Senior Citizen Savings Scheme (SCSS) 2026: Maximize Your Returns & Tax Benefits

Why the Senior Citizen Savings Scheme (SCSS) is the Ultimate Retirement Investment in 2026

If you have recently retired or you’re helping a parent, make sense of life after retirement, you’ve probably heard the term Senior Citizen Savings Scheme more than once. Bank managers recommend it. Financial advisors bring it up early in the conversation. And among retirees, it often comes up whenever the discussion turns to safe and reliable income.

There’s a simple reason for that.

Many retirement products promise attractive returns, but those returns often come with a level of risk that isn’t always obvious at first glance. The Senior Citizen Savings Scheme (SCSS) takes a different approach. It is backed by the Government of India, offers regular quarterly income directly into your bank account, and, as of Q1 FY 2026–27, provides an interest rate of 8.2% per annum, higher than what most senior citizen fixed deposits currently offer.

In this guide, we’ll walk through everything you need to know about the Senior Citizen Savings Scheme in 2026. You’ll learn who can open an account, how much you can invest, how the quarterly interest payments work, the tax implications, where the scheme is available, and the potential drawbacks that retirees should be aware of before investing. We’ll also compare SCSS with bank fixed deposits and other popular post office savings options so you can decide where it fits into your retirement plan.

All key figures and scheme details have been sourced from the official government portal, India Post, and the scheme’s official listing.

At A Glance: Senior Citizen Savings Scheme (SCSS) 2026

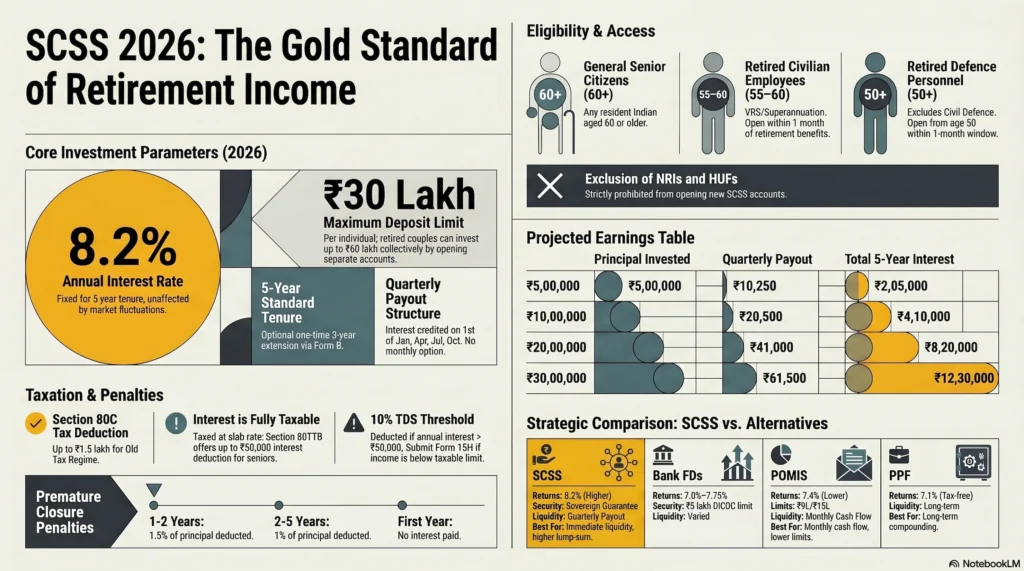

- Guaranteed Interest Rate: Secure a fixed 8.2% per annum, locked in for the entire 5-year tenure (current as of Q1 FY 2026–27).

- Predictable Cash Flow: Returns are credited quarterly (not monthly) directly to your linked savings account, ensuring a reliable income stream.

- Investment Limits: Open an account with a minimum of ₹1,000, up to a maximum deposit of ₹30 Lakh per individual. A retired couple can jointly secure up to ₹60 Lakh through separate accounts.

- Scheme Tenure: The standard maturity period is 5 years, with a one-time option to extend the account for an additional 3 years at the prevailing interest rate.

- Eligibility Rules: Open to resident Indians aged 60 and above. Early access is granted to retired civilian employees (55+) and retired defence personnel (50+) if opened within one month of receiving retirement benefits. Non-Resident Indians (NRIs) and HUFs cannot open accounts.

- Tax Benefits & Deductions: Initial deposits qualify for Section 80C deductions up to ₹1.5 Lakh under the old tax regime. While the quarterly interest is taxable, eligible senior citizens can claim a deduction of up to ₹50,000 under Section 80TTB.

- Sovereign Safety: Backed entirely by the Government of India, the scheme offers a 100% sovereign guarantee, eliminating the risk associated with standard bank fixed deposits.

- Wide Accessibility: Accounts can be easily opened across India Post branches and authorized public and private sector banks (including SBI, HDFC, and ICICI).

What are the details of the SCSS Senior Citizen Savings Scheme in 2026?

The Senior Citizen Savings Scheme (SCSS) was introduced in 2004 under the Government Savings Promotion Act, 1873, with a clear objective: to give retirees a safe place to park their retirement savings while generating a steady and predictable income. More than two decades later, it remains one of India’s most trusted retirement-focused investment options.

Its popularity hasn’t happened by accident. Retirees generally have different priorities from younger investors. Instead of chasing high-growth opportunities, many are looking for stability, regular cash flow, and protection of capital. SCSS was designed specifically with those needs in mind. According to RTI Wiki, the scheme had approximately 2.6 crore active accounts across India Post and authorized banks by the end of FY 2024-25, highlighting just how widely it is used across the country.

As of 2026, the scheme operates under the following key parameters:

| Feature | Details |

| Interest Rate | 8.2% per annum |

| Minimum Deposit | ₹1,000 |

| Maximum Deposit | ₹30,00,000 (₹30 Lakh) |

| Tenure | 5 years |

| Extension | Once, for 3 additional years |

| Interest Payout | Quarterly (not monthly) |

| Tax Benefit | Section 80C deduction up to ₹1.5 lakh |

| TDS Threshold | ₹50,000 per year |

Eligibility and Age Criteria

Eligibility for SCSS is governed by the Senior Citizen Savings Scheme Rules, 2004, along with subsequent amendments. Broadly speaking, there are three categories of people who can open an account, as confirmed by the official government listing of the scheme.

Category 1 – General Senior Citizens

Any resident Indian who is 60 years of age or older can open an SCSS account. This is the most common route and applies to the vast majority of applicants.

Category 2 – Retired Civilian Employees (VRS/Superannuation)

Individuals between 55 and 60 years of age may also qualify if they have retired through superannuation, voluntary retirement (VRS), or a special VRS scheme. However, there is an important condition: the account must be opened within one month of receiving retirement benefits, and the amount invested cannot exceed those benefits.

Category 3 – Retired Defence Personnel

Defence personnel (excluding Civil Defence employees) can open an SCSS account from the age of 50 onwards. The same one-month rule from receipt of retirement benefits applies here as well.

Who Cannot Open an SCSS Account?

Not everyone qualifies.

Non-Resident Indians (NRIs) and Hindu Undivided Families (HUFs) are specifically excluded from the scheme. If an individual becomes an NRI after opening an SCSS account, the account is generally allowed to continue until maturity, although it’s always advisable to confirm the latest rules with the bank or post office handling the account.

Joint Account Rules

SCSS accounts can be opened jointly, which is often useful for married couples. The key requirement is that the primary account holder must satisfy the age eligibility criteria. The second holder can be younger than 60 years.

For taxation purposes, however, the account belongs to the primary holder. Interest income and deposits are attributed to the first holder, not shared between both account holders.

Documents Required for Opening an Account

Opening an SCSS account is usually a straightforward process. In most banks and post offices, the account can be activated on the same day if all documents are available.

Typically, you’ll need:

- Aadhaar card

- PAN card (mandatory for deposits above ₹50,000)

- Proof of age

- Passport-size photograph

- Cheque, bank transfer, or other accepted payment method for the deposit amount

It is also strongly recommended to add a nominee during account opening. This can be done through Form SC-2 and helps ensure a smoother transfer process for family members in the future.

Senior Citizen Savings Scheme Maximum Amount & Minimums

The scheme allows a minimum deposit of ₹1,000, and all deposits must be made in multiples of ₹1,000.

On the upper end, the maximum investment limit is ₹30 lakh per individual. This limit was increased from ₹15 lakh to ₹30 lakh through the Union Budget 2023 and became effective from 1 April 2023, as noted by this guide.

A point that often causes confusion is how this limit applies to couples.

The ₹30 lakh ceiling applies to each eligible individual, not to a household. This means that a husband and wife can each open separate SCSS accounts and invest up to ₹30 lakh each. Together, a retired couple can therefore invest as much as ₹60 lakh under the scheme.

One important restriction remains: SCSS accepts only a lump-sum deposit at the time of opening. Once the account is active, you cannot keep adding money to it later.

For couples able to invest the maximum amount, the income generated can be substantial. At the current 8.2% rate, a ₹30 lakh investment produces ₹2,46,000 annually in interest. For two separate accounts at the maximum limit, the combined annual interest reaches ₹4,92,000, paid out in quarterly installments. This predictable income stream is one of the main reasons financial planners often recommend SCSS as the first destination for retirement funds before exploring other fixed-income options.

Deposits can be made through cheque, cash (subject to applicable limits), or electronic transfer methods such as NEFT and IMPS, depending on the bank or post office branch handling the account.

Tenure and Extension Rules

An SCSS account comes with a standard tenure of five years from the date it is opened. That timeframe strikes a balance between providing retirees with a stable income source and giving them access to their capital within a reasonable period.

When the account reaches maturity, investors have three possible paths to choose from.

1. Withdraw the principal and close the account

This is the simplest option. Since the scheme pays interest every quarter throughout the five-year period, there is no accumulated interest waiting at maturity. You simply receive your original principal back and close the account.

2. Extend the account for an additional three years

SCSS allows a one-time extension of three years beyond the original five-year term. To do this, you must submit Form B at the post office or authorized bank branch within one year of the maturity date.

There is one detail many investors overlook: the interest rate during the extension period is not the rate you originally locked in when opening the account. Instead, the account earns whatever SCSS rate is applicable at the time the extension is approved.

That means the extension could work in your favor if rates are higher in the future. On the other hand, if rates have declined, your income from the account could be lower than during the first five years.

3. Leave the account unattended after maturity

While some institutions may continue paying interest at the prevailing Post Office Savings Account rate if the funds remain unclaimed, this rate is usually far lower than the SCSS rate. In practice, allowing the account to drift beyond maturity rarely makes financial sense.

For that reason, it’s worth marking the maturity date well in advance and deciding whether you’ll withdraw or extend the account before the deadline arrives.

Premature Withdrawal Rules

Life doesn’t always follow a plan, and sometimes retirees need access to their funds earlier than expected.

SCSS does permit premature closure, but penalties apply. As noted by this guide.

- If the account is closed before completing one year, no interest is payable.

- If closed after one year but before two years, a penalty of 1.5% of the principal amount is deducted.

- If closed after two years but before five years, the penalty reduces to 1% of the principal amount.

The penalties are not severe compared with many other long-term savings products, but they are still worth factoring into your retirement planning. Ideally, money placed in SCSS should be capital you are unlikely to need for major emergencies during the tenure.

SCSS Interest Rate & Payout Structure (Updated 2026)

For most retirees, the interest rate is the main attraction of the Senior Citizen Savings Scheme, and in 2026, it remains one of the strongest reasons to consider the product.

Current SCSS Interest Rates

The SCSS interest rate is determined by the Ministry of Finance and reviewed every quarter. For Q1 FY 2026–27 (April–June 2026), the rate remains at 8.2% per annum, unchanged from previous quarters.

According to this guide, the government maintained the same rate throughout FY 2025–26 as well, creating a rare period of stability in a market where interest rates often move up and down.

One of the biggest advantages of SCSS is that the interest rate is locked in when you open the account.

This means that if you invest today at 8.2%, you continue earning 8.2% for the entire five-year tenure, even if the government reduces the SCSS rate for new investors in future quarters. That predictability is particularly valuable for retirees who depend on regular income and prefer certainty over constantly chasing higher rates.

A quick look at recent history helps put today’s rate into perspective:

| Period | SCSS Rate |

| FY 2020–21 | 7.4% |

| FY 2022–23 | 7.4%–8.0% |

| Q1 FY 2023–24 onwards | 8.2% |

| Q1 FY 2026–27 | 8.2% |

The fact that the scheme has remained at 8.2% since April 2023 highlights both the government’s focus on senior citizen welfare and the broader interest-rate environment over the past few years.

Addressing the “Post Office Senior Citizen Savings Scheme Monthly Income” Myth

A surprisingly common misconception is that SCSS pays interest every month.

It doesn’t.

SCSS pays interest quarterly, not monthly.

The interest is credited directly to the linked savings account on the first day of each quarter month:

| Quarter | Interest Payout Date |

| April–June | 1st July |

| July–September | 1st October |

| October–December | 1st January |

| January–March | 1st April |

This schedule is confirmed here.

The confusion usually arises because many retirees compare SCSS with other post office products that do provide monthly income. If your goal is to receive money every month, you’re probably thinking of the Post Office Monthly Income Scheme (POMIS), which currently offers a lower interest rate but distributes earnings monthly.

In practice, many retirees use both products together. SCSS provides a higher overall return, while POMIS helps smooth monthly cash flow. The combination can create a more predictable retirement income structure without taking on additional investment risk.

A simple but useful tip: enable SMS or app notifications on the savings account linked to your SCSS investment. That way, you’ll receive an alert every time the quarterly interest arrives, making it easy to track your income without manually checking passbooks or statements.

Senior Citizen Savings Scheme Interest Rate Calculator / Post Office Senior Citizen Scheme Calculator

Estimating your income from SCSS is relatively straightforward because the scheme pays simple interest.

The calculation is:

Quarterly Interest = (Principal × 8.2%) ÷ 4

Here is how the numbers work out at common investment levels:

| Principal Invested | Quarterly Interest | Annual Interest (Total over 5 years) |

| ₹5,00,000 | ₹10,250 | ₹41,000 (₹2,05,000 over 5 years) |

| ₹10,00,000 | ₹20,500 | ₹82,000 (₹4,10,000 over 5 years) |

| ₹15,00,000 | ₹30,750 | ₹1,23,000 (₹6,15,000 over 5 years) |

| ₹20,00,000 | ₹41,000 | ₹1,64,000 (₹8,20,000 over 5 years) |

| ₹30,00,000 | ₹61,500 | ₹2,46,000 (₹12,30,000 over 5 years) |

One thing worth remembering is that SCSS does not compound interest. Every quarter, you receive the same fixed payout, and your original principal remains unchanged until maturity.

That design is intentional. SCSS is built to generate income, not to grow a corpus through reinvestment.

If you’d like to calculate projected earnings for your own deposit amount, you can use these calculators: https://www.getyep.co/scss-calculator/ or https://groww.in/calculators/scss-calculator.

Both tools provide instant estimates of quarterly payouts and total interest income. A more detailed calculator with tax-impact projections is also available here.

Where to Open an SCSS Account

SCSS is widely accessible across India, which is one of the reasons it has become such a popular retirement savings option. Whether you live in a major city or a small town, opening an account is usually straightforward.

Broadly, you have two choices: a post office or an authorized bank.

Post Office vs. Authorized Banks

The Senior Citizen Savings Scheme can be opened through:

India Post (Post Offices)

India Post remains the largest distribution network for SCSS. With more than 1.6 lakh post office branches across the country, it offers unmatched reach, especially in rural and semi-urban areas where banking options may be limited.

Existing account holders can access certain services online through India Post, although new account openings generally still require an in-person visit.

For many retirees, particularly those living outside major cities, the local post office remains the most convenient and familiar option.

Authorized Banks

SCSS is also available through a number of government-authorized public and private sector banks. As of 2026, these include institutions such as:

- State Bank of India (SBI)

- Punjab National Bank (PNB)

- Bank of Baroda

- Canara Bank

- Indian Bank

- Union Bank of India

- ICICI Bank

- HDFC Bank (select branches)

The process is largely identical regardless of where you open the account. You’ll need to complete the application form, submit KYC documents, and fund the deposit through cheque, transfer, or another accepted payment method. In most cases, the passbook is issued on the same day.

For retirees who already maintain a long-standing relationship with a particular bank, opening SCSS there often feels more convenient. Others prefer the post office because of its familiarity and extensive branch network.

Ultimately, the scheme itself remains exactly the same regardless of the institution you choose.

Senior Citizen Savings Scheme Interest Rate SBI & Other Major Banks

One question comes up repeatedly: does SBI offer a better SCSS interest rate than the post office? What about ICICI Bank, HDFC Bank, or Bank of Baroda?

The answer is simple: no.

SCSS is a government-backed scheme, not a bank-designed deposit product. The interest rate is fixed by the Government of India and applies uniformly across all authorized institutions.

Whether you open your account at a post office, SBI, PNB, ICICI Bank, Bank of Baroda, or any other approved institution, the interest rate remains exactly 8.2% per annum.

What differs is not the return, but the experience.

Some institutions may offer better online access. Others may have more convenient branch locations, faster service, or stronger customer support. Those operational differences often matter more than retirees initially realize.

For example, many investors choose SBI simply because of its nationwide presence and extensive branch network. Details of SBI’s SCSS offering can be found here.

Similarly:

- Bank of India’s SCSS information is available at https://bankofindia.bank.in/senior-citizens-savings-scheme

- Bank of Baroda provides scheme details at https://bankofbaroda.bank.in/investments/government-deposit-schemes/senior-citizen-savings-deposit-scheme

- ICICI Bank’s SCSS FAQs are available at https://www.icici.bank.in/personal-banking/accounts/savings-account/senior-citizens/faqs

- HDFC Bank’s senior citizen account information can be accessed at https://www.hdfc.bank.in/savings-account/senior-citizen-account

- PNB-related information is available at https://www.bankbazaar.com/saving-schemes/pnb-senior-citizens-savings-scheme.html

For most retirees, the practical approach is straightforward: if you already have a savings account with a bank you trust, opening SCSS there can make quarterly interest credits seamless and easier to track.

If you’re starting from scratch and simply want broad accessibility, a nearby SBI branch, another large public-sector bank, or your local post office will generally serve the purpose equally well.

The important thing to remember is that your return remains identical wherever you open the account. The decision is really about convenience, accessibility, and service, not interest rate.

Tax Benefits and TDS Rules for SCSS

For many retirees, the appeal of SCSS isn’t limited to its 8.2% return. The scheme also offers certain tax advantages that can improve overall returns, provided you understand how the rules actually work.

At the same time, SCSS is often misunderstood as a tax-free investment. It isn’t. While there are tax deductions available, the interest earned remains taxable in most cases.

Let’s break down the rules clearly.

Section 80C Deductions on Deposits

Deposits made into SCSS qualify for deduction under Section 80C of the Income Tax Act, subject to the overall Section 80C limit of ₹1.5 lakh per financial year.

However, there’s an important catch.

As explained in this guide, this deduction is available only under the old tax regime. If you have opted for the new tax regime, which is now the default regime for most taxpayers, you cannot claim the Section 80C benefit.

For retirees who continue under the old regime, SCSS can help utilize part or all of the annual ₹1.5 lakh deduction limit.

For example:

- If you invest ₹1.5 lakh or more into SCSS during a financial year, you can potentially claim the full ₹1.5 lakh Section 80C deduction.

- A senior citizen in the 20% tax bracket could save approximately ₹30,000 in tax (before cess) through this deduction alone.

Additional details regarding Section 80C deductions are available here.

One point that often causes confusion is the difference between the deposit and the interest.

The Section 80C deduction applies only to the amount invested in the year of deposit. It does not apply to the interest earned in future years.

For instance, if you invest ₹30 lakh into SCSS in FY 2026–27, your deduction is still capped at ₹1.5 lakh. The deduction does not increase simply because the investment amount is larger.

Is SCSS Interest Taxable?

Yes.

This is arguably the most important tax rule investors should understand before opening an SCSS account.

Unlike products such as PPF or Sukanya Samriddhi Yojana, where interest enjoys tax-free treatment, SCSS interest is fully taxable. Every quarterly interest payment must be reported as “Income from Other Sources” when filing your income tax return.

The amount is taxed according to your applicable income tax slab.

That said, senior citizens do receive some relief through Section 80TTB.

According to Clear Tax, Section 80TTB allows eligible senior citizens to claim a deduction of up to ₹50,000 per year on interest income earned from eligible deposits, including SCSS, bank fixed deposits, and certain post office deposits.

A couple of examples make this easier to understand:

- A senior citizen who earns ₹49,200 annually from SCSS interest may effectively pay no tax on that interest if they have no other eligible interest income, since it falls within the ₹50,000 Section 80TTB deduction limit.

- A senior citizen earning ₹2,46,000 annually from a ₹30 lakh SCSS investment can claim the ₹50,000 deduction, leaving ₹1,96,000 subject to taxation at their applicable slab rate.

The deduction helps, but it doesn’t make SCSS interest tax-free.

TDS Rules on SCSS Interest

Another area where investors frequently have questions is TDS (Tax Deducted at Source).

Banks and post offices are required to deduct TDS at 10% if the annual interest earned from SCSS exceeds ₹50,000 during a financial year.

The rules generally work as follows:

- Annual interest up to ₹50,000: No TDS deduction.

- Annual interest above ₹50,000: TDS may be deducted at the applicable rate.

- Eligible senior citizens with taxable income below the applicable threshold can submit Form 15H to request that TDS not be deducted.

Submitting Form 15H does not eliminate the obligation to report income. It simply prevents tax from being deducted upfront when your overall income remains below taxable limits.

Many retirees submit Form 15H at the beginning of each financial year to avoid unnecessary TDS deductions and subsequent refund claims.

Senior Citizen Tax Slabs and SCSS Income

The actual tax payable on SCSS interest depends on your total income, not just the interest earned from the scheme.

Under the old tax regime, senior citizens enjoy higher basic exemption limits than non-senior taxpayers.

As referenced at in this guide:

- Senior citizens aged 60–80 years have a basic exemption limit of ₹3 lakh.

- Super senior citizens aged above 80 years have a basic exemption limit of ₹5 lakh.

Because of these higher thresholds, many retirees with modest pension income and limited investment earnings may end up paying little or no tax on their SCSS interest after accounting for exemptions and deductions.

The key takeaway is simple: SCSS offers useful tax benefits, but it should not be viewed as a tax-free investment. The deposit may qualify for Section 80C (under the old regime), and interest may benefit from Section 80TTB, yet the interest itself remains taxable income and should be factored into retirement planning calculations.

Disadvantages of Senior Citizen Savings Scheme

No financial product is perfect, and SCSS is no exception.

While it remains one of the strongest retirement-oriented savings options available in India, it also comes with limitations that deserve careful consideration. Understanding these drawbacks upfront helps ensure that expectations remain realistic and that the scheme is used for the purpose it was designed for.

1. Interest Is Taxable

Perhaps the biggest drawback of SCSS is that the interest earned is fully taxable.

Many retirees assume that because SCSS is a government-backed scheme, the interest must be tax-free. Unfortunately, that’s not the case.

Unlike PPF, where both the investment growth and maturity proceeds enjoy tax-free treatment, SCSS interest is taxed according to your income tax slab.

For retirees in higher tax brackets, this can significantly reduce the effective return.

Consider a senior citizen who invests the maximum ₹30 lakh and earns ₹2,46,000 annually in interest. After claiming the ₹50,000 deduction available under Section 80TTB, the remaining ₹1,96,000 becomes taxable. For someone in the 30% tax bracket, that translates into a substantial tax liability that lowers the effective post-tax yield.

The headline rate may be 8.2%, but your actual take-home return could be noticeably lower depending on your tax situation.

2. No Compounding Benefit

SCSS is structured as an income-generating scheme rather than a wealth-building product.

The quarterly interest is paid out directly to your linked savings account and is not automatically reinvested into the scheme. As a result, the principal remains unchanged throughout the tenure.

For retirees who need regular income, this design works perfectly.

However, investors seeking long-term compounding may find it limiting. Products such as PPF, certain fixed deposits, or reinvested debt instruments can potentially grow a corpus more effectively because earnings remain invested rather than being distributed.

In simple terms, SCSS helps generate cash flow. It is not designed to maximize long-term wealth accumulation.

3. Limited Liquidity During the Tenure

Although premature closure is allowed, SCSS is not particularly flexible when compared with savings accounts, liquid funds, or short-term deposits.

The scheme is built around a five-year commitment. Withdrawing funds before maturity triggers penalties, and the process is less convenient than redeeming a mutual fund or breaking a standard bank deposit.

This doesn’t make SCSS unsuitable; it simply means that money invested here should ideally be money you won’t need immediately.

For this reason, many financial planners recommend keeping a separate emergency fund rather than relying on SCSS for unexpected expenses.

4. No Additional Contributions After Opening

One of the less-discussed limitations of SCSS is that it accepts only a one-time lump-sum investment.

Once the account has been opened and funded, you cannot continue adding money to it.

This differs from products such as:

- Public Provident Fund (PPF)

- Recurring Deposits (RDs)

- Systematic investment plans (SIPs)

- Certain pension-oriented savings products

Retirees who receive periodic pension income and wish to invest gradually may find this restriction inconvenient.

The investment decision has to be made upfront, and the amount remains fixed throughout the tenure.

5. Deposit Limit of ₹30 Lakh Per Person

The increase in the maximum investment limit from ₹15 lakh to ₹30 lakh was a major improvement. Even so, the cap remains a limitation for retirees with larger retirement corpora.

For example, someone retiring with ₹1 crore, ₹2 crore, or more cannot place the entire amount into SCSS.

While a married couple can collectively invest up to ₹60 lakh through separate accounts, larger portfolios will still require additional investment avenues such as:

- RBI Floating Rate Savings Bonds

- Bank fixed deposits

- Post office schemes

- Debt mutual funds

- Other retirement-oriented investments

SCSS works extremely well as a foundation, but it is rarely the only solution for high-net-worth retirees.

6. Interest Rate Risk at Extension

One of SCSS’s biggest strengths is that the interest rate is locked in for the original five-year tenure.

However, that protection does not extend to the optional three-year extension period.

If you choose to extend the account, the new rate will be whatever the government has notified at that time.

This introduces an element of uncertainty.

Today’s 8.2% rate may look attractive, but nobody can predict where interest rates will stand five years from now. If rates are lower when the extension begins, your quarterly income could decline accordingly.

For retirees who are building long-term income projections, this is an important detail to keep in mind.

7. Administrative and Operational Hassles

Although service standards have improved significantly in recent years, SCSS is still more paperwork-heavy than many modern investment platforms.

Depending on the institution, account opening, nomination updates, extensions, and certain service requests may require branch visits and physical documentation.

This is rarely a deal-breaker, but it can be frustrating for seniors who prefer entirely digital financial management.

Post offices in particular have made progress with online services, yet many transactions still involve some level of in-person interaction.

The Bottom Line

None of these disadvantages are severe enough to outweigh the scheme’s core strengths for most retirees.

In fact, many of these “drawbacks” exist because SCSS was designed with a very specific objective: preserving capital and providing predictable income.

If your primary goal is safety, government backing, and reliable quarterly cash flow, SCSS remains difficult to beat.

But if you need high liquidity, tax-free growth, unlimited investment capacity, or long-term compounding, you’ll almost certainly need to complement SCSS with other financial products rather than rely on it exclusively.

Alternatives: Which is Better, SCSS or FD for Senior Citizens?

Choosing between SCSS and a senior citizen fixed deposit is one of the most common decisions retirees face after receiving retirement benefits.

At first glance, the two products appear quite similar. Both are relatively low-risk, both generate regular income, and both are widely available through banks. But once you look beyond the surface, some important differences emerge.

For many retirees, the choice isn’t necessarily SCSS or FD. It’s often a question of which one should come first.

SCSS vs. Senior Citizen Bank FDs

Here’s a side-by-side comparison of the key features:

| Parameter | SCSS | Senior Citizen Bank FD |

| Interest Rate (2026) | 8.2% | 7.0%–7.75% (typical range) |

| Safety | Sovereign guarantee (Government of India) | DICGC insurance up to ₹5 lakh per bank |

| Interest Payout | Quarterly only | Monthly, quarterly, or cumulative options |

| Maximum Deposit | ₹30 lakh per person | No statutory limit |

| Tenure | 5 years (extendable once by 3 years) | Flexible: 7 days to 10 years |

| Premature Withdrawal | Allowed with penalty | Allowed with penalty |

| Section 80C Benefit | Yes (subject to limits) | Only for eligible tax-saving FDs |

| Tax on Interest | Taxable; Section 80TTB applicable | Taxable; Section 80TTB applicable |

The biggest advantage SCSS currently holds is its interest rate.

At 8.2%, it comfortably exceeds the rates offered by most senior citizen fixed deposits. Even a difference of 0.75% to 1% can have a meaningful impact when large retirement sums are involved.

Take a ₹30 lakh investment as an example.

At 8.2%, SCSS generates ₹2,46,000 annually in interest.

A comparable FD paying 7.5% generates ₹2,25,000 annually.

That’s a difference of ₹21,000 every year. Over a five-year period, the gap widens to ₹1,05,000 without taking compounding effects into account.

For retirees depending on investment income, that additional cash flow can make a noticeable difference.

The Safety Advantage

Returns matter, but safety often matters even more after retirement.

This is where SCSS enjoys another significant edge.

Bank fixed deposits are protected by DICGC insurance only up to ₹5 lakh per depositor per bank. While bank failures are rare, the insurance ceiling is something investors with large deposits should understand.

SCSS, on the other hand, carries sovereign backing from the Government of India.

That means both principal and interest are backed by the government, regardless of the amount invested within the scheme’s limits.

For retirees who prioritize capital preservation above everything else, that additional layer of security is often a deciding factor.

When a Fixed Deposit Might Be Better

Despite SCSS’s advantages, there are situations where a fixed deposit may be the more suitable option.

For example:

- You need monthly income rather than quarterly payouts.

- You want the flexibility to choose shorter or longer tenures.

- You may need access to funds before five years.

- Your retirement corpus exceeds the SCSS investment limit.

- You prefer cumulative growth instead of regular payouts.

Fixed deposits offer more flexibility in terms of tenure and payout structure, which can be useful depending on individual retirement goals.

This is why many retirees ultimately use both products rather than choosing one exclusively.

Which Bank Gives 9.5% Interest on FD for Senior Citizens?

This is another question that frequently appears in retirement planning discussions.

As of mid-2026, no major scheduled commercial bank is offering a standard senior citizen fixed deposit rate of 9.5%.

While some cooperative banks, small finance banks, or NBFCs occasionally advertise rates approaching 9% or higher, those higher returns generally come with higher risk.

Details of historical FD rates can be viewed here.

A useful rule of thumb is this: when an institution is offering a rate significantly above prevailing market rates, it’s worth asking why.

Higher returns are rarely free. They are often compensation for taking additional credit risk, liquidity risk, or institutional risk.

For retirees whose primary objective is protecting their retirement corpus, sacrificing some safety for an extra percentage point of yield may not always be a wise trade-off.

That’s one of the reasons SCSS continues to attract so much interest despite not having the highest advertised return in the market.

Post Office Monthly Income Scheme for Senior Citizens (POMIS)

Another alternative worth considering is the Post Office Monthly Income Scheme (POMIS).

Both SCSS and POMIS belong to the government-backed small savings ecosystem, but they serve slightly different purposes.

| Parameter | SCSS | POMIS |

| Interest Rate | 8.2% p.a. | 7.4% p.a. |

| Payout Frequency | Quarterly | Monthly |

| Maximum Deposit | ₹30 lakh (single) / ₹60 lakh (couple) | ₹9 lakh (single) / ₹15 lakh (joint) |

| Section 80C Benefit | Yes | No |

| Tenure | 5 years | 5 years |

| Primary Objective | Higher return and quarterly income | Monthly cash flow |

The biggest advantage of POMIS is right there in its name. It pays every month.

For retirees who rely heavily on investment income to cover routine expenses such as groceries, utility bills, and medical costs, monthly payouts can feel more practical than waiting for quarterly credits.

The trade-off is a lower interest rate and lower investment limits.

As a result, many financial planners recommend using both schemes together rather than treating them as competitors.

A common approach is:

- Maximize SCSS first to benefit from the higher 8.2% rate.

- Use POMIS alongside it to create a smoother monthly income stream.

Additional information about POMIS and related schemes can be found in Clear Tax and on India Post’s official savings page.

Best Saving Scheme for Senior Citizens

When viewed purely through the lens of safety, income generation, and ease of use, SCSS remains difficult to displace.

For most retirees in India, a practical priority order often looks like this:

First: SCSS

The combination of an 8.2% return, sovereign backing, quarterly income, and Section 80C eligibility makes SCSS the natural starting point for retirement income planning.

Second: POMIS

Ideal for retirees who want additional monthly cash flow alongside SCSS.

Third: RBI Floating Rate Savings Bonds (FRSB)

Currently offering attractive rates with no upper investment limit, making them useful once SCSS limits are exhausted.

Fourth: Senior Citizen Fixed Deposits

Useful for diversification, shorter-term needs, and flexible payout options.

Fifth: Liquid Funds and Short-Term Debt Funds

Suitable for emergency reserves and money that may be needed within the next few years.

Further retirement planning resources are available here

The key takeaway is simple.

SCSS is rarely the only retirement product you should own, but for many retirees, it remains the first one worth considering. Once that foundation is in place, other products can be layered on top to address liquidity needs, monthly cash flow requirements, and long-term diversification.

How Much Money Can a Senior Citizen Have in the Bank in India?

A common misconception among retirees is that there must be some legal limit on how much money a senior citizen can keep in a bank account or fixed deposit. In reality, no such limit exists.

Whether you have ₹10 lakh, ₹50 lakh, ₹1 crore, or even more, Indian law does not impose a ceiling on the amount you can hold in bank accounts, fixed deposits, or similar banking products. Large balances are perfectly legal, provided the source of funds is legitimate and income is reported correctly in your tax returns.

Where many people get caught out is not on the question of ownership, but on the question of protection.

Just because you can keep a large amount with a bank does not mean all of it is guaranteed if something goes wrong.

This is where the Deposit Insurance and Credit Guarantee Corporation (DICGC) becomes important. DICGC insurance covers savings accounts, fixed deposits, recurring deposits, and other eligible bank deposits up to ₹5 lakh per depositor per bank.

To put that into perspective:

- If you have ₹5 lakh in a bank, the entire amount is covered.

- If you have ₹30 lakh in a single bank FD, only ₹5 lakh falls within the insurance cover.

For retirees who have spent decades building their retirement corpus, that is a detail worth paying attention to.

This is one of the strongest arguments in favour of SCSS as a core retirement income product. Unlike a bank FD, an SCSS deposit carries the backing of the Government of India. The protection is not limited to the first ₹5 lakh. The full amount invested under the scheme’s limits is supported by a sovereign guarantee.

For someone investing ₹30 lakh in SCSS, that distinction can provide a significant degree of comfort. The objective after retirement is not only earning income but also preserving capital, and government-backed schemes tend to rank highly on that front.

For retirees whose savings exceed the ₹30 lakh SCSS limit, a sensible strategy is often to combine multiple instruments rather than relying on a single one. This may involve spreading deposits across different banks, using sovereign-backed products such as RBI Floating Rate Savings Bonds, considering the Post Office Monthly Income Scheme, or continuing contributions to eligible long-term savings products.

The underlying principle is simple: build a retirement portfolio where as much of your money as possible sits within established protection frameworks, whether through government guarantees or deposit insurance.

Can NRIs Open an SCSS Account?

No, Non-Resident Indians (NRIs) cannot open a new SCSS account.

This restriction is built into the Senior Citizen Savings Scheme rules and remains one of the core eligibility requirements. SCSS is intended specifically for resident Indians, so NRI status at the time of application makes an individual ineligible to open a fresh account.

Where things get slightly more nuanced is when someone becomes an NRI after already opening an SCSS account.

In many cases, accounts that were opened while the individual was a resident Indian are allowed to continue until maturity. Since the account was opened legally under the prevailing eligibility rules, institutions generally permit it to run its course rather than forcing immediate closure.

That said, there is an important distinction between continuing an existing account and opening a new one.

An individual who has become an NRI is typically not permitted to:

- Open a new SCSS account.

- Make fresh deposits into the scheme.

- Open additional SCSS accounts after acquiring NRI status.

If an NRI later returns to India and re-establishes resident status, they may become eligible again, provided they satisfy the scheme’s age and residency requirements at that time.

As with many banking and small-savings matters, administrative procedures can vary slightly between institutions. If your residency status has changed recently or is likely to change soon, it is worth speaking directly with your bank or post office branch before making any decisions.

For most retirees residing in India, this rule has little practical impact. But for those who split their time between countries or plan to relocate after retirement, understanding the residency requirement upfront can help avoid confusion later.

Can I Open Multiple SCSS Accounts?

Yes, you can open more than one SCSS account.

This often surprises people because many assume the scheme restricts investors to a single account. In reality, the rules allow you to maintain multiple SCSS accounts across different institutions if you wish.

For example, you could:

- Open one account at a post office.

- Open another at SBI or another authorized bank.

- Split your investment between different locations for convenience.

The key point to remember is that the investment limit applies to the individual, not to each account.

In other words, while multiple accounts are permitted, the total amount invested across all your SCSS accounts cannot exceed the overall limit of ₹30 lakh per person.

Think of it this way: the government tracks your cumulative SCSS investment, not the number of accounts you hold.

Some retirees deliberately split their investments between two accounts for practical reasons. A person who spends part of the year in one city and part in another may prefer to maintain accounts closer to both locations. Others do it for administrative convenience, estate planning considerations, or simply because they already have relationships with different institutions.

Fortunately, there is no interest rate disadvantage to taking this approach. Whether your ₹30 lakh is held in one account or spread across multiple accounts, the applicable SCSS interest rate remains the same.

That said, transparency is important.

When opening an additional SCSS account, you should disclose any existing SCSS holdings. Banks and post offices are expected to verify that your combined deposits remain within the permitted limit. Exceeding the ceiling, even unintentionally, can create complications later.

For most retirees, maintaining a single account is often the simplest option. But if there is a genuine operational reason to split investments, the scheme allows enough flexibility to do so without sacrificing any of its benefits.

What Happens If I Forget to Extend My SCSS Account at Maturity?

Five years can pass surprisingly quickly.

Many retirees diligently track their quarterly interest credits but pay far less attention to the account’s maturity date. Unfortunately, overlooking that date can be an expensive mistake.

If you wish to continue your SCSS account beyond its initial five-year tenure, you must submit Form B (the extension request form) within one year of the maturity date.

The extension is not automatic.

This is where some investors get caught out. They assume the account will simply roll over into another term at the prevailing rate. That’s not how SCSS works.

If no extension request is submitted within the permitted window, the account effectively becomes a matured account. The principal remains with the institution until you withdraw it, but it no longer enjoys the benefits of the SCSS interest rate.

In practical terms, that can mean a significant drop in earnings.

Depending on the institution and prevailing rules, the balance may earn only the Post Office Savings Account rate or another much lower rate until the funds are withdrawn. Either way, it is unlikely to come close to the 8.2% return you were previously receiving.

For retirees who rely on SCSS as part of their income strategy, that reduction can have a noticeable impact.

There’s another point worth remembering.

Even if you decide to extend the account, the extension period does not automatically carry the same interest rate that you originally locked in. The rate applicable to the extension will be the SCSS rate in force at the time the extension is approved.

That means:

- If rates have risen, you could benefit.

- If rates have fallen, your future income may be lower.

Because of this, it’s wise to review your options shortly before maturity rather than waiting until the last minute.

A simple solution is to set multiple reminders:

- One reminder six months before maturity.

- Another three months before maturity.

- A final reminder on the maturity date itself.

Most retirees spend years carefully building their retirement corpus. Losing interest income because of a missed administrative deadline is one of the easiest mistakes to avoid.

The good news is that the extension window is fairly generous. As long as you act within one year of maturity and complete the required paperwork, you can continue benefiting from the scheme without disruption.

Is SCSS Available Online?

The short answer is: partially, but not completely.

Over the last few years, both India Post and major banks have made noticeable progress in digitizing SCSS-related services. As a result, existing account holders can now perform many routine tasks online that previously required a branch visit.

However, SCSS still isn’t a fully digital product in the way that mutual funds, online fixed deposits, or stock market investments are.

What Can Be Done Online?

If your SCSS account is already active, several institutions allow you to access account information digitally.

For example, India Post has expanded its online banking services through India Post, enabling account holders to:

- Check account balances.

- View passbook entries.

- Track quarterly interest credits.

- Access selected account services online.

Similarly, banks such as SBI offer visibility through platforms like YONO and internet banking, allowing customers to monitor their SCSS accounts without visiting a branch.

For many retirees, this is a significant improvement. Quarterly interest payments can be verified from home, statements can be reviewed online, and account activity becomes much easier to track.

Can I Open an SCSS Account Online?

In most cases, no.

As of 2026, opening a new SCSS account generally requires an in-person visit to a post office or authorized bank branch.

The reason is largely regulatory.

Before an account can be opened, institutions must complete Know Your Customer (KYC) verification, confirm age eligibility, verify original documents, obtain signatures on the application forms, and validate details relating to retirement benefits where applicable.

These requirements still make physical verification the preferred process for most institutions.

While digital banking has advanced considerably, SCSS account opening remains one of the areas where paperwork and in-person verification continue to play an important role.

What If Mobility Is a Concern?

For some senior citizens, travelling to a branch can be inconvenient or difficult.

Fortunately, many institutions are becoming more accommodating.

Some banks offer:

- Prior appointment scheduling.

- Assisted account-opening services.

- Doorstep banking support in select locations.

- Dedicated senior citizen service desks.

SBI, for example, operates doorstep banking services in certain areas, which can be particularly helpful for elderly customers with mobility challenges.

If visiting a branch is difficult, it is worth calling ahead to ask what assistance may be available. A five-minute phone call can often save an unnecessary trip.

A Practical Tip Before Visiting

One of the most common reasons retirees end up making multiple visits is missing documentation.

Before heading to the branch, confirm:

- Which documents are required.

- Whether photocopies are needed.

- Whether photographs must be carried.

- Whether an appointment is recommended.

- What payment methods are accepted for the deposit.

A little preparation usually turns the entire process into a single visit.

The Bottom Line

SCSS has become far more digital than it was a decade ago, particularly when it comes to monitoring accounts and tracking interest payments.

However, fresh account opening still remains largely branch-based.

For most retirees, this is a minor inconvenience rather than a major drawback. Once the account is opened, ongoing management is relatively straightforward, and many routine tasks can now be handled online without repeatedly visiting the bank or post office.

What Is the Nomination Process for SCSS?

Of all the forms you’ll fill out when opening an SCSS account, nomination is probably the one that’s easiest to overlook and arguably the most important.

Most retirees focus on the deposit amount, interest rate, and quarterly payouts. That’s understandable. Yet a properly completed nomination can save family members months of paperwork and unnecessary stress in the future.

The good news is that setting up a nomination is simple.

Adding a Nominee at the Time of Account Opening

The easiest approach is to nominate someone when you open the account.

The SCSS application form includes a dedicated section where you can provide the nominee’s details, including:

- Name

- Relationship to the account holder

- Address

- Date of birth (where applicable)

The entire process usually takes just a few minutes, and there is no additional fee for adding a nominee.

For most people, this is a straightforward box to tick during account opening. But its importance becomes clear only when families are forced to deal with an account after the holder’s death.

Can You Add a Nominee Later?

Yes.

If you skipped nomination when opening the account or simply want to update it later, you can do so by submitting Form SC-2 at your bank or post office.

Life circumstances change. Families change. Relationships evolve.

The rules recognize this, which is why nomination details can be updated during the tenure of the account rather than being locked in permanently.

Who Can Be a Nominee?

SCSS rules are relatively flexible on this front.

Many account holders nominate:

- A spouse

- One or more children

- A sibling

- Another trusted family member

The nominee does not need to be a joint account holder.

The purpose of nomination is simply to identify the person entitled to claim the account proceeds if the account holder passes away.

Why Nomination Matters More Than Most People Realize

When a valid nomination exists, the claim process is usually straightforward.

In the unfortunate event of the account holder’s death, the nominee can typically approach the bank or post office with:

- The SCSS passbook

- Death certificate

- Identity proof

- Any additional documents requested by the institution

After verification, the principal amount and any eligible accrued interest can be released without a lengthy legal process.

For grieving family members, that simplicity can make an enormous difference.

What Happens If No Nomination Exists?

This is where things become considerably more complicated.

Without a valid nominee, legal heirs may need to establish their claim through succession-related legal procedures. Depending on the circumstances, this can involve:

- Additional documentation

- Legal heir certificates

- Succession certificates

- Court-related formalities

The process can take months and, in some cases, considerably longer.

Meanwhile, the funds remain inaccessible.

It’s one of those administrative issues that feels unimportant until the day it suddenly becomes very important.

A Small Step That Protects Your Family

Most retirement planning discussions focus on maximizing returns. Nomination is different.

It doesn’t increase your interest rate.

It doesn’t improve your tax benefits.

It doesn’t change your maturity value.

What it does is ensure that the money you’ve worked a lifetime to accumulate can be transferred to your chosen beneficiary with the least possible friction.

For that reason alone, nomination should be treated as a non-negotiable part of opening an SCSS account, not an optional formality to deal with later.

Does SCSS Interest Count Toward Income for Tax Filing Purposes?

Yes. Every rupee of interest earned from an SCSS account counts as taxable income and must be reported when filing your Income Tax Return (ITR).

This is one of the most misunderstood aspects of the scheme.

Many retirees assume that because SCSS is government-backed, the interest must be tax-free. Others believe that if no TDS was deducted, there is no need to report the income. Neither assumption is correct.

SCSS interest is taxable and should be declared under “Income from Other Sources” in your tax return.

How SCSS Interest Is Taxed

Unlike products such as PPF, where interest enjoys tax-exempt status, SCSS interest is added to your total taxable income for the financial year.

Every quarterly interest payment credited to your savings account forms part of your annual income.

This means the actual tax payable depends on:

- Your total income from all sources.

- Your chosen tax regime.

- Applicable deductions and exemptions.

- Your income tax slab.

For some retirees, the tax impact may be minimal. For others, particularly those with pension income, rental income, or large investments, the tax liability can be more significant.

Understanding TDS on SCSS Interest

Banks and post offices track the total interest earned on your SCSS account during the financial year.

If the annual interest crosses the prescribed threshold, TDS may be deducted before the interest is credited.

When TDS is deducted:

- The institution issues Form 16A.

- The deducted amount appears in your tax records.

- You can claim credit for the TDS while filing your ITR.

However, it’s important to understand that TDS is not the tax itself. It is merely an advance collection mechanism.

Many people confuse the two.

Even if TDS has been deducted, you must still report the full gross interest income while filing your return. The TDS amount is then adjusted against your final tax liability.

What If No TDS Is Deducted?

The reporting requirement does not disappear.

You are still required to declare SCSS interest even if:

- No TDS was deducted.

- You submitted Form 15H.

- Your income is below the taxable threshold.

- The interest amount is relatively small.

This is where many taxpayers make mistakes.

The absence of TDS does not mean the income becomes invisible for tax purposes. It simply means no tax was collected upfront.

How Section 80TTB Helps Senior Citizens

Senior citizens do receive some relief through Section 80TTB.

Under this provision, eligible senior citizens can claim a deduction of up to ₹50,000 on interest income from eligible deposits, including:

- SCSS accounts

- Bank fixed deposits

- Savings accounts

- Certain post office deposits

The deduction reduces taxable income, but it does not eliminate the requirement to report the interest in the first place.

A simple way to think about it is:

- Declare the gross interest income.

- Claim the eligible Section 80TTB deduction.

- Pay tax, if any, on the remaining amount.

Why Keeping Records Matters

Because SCSS pays interest quarterly, many retirees underestimate how much interest they receive over an entire year.

A practical habit is to maintain a simple record of:

- Quarterly interest credits.

- TDS deductions (if any).

- Form 16A issued by the bank or post office.

Doing this throughout the year makes tax filing much easier than trying to reconstruct everything at the last minute.

The Key Takeaway

SCSS interest is not tax-free.

Every quarterly interest payment forms part of your taxable income and must be reported in your Income Tax Return under “Income from Other Sources.” Deductions such as Section 80TTB can reduce the tax burden, but they do not remove the obligation to disclose the income.

For most retirees, a little record-keeping throughout the year is enough to make the entire process straightforward and stress-free.

Can a Retired Defence Person Open SCSS at Age 52?

Yes.

Retired defence personnel are one of the few groups permitted to open an SCSS account before the standard age of 60. In fact, eligible defence retirees can open an account from the age of 50 onwards, provided they meet the scheme’s other conditions.

This exception exists for a practical reason.

Unlike most civilian employees, many members of the armed forces complete their service careers much earlier. It is not unusual for defence personnel to retire in their late 40s or early 50s after fulfilling their service obligations. Recognizing this, the Government created a separate eligibility category so that retired servicemen are not excluded from retirement-focused savings benefits simply because they retire earlier than the general population.

Who Qualifies?

The provision applies to retired defence personnel, excluding Civil Defence employees.

To qualify, an individual must:

- Be at least 50 years of age.

- Have retired from defence service.

- Open the SCSS account within one month of receiving retirement benefits.

- Ensure that the deposit amount does not exceed the retirement benefits received.

These retirement benefits may include:

- Gratuity

- Provident fund proceeds

- Leave encashment

- Commuted pension amounts

- Other eligible retirement payments

The government introduced these conditions to ensure that SCSS serves its intended purpose: helping retirees deploy their retirement corpus into a secure income-generating instrument.

A Practical Example

Consider a retired Army Subedar who leaves service at age 52 and receives ₹18 lakh in retirement benefits.

Provided the account is opened within the prescribed time window, that individual can invest up to ₹18 lakh in SCSS immediately, even though they have not yet reached age 60.

This allows retired defence personnel to begin earning regular quarterly income from their retirement savings without waiting several years to satisfy the standard age requirement.

Documents Typically Required

In addition to the standard SCSS documentation, defence retirees should be prepared to provide evidence of their retirement status.

This may include:

- Retirement order

- Discharge certificate

- Pension sanction documents

- Other official retirement records

Along with these, the usual KYC documents are required:

- Aadhaar card

- PAN card

- Passport-size photographs

- Linked bank account details

- Deposit instrument or transfer proof

Carrying all documents during the initial visit can help avoid delays and repeat trips to the branch.

Why This Provision Matters

For many defence personnel, retirement arrives much earlier than it does for civilian employees.

Without this special provision, a retired serviceman could potentially spend years holding retirement funds in lower-yielding savings products while waiting to become eligible for SCSS.

The defence exemption closes that gap.

It allows eligible retirees to access one of India’s safest and most popular retirement-income schemes at the point when they actually retire, rather than at a later age.

The Bottom Line

A retired defence person aged 52 can absolutely open an SCSS account, provided the account is opened within the prescribed time frame after retirement and the investment amount does not exceed the retirement benefits received.

For many former service personnel, this early-access provision makes SCSS one of the most effective tools available for turning retirement benefits into a reliable, government-backed income stream.

How Is the SCSS Interest Rate Decided?

One of the reasons SCSS attracts so much attention from retirees is its relatively high interest rate. Naturally, that leads to an important question: who decides the rate, and how is it calculated?

The answer lies with the Ministry of Finance.

The interest rate on the Senior Citizen Savings Scheme is determined by the Department of Economic Affairs under the Ministry of Finance, which reviews small savings scheme rates every quarter. These reviews typically take place before the start of each quarter, and the updated rates are announced through official notifications.

What Influences the SCSS Interest Rate?

SCSS rates are not chosen randomly.

The government generally uses yields on Government of India securities as the benchmark. Since SCSS is a government-backed savings scheme, it is designed to move broadly in line with prevailing interest-rate conditions in the economy.

In simple terms:

- When government bond yields rise, SCSS rates have the potential to move higher.

- When bond yields fall, SCSS rates may also come down over time.

To make SCSS attractive for retirees, the government typically provides a positive spread above comparable government security yields. This additional margin helps ensure that senior citizens receive a competitive return without taking on investment risk.

Why Has the Rate Stayed at 8.2% for So Long?

One notable feature of the current SCSS environment is the unusual stability of the rate.

The scheme has remained at 8.2% per annum since April 2023, making it one of the longest periods of rate stability in recent years.

Several factors may have contributed to this:

- Relatively stable interest-rate conditions.

- Government efforts to support senior citizen savings.

- The importance of predictable retirement income for retirees.

While no one can predict future rate movements with certainty, the extended period at 8.2% has provided retirees with a level of consistency that is uncommon in many fixed-income products.

The Most Important Feature: Rate Lock-In

This is where SCSS differs from many other savings products.

Although the government reviews rates every quarter, those changes affect only new investors.

Once you open an SCSS account, the interest rate applicable on the date of opening is locked in for the entire five-year tenure.

That means:

- If you open at 8.2%, you continue earning 8.2%.

- Future rate cuts do not affect your account.

- Future rate increases do not benefit your account either.

For retirees who value certainty, this feature is enormously valuable.

You know exactly what income to expect for the next five years, regardless of what happens to interest rates in the broader economy.

What About the Three-Year Extension?

The lock-in protection applies only to the original five-year term.

If you choose to extend the account for the optional three-year period, the interest rate will reset to whatever SCSS rate is in force at the time of extension.

This introduces an element of uncertainty.

Five years from now:

- Rates may be higher.

- Rates may be lower.

- Rates may be broadly unchanged.

Nobody knows.

As a result, retirees planning long-term income should think of the extension period as a new investment decision rather than an automatic continuation of the original account.

Why the Rate-Setting Process Matters

Understanding how SCSS rates are determined helps explain why the scheme has remained so popular.

The rate is not tied to a particular bank’s business strategy. It is not influenced by promotional campaigns or temporary offers. Instead, it is linked to broader government borrowing costs and reviewed through an established framework.

For retirees, that translates into a rare combination:

- Competitive returns.

- Government backing.

- Predictable income.

- Protection from future rate cuts after account opening.

The Bottom Line

The Ministry of Finance reviews SCSS rates every quarter using government security yields as the primary benchmark. While rates can rise or fall for new investors, existing account holders enjoy a valuable benefit: the rate they receive at account opening remains fixed for the entire five-year tenure.

For many retirees, that certainty is just as important as the interest rate itself. After all, retirement planning becomes much easier when you know exactly how much income your savings will generate year after year.

What If the First SCSS Account Holder Dies During the Tenure?

It’s not a topic anyone likes to think about, but it is an important one.

One of the questions families often ask is what happens to an SCSS account if the primary account holder passes away before the account reaches maturity. Fortunately, the scheme has clear provisions in place to protect both the investment and the beneficiaries.

What happens next depends largely on how the account was structured when it was opened.

If the Account Is Held Jointly

In a joint SCSS account, the process is usually straightforward.

If the primary account holder dies during the tenure, the surviving joint holder can generally continue the account until maturity under the existing terms. The account does not need to be closed and reopened, and the original interest rate continues to apply.

From an operational perspective, this is the smoothest outcome because the account already contains a recognized secondary holder.

The surviving holder continues receiving the benefits of the scheme and can claim the principal amount when the account matures.

If the Account Is in a Single Name With a Nominee

This is the next-best scenario.

When a valid nomination has been registered, the nominee can approach the bank or post office with the required documents, which typically include:

- The SCSS passbook

- Death certificate of the account holder

- Identity proof of the nominee

- Any additional forms requested by the institution

Once the claim is processed, the nominee becomes entitled to receive the principal amount along with any eligible accrued interest.

While some paperwork is unavoidable, the process is usually far quicker and less stressful than situations where no nomination exists.

This is precisely why nomination should never be treated as an optional administrative step.

A Crucial Benefit: No Premature Closure Penalty

There is another important protection built into the scheme.

Normally, closing an SCSS account before maturity can attract penalties depending on how long the account has been active.

However, when closure occurs because of the account holder’s death, those standard premature-withdrawal penalties do not apply.

The beneficiary is entitled to:

- The full principal amount.

- Interest accrued up to the date of death.

- Payment without the usual premature-withdrawal deductions.

For families already dealing with a difficult situation, this provision provides valuable financial protection.

What If There Is No Nominee and No Joint Holder?

This is where complications begin.

Without a joint holder or registered nominee, legal heirs must establish their entitlement through formal legal processes before the institution can release the funds.

Depending on the circumstances, this may involve:

- Legal heir documentation.

- Succession certificates.

- Court procedures.

- Additional verification requirements.

The process can take months and sometimes considerably longer.

During that period, access to the funds may remain restricted.

This is why financial advisors routinely emphasize the importance of setting up a nomination on day one rather than postponing it indefinitely.

Why Planning Ahead Matters

Most people spend a great deal of time deciding where to invest their retirement corpus. Far fewer spend time thinking about what happens if something happens to them.

Yet a properly structured account, with either a joint holder, a nominee, or both, can spare family members a significant amount of stress during an already emotional period.

A few minutes spent completing nomination paperwork today can save months of administrative difficulties later.

The Bottom Line

If the first SCSS account holder dies during the tenure, the treatment depends on the account structure. Joint holders can generally continue the account, while nominees can claim the principal and accrued interest through a relatively straightforward process.

Most importantly, death-related closure does not attract the usual premature-withdrawal penalties, ensuring that beneficiaries receive the full value of the investment. For that reason alone, maintaining updated nomination details should be considered an essential part of managing an SCSS account.

Can I Open an SCSS Account for My Parent?

This is a question that comes up quite often, especially when adult children are helping their parents organize retirement finances.

The short answer is: no, you cannot open an SCSS account in your own capacity on behalf of your parent.

The account must be opened in the name of the eligible senior citizen who meets the scheme’s age and residency requirements.

In other words, even if you are providing the funds or handling the paperwork, the account holder must be your parent, not you.

Why the Account Must Be Opened by the Eligible Individual

SCSS is designed as an individual retirement savings scheme. The eligibility conditions, tax treatment, interest income, and ownership rights all belong to the person whose name appears on the account.

Because of that, banks and post offices require the eligible senior citizen to:

- Complete the application.

- Meet the age criteria.

- Submit the required KYC documents.

- Sign the necessary forms.

The account cannot simply be opened by a son, daughter, or other relative acting independently.

How You Can Help Your Parent

While you cannot open the account in your own name for them, you can absolutely assist throughout the process.

In practice, many families handle SCSS applications this way.

You can help by:

- Gathering Aadhaar, PAN, and other required documents.

- Completing portions of the application form.

- Accompanying your parent to the bank or post office.

- Arranging the transfer of funds.

- Setting up nomination details correctly.

- Keeping track of maturity and extension dates.

For elderly parents who are unfamiliar with banking paperwork, this assistance can be invaluable.

What About Power of Attorney (PoA)?

There is an important exception worth understanding.

If your parent has granted you a valid and registered Power of Attorney (PoA), certain account-related activities may be permitted on their behalf, subject to the policies of the bank or post office.

Depending on the institution, a PoA holder may be able to assist with:

- Account operations.

- Form submissions.

- Communication with the branch.

- Certain administrative tasks.

However, practices can vary between institutions, and some may require the account holder’s physical presence during the initial account-opening process.

For that reason, it is always advisable to contact the branch beforehand if a Power of Attorney arrangement is involved.

Who Owns the Account?

This point is important.

Even when a child helps organize the entire process or operates the account under a valid PoA, the SCSS account remains the property of the parent.

That means:

- The principal belongs to the parent.

- The interest income belongs to the parent.

- The tax liability belongs to the parent.

- The account is reported under the parent’s financial records.

Providing assistance does not change ownership.

A Practical Approach for Families

Many retirees appreciate help with financial administration, particularly when dealing with forms, branch visits, and documentation.

The most effective approach is usually collaborative:

- Let the parent remain the account holder.

- Help with paperwork and logistics.

- Ensure nomination details are completed properly.

- Maintain records of deposits, interest credits, and maturity dates.

This keeps the account fully compliant while making the process far less stressful for elderly family members.

The Bottom Line

You cannot independently open an SCSS account for your parent because the account must belong to the eligible senior citizen. However, you can assist with virtually every step of the process, from paperwork and documentation to branch visits and account management.

If a valid Power of Attorney exists, additional operational support may also be possible, subject to the policies of the bank or post office. Regardless of who helps with the administration, the account and all associated benefits remain in the parent’s name.

Can I Use My SCSS Account as Collateral for a Loan?

Yes, in many cases you can.

Although most people think of SCSS purely as an income-generating retirement product, it can also serve another purpose: acting as collateral for a loan. This can be particularly useful when you need temporary access to funds but don’t want to prematurely close your account and lose the benefits associated with it.

Why Would Someone Borrow Against an SCSS Account?

Retirement rarely unfolds exactly as planned.

Unexpected medical expenses, home repairs, family obligations, or other large costs can arise at any time. When that happens, many retirees instinctively consider breaking their investments.

With SCSS, that isn’t always the most efficient solution.

Premature closure may involve penalties and could disrupt a steady income stream you’ve built into your retirement plan. In some situations, borrowing against the account can be the more practical option.

How Loans Against SCSS Typically Work?

Many banks accept government-backed savings instruments as security because they are considered extremely low-risk collateral.

Since SCSS deposits carry the backing of the Government of India, lenders generally view them as strong security.

While policies differ between institutions, banks that offer loans against SCSS often allow borrowers to access a percentage of the deposit value rather than the full amount.

The exact terms depend on:

- The lending institution.

- The outstanding tenure of the SCSS account.

- Internal bank policies.

- Prevailing lending rates.

Because of these differences, it’s always worth checking directly with your bank rather than assuming all institutions follow the same rules.

A Simple Example

Imagine you have ₹20 lakh invested in SCSS and suddenly face a large medical expense.

You could:

- Prematurely close the account and potentially incur penalties.