RBI Sovereign Gold Bonds 2026: New Tax Rules & May Redemption Guide

The 2026 SGB Landscape: Navigating Record Gains and New Tax Realities

If you are holding Sovereign Gold Bonds (SGBs) in 2026, you’re probably sitting on sizeable gains. But you’re also dealing with a tax framework that looks very different from what investors got used to over the past several years. Herein comes the RBI Sovereign Gold Bonds 2026.

For a long stretch, SGBs had a kind of almost unfair advantage in the Indian investment landscape. You got exposure to gold without worrying about storage, purity, or making charges. The government paid you 2.5% annual interest on top of that. And then there was the big attraction: capital gains from redemption were effectively tax-free. That combination made SGBs feel unusually efficient, especially compared to physical gold or Gold ETFs.

That simplicity is gone now.

Budget 2026 has changed the rules in ways that are surprisingly consequential. The tax outcome now depends heavily on how you purchased the bond, whether you were an original subscriber or a secondary-market buyer, how long you’ve held it, and even the route you choose to exit. Two investors holding the same SGB tranche can now face completely different tax liabilities. That’s the part many people are only beginning to realise.

At the same time, gold prices are hovering near record territory, and the RBI’s premature redemption calendar for 2026 is packed. Between April and September alone, dozens of redemption windows are opening up. For many investors, this is the first real decision point since they bought these bonds years ago: hold, redeem, or sell on the exchange?

This guide breaks all of that down in plain English. We’ll look at the new tax rules, who is affected, how redemption prices are calculated, the May 2026 redemption schedule, the mechanics of online and offline exits, and the practical trade-offs between maturity redemption, premature redemption, and secondary-market sales.

Because in 2026, owning SGBs is no longer just about owning gold. It’s about navigating the fine print properly.

At A Glance: RBI Sovereign Gold Bonds 2026

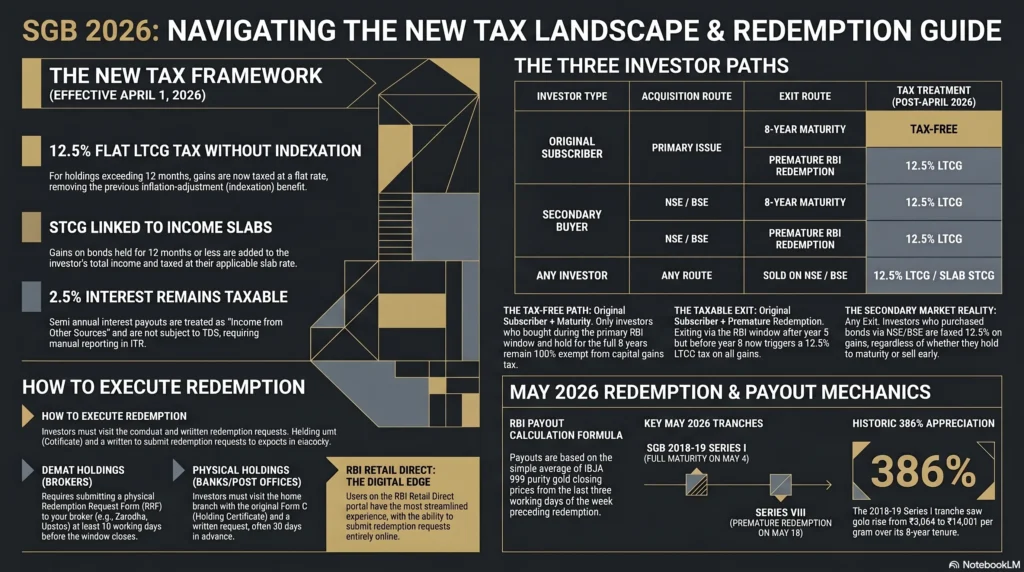

- The 2026 Tax Shift: The tax-free maturity benefit is now restricted strictly to original subscribers who hold their Sovereign Gold Bonds for the full 8-year tenure.

- 12.5% LTCG Tax Applied: If you purchase an SGB on the secondary market (NSE/BSE) or execute a premature RBI redemption, your capital gains are now taxed at a flat 12.5% without indexation.

- Interest Remains Taxable: The 2.5% annual interest payout remains unchanged. It is taxed according to your applicable income tax slab as “Income from Other Sources.”

- May 2026 Redemption Windows: The RBI has opened early exit windows for eligible tranches crossing the 5-year mark (e.g., Series II and Series VIII). Payout prices are based on the 3-day average IBJA gold rate.

- Execution Deadlines: Premature redemption is not instant. You must submit a formal request through your demat broker (Zerodha, Upstox) or bank (SBI, HDFC) typically 10 to 30 days prior to the exact coupon date.

Understanding the New SGB Tax Rules for 2026

The Budget 2026 Impact on SGB Taxation

The single biggest shift for SGB investors in 2026 comes from the amendment to Section 70(1)(x) of the Income Tax Act, 2025, the new tax framework replacing the older 1961 regime. And unlike some budget announcements that sound dramatic but barely affect retail investors, this one genuinely changes the economics of Sovereign Gold Bonds.

As explained by NISM, Budget 2026 has fundamentally narrowed the tax exemption that made SGBs so attractive in the first place.

Earlier, the rule was relatively straightforward: if you redeemed an SGB through the RBI, the capital gains were exempt from tax. It didn’t really matter whether you were the original buyer or someone who purchased the bond later from the secondary market. The exemption was broad enough that investors largely treated SGBs as the most tax-efficient way to own gold in India.

That’s no longer true from April 1, 2026 onward.

The exemption now survives only under two very specific conditions:

- You must have subscribed to the SGB during the original RBI issuance window, meaning directly through authorised channels like banks, post offices, stock exchanges during primary subscription, or RBI Retail Direct.

- You must continue holding the bond until the completion of its full 8-year tenure and redeem it with the RBI at maturity.

Miss either of those conditions, and the gains become taxable.

That distinction matters a lot more than it sounds. Someone who bought the exact same SGB tranche on NSE a few years later no longer gets the same treatment. Likewise, even an original subscriber loses the exemption if they opt for premature redemption before maturity.

According to ClearTax, the revised tax structure now works like this:

- Long-Term Capital Gains (LTCG): 12.5% flat tax without indexation for holdings exceeding 12 months

- Short-Term Capital Gains (STCG): Taxed according to the investor’s income slab for holdings of 12 months or less

There’s another point investors sometimes overlook because the capital gains story dominates the conversation: the 2.5% annual interest component was always taxable, and that part hasn’t changed. The interest is still treated as “Income from Other Sources” and added to your taxable income based on your slab. There’s no TDS deduction, which feels convenient in the moment, but it also means you’re responsible for correctly reporting it in your ITR.

One of the more debated aspects of the Budget 2026 change is the government’s interpretation regarding secondary-market investors. Arihant Capital’s explainer points to an Income Tax Department FAQ referencing an internal Department of Economic Affairs memo from December 2022. The position taken there is that the exemption was never intended for secondary-market buyers.

But tax professionals have pushed back on that interpretation. Their argument is fairly simple: whatever the intent may have been internally, the wording of the law before April 2026 did not explicitly distinguish between original subscribers and secondary-market buyers. Which is why the formal amendment became necessary in the first place.

That nuance may eventually matter in legal or interpretational debates, though for practical purposes, investors now have to work with the amended rules already in force.

And honestly, this is where things get messy for ordinary investors. SGB taxation used to be one of the easiest things to explain in personal finance. Now it has layers, acquisition route, holding period, redemption method, and maturity timing. Enough moving parts that speaking to a chartered accountant before making a large redemption decision is probably sensible rather than optional.

Original Subscribers vs. Secondary Market Buyers

Budget 2026 has effectively split SGB investors into two very different camps. On paper, the bonds may look identical. In practice, their tax treatment can now diverge sharply.

Category 1: Original Subscriber, Holding Till Maturity

If you bought your SGBs directly during the original RBI subscription window, through SBI, HDFC Bank, ICICI Bank, Zerodha, Upstox, a post office, or RBI Retail Direct, and you hold those bonds all the way to the end of the 8-year term, your capital gains remain fully tax-free.

That benefit survives intact.

So, despite all the anxiety around the Budget changes, long-term original subscribers are still in an enviable position. As confirmed by INDmoney, investors who entered through the primary issue and stay invested until maturity continue enjoying the old exemption.

In many ways, the government is signalling exactly what kind of behaviour it wants to reward: patient, long-duration holding rather than active trading.

Category 2: Original Subscriber, Premature Redemption After April 1, 2026

This is where many investors have been caught off guard.

Even if you were an original subscriber, choosing the RBI’s premature redemption route after April 1, 2026 now triggers taxation on the gains. Since premature redemption is allowed only after the fifth year, almost all such exits will fall under LTCG taxation.

Which means 12.5% tax without indexation.

For investors who were planning to exit early simply because gold prices are currently elevated, this changes the calculation quite a bit. A premature redemption that once felt clean and tax-efficient now comes with a meaningful haircut.

Category 3: Secondary Market Buyer

This is arguably the group most affected by the change.

If you purchased SGBs later on NSE or BSE instead of during the original RBI issue, your gains are now taxable regardless of whether you redeem at maturity or exit early.

That means:

- More than 12 months holding period: 12.5% LTCG

- 12 months or less: slab-rate STCG

Previously, many investors intentionally bought discounted SGBs from the exchange because they expected to eventually receive tax-free maturity redemption from the RBI. That arbitrage strategy has lost a lot of its appeal.

Kotak Neo’s analysis notes that the broader intent appears to be discouraging speculative trading while preserving incentives for long-term primary subscribers.

And when you step back, the new structure becomes pretty stark:

| Investor Type | How Purchased | Exit Route | Tax Treatment (from April 1, 2026) |

| Original subscriber | Primary issue | Held to 8-year maturity | Tax-Free |

| Original subscriber | Primary issue | Premature RBI redemption | 12.5% LTCG (without indexation) |

| Secondary market buyer | NSE/BSE | Held to 8-year maturity | 12.5% LTCG (without indexation) |

| Secondary market buyer | NSE/BSE | Premature RBI redemption | 12.5% LTCG (without indexation) |

| Any investor | Primary or Secondary | Sold on NSE/BSE | 12.5% LTCG or slab-rate STCG |

Do I have to pay tax on SGB maturity in 2026?

The answer depends entirely on how you acquired the bond.

If you subscribed during the original RBI issue and hold the SGB until the full 8-year maturity date, your capital gains remain tax-free even after Budget 2026.

But if you bought the same bond later from the secondary market, through NSE or BSE, the exemption no longer applies. In that case, you’ll owe 12.5% LTCG tax on the gains when the bond matures.

Likewise, if you are an original subscriber but choose premature redemption after the fifth year instead of waiting for maturity, the gains from that exit are also taxable at 12.5% LTCG from April 1, 2026 onward.

One thing that hasn’t changed: the 2.5% annual interest remains taxable according to your income slab. That part was never exempt.

For updated references on the broader April 2026 financial rule changes see here,

SGB LTCG tax rate 2026 without indexation

Under the revised framework effective from April 1, 2026, non-exempt SGB gains are taxed at a flat 12.5% LTCG rate without indexation.

That “without indexation” part matters more than many investors realise.

Indexation normally adjusts your purchase price upward to account for inflation, reducing the taxable gain on paper. But SGBs under the new rules don’t get that adjustment. So the tax applies to the full nominal gain.

Say someone bought SGBs at ₹8,000 per gram and eventually redeems them at ₹15,000 per gram. The taxable gain becomes ₹7,000 per gram, and the LTCG tax works out to ₹875 per gram.

ClearTax provides a larger worked example: a secondary-market investor who bought SGBs worth ₹15 lakh and redeemed them later for ₹40 lakh would generate a taxable gain of ₹25 lakh, resulting in ₹3,12,500 in LTCG tax.

Under the older regime, that liability would effectively have been zero.

That’s the scale of the shift investors are now dealing with.

SGB Premature Redemption: May 2026 Window

Eligible SGB Tranches for May 2026 Redemption

For SGB investors considering an early exit in 2026, May is an important month. The RBI’s premature redemption calendar is now active for a large batch of older Sovereign Gold Bond tranches that have crossed the mandatory five-year holding requirement.

According to Angel One’s report, the April to September 2026 schedule covers 33 different SGB tranches spanning the 2018-19 through 2021-22 issuances. In plain terms, a huge number of investors who bought bonds several years ago are suddenly becoming eligible to exit through the RBI route.

And because gold prices are hovering near historic highs, many people are paying attention now in a way they probably weren’t six months ago.

One of the earliest tranches in this cycle is the SGB 2018-19 Series II (ISIN: IN0020181001), originally issued on October 23, 2018. Its premature redemption date fell on April 23, 2026, with the submission window running from March 23 to April 13, 2026.

That timing pattern matters because many investors misunderstand how these windows work. You cannot simply wake up on the redemption date and decide to exit. The request typically needs to be submitted weeks in advance.

Meanwhile, May 2026 itself includes several notable maturity and redemption events tied to the 2018-19 and 2019-20 series.

The standout example is the SGB 2018-19 Series I, which reached full 8-year maturity on May 4, 2026. The RBI fixed the final redemption price at ₹14,901 per gram, compared to the original issue price of ₹3,064 per gram. That translates into an eye-catching return of roughly 386%, as covered by Angel One.

Honestly, numbers like that explain why SGBs built such a loyal investor base in India. Someone who quietly bought these bonds years ago and simply forgot about them has suddenly ended up sitting on extraordinary gains.

For investors dealing specifically with May 2026 premature redemptions, the most reliable operational reference remains the NSDL redemption calendar.

That document contains the exact redemption dates, submission deadlines, and eligible tranches.

Another important May event involved the SGB 2018-19 Series VIII tranche. The RBI officially notified the premature redemption price for bonds due on May 18, 2026.

Recent redemption cycles have generally produced payout prices in the ₹14,800 to ₹14,950 per gram range, reflecting the sharp rise in gold prices globally and domestically.

For investors trying to confirm whether their bonds are eligible in May 2026, the following tranches are among the key ones to verify against the NSDL calendar:

- SGB 2018-19 Series III through VII

- SGB 2019-20 Series I and II

The easiest way to check is by locating your ISIN code in your demat statement and matching it against the official schedule. Slightly tedious, yes. But necessary.

For investors holding multiple SGB tranches across different years, this becomes especially important because redemption windows do not open simultaneously for every issue.

How RBI Calculates the SGB Redemption Price

One question comes up almost every time an SGB redemption window approaches:

“How exactly does the RBI decide the payout amount?”

Fortunately, the formula itself is straightforward, even if gold price movements make the final number unpredictable.

As specified in the RBI notification governing the scheme, the redemption price is calculated as:

Redemption Price = The simple average of the closing price of 999 purity gold published by the India Bullion and Jewellers Association (IBJA) for the last three working days of the week preceding redemption.

That sounds technical at first glance, but practically it means:

- The RBI does not use a single day’s gold price

- It averages the final three working days before redemption

- IBJA rates are treated as the official benchmark

- The calculation is based on 24-karat (999 purity) gold

- Payment is always made in Indian Rupees, not physical gold

You can track the benchmark rates directly at:

https://ibjarates.com/

Take the May 2026 maturity of SGB 2018-19 Series I as an example. The RBI used the gold closing prices from April 28, 29, and 30, 2026. The resulting average came to ₹14,901 per gram.

That figure then became the official redemption payout.

For premature redemptions, the same process applies. Typically, the RBI publishes the official redemption price around two business days before the actual payout date.

Investors can monitor upcoming announcements through the RBI press release page.

Several platforms also track these notifications in simpler language. Angel One, for instance, covered the February 2026 premature redemption for SGB 2018-19 Series VI.

There have already been multiple redemption announcements this year. Investors who exited through the January 2026 premature redemption cycle received payouts documented here.

And the first full SGB maturity payout of 2026 was discussed in detail by Upstox.

One subtle thing worth noting, because many investors confuse this point, is that the RBI redemption price is based on benchmark gold rates, not the secondary-market trading price of your SGB on NSE or BSE.

Those two numbers can differ. Sometimes meaningfully.

Can I redeem Sovereign Gold Bonds before 5 years?

No. SGBs come with a mandatory 5-year lock-in period for RBI redemption.

Before completing five years from the issue date, you cannot use the RBI’s premature redemption facility under any circumstances. The only available exit route during that period is selling the bonds on the secondary market through NSE or BSE.

That distinction catches some investors by surprise. Technically, SGBs are liquid before five years, but only if there’s enough market demand and trading volume on the exchange.

After the five-year mark, things change. The RBI opens premature redemption windows every six months, aligned with coupon payment dates. Additional windows continue during the sixth and seventh years as well.

This structure is confirmed both by Zerodha’s support documentation and the RBI FAQ.

There’s another important wrinkle now after Budget 2026: even if you qualify for premature redemption as an original subscriber, the gains from that early exit are taxable at 12.5% LTCG from April 1, 2026 onward.

So the “should I redeem early?” decision is no longer just about gold prices or liquidity needs. Tax efficiency has suddenly become central to the conversation.

SGB May 2026 exact redemption dates

The exact May 2026 redemption dates depend entirely on the specific SGB tranche and its coupon schedule.

According to the NSDL premature redemption calendar, most May 2026 redemption opportunities are linked to coupon payment dates for bonds issued during late 2018 and mid-2019.

One confirmed example is SGB 2018-19 Series VIII, whose premature redemption date fell on May 18, 2026. The RBI published the official redemption price notification on May 15, 2026.

In most cases, submission windows open roughly 30 days before the redemption date and close around 10 to 14 working days prior.

That timeline matters because many investors miss the window simply by assuming the process is instantaneous. It isn’t. Brokers and banks need advance processing time, and once a deadline passes, you generally have to wait for the next eligible redemption cycle six months later.

The safest approach is simple:

Check your ISIN, verify the redemption schedule, and mark the submission cutoff date separately from the actual redemption date.

Maturity vs. Premature Redemption: The Financial Impact

The Tax-Free Advantage of Holding SGB to Maturity

For original subscribers, holding Sovereign Gold Bonds until the full 8-year maturity date has become dramatically more valuable after Budget 2026.

Before the tax rule changes, the difference between maturity redemption and premature redemption was mostly about timing and liquidity. Now, the gap is financial. Materially financial.

Because once you redeem early, the 12.5% LTCG tax enters the picture.

And when gold prices have risen the way they have over the last several years, that tax can translate into a surprisingly large amount in rupee terms.

The best real-world example so far is the SGB 2018-19 Series I maturity in May 2026. Investors who entered at the issue price of ₹3,064 per gram received a final redemption value of ₹14,901 per gram. That’s an appreciation of roughly ₹11,837 per gram, about a 386% gain over the holding period.

Angel One covered the maturity payout.

Put differently, an investor who committed ₹1 lakh during the original issue would have ended up with approximately ₹4.86 lakh at maturity, and for qualifying primary subscribers, that gain remains entirely tax-free.

That’s the part that still makes SGBs unusual even after all the Budget changes. Very few investment products in India allow such large long-term gains to escape capital gains taxation completely.

And then there’s the interest component.

SGBs also pay 2.5% annual interest, credited semi-annually. On a ₹1 lakh investment, that works out to roughly ₹20,000 in interest over the full 8-year tenure. Yes, the interest is taxable according to your slab. Still, it’s an additional layer of return that physical gold and Gold ETFs simply do not provide.

There are also the less glamorous but practical advantages people tend to forget until they actually deal with physical gold:

- No storage worries

- No locker costs

- No purity concerns

- No making charges

- No theft risk

Upstox, in its analysis of the SGB 2018-19 Series I maturity at, estimated that investors earned nearly five times their original investment once interest payouts were included.

That’s an extraordinary outcome for what was, fundamentally, a government-backed gold instrument.

Which is why many advisors are now telling eligible primary subscribers something very simple: if you can afford to wait until maturity, waiting is probably worth it.

The tax-free maturity benefit has become the crown jewel of SGB investing after Budget 2026.

Tax Implications of Premature Redemption via RBI

Premature redemption used to feel like a clean middle ground. Investors could hold SGBs for five years, benefit from substantial gold appreciation, and still exit through the RBI route without worrying about capital gains tax.

That era ended on April 1, 2026.

Now, even original subscribers triggering premature redemption through the RBI’s official window face 12.5% LTCG tax without indexation.

And because gold has appreciated so sharply over recent years, the numbers can become large very quickly.

Consider this example:

Suppose an investor originally purchased SGBs worth ₹5 lakh at an issue price of ₹5,000 per gram. That would translate to roughly 100 grams/units. If the current RBI premature redemption price is ₹14,900 per gram, the redemption value becomes ₹14.9 lakh.

The gain is ₹9.9 lakh.

Under the old regime, that gain would have been exempt.

Under the new rules, the investor owes 12.5% LTCG tax, approximately ₹1,23,750.

That’s not a minor adjustment. For many people, it’s large enough to completely change the redemption decision.

This is why a lot of investors who initially planned to exit during the 2026 redemption windows are now reconsidering. If maturity is only a year or two away, waiting may preserve a very significant amount of money.

That said, premature redemption can still make sense in certain situations.

For example:

- Immediate liquidity needs

- Reallocating funds into higher-return opportunities

- Estate planning considerations

- Concerns about future gold price declines

- Reducing the concentration in gold exposure

Financial decisions are rarely purely mathematical. Timing, personal cash flow, and risk appetite matter too.

Another useful point highlighted by ClearTax is that capital losses from other investments may potentially be set off against SGB capital gains, subject to the standard provisions of the Income Tax Act.

That won’t eliminate tax for everyone, obviously. But for investors already carrying realised losses elsewhere in their portfolio, it may soften the impact.

What happens if I sell SGB before maturity?

If you sell your SGB on NSE or BSE before maturity, the transaction is treated like the sale of a listed security.

The taxation works as follows:

- Held for more than 12 months → 12.5% LTCG without indexation

- Held for 12 months or less → taxed as short-term capital gains according to your slab rate

This applies regardless of whether you originally subscribed through the RBI issue or bought the bond later on the secondary market.

One thing worth clarifying because there’s often confusion around it:

secondary-market sales were already taxable before Budget 2026. That part is not new.

What changed is the treatment of:

- RBI premature redemption for original subscribers

- Secondary-market buyers who hold SGBs until maturity

There’s also a practical issue investors sometimes underestimate: liquidity.

Not all SGB tranches trade actively on the exchange. Some have very low daily volumes, and many trade below their equivalent gold value (NAV). That means you may end up selling at a discount relative to what the RBI would pay through official redemption.

Live SGB prices and trading volumes can be tracked on the NSE here.

In reality, this creates an interesting dynamic:

the “best” exit route is no longer purely about taxes. It’s also about pricing, liquidity, timing, and convenience.

And in 2026, those trade-offs suddenly matter a lot more than they used to.

Selling SGB on the Secondary Market (NSE/BSE)

How the 12.5% LTCG Tax Impacts Secondary Market Sales

Selling Sovereign Gold Bonds on the stock exchange has always been taxable. That part didn’t change with Budget 2026.

What changed, and this is the crucial distinction, is that secondary-market buyers no longer enjoy a tax-free escape route at maturity.

Earlier, many investors bought discounted SGBs on NSE or BSE with the assumption that if they simply held the bonds until maturity, the RBI redemption would eventually be tax-free. That strategy made secondary-market SGBs especially attractive during periods when they traded below their intrinsic gold value.

From April 1, 2026 onward, that advantage is effectively gone.

Now, whether you:

- sell the SGB on the exchange, or

- hold it until maturity after purchasing from the secondary market,

…the gains are taxable.

The structure is straightforward:

- Holdings above 12 months: 12.5% LTCG without indexation

- Holdings of 12 months or less: taxed according to your income slab as STCG

In practical terms, this means secondary-market investors now need to evaluate SGBs more like conventional financial assets rather than uniquely tax-privileged instruments.

And honestly, this changes investor psychology quite a bit.

Previously, the “discount-to-NAV” trade was compelling. You could buy an SGB below its equivalent gold value on the exchange, collect 2.5% annual interest, then eventually redeem through the RBI tax-free. The arbitrage almost felt too good at times.

Budget 2026 narrowed that opportunity sharply.

Now the post-tax return matters far more than the headline discount.

That doesn’t make secondary-market SGBs unattractive. Far from it. They still offer:

- sovereign backing

- exposure to gold prices

- semi-annual interest income

- no storage or purity concerns

But investors now have to mentally subtract the future 12.5% LTCG liability while evaluating potential gains.

This makes pricing discipline more important than before.

Arbitrage: Premature RBI Redemption vs. Stock Exchange Sale

One of the more interesting questions in the 2026 SGB landscape is this:

If both RBI premature redemption and exchange sales are taxable now, which exit route actually makes more sense?

The answer depends mainly on four things:

price, liquidity, timing, and convenience.

1. Price

RBI redemption prices are calculated using the official 3-day IBJA average. That makes them transparent and closely linked to prevailing gold rates.

Secondary-market prices, however, move according to actual trading demand and supply.

That means an SGB may trade:

- at a premium to its gold value

- exactly at fair value

- or at a discount

You can track live SGB exchange prices here.

And compare them against benchmark IBJA rates here.

Sometimes the difference is surprisingly wide.

Thin liquidity can create odd pricing gaps, especially in less actively traded tranches. Investors occasionally find SGBs available at meaningful discounts during weak market sessions. Other times, scarcity pushes prices above fair value.

So before choosing a redemption route, it’s worth checking both numbers side by side.

2. Tax Treatment

Post-Budget 2026, the taxation between the two routes is broadly aligned.

For holdings above 12 months:

- RBI premature redemption: 12.5% LTCG

- NSE/BSE sale: 12.5% LTCG

Which means the tax angle is no longer the deciding factor for most investors.

That’s a major shift from earlier years when RBI redemption often carried a clear tax advantage.

Now the better option usually comes down to whichever route leaves you with the higher post-tax proceeds.

3. Timing and Flexibility

This is where exchange sales still retain an edge.

RBI’s premature redemption windows open only at fixed intervals tied to coupon dates. Miss the submission deadline, and you may have to wait another six months.

Exchange sales, meanwhile, can happen any trading day.

That flexibility matters if:

- you urgently need liquidity

- you expect gold prices to fall

- or you simply want faster execution

Of course, flexibility only helps if liquidity exists in your specific tranche.

Some SGBs trade actively. Others barely move.

4. Operational Simplicity

For many retail investors, exchange sales are simply easier.

Selling through your broker works much like selling any listed stock:

- place an order

- execute the trade

- receive settlement proceeds

RBI redemption requires paperwork, deadlines, and advance requests through banks or brokers.

Not difficult exactly. Just slower and more procedural.

For investors who value certainty and official benchmark pricing, RBI redemption may still feel cleaner. For investors prioritising speed and flexibility, exchange sales may be more practical.

As noted by Arihant Plus, Budget 2026 has effectively levelled the tax playing field between these two exit routes. The decision now revolves far more around pricing and execution.

SGB secondary market live price today NSE

To track live SGB prices, the primary reference point is the NSE’s Sovereign Gold Bond page.

This page provides:

- current market prices

- ISIN codes

- trading volumes

- coupon schedules

- price movement data for each SGB tranche

Every listed SGB series carries a unique ISIN beginning with “IN002.”

When evaluating whether a particular SGB is attractively priced, investors often compare the market price against the prevailing IBJA gold benchmark.

If an SGB trades below its equivalent gold value, you are effectively buying gold exposure at a discount.

But after Budget 2026, that discount alone is no longer enough to judge attractiveness. The future tax liability also has to be factored in.

That’s probably the defining theme of the new SGB regime:

the product is still powerful, but the easy arbitrage era is fading. Investors now need to think a little more carefully about entry price, holding period, and exit strategy than they did a few years ago.

Step-by-Step Guide to Redeeming SGBs

Submitting an SGB Redemption Request via Demat Brokers (Zerodha, Upstox)

For investors holding Sovereign Gold Bonds in demat form, broker-assisted redemption is usually the simplest route, though “simple” in the SGB world still involves paperwork, deadlines, and a bit more planning than people initially expect.

A common misconception is that premature redemption works like selling a stock. It doesn’t. You cannot just click “Sell” on redemption day and instantly exit through the RBI route. Premature redemption through brokers requires advance submission of a formal request.

Here’s how the process generally works for major brokers.

Zerodha (Console)

Zerodha’s official process is detailed here.

The steps are fairly procedural:

- Download the Redemption Request Form (RRF)

Zerodha provides a PDF redemption form through its support portal. You’ll need to enter details like:- your PAN

- SGB ISIN code

- quantity of units

- linked bank account details

- Fill and physically sign the form

This catches some investors off guard because digital submission is not currently accepted for premature redemption requests. A physical signature is mandatory. - Courier or mail the form to Zerodha

The signed document must be sent to Zerodha’s support centre in Bengaluru:

192A 4th Floor, Kalyani Vista,

3rd Main Road, JP Nagar 4th Phase,

Bengaluru – 560076

- Meet the submission deadline

Timing matters here. Zerodha requires the form to reach them at least 10 working days before the coupon/redemption date.

Miss that cutoff, and your redemption request typically shifts to the next eligible window, which could mean waiting another six months.

- Charges

Zerodha currently charges ₹150 plus 18% GST per redemption request. - Payout credit

Once processed, the RBI credits the redemption proceeds directly into your linked bank account on or shortly after the redemption date.

Operationally, the process is straightforward. But because it still relies on physical paperwork, many investors underestimate the lead time involved.

Upstox

Upstox follows a broadly similar structure for demat-held SGB redemptions.

Investors can monitor eligible redemption windows within their portfolio section, but the actual premature redemption request generally requires form submission ahead of the coupon date.

Upstox has also published detailed coverage of SGB redemption returns here.

The important thing to remember with all brokers is this:

The operational mechanics may vary slightly, but the RBI redemption schedule itself remains fixed. Your broker cannot override the official deadlines.

Angel One

Angel One investors should refer to the RBI’s April-September 2026 premature redemption calendar, which includes 33 eligible tranches.

On the platform side, Angel One generally allows investors to view upcoming redemption opportunities within the holdings or portfolio section.

The actual submission workflow may depend on whether the bonds are held directly in demat or through linked depository arrangements.

Important Tips for Demat-Held SGB Redemptions

A few practical checks can save a lot of frustration later:

- Confirm the SGB units are visible under your demat holdings before initiating redemption

- Verify the exact deadline for your specific tranche; deadlines differ across series

- Double-check your linked bank account details

- Keep a scanned copy of all submitted forms and acknowledgments

- If your bonds are held in physical certificate form instead of demat, the process is entirely different

For investors with physical-mode holdings, NSE issued separate guidance here.

Meanwhile, RBI Retail Direct users can submit redemption requests online through the RBI Retail Direct portal itself, which is arguably the cleanest workflow currently available.

Redeeming SGBs Offline via Banks (SBI, HDFC) and Post Offices

Not every SGB investor uses a demat account.

A large number of earlier subscribers, especially those who purchased bonds during the 2016-2019 years, still hold physical Holding Certificates issued through banks or post offices.

For these investors, redemption remains largely branch-driven and paperwork-heavy.

A little old-school, honestly. But still functional.

SBI

SBI remains one of the largest SGB distribution channels in India and handles both maturity payouts and premature redemption processing.

If your SGBs were originally subscribed through SBI, you’ll generally need to visit your home branch with:

- Original SGB Holding Certificate (Form C)

- PAN card and Aadhaar

- Bank passbook or cancelled cheque

- Written premature redemption request

Additional details on SBI-linked SGB servicing are available here.

One important operational point:

premature redemption requests usually need to be submitted around 30 calendar days before the coupon/redemption date.

That window is longer than many broker timelines.

HDFC Bank

HDFC Bank also processes premature redemption requests for bonds originally issued through its branches.

The process broadly mirrors SBI:

- visit the branch

- submit supporting documents

- file the redemption request ahead of the deadline

HDFC’s SGB information portal is available here,

And its FAQ section covering redemption and taxation changes is here.

Post Offices

Many older SGB investors subscribed through post offices, especially during the early years when awareness around demat investing was lower.

The RBI officially recognises designated post offices as authorised receiving offices for SGB-related transactions.

If your bonds were issued through a post office, redemption requests can generally be processed there as well.

Though practically speaking, procedures may vary somewhat depending on the branch and local operational familiarity with SGB handling.

ICICI Bank

ICICI Bank customers who originally subscribed through the bank can also process offline redemptions through branch visits.

Information regarding ICICI’s SGB servicing is available here.

As with other offline channels, carrying original documentation and verifying redemption deadlines in advance is essential.

One Important Habit: Always Take Written Acknowledgment

This sounds small, but it matters.

Whenever submitting an offline redemption request:

- ask for a stamped acknowledgment copy

- note the submission date

- retain photocopies of every document submitted

SGB redemptions are usually smooth, but when deadlines are involved, paperwork proof becomes extremely valuable if any dispute or delay arises later.

RBI SGB premature redemption form PDF download

For Zerodha users, the official Redemption Request Form (RRF) can be downloaded directly through Zerodha’s support article.

For NSDL/CDSL-linked holdings, redemption forms may also be available through the respective depository websites.

Bank-held SGB investors can usually obtain the required forms directly from:

- their issuing branch

- the bank’s investment portal

- or customer service channels

The RBI’s primary FAQ page for Sovereign Gold Bonds remains one of the best central references for operational guidance.

And honestly, given how many procedural deadlines now matter after Budget 2026, it’s worth checking the official RBI and NSDL resources directly instead of relying solely on third-party summaries floating around social media or forums.

Should You Hold or Sell Your SGBs in 2026?

Comparing SGB Returns to Gold ETFs and Physical Gold Post-Budget

Budget 2026 has forced many gold investors to revisit a question they probably thought was already settled:

Are Sovereign Gold Bonds still the best way to invest in gold?

The answer now depends far more on how you own SGBs than it did a few years ago.

Before the tax changes, the comparison was relatively easy. SGBs combined gold price exposure, sovereign backing, annual interest income, and broad tax advantages in a way that physical gold and Gold ETFs simply couldn’t match.

Now the gap has narrowed in some cases, though not evenly across all investors.

SGBs (Primary Subscribers Holding to Maturity) vs. Gold ETFs

For original subscribers who intend to hold until full maturity, SGBs still retain a major edge.

The biggest reason is straightforward:

capital gains at maturity remain tax-free.

Gold ETFs, meanwhile, now attract 12.5% LTCG tax after the broader taxation changes introduced over the last two budgets. Indexation benefits are gone there too.

So, if two investors both benefit from rising gold prices over eight years:

- the Gold ETF investor eventually pays tax on gains

- the eligible SGB maturity investor does not

That’s a meaningful difference in long-term compounding.

And then there’s the 2.5% annual interest.

Gold ETFs track gold prices, but they don’t generate income. SGBs do. Even after taxation at slab rates, that extra return layer adds up over long holding periods.

The RBI’s FAQ also confirms that SGBs remain fully linked to gold prices because they are denominated in grams of gold.

So for disciplined long-term investors who subscribed through primary issuance, SGBs still arguably sit in a class of their own.

SGBs (Secondary Market Buyers) vs. Gold ETFs

This comparison has become more balanced after Budget 2026.

Secondary-market SGB buyers no longer receive tax-free maturity treatment, which means both SGBs and Gold ETFs now broadly fall under the same 12.5% LTCG framework.

That reduces one of the historic advantages of buying SGBs from NSE/BSE.

Gold ETFs, meanwhile, retain some practical strengths:

- better exchange liquidity

- tighter bid-ask spreads

- easier intraday execution

- no redemption-window restrictions

But SGBs still offer something ETFs don’t:

the 2.5% annual interest payout.

For investors in lower or moderate tax brackets, that additional income can still tilt the comparison in favour of SGBs over long periods.

So, the newer post-Budget reality is less about “which product is universally superior” and more about investor behaviour:

- long-term original subscribers → SGBs remain exceptionally attractive

- active traders or liquidity-focused investors → Gold ETFs become more competitive

SGBs vs. Physical Gold

This is the one comparison where SGBs still dominate rather comfortably.

Physical gold carries hidden costs that investors often normalise because they’re culturally familiar:

- making charges

- storage costs

- locker fees

- insurance

- purity verification issues

- theft risk

And after the recent tax changes, physical gold now faces broadly similar capital gains taxation anyway.

Which raises an obvious question:

if both are taxable, why absorb all the operational friction of physical gold when SGBs additionally provide 2.5% annual interest?

Physical gold does retain one advantage:

instant liquidity without waiting for redemption windows.

You can sell jewellery or coins anytime. Though practically, that often comes with deduction losses, resale spreads, or valuation negotiations.

For long-term investors focused primarily on wealth creation rather than jewellery consumption, SGBs remain structurally more efficient.

Canara HSBC Life summarised this point well here.

Even after Budget 2026, eligible primary subscribers holding to maturity continue enjoying one of the strongest post-tax return profiles available in India’s gold investment ecosystem.

Is it wise to sell SGB now?

That depends almost entirely on what category of investor you fall into.

For Original Subscribers

In most cases, selling now probably isn’t the financially optimal move if maturity is still realistically achievable.

Why?

Because the tax-free maturity benefit has become disproportionately valuable after Budget 2026.

If you:

- redeem prematurely through RBI, or

- sell on the secondary market,

…you trigger 12.5% LTCG tax on gains that could otherwise remain exempt at maturity.

For investors who entered SGBs years ago at ₹3,000–₹5,000 per gram levels, the gains today are substantial enough that the tax impact becomes very real in rupee terms.

Unless you:

- urgently need liquidity

- expect a sharp gold price correction

- or need to rebalance your portfolio,

holding until maturity often remains the stronger financial decision.

For Secondary Market Buyers

The situation is more nuanced.

Since secondary-market investors now face LTCG taxation regardless of exit route, the decision becomes more about market timing and opportunity cost than tax optimisation.

In simple terms:

- Do you believe gold prices still have meaningful upside?

- Or are current levels attractive enough to lock in gains?

That’s the real question now.

Because from a tax perspective, there’s no major advantage in waiting for maturity anymore if you entered through NSE/BSE.

For these investors, comparing:

- RBI redemption pricing via IBJA benchmarks

against:

…becomes more important than before.

Sometimes the exchange premium may justify an immediate sale. Other times, RBI redemption offers cleaner value.

The Bigger Picture: Gold Has Already Had a Massive Run

One reason these decisions feel emotionally difficult in 2026 is that the returns have been extraordinary.

Investors who bought SGBs between 2017 and 2020 at prices around ₹2,800–₹5,000 per gram are now looking at gold values near ₹14,500–₹15,000 per gram.

That kind of appreciation changes investor psychology.

People start wondering:

- “Should I lock profits now?”

- “What if gold corrects?”

- “What if prices go even higher?”

And honestly, there’s no universally correct answer there.

Gold has benefited globally from:

- geopolitical uncertainty

- central-bank buying

- inflation concerns

- currency volatility

- safe-haven demand

Whether that trend continues depends on macroeconomic conditions far larger than any single SGB tranche.

A Final Note on New SGB Issuances

One overlooked detail in all the discussion around Budget 2026 is this:

new SGB issuances are still expected.

The government indicated in Budget 2025-26 that additional tranches would continue to be issued.

That matters because fresh primary subscriptions still qualify for the full maturity exemption under the revised rules.

So despite all the noise around taxation changes, the original SGB formula still survives for disciplined long-term investors willing to:

- subscribe during primary issuance

- hold patiently for eight years

New issuance announcements can be tracked through the PIB.

And in some ways, that may end up being the clearest dividing line in the new SGB era:

patient primary subscribers remain highly rewarded; everyone else now has to think more carefully about taxes, timing, and exits.

Navigating the New SGB Landscape

Sovereign Gold Bonds are still one of the most thoughtfully designed investment products India has produced. That hasn’t changed.

What has changed is the simplicity.

For years, SGBs enjoyed a reputation as the “easy yes” gold investment, government-backed, interest-paying, tax-efficient, and relatively hassle-free. Budget 2026 hasn’t destroyed those advantages, but it has made them far more conditional.

The broad, universal tax exemption that once applied across most redemption scenarios is now sharply targeted. The biggest beneficiaries going forward are patient investors who subscribed during the original RBI issuance and are willing to stay invested until full maturity.

Everyone else now has to calculate more carefully.

Here’s what really matters in the new landscape:

If You Are a Primary Subscriber

Your tax-free maturity benefit is now extremely valuable.

In many cases, it may be the single most important reason to continue holding the bond until the end of the 8-year term. Premature redemption or secondary-market sale could trigger a 12.5% LTCG liability on gains that might otherwise remain fully exempt.

And when those gains are already running into several lakhs for older tranches, that difference becomes impossible to ignore.

Unless you genuinely need liquidity or have a strong strategic reason to exit, patience may still be the highest-return decision.

If You Bought Through the Secondary Market

The rules are now more straightforward, even if less favourable.

You should assume your gains will be taxed at 12.5% LTCG regardless of whether you:

- redeem through RBI, or

- sell on the exchange

That shifts the focus away from tax arbitrage and toward execution quality:

- Which route gives the better price?

- Is the exchange trading at a premium or discount?

- Does immediate liquidity matter?

The 2.5% annual interest still improves overall returns, but the old “tax-free maturity” strategy for secondary-market buyers is effectively gone.

For Investors Planning May 2026 Redemptions

Operational details matter more than many people expect.

Check the NSDL premature redemption calendar carefully. Verify:

- your tranche eligibility

- ISIN code

- submission deadline

- redemption date

If using brokers like Zerodha, ensure forms reach them at least 10 working days before the coupon date. For bank-held SGBs, the lead time may be closer to 30 calendar days.

And remember:

the RBI generally announces the final redemption price around two business days before payout.

For Tax Planning

This is no longer a product where investors should casually assume the tax treatment.

Depending on:

- acquisition method

- holding period

- exit route

- capital-loss set-offs

- and broader portfolio structure,

…the actual post-tax outcome can vary significantly between investors holding seemingly identical bonds.

Speaking with a chartered accountant or SEBI-registered investment advisor before a large redemption decision is probably prudent now, especially for investors sitting on substantial gains from older SGB tranches.

Frequently Asked Questions: RBI Sovereign Gold Bonds 2026

Following Budget 2026 amendments effective April 1, 2026, the complete capital gains tax exemption at maturity applies strictly to original subscribers who buy during the primary RBI issuance and hold the bond for the full 8-year tenure. If you buy SGBs from the secondary market (NSE/BSE) or opt for premature RBI redemption, your profits are subject to a flat 12.5% Long-Term Capital Gains (LTCG) tax with zero indexation benefits.

No. The RBI enforces a strict 5-year lock-in period from the initial issue date, during which official premature redemption is prohibited. If you require liquidity before 5 years, your only exit route is selling your dematerialized SGB units on the secondary market via a stock exchange (NSE or BSE), subject to prevailing market demand and trading volumes.

The RBI determines the SGB redemption price using a transparent benchmark formula: the simple average of the closing prices of 999 purity (24-karat) gold published by the India Bullion and Jewellers Association Limited (IBJA) for the last three working days of the week preceding the redemption date.

| Investor Type | Acquisition Route | Exit Route | Holding Period | Capital Gains Tax | Interest Taxation | Operational Method |

| Original Subscriber | Primary Issue | RBI Maturity | Full 8 years | Tax-Free | Taxed at slab rates | Automatic bank credit on maturity |

| Original Subscriber | Primary Issue | RBI Premature Redemption | 5 to 8 years | 12.5% LTCG (no indexation) | Taxed at slab rates | Submit physical RRF to bank/broker 10-30 days before coupon date |

| Secondary Market Buyer | NSE / BSE | RBI Maturity | More than 12 months | 12.5% LTCG (no indexation) | Taxed at slab rates | Automatic bank credit on maturity |

| Secondary Market Buyer | NSE / BSE | RBI Premature Redemption | More than 5 years from issue | 12.5% LTCG (no indexation) | Taxed at slab rates | Submit physical RRF to broker during RBI window |

| Any Investor | Primary or Secondary | Stock Exchange Sale | More than 12 months | 12.5% LTCG (no indexation) | Taxed at slab rates | Instant electronic sale via trading platform |

| Any Investor | Primary or Secondary | Stock Exchange Sale | 12 months or less | STCG (Taxed at slab rates) | Taxed at slab rates | Instant electronic sale via trading platform |

The Bigger Reality

Despite all the noise around Budget 2026, one thing remains undeniable:

SGBs have delivered extraordinary long-term returns.

The first 2026 maturity cycle demonstrated that clearly. Investors who entered early SGB tranches at prices near ₹3,000 per gram saw redemption values approach ₹15,000 per gram, alongside years of additional interest income.

That kind of performance is difficult to dismiss.

So while the rules have become more layered and less forgiving, the core story of Sovereign Gold Bonds still holds up surprisingly well: For patient investors who understand the structure, SGBs remain one of the strongest long-term gold investment vehicles available in India.

Disclaimer

This article is for informational purposes only and does not constitute financial or tax advice. SGB taxation is a complex subject with nuances that may affect individual investors differently. Please consult a SEBI-registered investment advisor and a qualified chartered accountant before making investment or tax decisions related to Sovereign Gold Bonds.

Leave a Reply