t universally paid

These can be excluded, but only up to a point.

And that’s where the 50% rule quietly steps in and changes the game. If all these exclusions together cross half of your total salary, the excess doesn’t stay excluded anymore. It gets pulled back into “wages” whether you like it or not.

It’s a bit like trying to pack too much into a carry-on bag at the airport. You can try to squeeze things in, but once you cross the limit, something has to come out and in this case, it comes back into your PF calculation.

The 50% Basic Pay Rule Explained

The Core Concept

Most people hear “50% Basic Pay rule” and assume it’s a direct instruction: your Basic must be 50% of your salary. That’s not exactly what’s happening. It’s a bit more indirect, almost sneaky, in how it works.

The rule doesn’t go after Basic Pay itself. Instead, it looks at everything you’re trying to exclude from wages.

Here’s the test: take all those excluded components-HRA, conveyance, certain allowances-and add them up. If that total cross 50% of your monthly salary, the excess portion loses its “excluded” status. It gets dragged back into wages and becomes part of the PF calculation base.

So even if a company tries to keep Basic Pay low on paper, the rule kind of corrects it in the background. It says, “Fine, structure it however you want, but if exclusions go too far, we’ll just reclassify the surplus.”

In practice, this creates a floor. Your PF-eligible salary can’t really drop below 50% of your total pay anymore.

And for a lot of companies, especially the big ones where Basic Pay used to hover around 30–40%, this is where things start to shift uncomfortably. Not dramatically overnight, but enough that payroll teams have to rethink the entire structure.

Impact on Salary Structure

Now, how are companies actually dealing with this?

From what’s happening on the ground, there are basically two approaches, and neither is perfect.

The first is straightforward restructuring. Employers take a chunk of those “flexible” allowances, usually a special allowance, and convert them into Basic Pay. Same CTC but different composition. On paper, nothing changes. But behind the scenes, your PF contribution increases because the wage base is higher.

Which means your take-home dips a little.

The second approach is more of a financial adjustment. Instead of letting PF contributions eat into your take-home, companies increase the overall CTC to absorb the higher employer contribution. So, your in-hand salary feels similar, but the total cost to the company goes up.

Neither route is universally better—it depends on the company, margins, hiring strategy, all of that. But either way, the days of heavily allowance-loaded salary structures are clearly numbered.

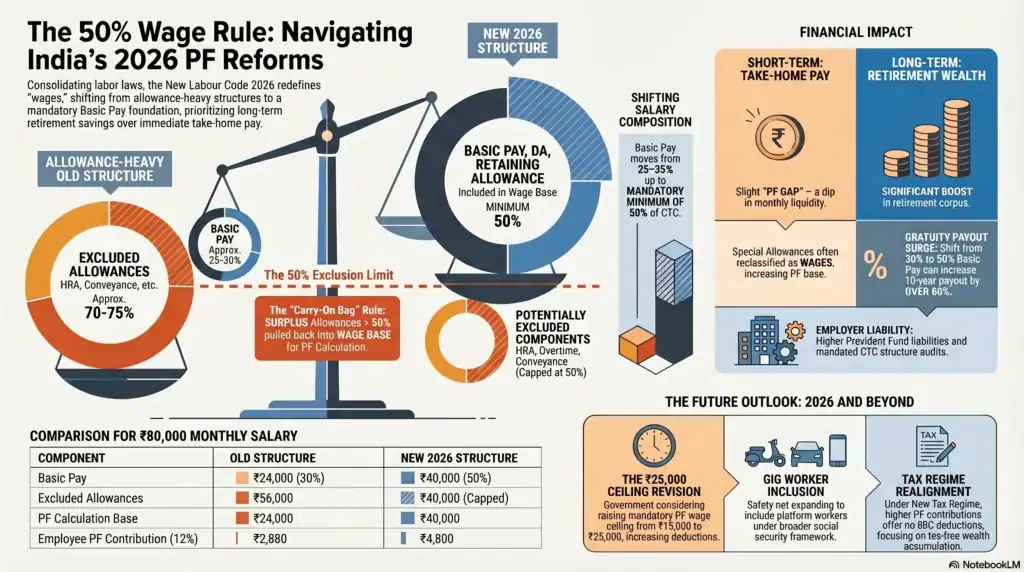

Scenario Comparison: Old vs New Structure

Let’s make this less abstract.

Say someone earns ₹80,000 a month. Under the old structure, it might look something like this:

- Basic Pay: ₹24,000 (30%)

- HRA: ₹12,000

- Special Allowance: ₹32,000

- Conveyance: ₹3,200

- Other Allowances: ₹8,800

PF is calculated on the Basic—₹24,000. So, the employee contributes ₹2,880 monthly, and the employer matches it.

Simple enough.

Now under the 2026 rules, things get a bit layered.

First, you test the excluded components:

HRA (₹12,000) + Conveyance (₹3,200) + Other (₹8,800) = ₹24,000

50% of total salary (₹80,000) is ₹40,000. Since ₹24,000 is below that, no issue there.

But here’s where it gets interesting—Special Allowance.

In many cases, Special Allowance isn’t truly “special.” It’s paid to almost everyone. Which means it may be treated as part of wages rather than an exclusion.

If that happens, suddenly your exclusions jump to ₹56,000. That crosses the ₹40,000 threshold by ₹16,000.

And that excess? It doesn’t stay excluded. It comes back into wages.

So now your PF base becomes:

₹24,000 (Basic) + ₹16,000 (excess) = ₹40,000

That’s a pretty big jump, from ₹24k to ₹40k, without your CTC changing at all.

And this is exactly the kind of silent shift people don’t notice until their salary credit looks lighter.

Salary Scenarios: PF Calculation for ₹20,000 and ₹21,000 CTC

The easiest way to understand how the 50% basic pay rule affects your salary is to look at actual examples. The impact is often more noticeable for employees in entry-level and lower-mid salary brackets, where salary structures have traditionally relied more heavily on allowances.

Scenario A: ₹20,000 CTC

- Total Salary: ₹20,000

- Minimum Mandatory Basic Pay (50%): ₹10,000

- Maximum Permissible Allowances: ₹10,000

- PF Deduction (12% of Basic): ₹1,200 (Employee) + ₹1,200 (Employer)

Net Impact: If your basic pay was previously fixed at ₹6,000, your monthly PF contribution would have been ₹720. Under the revised wage structure, the contribution increases to ₹1,200. That means an additional ₹480 is set aside every month for your Provident Fund. While this reduces your immediate take-home salary, it also helps build a larger retirement corpus over time.

Scenario B: ₹21,000 CTC

- Total Salary: ₹21,000

- Minimum Mandatory Basic Pay (50%): ₹10,500

- Maximum Permissible Allowances: ₹10,500

- PF Deduction (12% of Basic): ₹1,260 (Employee) + ₹1,260 (Employer)

Net Impact: As your salary increases, your mandatory PF contribution also rises because it is linked to the revised basic pay. This ensures that retirement savings grow in proportion to your earnings instead of remaining tied to a salary structure where a large portion of compensation is classified as allowances.

Impact on Employers

From the employer’s side, this isn’t just a minor tweak; it adds up quickly.

If your PF base moves from, say, 30% of CTC to 50%, the employer’s contribution rises proportionally. And when you scale that across hundreds or thousands of employees, it becomes a serious cost line.

Not catastrophic, but definitely not trivial either.

This is why consulting firms like KPMG and Deloitte have been flagging it as a real planning concern—not just compliance, but budgeting, forecasting, and even hiring strategy.

You can already see some companies being cautious—slowing hiring, tweaking compensation offers, quietly recalibrating.

Long-Term Impact: Why Pension Payouts Are Likely to Increase

Much of the discussion around the Code on Social Security has focused on the possibility of lower take-home pay. However, the long-term picture is different. With a larger portion of your salary being treated as basic wages, your retirement savings and pension contributions are also likely to grow.

The employer’s 12% PF contribution is divided into two parts. Of this, 3.67% is credited to the Employees’ Provident Fund (EPF), while 8.33% goes to the Employees’ Pension Scheme (EPS). When the basic wage increases under the 50% wage rule, the amount calculated for these contributions also rises.

Over the course of a long career, this can make a meaningful difference. Higher contributions to the EPF and EPS have the potential to build a larger retirement corpus and improve future pension benefits. The broader intent of the revised wage definition is to align retirement savings more closely with an employee’s actual earnings, rather than allowing a significant portion of compensation to be shifted into allowances that reduce long-term benefits.

The Math: PF calculation in New Labour Code 2026

The Current Formula

Before all these changes, PF calculation was almost comforting in its simplicity.

You took Basic Pay + DA, applied 12%, and that was your contribution; the same amount from your employer.

There was one important cap, though—the ₹15,000 wage ceiling. Even if your Basic Pay was ₹40,000 or ₹60,000, the mandatory PF contribution was still calculated only on ₹15,000. So, both employee and employer would contribute ₹1,800 each per month, unless you voluntarily opt to contribute on the higher amount.

For a lot of people, especially mid- and high-income earners, this meant PF quietly became a capped, predictable deduction. Almost ignorable.

The New Formula

No, it’s not so ignorable.

Under the 2026 rules, PF is calculated as 12% of what’s now called “Redefined Wages.” Which sounds like jargon, but the idea is actually pretty simple once you strip it down.

Your PF base is now the higher of:

- Your actual Basic Pay + DA

- Or the adjusted wage figure after applying the 50% exclusion rule

So even if a salary is structured to keep Basic low, the rule steps in and says, “No, your PF should be based on something closer to half your salary.”

In other words, the system has stopped taking your salary structure at face value. It double-checks it. Quietly, but firmly. https://easyhr.app/blog/pf-calculation-formula-2026

Official EPFO Guidelines on 12% Basic Wages Contribution

Understanding the New Labour Codes can feel complicated, but one rule has stayed consistent. As per the Employees’ Provident Fund Organisation (EPFO), employees are required to contribute 12% of their basic wages towards the Provident Fund.

In the past, many employers kept PF contributions lower by allocating a larger share of an employee’s salary to allowances instead of basic pay. The Code on Social Security, 2020, addresses this practice by tightening the definition of “wages.” If excluded allowances, including HRA, conveyance, and special allowances, make up more than 50% of your total remuneration, the amount above that limit is treated as basic wages for PF purposes. As a result, the mandatory 12% contribution is calculated on this revised wage base. The objective is to ensure that retirement savings are based on a more realistic salary structure and to discourage artificially low basic pay.

Would you like me to proceed with the next section, “Salary Scenarios: PF Calculation for ₹20,000 and ₹21,000 CTC”?

Step-by-Step Calculation Guide

If you ever sit down with your salary slip and try to make sense of it (which, let’s be honest, most people avoid), this is the sequence you’d follow:

Step 1: Break down your salary

List every component—Basic, DA, HRA, allowances, everything. Then split them into two buckets:

- Included (Basic, DA, retaining allowance)

- Potentially excluded (HRA, conveyance, etc.)

This step alone can be trickier than it sounds. Some allowances look excludable but aren’t always treated that way.

Step 2: Apply the 50% test

Add up all the excluded components. Now compare that to 50% of your total salary.

If the exclusions cross that line, the excess portion doesn’t stay excluded; it gets pulled back into wages.

This is the step where most “unexpected” increases in PF happen.

Step 3: Find your effective wage base

Take your included components and add any excess from the previous step.

That total becomes your actual PF calculation base. Think of it as your “deemed Basic,” even if your official Basic Pay says something else.

Step 4: Apply the 12% rate

Now apply 12% to that number—for both employee and employer.

The employer’s contribution gets split:

- 3.67% to EPF

- 8.33% to EPS (pension), subject to the wage ceiling

This part hasn’t changed, but because the base is higher, the actual rupee amount increases.

The ₹1,800 PF Ceiling Limit Explained

One area that often creates confusion is the ₹1,800 monthly PF contribution limit.

Under the current EPF framework, mandatory PF contributions are calculated on a wage ceiling of ₹15,000 per month. Since both the employee and employer contribute 12% of this amount, the maximum mandatory contribution works out to ₹1,800 each per month.

It is important to understand that the 50% wage rule does not automatically remove this ceiling. Even if your revised basic wage, after applying the new wage definition, exceeds ₹15,000, the mandatory PF contribution can still be capped at ₹1,800 for both the employee and the employer. A higher contribution is possible only if both parties voluntarily agree to contribute on the actual basic salary instead of the statutory wage ceiling.

This distinction matters because it helps prevent a sudden increase in mandatory deductions for many employees while continuing to ensure compliance with EPF regulations.

Statutory Ceilings and the ₹25,000 Revision

Now here’s where things get a bit unsettled.

The current wage ceiling for mandatory PF is ₹15,000. It’s been that way since 2014, which, if you think about inflation alone, feels a bit outdated.

There’s been an ongoing discussion about raising it to ₹25,000. And in early 2026, multiple reports suggest this isn’t just talk anymore, it’s actively being considered.

If that happens, the impact compounds.

Right now, many employees already have a higher PF base due to the 50% rule, but their mandatory contribution is still capped at ₹1,800. If the ceiling moves to ₹25,000, that cap rises to ₹3,000.

So suddenly, two changes collide:

- Higher wage base

- Higher ceiling

And the result is a noticeably larger deduction and contribution each month.

Voluntary Provident Fund (VPF)

This part is easy to overlook, but it’s quietly powerful.

VPF lets you contribute more than the mandatory 12%. Same account, same interest rate. Just a higher contribution from your side.

Now here’s the interesting bit: because your wage base itself is increasing under the new rules, even a fixed VPF percentage leads to a larger absolute contribution.

So, if you were contributing, say, 5% extra on a ₹20,000 base earlier, you might now be contributing 5% on ₹30,000 or ₹40,000 without changing anything manually.

It’s one of those rare cases where a structural change kind of nudges you into saving more whether you planned to or not.

Real-World Scenarios and Calculations

Scenario A: The Entry-Level Employee (Rs 30,000 Monthly CTC)

Let’s start at the beginning—someone just out of college, first or second job, earning ₹30,000 a month.

Under the old structure, things might have looked like this:

- Basic: ₹9,000

- HRA: ₹4,500

- Special Allowance: ₹12,000

- Conveyance: ₹1,600

- Other: ₹2,900

Now, if you apply the 50% test, the clearly excluded components (HRA + conveyance + other) add up to ₹9,000. Half the salary is ₹15,000, so no issue there.

But again, it’s that Special Allowance that complicates things.

If it’s treated as part of wages (which, in many companies, it will be), your PF base doesn’t stay at ₹9,000. It jumps to ₹21,000.

So your monthly PF contribution becomes ₹2,520 instead of ₹1,080.

That’s a difference of ₹1,440 every month.

Now, if you’re early in your career, ₹1,440 is not nothing. That’s a couple of dinners out. A subscription or two. Maybe your fuel budget.

But—and this is where it gets slightly philosophical—that same ₹1,440, compounded over 25–30 years at EPF rates, turns into something… surprisingly large. Not life-changing overnight, but quietly substantial over time.

It’s one of those trade-offs that feels annoying now and sensible later.

Scenario B: The Mid-Level Professional (Rs 80,000 Monthly CTC)

Now let’s move to someone a bit further along—₹80,000 monthly income. This is where things get a little more nuanced.

Old structure:

- Basic: ₹24,000

- PF calculated on ₹15,000 (due to ceiling)

- Monthly PF: ₹1,800

Under the new rules, if Special Allowance is treated as wages, your PF base effectively becomes ₹40,000 (half the CTC).

But, and this is important, the ceiling still matters.

If the wage ceiling stays at ₹15,000, your mandatory PF contribution doesn’t change. It remains ₹1,800.

So, in that case, despite all the restructuring, your take-home doesn’t really shift much from a PF standpoint.

But if (or when) the ceiling moves to ₹25,000, things change.

Now your contribution becomes ₹3,000.

Not massive, but noticeable. Enough to feel like your salary got “adjusted” without actually increasing.

And here’s the subtle part: a lot depends on how your company classifies allowances. Two people with the same CTC could see slightly different outcomes depending on that one decision.

Scenario C: High Earners (Rs 2,00,000 and Above Monthly)

At higher salary levels, the story shifts a bit.

Because of the wage ceiling, mandatory PF contributions are still capped. So even if your wage base increases, your required contribution doesn’t necessarily follow.

Which means the immediate impact on take-home salary is limited.

But the conversation moves somewhere else—tax planning.

Under the old tax regime, higher PF contributions helped reduce taxable income through Section 80C. That was a nice little cushion.

Under the newer tax regime, that cushion mostly disappears. There are no 80C deductions.

So now, PF becomes less about tax-saving and more about long-term wealth building. The main benefit is the tax-free interest (up to the allowed limits) and the eventual lump sum at retirement.

It’s less immediately rewarding, more quietly strategic.

Scenario D: The Gig Worker and Contract Employee

This one’s a bit of a shift, not just in numbers, but in who even gets included.

Earlier, if you were a gig worker or on a contract payroll, EPF wasn’t really part of your world. You earned, you saved (or didn’t), and that was that.

The Code on Social Security 2020 changes that equation.

Now, gig workers, platform workers-people driving cabs, delivering food, working through aggregators-are being brought into a broader social security framework.

Instead of traditional PF contributions, platforms themselves are expected to contribute to a social security fund on behalf of these workers.

Details are still evolving, and honestly, this part feels less settled than the salaried PF rules. But the direction is clear: the safety net is expanding.

Which, depending on how you look at it, is either overdue or complicated

Impact on Gratuity and Other Benefits

The Connection Between PF Wages and Gratuity

Gratuity is one of those things most people don’t think about until they’ve been in a company for years. It sits in the background—quiet, predictable, slightly abstract.

But it’s directly tied to Basic Pay. And that’s where this whole shift starts to matter.

The formula itself hasn’t changed, but the input has. If your Basic Pay increases because of the 50% rule (which, for many people, it will), then your gratuity calculation automatically rises along with it.

Let’s make that tangible.

Earlier, if someone had a Basic Pay of ₹24,000 and completed 10 years of service, their gratuity would land somewhere around ₹1.38 lakh.

Now, if that same person’s Basic Pay gets restructured to ₹40,000—same role, same tenure—the gratuity jumps to about ₹2.3 lakh.

That’s not a marginal increase butit’s noticeable.

From an employee’s perspective, it’s a quiet win. From an employer’s side, though, it adds up fast, especially across a large workforce. That’s why firms like KPMG have been pointing out that gratuity provisioning is going to be one of the biggest cost pressures alongside PF contributions.

It’s one of those rare situations where both sides feel the change, just in different ways.

Gratuity Calculation 2026: Formula Applied

The formula itself stays exactly the same. No tweaks and no redesign.

It’s still:

Gratuity = (Last drawn Basic Pay + DA) × 15/26 × Years of service

What changes is what “last drawn Basic Pay” looks like.

And that’s the key detail.

If you’ve worked across both regimes, before and after this restructuring, your final gratuity payout will reflect that higher Basic Pay at the end of your tenure. Not an average, not a blended number, and just the last drawn amount.

So even if the shift happens midway through your career, the benefit compounds toward the end.

It’s one of those things people don’t notice until exit time, and then suddenly it matters a lot.

Employee State Insurance (ESI)

ESI is a slightly different story. A bit more fluid, less predictable.

Right now, ESI applies to employees earning up to ₹21,000 per month (₹25,000 for employees with disabilities). But with the redefinition of wages, that boundary can get a little blurry.

Some employees who were previously outside the ESI bracket because their gross salary was structured a certain way might find themselves pulled into it. Others might move out, depending on how their wage components are recalibrated.

It’s not as straightforward as PF, where the direction is clearly “upward contribution.”

Here, it depends.

And there’s another layer: if the government revises the ESI threshold to align with the new wage definitions (which isn’t off the table), eligibility could shift again.

So, this is one area where HR departments are likely to keep a closer eye and where employees might want to double-check their status rather than assume it hasn’t changed.

Frequently Asked Questions: PF Contribution Calculation Under New Labour Codes

For many employees, take-home salary will decrease, but long-term savings will increase.

Under the Code on Wages, basic pay must constitute at least 50% of your total remuneration. Previously, many companies kept basic pay around 20–30% of the CTC, padding the rest with allowances to increase your monthly cash in hand and reduce their Provident Fund (PF) and Gratuity liabilities.

With the new mandated 50% basic threshold, a larger portion of your salary is subject to the 12% EPF deduction. While your gross CTC remains unchanged, more money is routed directly into your retirement cushion. It is a trade-off: less immediate liquidity for significantly compounded, tax-efficient savings over the span of your career.

Yes, the 50% rule is mandatory for all companies with 20 or more employees falling under EPF applicability. It is not an optional best practice; it is a statutory requirement baked into the Code on Wages.

The rule explicitly states that allowances (like HRA, conveyance, and special allowances) cannot exceed 50% of total gross compensation. If they do, the excess amount is automatically treated as “wages” for the purpose of calculating PF and Gratuity. While interpretations of highly specific allowances may vary slightly until court precedents are established, the core requirement to restructure allowance-heavy CTCs is non-negotiable.

This requires looking at both employee and employer contributions.

Under the New Tax Regime, your personal 12% PF contribution no longer qualifies for the Section 80C deduction. Therefore, a higher mandated PF contribution will not lower your immediate taxable income.

However, the employer’s matching contribution to your EPF remains completely tax-exempt (up to a combined annual limit of ₹7.5 Lakhs across EPF, NPS, and Superannuation). Furthermore, you retain long-term tax efficiency: interest earned on EPF is tax-free (on annual employee contributions up to ₹2.5 Lakhs), and the final maturity amount remains tax-exempt. The benefit has shifted from an immediate yearly deduction to a protected, long-term wealth accumulation strategy.

Opting out of the EPF is highly restrictive and operates as a one-time, entry-level decision. You can only legally opt out if your basic salary at the time of joining your first job exceeds the statutory wage ceiling (currently ₹15,000 per month), and you and your employer mutually agree to it via Form 11.

If your starting basic pay is below ₹15,000, enrollment is mandatory. More importantly, if you have ever contributed to the EPF and a Universal Account Number (UAN) has been generated, you are permanently in the system. You cannot step out of the EPF in subsequent jobs, even if your salary later exceeds the ₹15,000 ceiling.

Checklist for Employees and HR Professionals

For Employees

- Take a proper look at your revised salary slip

Not just the net pay—actually scan the breakdown. Basic Pay, PF deduction, allowances. This is where the change shows up first, even if no one explicitly explains it to you. - Log into your EPF account and verify contributions

It takes a few minutes, but it’s worth doing. The EPFO Unified Member Portal shows your monthly credits. If something looks off, it’s easier to flag it early than untangle it later. - Check your Form 16 when it’s issued

Most people glance at it and move on. This year, maybe don’t. Make sure the PF deductions are reflected correctly—it ties into your overall tax picture more than you might expect. - Revisit your VPF contribution (if you have one)

If you’ve set VPF as a percentage, your actual contribution amount has probably increased already without you noticing. It might be fine—or it might be more than you’re comfortable with. Worth recalculating. - Double-check your ESI eligibility

If your salary was hovering around the ₹21,000 mark earlier, the new wage definition might shift you in or out of eligibility. It’s one of those quiet changes that doesn’t always get communicated clearly. - Talk to a CA if you’re serious about tax planning

Especially now that PF contributions are higher and the New Tax Regime changes the deduction landscape. The “old vs new regime” decision isn’t as obvious as it used to be.

For HR and Employers

- Run a full payroll audit

Identify where excluded allowances exceed that 50% threshold. This is ground zero for compliance issues. - Update payroll systems (properly, not halfway)

Most HRMS platforms—greytHR, Zoho Payroll—have already rolled out updates. But implementation matters. A misclassification here can snowball across hundreds of employees. - Revise offer letters and CTC structures

New hires shouldn’t be onboarded on outdated salary structures. It sounds obvious, but this is where a lot of companies slip—especially during transition phases. - Recalculate gratuity liabilities

Higher Basic Pay = higher future payouts. This needs to reflect in financial planning now, not years later when employees start exiting. - Reassess ESI applicability

Borderline cases need a second look. The redefinition of wages can push employees across eligibility thresholds in either direction. - Train payroll and HR teams on allowance classification

This is the subtle but critical part. Whether something is “universally paid” or not isn’t just semantics—it directly affects PF calculations. - Keep tracking EPFO updates

Especially regarding the wage ceiling revision. If it moves to ₹25,000, systems and contributions need to adjust quickly. The official EPFO site is still the source of truth here.

Balancing Take-Home Salary and Retirement Under the 50% Wage Rule

The rollout of the new Labour Codes, and especially this 50% wage rule, is going to feel disruptive at first. There’s no way around that.

Payroll teams will be busy untangling structures, updating systems, and reissuing offer letters. Employees will notice their take-home dip and wonder what just happened. And yes, for employers, the cost implications are very real.

But if you zoom out a little, past the immediate friction, there’s a bigger shift happening here.

For a long time, India’s retirement savings story hasn’t exactly been strong. EPF was meant to be the backbone for salaried workers, but over the years, salary structures kind of worked around it. Too much sitting in allowances, not enough flowing into long-term savings. The result? Smaller retirement corpuses than people probably expected.

This change is, in many ways, a correction.

If someone earning ₹80,000 a month now contributes PF on ₹40,000 instead of ₹24,000, that difference doesn’t feel great today. But over 20-30 years, with compounding at play, it becomes significant. Not abstractly significant but actually meaningful when you’re no longer earning a monthly salary.

So, for employees, the instinct to focus only on reduced take-home is understandable, but a bit incomplete. It helps to run the longer-term numbers. For anyone early or mid-career, the math tends to tilt in your favour, even if it doesn’t feel that way right now.

For employers, this isn’t just a compliance exercise to get through and forget. It’s an opportunity, maybe an inconvenient one, to rethink compensation structures altogether. Cleaner, more transparent, aligned with regulations, but still competitive enough to attract talent.

And somewhere in between all this, between regulation and reality, is where most people will land: adjusting, recalibrating, figuring out what this actually means for their own situation. If you want to go a step further and see how this plays out with your own numbers, using a calculator or even a simple Excel sheet will be useful. Plug in your current CTC, apply the 50% rule, and see what shifts. It makes the whole thing less abstract

Disclaimer

The content on this page is intended for informational and educational purposes only and should not be construed as professional financial, tax, or legal advice. India Policy Hub and its authors are not certified financial planners, registered investment advisors, or practicing Chartered Accountants (CAs). Tax laws, particularly regarding international assets and compliance, are complex and subject to change. Always consult a qualified professional or Chartered Accountant regarding your specific financial situation, tax liabilities, or legal compliance before making any financial decisions or submitting tax declarations.

You actually make it seem so easy with your presentation but I find this topic to be actually

something that I think I would never understand.

It seems too complicated and extremely broad for me.

I am looking forward for your next post, I will try

to get the hang of it!

Hello there, I found your web site by means of Google while looking for a

similar matter, your web site got here up, it appears good.

I’ve bookmarked it in my google bookmarks.

Hello there, just was aware of your blog thru Google, and found that it’s truly informative.

I am going to be careful for brussels. I’ll be grateful for those who continue this in future.

Numerous people shall be benefited from your writing.

Cheers!

Good way of telling, and fastidious piece of writing to take information regarding my presentation topic, which i am going to convey in school.