Hidden Charges In Insurance Policy? How to File an IRDAI Grievance Successfully

Have You Discovered Hidden Charges In Insurance Policy Payouts?

If you’ve ever received an insurance payout that seemed far lower than you expected, you’re not the only one. It happens more often than many people realise, and in many cases, there is a clear process, backed by the regulator, to challenge the outcome. Herein comes the issue of hidden charges in an insurance policy.

Maybe your health insurance settlement covered only a fraction of your hospital bill. Perhaps your motor insurance claim dropped sharply after depreciation was applied. Or you surrendered a life insurance policy only to discover the amount returned was nowhere close to what you’d paid over the years. Situations like these usually come down to deductions and charges that weren’t properly explained when the policy was sold.

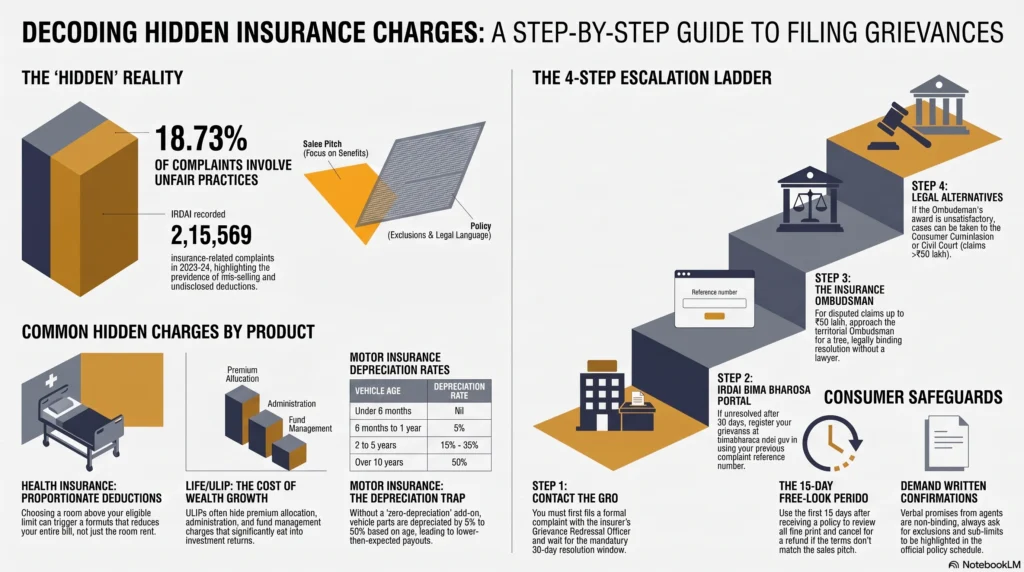

The numbers highlight just how common this has become. According to the IRDAI Annual Report 2023-24, policyholders filed 2,15,569 insurance-related complaints in a single year. Nearly 18.73% of those complaints involved unfair business practices, including mis-selling.

This guide explains where these hidden charges typically come from, how to review your policy for deductions that may not be justified, and the steps you can take if your insurer doesn’t resolve the issue. You’ll also learn how to escalate your complaint through your insurer’s Grievance Redressal Officer, the IRDAI Bima Bharosa portal, and, if necessary, the Insurance Ombudsman.

At A Glance: Hidden Charges In Insurance Policy

Identify Hidden Charges: Learn to spot undisclosed insurance fees, arbitrary proportionate room-rent deductions, and concealed co-pays buried deep in your policy wording.

Initial Escalation: Always file a formal, evidence-based complaint with your insurer’s Grievance Redressal Officer (GRO) first, adhering to the mandatory 30-day resolution window.

IRDAI Bima Bharosa Portal: If the insurer fails to resolve the issue, escalate your dispute directly to the regulator via the Bima Bharosa grievance system using your previous complaint reference number.

The Insurance Ombudsman: For disputed claims up to ₹50 lakh, approach the Insurance Ombudsman for a free, legally binding resolution without the need for a lawyer.

Consumer Safeguards: Protect your financial rights by utilizing the 15-day free-look period to cancel mis-sold policies and demanding written policy confirmations from agents.

Understanding Hidden Charges in Insurance Policies

What Are Hidden Charges in the Context of Insurance?

Not every deduction from an insurance claim is unfair. Many charges are perfectly valid, provided they’re clearly mentioned in your policy documents. Co-payment clauses, disease-specific sub-limits, depreciation rules, and administration fees are all legitimate if they’re spelled out in the policy schedule or wording.

The problem starts when a deduction catches you completely off guard. If your insurer can’t point to the exact clause and page in your policy that justifies a deduction, you have every reason to question it.

It’s also worth remembering that “hidden” doesn’t always mean illegal. In many cases, the clause was buried in lengthy policy documents or written in technical language that was never properly explained when the policy was sold. As a result, policyholders often discover these conditions only when they file a claim or decide to surrender the policy.

The Financial Impact of Unfair and Undisclosed Insurance Fees

The financial impact of these deductions is anything but minor. Insurance Samadhan’s Q2 2025 Trends Report recorded 974 complaints, up from 684 in the previous quarter, representing a 45% increase. During the same period, the value of disputed claims jumped from ₹83.5 crore to ₹119.5 crore, an increase of more than 43%.

Health insurance accounted for roughly 68% of all complaints, followed by life insurance at 25.5% and general insurance at 6.9%. Endowment policies also stood out as one of the most frequently mis-sold products.

For an individual policyholder, the loss can be substantial. A room-rent proportionate deduction alone can reduce an otherwise valid hospital claim by 30% to 50% if applied incorrectly.

Interestingly, people aged 31 to 40 filed the highest number of complaints, while Uttar Pradesh contributed around 16% of the country’s total grievances. That suggests awareness plays a significant role. People who understand their rights are often more likely to challenge questionable deductions instead of accepting them without question.

How Insurance Companies Conceal Extra Costs in the Fine Print

One of the biggest reasons these disputes arise is the gap between what is explained during the sale and what actually appears in the policy document.

The Union consumer affairs department has highlighted this issue to the finance ministry, noting that insurance policies are often filled with dense legal language while sales conversations focus almost entirely on benefits. Important exclusions and limitations frequently come to light only after a claim has been filed.

The same report discusses proposals such as offering policy documents in regional languages and requiring agents to maintain audio and video recordings of their sales pitches. The objective is simple: reduce the gap between what customers are promised and what their policies actually provide.

The Difference Between Standard Premiums and Hidden Deductions

The premium is the amount you agree to pay when purchasing the policy. Hidden deductions, on the other hand, usually remain dormant until you make a claim.

These can include co-pay clauses, treatment sub-limits, depreciation schedules, compulsory deductibles, or proportionate deduction formulas. In many cases, a policy carries a lower premium precisely because these restrictions are built into the coverage.

That’s why comparing policies based only on premium can be misleading. A cheaper policy isn’t necessarily better value if it includes deductions that significantly reduce your claim when you need the cover the most. Reading the schedule of benefits alongside the premium is just as important as comparing the price itself.

Common Types of Hidden Fees Across Different Insurance Products

Hidden Costs in Unit-Linked Insurance Plans (ULIPs) and Life Insurance

ULIPs combine life insurance with market-linked investments, which is why they’re often presented as products that can help grow your wealth while offering insurance protection. The trouble begins when buyers are told only about the potential returns and not about the costs that come with the policy.

A typical ULIP may include premium allocation charges, policy administration charges, fund management charges, and mortality charges. If you decide to stop paying premiums or surrender the policy before the mandatory lock-in period ends, a discontinuance charge may apply as well, reducing the value you’ve accumulated.

Endowment plans can create a different kind of misunderstanding. They’re sometimes marketed as investment products with attractive guaranteed returns, even though their primary purpose is insurance protection, with bonuses that are often modest and not always guaranteed. If you exit either type of policy early, surrender charges can significantly reduce the amount you receive. Before signing up, it’s worth checking the likely surrender value using a calculator.

Uncovering Concealed Co-Payments and Deductibles in Health Insurance

Health insurance disputes often come down to a handful of deductions that policyholders either didn’t notice or didn’t fully understand when buying the policy.

| Deduction Type | What it Means | Common Red Flag |

| Co-payment | You pay a fixed percentage of every claim yourself. | The insurer applies it even though it’s missing from your policy schedule, or uses it for hospitalisations when it should apply only to specific treatments. |

| Disease or treatment sub-limit | A fixed cap on the amount payable for certain procedures, such as cataract surgery, hernia treatment, knee replacement, ICU expenses, or ambulance charges. | The insurer relies on an outdated policy version or extends the cap to related expenses that were never meant to be restricted. |

| Non-medical or non-payable items | Consumables and administrative expenses that insurers are permitted to exclude under IRDAI guidelines. | Items already included in a hospital package are deducted again as separate charges. |

Non-payable items typically account for around 5% to 15% of a hospital bill. In many cases, these deductions arise simply because the hospital bundled certain consumables into a package instead of listing them separately, making them open to dispute.

Another costly issue is the room-rent proportionate deduction. If you choose a hospital room that’s more expensive than the category allowed under your policy, insurers often calculate the payable claim using the formula:

Payable Amount = Total Bill × (Eligible Room Rent ÷ Actual Room Rent Availed)

While this adjustment may be valid for charges directly linked to the room category, such as the surgeon’s fee, nursing charges, or operating theatre costs, it is sometimes applied across the entire hospital bill. Courts and IRDAI have indicated that such deductions should generally be limited to expenses genuinely affected by the room category.

Obscure Depreciation Clauses and Compulsory Deductibles in Motor Insurance

Motor insurance claims almost always involve depreciation unless you’ve purchased a zero-depreciation add-on.

Standard own-damage claims apply depreciation to replaced vehicle parts based on the vehicle’s age :

| Vehicle Age | Standard Depreciation Rate |

| Under 6 months | Nil |

| 6 months to 1 year | 5% |

| 1 to 2 years | 10% |

| 2 to 3 years | 15% |

| 3 to 4 years | 25% |

| 4 to 5 years | 35% |

| 5 to 10 years | 40% |

| Over 10 years | 50% |

Without zero-depreciation cover, these deductions can make a noticeable difference. A repair bill of ₹30,000, for example, could result in an insurance payout of only around ₹19,000 once depreciation is applied.

Even if you’ve purchased zero-depreciation cover, it’s worth reading the policy carefully. Tyres, tubes, and batteries are often reimbursed at only 50%, rather than being fully protected from depreciation.

You’ll also come across compulsory deductibles. These are fixed amounts that every policyholder must bear on each own-damage claim, regardless of any add-ons. They’re different from voluntary deductibles, which you choose yourself in exchange for a lower premium. Both figures are clearly mentioned in your policy schedule and should be reviewed before you assume comprehensive insurance covers every expense.

Unauthorized Administration Fees and Agent Commissions

Many hidden-charge disputes begin long before a claim is ever filed. They start during the sales process.

IRDAI’s 2022-23 data showed that around 20% of complaints against life insurers involved mis-selling. Moneylife has also documented cases where senior citizens were sold life insurance products after being told they were purchasing annuity plans, often through bank relationship managers.

Some warning signs deserve immediate attention :

- Promises of guaranteed or doubled returns without clearly explaining who is providing that guarantee.

- Being told you must buy an insurance policy to secure a home loan, even though the Reserve Bank of India does not require property insurance as a condition for loan approval.

- Being encouraged to buy a policy that doesn’t match your financial goals or risk tolerance.

- High-pressure sales tactics involving cashback offers, freebies, or claims that you must sign before the end of the day.

If any of these situations arise, it’s worth slowing the conversation down and asking for everything in writing before committing to the policy.

How to Audit Your Insurance Policy for Undisclosed Charges

Maximizing the 15-Day Free-Look Period for Policy Review

One of the easiest opportunities to avoid a costly mistake comes immediately after you receive your policy. IRDAI regulations provide a free-look period, typically 15 days from the date you receive the policy document, giving you time to review the terms and decide whether the policy matches what you were promised.

If you purchased the policy online or through another distance-marketing channel, some insurers may offer a longer free-look period. Instead of assuming the standard 15 days applies, check your policy schedule for the exact timeline.

Use this period wisely. Compare the benefits explained during the sales process with the actual policy wording. Pay close attention to exclusions, waiting periods, co-pay clauses, sub-limits, lock-in conditions, and surrender terms. If you discover that the policy doesn’t reflect what was represented to you, you can usually cancel it during the free-look period, subject to the deductions permitted under IRDAI regulations. Once this window closes, correcting a poor purchase becomes much more difficult.

Requesting a Detailed Premium Breakup from Your Insurer

If you notice deductions during a claim settlement, don’t assume they’re correct. Ask your insurer to explain each one.

Write to your insurer’s claims department or Third-Party Administrator (TPA) and request the exact policy clause and page number that authorises every deduction. Giving the insurer about a week to respond creates a written record of your communication and, in some cases, prompts the company to review or even reverse an incorrect deduction without the need for further escalation.

Even if the matter eventually reaches IRDAI or the Insurance Ombudsman, this correspondence becomes valuable evidence. A clear response from the insurer, or the absence of one, helps establish that you first attempted to resolve the issue through the insurer’s own grievance process.

Decoding Policy Exclusions, Sub-Limits, and Ambiguous Terms

Insurance documents often use terms that sound similar but mean very different things. Misunderstanding these definitions is one of the biggest reasons policyholders end up disappointed when they make a claim.

A co-pay means you pay a fixed percentage of every eligible claim yourself. A deductible is a fixed amount that must be borne before the insurer starts paying. A sub-limit places a cap on how much the insurer will pay for a specific treatment or expense, while a waiting period temporarily excludes coverage for certain illnesses or conditions.

Treating these terms as interchangeable can lead to unrealistic expectations. For example, many people assume that buying a comprehensive health insurance policy automatically means there are no treatment caps or co-pay clauses. That isn’t always the case.

Two people can even hold policies from the same insurer with completely different conditions. A senior citizen’s policy may include a mandatory 20% co-pay, while a family floater for younger members may not. The only reliable way to know what applies to you is to read your own policy schedule rather than relying on someone else’s experience.

Identifying Discrepancies Between Benefit Illustrations and Actual Deductions

When you receive a claim settlement, don’t focus only on the final amount. Take the time to compare it with the documents you already have.

Keep your settlement letter alongside the hospital’s itemised bill or the vehicle repair estimate. Then prepare a simple three-column list:

| Deducted Item | Insurer’s Reason | Your Observation |

| Item deducted | Clause or explanation provided | Does the clause actually exist in your policy? Was the calculation applied correctly? |

Go through each deduction individually. Verify whether the insurer has cited a clause that genuinely appears in your policy schedule and check the arithmetic carefully. Even small calculation errors can add up to a significant reduction in your payout.

By the end of this exercise, you’ll have a clear picture of the deductions you believe are incorrect. That document will become the foundation of your formal grievance and make it much easier to explain your case if you need to escalate it later.

Step 1: Initiating the Grievance Redressal Process with Your Insurer

Why You Must Contact the Insurance Company First

If you believe your insurer has treated your claim unfairly, your first step is always to raise the issue with the insurer itself. You cannot bypass this stage and go straight to IRDAI or the Insurance Ombudsman.

Before a complaint can be escalated, you must show that you’ve already given the insurer an opportunity to resolve the matter. If you skip this step, your complaint on the Bima Bharosa portal may be rejected for not following the prescribed process.

The Council for Insurance Ombudsmen also makes this requirement clear in its grievance procedure. While it may seem like an extra administrative step, many disputes are resolved during the insurer’s internal review, saving policyholders the time and effort involved in further escalation.

Locating the Grievance Redressal Officer (GRO) for Your Insurer

Every insurance company is required to appoint a Grievance Redressal Officer (GRO) to handle customer complaints.

You can usually find the GRO’s contact details on the insurer’s official website, in your policy document, or on the company’s grievance redressal page. Many insurers also include these details on the final pages of the policy schedule, making it easier to locate the right contact without searching extensively.

If you’re unable to find the information, the Council for Insurance Ombudsmen maintains centralised directories of GROs for life and health insurers as well as non-life insurers.

Taking a few minutes to identify the correct officer helps ensure your complaint reaches the appropriate department from the outset.

Drafting a Factual and Evidence-Based Complaint Letter

A well-documented complaint carries far more weight than an emotional one.

Start by including your policy number, claim number if applicable, important dates, and a clear explanation of what happened. Stick to the facts and avoid making assumptions or accusations that you cannot support with evidence.

Attach copies of every relevant document, including:

- Your policy schedule.

- The itemised hospital bill or vehicle repair estimate.

- The insurer’s settlement or rejection letter.

- Previous emails or letters exchanged with the insurer.

- Any additional documents that support your claim.

Wherever you disagree with a deduction, ask the insurer to identify the exact clause number and page in the policy that authorises it. If you believe the deduction has no contractual basis, state that clearly and politely. You can also mention that you’ll escalate the matter through the IRDAI Bima Bharosa portal and, if necessary, the Insurance Ombudsman if the issue remains unresolved.

Understanding the Mandatory 30-Day Resolution Window

Once your complaint reaches the insurer, the company is expected to examine the matter and respond within the prescribed timeframe.

According to the Council for Insurance Ombudsmen’s published procedure, insurers and brokers are expected to resolve complaints within 30 days. If you’re dissatisfied with the response, or you receive no response at all during this period, you’re generally entitled to move to the next stage of the grievance process.

You may also come across references to a shorter 15-day internal benchmark used by some insurers or mentioned in resources discussing Bima Bharosa readiness. Even so, the 30-day period remains the recognised outer limit under the Insurance Ombudsman Rules, 2017 for exhausting the insurer’s internal grievance mechanism.

Tracking Your Internal Complaint Status and Acknowledgment Receipts

Don’t rely on memory when dealing with an insurance dispute. Keep a record of every communication.

Save copies of the complaint email, courier receipt, acknowledgement, and any delivery or read confirmations you receive. Once the insurer assigns a complaint reference number, note it carefully and keep it with your other documents.

That reference number becomes important throughout the grievance process. You’ll need it if you later approach IRDAI or the Insurance Ombudsman, and failing to provide it is one of the most common reasons complaints are sent back for clarification or rejected during escalation.

A simple folder containing your emails, acknowledgements, and supporting documents can save considerable time if the dispute moves beyond the insurer’s internal process.

Step 2: Introduction to the IRDAI Grievance Redressal Mechanism

The Role of the Insurance Regulatory and Development Authority of India (IRDAI)

The Insurance Regulatory and Development Authority of India (IRDAI) is the regulator responsible for overseeing the insurance industry in India. Established under the Insurance Regulatory and Development Authority Act, 1999, it sets the rules insurers must follow and works to protect the interests of policyholders.

Beyond regulating insurers, IRDAI also establishes the grievance redressal framework that governs how complaints should be handled. It lays down timelines for acknowledging grievances, processing claims, and resolving disputes, while also providing mechanisms for policyholders to seek help when an insurer fails to address their concerns.

How IRDAI Protects Policyholders from Mis-Selling and Fraud

When you file a complaint with IRDAI, you’re not just pursuing your own case. Your complaint also becomes part of a larger system that helps the regulator identify recurring issues across insurers.

By analysing complaint trends, IRDAI can spot patterns such as repeated instances of mis-selling, claim delays, or poor customer service and take regulatory action where necessary.

IRDAI also strengthens consumer protection through regulatory reforms. For example, its Master Circular issued in May 2024 requires insurers to decide on cashless hospital discharge requests within three hours of receiving them from the hospital. If an insurer fails to meet that timeline and the delay results in additional hospital charges, those costs must be borne by the insurer rather than the policyholder.

The Evolution from IGMS to the Bima Bharosa Portal in 2026

IRDAI’s earlier online grievance platform, the Integrated Grievance Management System (IGMS), has now been replaced by Bima Bharosa, a more comprehensive portal designed to simplify the complaint process and improve transparency.

The platform enables policyholders to submit grievances, monitor their status, and allows IRDAI to track how insurers handle complaints across the industry. It also serves as a central repository for grievance data, making it easier to identify recurring issues and improve oversight.

The latest version, Bima Bharosa 2.0, has been designed with accessibility in mind. It requires only eight mandatory personal details to register a complaint and supports 13 regional languages, making the platform easier for a wider range of policyholders to use.

When Does an Issue Qualify for an Official IRDAI Complaint?

You become eligible to approach IRDAI once you’ve completed the insurer’s internal grievance process and the issue remains unresolved.

In practical terms, that means you’ve already written to your insurer’s Grievance Redressal Officer and either:

- Received a response that doesn’t satisfactorily resolve your complaint, or

- Received no response within the prescribed resolution period.

Common reasons for escalating a complaint include delayed claim settlements, unexplained deductions, partial claim payments without adequate justification, policy mis-selling, incorrect policy servicing, and other disputes that the insurer has failed to resolve despite being given the opportunity to do so.

At this stage, Bima Bharosa acts as the next formal step in the grievance process, helping ensure your complaint receives regulatory oversight if the insurer’s internal mechanism has not delivered a satisfactory outcome.

Step 3: How to File a Complaint on the Bima Bharosa Portal Successfully

Registering a New Account on the Bima Bharosa System

To begin the online complaint process, visit https://bimabharosa.irdai.gov.in and register for a new account using your name, mobile number, and email address. If you’ve already created an account, simply sign in with your existing credentials.

The registration process is straightforward, but it’s worth taking a moment to ensure that the contact details you provide are accurate. These details will be used for future updates about your complaint.

Selecting the Right Complaint Category (Insurer, Broker, or Intermediary)

After logging in, navigate to the Grievance section and select Register New Grievance.

You’ll then be asked to identify the nature of your complaint. This includes choosing the relevant category, such as claim settlement, policy servicing, or mis-selling, and specifying whether your grievance is against an insurance company, broker, agent, or another intermediary.

Choosing the correct category from the beginning helps direct your complaint to the appropriate team and can reduce unnecessary delays during the review process.

Filling Out Policy Details and Complainant Information Accurately

Bima Bharosa 2.0 has been designed to keep the filing process simple. Registering a grievance requires only eight mandatory details, including your policy number, the insurer’s name, and a brief description of the issue you’re facing.

When describing your complaint, focus on the key facts rather than writing a lengthy narrative. Mention what happened, when it happened, and why you believe the insurer’s action was incorrect.

It’s equally important to double-check the policy number and insurer details before submitting the form. Even a small mistake can slow down the routing of your complaint.

Uploading Crucial Supporting Documents (Emails, Rejection Letters, Audio Records)

Supporting documents often determine how smoothly your complaint progresses.

Attach copies of every document that helps explain your case, including:

- Your complaint submitted to the insurer’s Grievance Redressal Officer.

- The insurer’s settlement or rejection letter.

- Your complaint reference number issued by the insurer.

- Relevant emails and written correspondence.

- Any additional documents that support your claim.

According to guidance on the Bima Bharosa process, missing the insurer’s rejection letter or failing to include the earlier complaint reference number are among the most common reasons complaints are returned or rejected during escalation.

Before clicking submit, review each uploaded file to make sure it’s complete, readable, and attached correctly.

Tracking Your Grievance Status Using the Unique Reference Token

Once your grievance is successfully submitted, Bima Bharosa generates an acknowledgement along with a unique grievance ID. You’ll also receive an email or SMS containing an IRDAI token number that can be used to track your complaint throughout the process.

One advantage of the portal is that it allows you to follow your complaint at every stage. You can see whether it’s awaiting the insurer’s response, under IRDAI’s review, or has already been resolved. Having this visibility makes it easier to monitor progress without repeatedly contacting customer support.

Alternative Methods to Register an IRDAI Grievance

Not everyone is comfortable using an online portal, and IRDAI provides several alternative ways to register a grievance.

Reaching the IRDAI Grievance Call Centre (IGCC) via Toll-Free Numbers

If you’d rather speak to someone directly, you can contact the IRDAI Grievance Call Centre (IGCC) by calling either 155255 or 1800-4254-732. The helpline generally operates from 8:00 AM to 8:00 PM, Monday through Saturday.

Before calling, keep your policy number, complaint reference number, and relevant documents handy. It makes the conversation quicker and helps the support representative assist you more effectively.

Submitting an Official Grievance via Email to IRDAI

If you prefer written communication, you can email your grievance directly to complaints@irdai.gov.in.

A clear, well-organised email that includes your policy details, complaint history, and supporting documents is likely to be easier for officials to review than a brief message with limited information.

Mailing a Physical Complaint to the IRDAI Consumer Affairs Department

Policyholders who prefer traditional correspondence can also submit a written complaint by post to:

Insurance Regulatory and Development Authority of India

Consumer Affairs Department – Grievance Redressal Cell

Sy. No. 115/1, Financial District

Nanakramguda, Gachibowli

Hyderabad – 500032, Telangana

One point that’s easy to overlook is that IRDAI’s grievance cell accepts complaints only from the insured person or the claimant. Complaints submitted solely by advocates, agents, or other third parties on behalf of a policyholder are generally not entertained.

Special Assistance Channels for Senior Citizens

Senior citizens who aren’t comfortable using online services don’t have to rely on the Bima Bharosa portal. They can use the same toll-free helpline or postal grievance process instead.

Under the Insurance Ombudsman framework, a legal heir, nominee, or assignee may also file and pursue a complaint on behalf of a senior citizen where appropriate.

IRDAI also expects insurers to pay special attention to the servicing and claims of senior citizens under its health insurance guidelines. If age, mobility issues, or health conditions make it difficult to complete the process independently, it’s a good idea to mention these circumstances while communicating with the insurer or the IGCC. Having a trusted family member help organise documents can also make the process much less stressful, even if the complaint itself continues to be filed in the policyholder’s name.

Step 4: Escalating Unresolved Complaints to the Insurance Ombudsman

Before moving to the next stage, it helps to understand how the grievance process is structured:

| Stage | Where to Go | Cost | Typical Timeline |

| Insurer / GRO | Your insurer’s Grievance Redressal Officer | Free | Insurer expected to respond within 30 days |

| IRDAI Bima Bharosa | https://bimabharosa.irdai.gov.in | Free | Reviewed after the insurer’s internal process is completed |

| Insurance Ombudsman | Your territorial Ombudsman office, via https://www.cioins.co.in | Free | Award generally issued within 3 months after all requirements are received |

| Consumer Commission | District, State, or National Commission under the Consumer Protection Act, 2019 | Nominal filing fee | Typically filed within 2 years of the cause of action |

Many policyholders stop after filing a complaint with their insurer or through Bima Bharosa, assuming there are no further options. In reality, the Insurance Ombudsman offers another avenue for resolving disputes without the expense and complexity of court proceedings.

What is the Insurance Ombudsman and When Should You Approach Them?

The Insurance Ombudsman is a statutory, quasi-judicial authority established under the Insurance Ombudsman Rules, 2017 to provide policyholders with a simple, cost-free way to resolve insurance disputes outside the traditional court system.

You can approach the Ombudsman for a range of issues, including:

- Delayed claim settlements.

- Partial or complete rejection of claims.

- Premium-related disputes.

- Misrepresentation of policy terms.

- Disagreements over how policy provisions should be interpreted during a claim.

- Policy servicing deficiencies.

- Policies issued with terms that don’t match the proposal form.

- Failure to issue a policy after receiving the premium.

- Other regulatory violations connected with these matters.

The Ombudsman becomes the appropriate forum once you’ve exhausted the insurer’s internal grievance process and the issue still hasn’t been resolved satisfactorily.

Verifying Ombudsman Territorial Jurisdiction for Your City or State

India currently has 17 Insurance Ombudsman offices, and your complaint can generally be filed with the office that has jurisdiction over either your place of residence or the insurer’s branch that handled your policy.

For example, the Chennai Ombudsman office covers Tamil Nadu along with Puducherry town and Karaikal, while the Bengaluru office handles Karnataka. The Delhi office has jurisdiction over Delhi as well as Gurugram, Faridabad, Sonepat, and Bahadurgarh in Haryana.

Here is a A complete and updated list of all Ombudsman offices, along with their contact details and territorial jurisdiction.

Navigating the Council for Insurance Ombudsmen (CIO) Online Portal

The Council for Insurance Ombudsmen provides an online portal where policyholders can both file and monitor complaints.

You can register a fresh complaint through here. If you’ve already submitted one, you can check its progress through the complaint tracking facility available at here.

The portal keeps the process organised by allowing policyholders to submit documents, monitor updates, and stay informed without relying entirely on offline communication.

The ₹50 Lakh Compensation Limit and Eligibility Rules

The Ombudsman can consider complaints where the total amount in dispute, including related expenses, does not exceed ₹50 lakh, and there is no fee for filing the complaint.

To qualify, the complaint must generally be filed:

- Within one year of the insurer rejecting your complaint, or

- Within one year from the date the insurer failed to respond within one month of receiving your written representation.

The matter should also not already be pending before, or decided by, a court, consumer commission, or arbitrator.

The Ombudsman system is primarily intended for individual policyholders, sole proprietorships, and eligible micro enterprises, including those meeting the investment and turnover thresholds notified on 21 March 2025. Beneficiaries under group or master insurance policies may also be eligible to file complaints.

Why Legal Representation is Banned in Ombudsman Hearings

One feature that makes the Ombudsman process different from court proceedings is its simplicity.

The Insurance Ombudsman Rules, 2017 do not provide for representation through lawyers during these proceedings.

The idea is to keep the process informal, accessible, and affordable so that policyholders can present their cases without needing to hire legal counsel. While the hearings remain structured and evidence-based, the emphasis is on resolving disputes efficiently rather than following lengthy courtroom procedures.

The Ombudsman Hearing Process and Final Resolution

Preparing Your Arguments and Chronology of Events

Good preparation can make a significant difference.

Arrange your documents in chronological order so that anyone reviewing the file can easily follow the sequence of events. Include your policy schedule, your complaint to the insurer, the insurer’s reply or rejection letter, claim documents, and all subsequent correspondence.

According to the Council for Insurance Ombudsmen, you’ll generally need documents such as:

- A copy of your written representation to the insurer.

- Valid KYC documents.

- A recent photograph for online filing.

- The insurer’s rejection or settlement letter.

- A copy of the insurance policy.

Presenting documents in an organised manner often makes it easier to explain your grievance during the proceedings.

What to Expect During an Online Video Hearing

Not every complaint results in a hearing. The Ombudsman may decide a case based solely on the documents submitted if no additional clarification is needed.

Where a hearing is considered necessary, it may be conducted either in person or through video conferencing. Hearings can also take place outside the Ombudsman’s headquarters, provided they’re held within the relevant territorial jurisdiction and both parties receive prior notice .

During the hearing, you’ll generally be given an opportunity to explain your grievance, while the insurer presents its position. The Ombudsman then reviews the evidence before reaching a decision.

The 3-Month Timeline for Receiving the Ombudsman Award

If both parties agree to resolve the matter through mediation, the Ombudsman aims to issue a recommendation within one month after receiving written consent from both sides.

Where mediation isn’t used or doesn’t lead to a settlement, the Ombudsman is required to issue a formal award within three months of receiving all the necessary documents and information from the complainant.

Although timelines can vary depending on the complexity of the dispute, this framework provides policyholders with a reasonable expectation of when the matter is likely to conclude.

Understanding the Binding Nature of the Decision on Insurers

Once the Ombudsman issues an award, it becomes binding on the insurer or broker.

It’s important to understand, however, that the Ombudsman can award only what you’re entitled to under the terms of your insurance policy. The forum cannot grant ex gratia payments or compensation that falls outside the contractual benefits available under the policy.

Your Rights if You Reject the Ombudsman’s Final Award

While the insurer is bound by the Ombudsman’s award, you are not.

If you’re dissatisfied with the outcome, you remain free to pursue other legal remedies, including filing a case before the appropriate Consumer Disputes Redressal Commission or a competent civil court .

The Ombudsman process is intended to provide a faster and less expensive route for dispute resolution, but it doesn’t take away your right to seek relief through the regular legal system if you believe your grievance still hasn’t been adequately addressed.

Exploring Legal Alternatives Beyond IRDAI Regulations

Taking Your Dispute to the District Consumer Disputes Redressal Commission

If your grievance still isn’t resolved after going through the insurer and the Insurance Ombudsman, you may consider approaching the Consumer Disputes Redressal Commission under the Consumer Protection Act, 2019.

The forum you approach depends on the value of your claim. Generally, the District Commission hears disputes involving claims up to ₹50 lakh, the State Commission handles claims between ₹50 lakh and ₹2 crore, and the National Commission deals with matters exceeding ₹2 crore.

In most cases, complaints should be filed within two years from the date the cause of action arose. Besides directing insurers to honour valid claims, Consumer Commissions can also award compensation for loss or injury and reimburse litigation costs where appropriate under the Consumer Protection Act.

A notable example is Trilok Singh v. Cholamandalam MS General Insurance Co. Ltd. (2023). In that case, the Supreme Court overturned the insurer’s rejection of a theft claim that had been denied on a technical ground involving delayed intimation. The Court directed the insurer to pay ₹5,50,000 along with 9% annual interest, reinforcing the principle that genuine claims should not be rejected solely because of procedural lapses.

Filing a Civil Lawsuit for Claims Exceeding the ₹50 Lakh Threshold

Not every insurance dispute is suited for the Ombudsman or Consumer Commission. High-value claims, legally complex disputes, or matters involving contractual interpretation may ultimately require proceedings before a civil court or through arbitration, depending on the terms of the insurance policy .

Before choosing this route, review your policy carefully. Many insurance contracts contain an arbitration clause, particularly for disputes involving the amount payable under a claim. In such cases, you may be required to attempt arbitration before initiating civil proceedings.

Since litigation can be time-consuming and expensive, it’s usually sensible to obtain legal advice before deciding whether a civil suit is the most appropriate course of action.

Reporting Systemic Insurance Fraud to the Economic Offences Wing (EOW)

Not every insurance problem is simply a disagreement over a claim. Sometimes, the issue points to something much more serious.

If you suspect forged policy documents, fake insurance products, organised mis-selling, or any other large-scale fraudulent activity, you should consider reporting the matter to your state’s Economic Offences Wing (EOW) or the local cyber crime police in addition to pursuing your grievance through IRDAI or the Insurance Ombudsman.

The regulatory complaint process and criminal investigation serve different purposes. One aims to resolve your insurance dispute, while the other investigates potential criminal offences.

Some warning signs that may justify reporting the matter to law enforcement include:

- Purchasing a policy from someone who doesn’t hold a valid IRDAI agent or broker licence.

- Being asked to transfer premiums into a personal bank account instead of an authorised insurer payment channel.

- Discovering that the policy you paid for was never actually issued by the insurance company.

Where organised fraud appears to be involved, reporting it promptly may help protect not only your own interests but also those of other consumers.

Proactive Measures to Avoid Future Insurance Disputes

Buying Directly from Insurers vs. Relying on Third-Party Agents

Many insurance disputes can be avoided long before a claim is ever filed. One way to reduce the risk is to understand how the policy is being sold.

Since agents and intermediaries often earn commissions on the products they recommend, there can sometimes be an incentive to promote policies that are more rewarding for the seller than they are suitable for the buyer. Purchasing directly from an insurer or working with a fee-transparent advisor can reduce the likelihood of ending up with a policy that doesn’t match your needs .

That said, it’s important not to assume every agent is acting in bad faith. Many are knowledgeable professionals who genuinely help customers choose appropriate cover. Even so, the final responsibility for understanding the policy rests with you. Take time to compare features, ask questions, and verify every important promise before signing.

If someone tells you that buying insurance is compulsory to obtain another financial product, such as a home loan, don’t accept the statement without checking it independently. For example, the Reserve Bank of India does not require borrowers to purchase property insurance as a mandatory condition for sanctioning a home loan.

Demanding Written Confirmation for All Policy Promises

Verbal assurances can easily be forgotten or disputed later. Written confirmation is far more reliable.

Before purchasing any policy, ask the insurer or agent to clearly explain important aspects such as exclusions, waiting periods, lock-in requirements, surrender conditions, co-pay clauses, and exit options. If you’re promised benefits like “no co-pay” or “complete coverage,” make sure those assurances are reflected in the policy schedule itself.

If the written policy doesn’t match what you were told during the sales process, that discrepancy could become the basis for a mis-selling complaint.

A few extra questions before signing can prevent a much bigger dispute later.

Conducting Comprehensive Annual Portfolio Reviews

Your insurance needs don’t remain the same forever, and your policies shouldn’t be left unchecked for years at a time.

Medical costs rise, your family’s financial responsibilities change, and the value of your vehicle or other insured assets gradually declines. Reviewing your policies once a year helps ensure your cover continues to match your current situation.

During your review, consider checking:

- Whether your sum insured is still adequate.

- Any room-rent limits or treatment sub-limits.

- Whether optional riders are still relevant.

- Changes in your financial goals or family circumstances.

- Whether surrendering or replacing an existing policy makes financial sense.

Useful tools, including a surrender-value calculator and a portfolio review calculator can be used for the purpose.

A yearly review takes relatively little time, but it can help identify gaps before they become expensive surprises during a claim.

Frequently Asked Questions: Hidden Charges In Insurance Policy

In health insurance, hidden deductions typically surface during claim settlements as proportionate room-rent deductions, unlisted non-medical consumables, unauthorized co-payment clauses, and rigid disease-specific sub-limits that cap payouts for procedures like cataract or hernia surgeries without explicit prominence in the primary schedule.

To file an official IRDAI complaint, register at the Bima Bharosa portal (bimabharosa.irdai.gov.in) using your verified contact details. Select the correct grievance category, enter your insurance policy number, provide a factual summary, and upload the mandatory insurer rejection letter along with your unique internal complaint reference token.

Under the regulatory framework, insurance companies must provide a definitive response within a mandatory 30-day resolution window. If they fail to reply or issue an unsatisfactory verdict within this period, you are legally entitled to immediately escalate the case to the Insurance Ombudsman.

No. You cannot bypass the initial stages. You must first raise a formal complaint with your insurer’s specific Grievance Redressal Officer (GRO). Only after receiving an official rejection or passing the 30-day deadline without a response can you approach the Insurance Ombudsman.

The Insurance Ombudsman territorial jurisdiction allows them to adjudicate consumer complaints where the total disputed claim value, including compensation and related expenses, does not exceed a maximum financial cap of ₹50 lakh.

No. The Insurance Ombudsman Rules 2017 strictly ban legal representation by lawyers during these proceedings. The forum is intentionally designed to be an informal, cost-free, and highly accessible dispute resolution pipeline for individual policyholders presenting their own factual chronology of events.

The 15-day free-look period allows consumers to review the fine print immediately after delivery. If you detect undisclosed insurance fees or realize the product was mis-sold by an agent, you can cancel the contract for a full refund minus minimal regulatory administrative expenses.

Maintaining a Digital Repository of All Insurance Communications

Good documentation often makes the difference between a straightforward grievance and a prolonged dispute.

Keep digital copies of your policy schedule, premium receipts, renewal notices, hospital bills, repair estimates, settlement letters, emails, and every important communication exchanged with your insurer, Third-Party Administrator (TPA), or agent.

If a disagreement arises months or even years later, having these documents readily available can save considerable time. Both IRDAI and the Insurance Ombudsman rely heavily on documentary evidence when reviewing complaints, so maintaining an organised record puts you in a much stronger position if you ever need to challenge a claim decision.

Even something as simple as storing scanned copies in a secure cloud folder or clearly labelled digital folders can make the grievance process much smoother if the need ever arises.

Disclaimer

This article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Grievance procedures, monetary limits, and contact details are subject to change by IRDAI and the Council for Insurance Ombudsmen, so verify current details on the official portals before filing. For advice specific to your policy or dispute, consult a licensed insurance advisor or legal professional.

Leave a Reply