The 2026 Guide to 100% FDI in the Indian Insurance Sector: A Complete Policyholder Impact Analysis

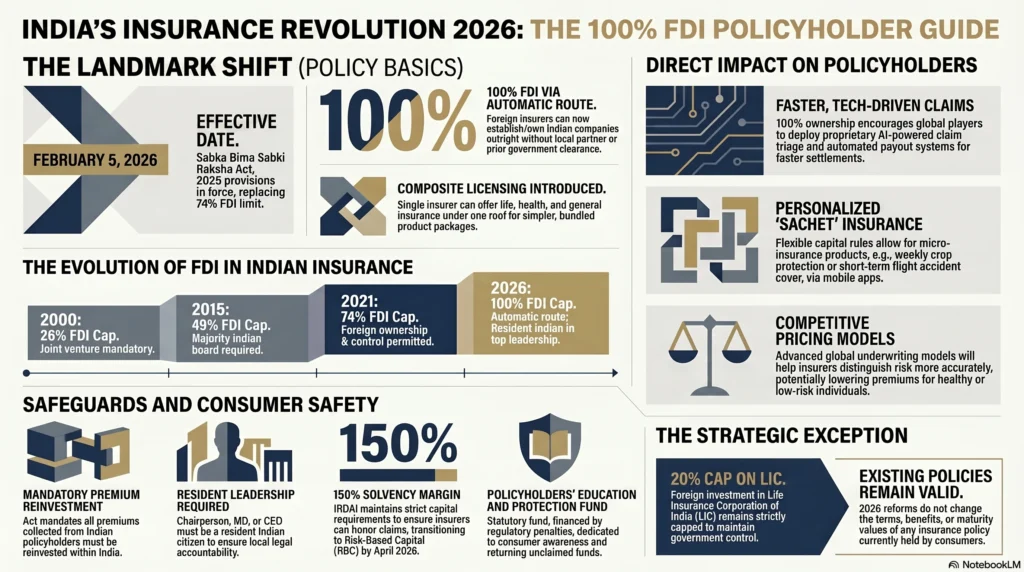

India’s insurance industry reached a turning point on 5 February 2026. On that day, most provisions of the Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, officially came into effect. The headline change was significant: the long-standing 74% cap on foreign direct investment (FDI) was removed and replaced with a framework that allows 100% foreign ownership through the automatic route, thus opening the door for 100% FDI in the Indian insurance sector.

For more than 500 million Indians who already hold an insurance policy, and for millions more who remain uninsured, this is not just another policy announcement from New Delhi. It has real-world implications. The reform changes who can own insurance companies operating in India, how those companies can invest and grow, and ultimately what kind of products, services, and protections are available to policyholders.

In practical terms, the companies responsible for protecting your family’s financial future, covering medical emergencies, or insuring your home and business now have access to a very different operating environment. More capital can enter the sector. New players can enter more easily. Existing insurers can rethink how they compete.

This guide breaks down what all of that means in plain English. We’ll look at the legislative journey behind the reform, explain how the automatic route works, examine the potential impact on premiums and claims, explore the safeguards introduced by IRDAI, and discuss the kinds of insurance products that could emerge as a result of this new framework.

At A Glance: 100% FDI in Indian Insurance Sector

· 100% FDI via Automatic Route: Foreign direct investment limits in Indian insurance increased from 74% to 100% effective February 5, 2026.

· Landmark Legislation: Enacted under the Sabka Bima Sabki Raksha Act, 2025, which also introduces composite licensing and flexible capital requirements.

· LIC Cap Maintained: The Life Insurance Corporation of India (LIC) remains sovereign-backed, with its foreign investment limit strictly capped at 20%.

· Mandatory Local Leadership: Even under 100% foreign ownership, at least one top executive (Chairperson, MD, or CEO) must be a resident Indian citizen.

· Strict Premium Reinvestment: To safeguard policyholders, all premiums collected in India must be reinvested within India.

· Enhanced Consumer Safety: The operational launch of the statutory Policyholders’ Education and Protection Fund strengthens regulatory oversight and claims security.

What Does 100% FDI in Insurance Mean for India?

Foreign direct investment in India’s insurance sector is not a new concept. The country first opened the industry to private and foreign participation in 2000, but it did so cautiously. At the time, foreign investors could own only 26% of an insurance company. Over the years, that ceiling was gradually raised as policymakers became more comfortable with greater international participation.

The progression tells the story:

| Year | FDI Cap | Key Condition |

| 2000 | 26% | Joint venture mandatory |

| 2015 | 49% | Majority Indian board required |

| 2021 | 74% | Foreign ownership and control permitted with conditions |

| 2026 | 100% | Automatic route; one resident Indian in top leadership role |

Each increase was accompanied by safeguards aimed at balancing foreign capital with domestic oversight. For years, insurers had to navigate board composition requirements, ownership restrictions, and governance conditions designed to ensure that Indian stakeholders retained meaningful influence.

That framework has now changed dramatically.

As detailed in the analysis by Skadden shows that the reforms introduced through the Sabka Bima Sabki Raksha Act represent the most substantial restructuring of India’s insurance regulations in more than two decades. At the heart of those reforms is the removal of the foreign equity ceiling.

So what does that mean in practical terms?

Simply put, a foreign insurer can now establish or own an Indian insurance company outright. A large European life insurer, a Japanese general insurer, or another global insurance group no longer needs an Indian partner holding the remaining 26% stake. Under the previous regime, that local ownership requirement was unavoidable. While many joint ventures were successful, they often involved competing priorities, slower decision-making, and limitations on how quickly capital and technology could be deployed.

Those constraints have largely disappeared.

The timing is not accidental. India’s insurance market remains significantly underpenetrated compared with global standards. Insurance penetration currently stands at roughly 3.7% of GDP, well below the global average of around 7%. As India Briefing notes, that gap is precisely what makes India so attractive to global insurers. From their perspective, this is not a mature market fighting for marginal growth. It is one of the world’s largest untapped insurance opportunities.

There is another reason international players are paying attention. Reaching customers in India has become considerably easier than it was a decade ago. Digital distribution platforms, insurance aggregators, bancassurance partnerships, and mobile-first customer journeys have transformed how policies are sold and serviced. New entrants no longer need decades to build a nationwide physical presence before competing effectively.

For policyholders, the significance goes beyond ownership structures and investment rules. More capital entering the sector can support innovation, expand product availability, and increase competition. In theory, that should lead to better services and more choice. Whether it translates into lower premiums, faster claims, and improved customer experience depends on how insurers execute over the coming years.

What is clear, though, is that India’s insurance market has entered a new phase. The debate is no longer whether foreign insurers can participate. The question now is how they will compete, invest, and reshape the industry in a market that remains far from fully insured.

Also Read: Ayushman Bharat for Gig Workers 2026: Enrollment & Eligibility Guide

From 74% to 100%: The Sabka Bima, Sabki Raksha Act 2025 Explained

The move to 100% foreign ownership did not happen overnight. It was the result of a multi-year policy process that combined industry consultations, committee recommendations, and a broader government push to expand insurance coverage across the country.

The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025 received presidential assent on 20 December 2025 and officially came into force on 5 February 2026. Rather than making a single isolated change, the legislation rewrote key parts of India’s insurance framework by amending three foundational laws at the same time:

- The Insurance Act, 1938

- The Life Insurance Corporation Act, 1956

- The Insurance Regulatory and Development Authority Act, 1999

That scope alone makes the reform notable. This was not simply an FDI amendment. It was a broader effort to modernise how insurance businesses are licensed, regulated, capitalised, and distributed.

According to the Jindal School of Government and Public Policy’s analysis many of the reforms can be traced back to the Standing Committee on Finance’s 66th Report, released in February 2024. The committee argued that India needed a more flexible insurance ecosystem if it hoped to achieve deeper penetration and make insurance accessible to a much larger share of the population.

Several of those recommendations eventually found their way into the final legislation.

The path from proposal to implementation unfolded over more than a year. As documented by Nishith Desai Associates the major milestones were:

- November 2024: The Ministry of Finance invited public feedback on the proposal to raise the FDI limit from 74% to 100%.

- February 2025: Budget 2025 formally announced the government’s intention to allow full foreign ownership, subject to conditions such as domestic investment of premiums.

- December 2025: Parliament passed the Sabka Bima Sabki Raksha Bill, followed by presidential assent on 20 December.

- 30 December 2025: Amendments to the Indian Insurance Companies (Foreign Investment) Rules, 2015 were officially notified.

- 2 February 2026: DPIIT issued Press Note No. 1 (2026 Series), incorporating the new 100% FDI framework into India’s Consolidated FDI Policy.

- 5 February 2026: The core provisions of the Act became operational.

While the FDI change received most of the headlines, several other reforms introduced by the Act may prove just as important over the long term.

Composite Licensing

Historically, insurers had to choose their lane. A company could operate as a life insurer or a general insurer, but not both. The new framework allows composite licensing, meaning a single insurer can offer life, health, and general insurance products under one roof.

For consumers, that could eventually translate into simpler product bundles and a more integrated insurance experience.

A More Flexible Capital Framework

Previously, insurers faced a uniform minimum capital requirement of ₹100 crore regardless of their size or business model.

The new legislation introduces a differentiated framework. Smaller entities such as micro-insurers, cooperatives, and specialised insurers can operate with capital requirements that better reflect their actual risk profile and scale.

This change is especially important for underserved markets, where smaller, more focused insurers may be able to reach customers that larger players have historically ignored.

Perpetual Registration for Intermediaries

Insurance intermediaries no longer need to navigate annual registration renewals. Instead, they can receive perpetual certificates of registration, reducing administrative burdens and allowing them to focus more on serving customers and expanding distribution.

It sounds like a technical adjustment, but in practice it removes a layer of recurring regulatory friction from the industry.

Broader Recognition of Insurance Intermediaries

The Act also expands how insurance intermediaries are defined and regulated. One notable addition is the formal recognition of Managing General Agents (MGAs), a model that has played an important role in insurance innovation across several mature markets.

Recognising these entities creates room for new distribution models and specialised insurance businesses to emerge.

The Policyholders’ Education and Protection Fund

Perhaps the most consumer-focused reform in the package is the creation of a statutory Policyholders’ Education and Protection Fund.

The fund is financed through penalties imposed by IRDAI and is designed to support consumer awareness initiatives while helping facilitate the return of unclaimed policyholder funds. In other words, money collected through regulatory enforcement is redirected toward strengthening policyholder protection rather than simply disappearing into the broader system.

Taken together, these reforms reveal the bigger picture. The Sabka Bima Sabki Raksha Act is not merely about allowing foreign ownership. It is an attempt to build a more flexible, competitive, and scalable insurance sector capable of reaching a far larger share of India’s population.

The 100% FDI provision may be the headline-grabber, but the supporting reforms are what will ultimately determine how much the industry changes over the next decade.

Understanding the “Automatic Route” for Foreign Investors

For most policyholders, the phrase automatic route sounds like regulatory jargon that belongs in a government notification rather than a conversation about insurance. Yet this seemingly technical change is one of the most important parts of the 2026 reforms because it directly affects how quickly new insurers can enter the market and invest in India.

At its simplest, the automatic route removes a layer of bureaucracy.

As explained in the analysis by IMI Global, India traditionally offered two pathways for foreign investment:

| Route | Process | Timeline |

| Government Route (old) | Prior approval required from the central government | Often several months |

| Automatic Route (new) | No prior approval required; investor complies with regulations and notifies authorities after investment | Typically weeks |

Under the earlier framework, larger foreign investments often triggered additional approval requirements. Even after finding the right local partner and structuring a deal, investors could face lengthy review processes before moving forward.

The new system is considerably more straightforward.

A foreign insurer can now establish or acquire a wholly owned Indian insurance business without first waiting for government clearance, provided it complies with applicable laws, IRDAI regulations, and foreign investment rules. Instead of seeking permission before investing, the investor completes the investment and follows the required post-investment reporting procedures.

For global insurance groups, that distinction matters a great deal.

Investment decisions are often made within strict timelines. Large multinational insurers compare opportunities across dozens of countries at the same time. Markets that involve complex approval processes can struggle to compete for capital when alternatives offer a more predictable path. By shifting insurance to the automatic route, India has effectively reduced one of the major friction points that previously discouraged or delayed investment.

The reform is also notable for what it does not do.

India has not abandoned oversight. Instead, it has shifted the focus from ownership restrictions to governance requirements.

As confirmed by Insurance Business Magazine a fully foreign-owned insurer must still ensure that at least one of the chairperson, managing director, or CEO is a resident Indian citizen. Compared with previous requirements around board composition and management residency, this is a significant relaxation, but it still preserves a degree of local accountability.

The thinking behind this approach is fairly straightforward. Policymakers are no longer primarily concerned with limiting foreign ownership. Instead, they want to ensure that insurers operating in India remain subject to Indian regulation, Indian supervision, and Indian legal accountability.

For policyholders, the automatic route is important because it shortens the distance between investment decisions and real-world improvements.

A foreign insurer that wants to launch a new product, build a digital claims platform, expand distribution, or inject additional capital into its Indian operations can now move more quickly than before. There are fewer structural hurdles, fewer approval delays, and fewer ownership constraints to navigate.

That does not mean consumers will see immediate changes overnight. Insurance markets tend to evolve gradually. New entrants need time to build operations, recruit staff, design products, and establish distribution networks.

What the automatic route does is create the conditions for those changes to happen faster.

Instead of spending years negotiating joint venture arrangements and navigating approval cycles, insurers can focus their attention on what actually matters to customers: launching products, improving service, investing in technology, and competing for business.

In that sense, the automatic route is not just an investment reform. It is a speed reform. It reduces the time between capital entering the country and consumers seeing the benefits of that capital in the marketplace.

Direct Impact of 100% FDI on Your Insurance Policies

How will FDI affect my insurance policy?

This is the question most people care about. Regulatory reforms, investment rules, and ownership structures are interesting, but they only matter if they eventually affect the policy sitting in your drawer or the premium being deducted from your bank account every month.

So, will 100% FDI make your insurance better?

The answer depends on the timeframe.

In the short term, very little changes. Your existing policy remains exactly what it was before the reform. Your coverage, benefits, exclusions, maturity values, and claim rights do not suddenly change because foreign ownership rules have changed.

The bigger effects are likely to emerge over the next three to five years as insurers respond to increased competition, fresh capital, and new technology investments.

If the reform works as intended, policyholders should gradually see three major benefits:

- More competitive pricing in certain insurance segments

- Faster and more efficient claims processing

- A wider range of insurance products tailored to different customer needs

Let’s look at each of those in more detail.

Will Foreign Competition Lower Insurance Premiums?

Competition is one of the strongest forces affecting insurance prices.

When a market is dominated by a relatively small group of established players, pricing tends to stabilise around existing industry norms. New entrants often disrupt that balance because they need a compelling reason for customers to switch.

Price is usually one of the first tools they use.

As more global insurers enter India or expand their presence through wholly owned subsidiaries, pressure on premiums is likely to increase in several categories. Insurers looking to build market share often compete through a mix of pricing, product innovation, and customer experience.

International examples suggest this can have a meaningful impact.

As Aranca notes in its analysis Brazil experienced increased product diversity, stronger competition, and more sophisticated risk management after relaxing foreign ownership restrictions in its insurance sector. Domestic insurers did not disappear. Instead, they adapted, improved efficiency, and responded to the new competitive environment.

India could follow a similar path.

Another factor is underwriting sophistication.

According to Khaitan & Co, full ownership gives global insurers greater freedom to deploy their proprietary underwriting systems, risk models, and technology platforms.

That matters because better underwriting often leads to more accurate pricing.

Traditionally, insurers have grouped customers into relatively broad risk categories. More advanced systems can analyse a much wider set of variables, helping insurers distinguish lower-risk customers from higher-risk ones with greater precision.

When risk is priced more accurately, some customers benefit from lower premiums.

Areas where pricing competition could become especially noticeable include:

- Health insurance, where lifestyle factors and medical data play a major role in risk assessment

- Term life insurance, where long-term actuarial expertise can create pricing advantages

- Commercial and SME insurance, where specialised international underwriting experience may allow insurers to price risks more confidently

On the other hand, some categories are unlikely to see dramatic changes in the near future.

These include:

- Motor third-party insurance, where pricing remains regulated by IRDAI

- Government-backed crop insurance schemes, where policy objectives often influence pricing more than market competition

One important caveat: lower premiums may not be the first thing consumers notice.

Many foreign insurers entering a new market focus initially on service quality, digital experiences, and product differentiation rather than aggressive price-cutting. Winning customer trust can be just as important as offering the cheapest policy.

As a result, policyholders may see improvements in convenience and customer experience before they see substantial reductions in premiums.

Changes to Claim Settlement Ratios and Processes

If premiums are what attract customers, claims are what determine whether an insurer truly delivers on its promise.

Most people rarely think about their insurance policy until they need to make a claim. That moment often defines their entire perception of the insurer.

This is where the 100% FDI reform could produce some of the most visible benefits.

Many global insurers have spent years investing in claims infrastructure, automation, fraud detection, and digital servicing tools. Those systems have matured in highly competitive markets where speed and customer satisfaction are critical.

Some of the technologies already common in developed insurance markets include:

- AI-powered claim triage, which automatically identifies straightforward claims and routes them for quicker processing

- Advanced fraud detection systems, which help reduce fraudulent claims that ultimately increase costs for honest policyholders

- Automated claim payouts, allowing eligible claims to be settled with minimal manual intervention

- Digital document verification, reducing paperwork and speeding up the review process

Anyone who has ever waited weeks for documents to be verified or repeatedly submitted paperwork already knows why these improvements matter.

Technology alone is not the whole story, though.

As noted in the Skadden’s, the reforms also create stronger incentives for foreign insurers to invest heavily in their Indian operations. With greater ownership control and more flexibility around profits, parent companies have a stronger business case for committing capital to long-term operational improvements.

At the same time, IRDAI has strengthened its enforcement powers.

The regulator can now impose higher penalties and order disgorgement of wrongful gains in cases of misconduct. Money collected through these penalties flows into the Policyholders’ Education and Protection Fund, creating a direct connection between regulatory enforcement and consumer protection.

The Act also increases transparency around regulatory decision-making by requiring public consultation and disclosure of responses during rulemaking processes.

Taken together, stronger regulation and stronger competition create pressure from both sides. Regulators push insurers to meet standards, while competitors push them to improve customer experience.

For policyholders, that combination could translate into faster settlements, better communication, and more reliable claims handling.

What Happens to Existing Policies with Indian Insurers?

For current policyholders, perhaps the most reassuring fact is also the simplest:

Nothing changes immediately.

If you already hold a policy with LIC, a public sector insurer, or a private insurer, your contract remains fully valid. The FDI reforms do not alter policy terms, reduce benefits, change maturity values, or weaken your legal rights as a policyholder.

The effects become relevant only as the market evolves.

There are three situations where you may begin to notice the impact.

Scenario 1: Your insurer receives new foreign investment

Fresh capital generally strengthens an insurer’s balance sheet. A better-capitalised insurer is often better positioned to invest in technology, expand service capabilities, and maintain financial resilience during periods of stress.

From a policyholder’s perspective, that is usually a positive development.

Scenario 2: New competitors enter your segment

Competition tends to benefit customers even when they never switch providers.

If new insurers enter the market with attractive pricing or better service, existing insurers often respond by improving their own offerings. When your policy comes up for renewal, you may find yourself with more options and greater negotiating power.

Scenario 3: Your insurer is acquired or merged

The Sabka Bima Sabki Raksha Act introduces a formal framework allowing insurance companies to merge with non-insurance entities, subject to regulatory approval.

If your insurer is acquired by a foreign group or becomes part of a larger organisation, IRDAI must review and approve the transaction. Policyholder interests are part of that review process.

Most importantly, your existing policy cannot simply be rewritten because ownership changes. Material changes to policy terms require appropriate approvals and, where necessary, policyholder consent.

For consumers, this means ownership may change, branding may change, and service models may evolve, but the contractual protections attached to your existing policy remain intact.

Ultimately, the biggest effect of 100% FDI is unlikely to be felt through existing policies. The real impact will be seen in the policies sold tomorrow: products that are more competitive, more personalised, and potentially much easier to buy, manage, and claim against than those available today.

IRDAI Safeguards: Is Your Money Safe with Foreign-Owned Insurers?

One of the first concerns people raise when they hear about 100% foreign ownership is a simple one: Is my money still safe?

It’s a fair question.

If an insurance company is entirely owned by a foreign group, what happens if that parent company faces financial trouble overseas? Could profits be prioritised over policyholders? And does greater foreign ownership mean weaker protection for Indian consumers?

The short answer is no. While the ownership rules have changed significantly, the regulatory safeguards protecting policyholders remain firmly in place. In several areas, they have actually become stronger.

The 2026 reforms were designed to open the sector to more capital and competition, not to dilute consumer protection. IRDAI continues to supervise insurers operating in India, regardless of who owns them, and every insurer must still comply with the same prudential and governance standards.

Let’s look at the key safeguards that remain in force.

Resident Management Requirements and Strict Solvency Margins

A major concern with foreign ownership is accountability. Policymakers addressed this by ensuring that fully foreign-owned insurers still maintain a meaningful leadership presence within India.

As confirmed by Insurance Business Magazine, every Indian insurer, including those that are 100% foreign-owned, must have at least one resident Indian citizen serving as either the chairperson, managing director, or CEO.

That requirement is more important than it might initially appear.

It ensures that a senior decision-maker remains directly accountable under Indian law, operates within IRDAI’s supervisory framework, and understands the realities of the local market. While ownership may sit overseas, leadership accountability cannot be entirely outsourced.

Financial safety, however, depends on more than governance.

Insurance ultimately works because insurers maintain enough capital to honour claims even during difficult periods. That’s where solvency requirements come in.

IRDAI requires insurers to maintain prescribed solvency margins designed to ensure they can meet future obligations. These requirements apply equally to domestic and foreign-owned insurers.

If an insurer’s solvency position weakens, IRDAI can intervene through enhanced supervision, corrective measures, restrictions on business growth, or other regulatory actions.

In other words, foreign ownership does not exempt an insurer from financial discipline.

The reforms also accelerate India’s transition toward a Risk-Based Capital (RBC) framework, targeted for implementation by April 2026.

Under the current model, insurers generally maintain a solvency ratio of 150% of the regulatory control level. The RBC framework takes a more tailored approach. Rather than applying the same capital formula to every insurer, capital requirements are calibrated according to the specific risks each company carries.

As highlighted by the Jindal Policy Research Lab this allows regulators to align capital requirements more closely with actual risk exposure, creating a more resilient and efficient system.

For policyholders, the practical takeaway is straightforward: insurers with riskier portfolios will be required to hold more capital, strengthening their ability to absorb shocks and pay claims.

Premium Reinvestment Safeguard

One of the most important protections introduced alongside the FDI reforms concerns the treatment of premiums collected from Indian policyholders.

A common fear is that foreign owners might simply move large amounts of money out of the country once they gain full control.

The legislation specifically addresses this concern.

Premiums collected in India must continue to be invested within India. The funds supporting policyholder obligations remain inside the Indian insurance entity and are subject to IRDAI’s investment regulations.

This means that the money backing your policy is not freely transferable to a parent company abroad.

The assets supporting future claims remain available within the regulated Indian insurance framework.

For policyholders, this is a crucial distinction. Ownership can be global, but the funds underpinning policyholder obligations remain locally regulated and protected.

Stronger Enforcement Powers

The reforms did not merely preserve IRDAI’s authority. They expanded it.

One notable change is the regulator’s ability to order disgorgement of wrongful gains. In simple terms, if an insurer profits from misconduct, IRDAI can require those gains to be surrendered.

This is more than a financial penalty.

Traditional fines sometimes become just another cost of doing business. Disgorgement removes the economic benefit of wrongdoing altogether, creating a stronger deterrent against misconduct.

The Act also increases the financial consequences of regulatory violations and channels penalty proceeds into the Policyholders’ Education and Protection Fund.

That creates an interesting feedback loop: enforcement actions against insurers ultimately contribute to initiatives designed to protect and educate consumers.

The reforms also adjust ownership oversight.

The threshold requiring IRDAI approval for share transfers has increased from 1% to 5%, reducing administrative burden for minor transactions while ensuring that significant ownership changes still receive regulatory scrutiny.

Why These Safeguards Matter

When viewed together, the protections form multiple layers of defence rather than relying on a single mechanism.

Policyholders benefit from:

- A mandatory resident Indian leader in the insurer’s top management structure

- IRDAI-mandated solvency requirements, with a shift toward risk-based capital standards

- Rules requiring premiums collected in India to remain invested within India

- Regulatory approval for material ownership changes

- Expanded enforcement powers and a stronger consumer-protection framework

The broader point is worth emphasising.

The 100% FDI reform allows foreign ownership, but it does not reduce regulatory oversight. In many respects, India has chosen a model that combines greater openness with stronger supervision.

For policyholders, the safety of an insurer still depends primarily on its capital strength, solvency position, governance standards, and regulatory compliance, not simply on whether its shareholders are domestic or foreign.

The ownership structure may have changed. The safeguards protecting policyholders remain very much intact.

The 20% Cap on LIC: Why the State Insurer Remains Protected

While the 2026 reforms opened most of India’s insurance sector to full foreign ownership, one institution remains in a category of its own: the Life Insurance Corporation of India, better known as LIC.

That distinction was deliberate.

LIC is not just another insurance company competing in the market. It occupies a unique place in India’s financial system, serving millions of policyholders across urban and rural India while also playing a significant role in the broader economy. Because of that status, lawmakers chose a different approach when redesigning the foreign investment framework.

The result is simple: although private insurers can now attract up to 100% foreign ownership, LIC continues to operate under a separate limit.

As documented by SCC Times, foreign investment in LIC remains capped at 20% under the automatic route.

That cap was preserved through amendments to the LIC Act alongside the broader insurance reforms. In practical terms, it means no foreign investor can acquire a controlling position in LIC, either individually or collectively. The Indian government continues to hold the dominant stake and retains control over the corporation’s strategic direction.

For policyholders, that continuity matters.

Many LIC customers view the insurer differently from private-sector competitors. The organisation has long been associated with stability, government backing, and a presence that extends deep into rural and semi-urban India. The reforms do not alter that perception or the underlying ownership structure supporting it.

If you already hold an LIC policy, the message is straightforward: the safeguards and institutional backing that existed before the FDI reforms remain unchanged.

At the same time, LIC has not been left entirely untouched by the legislative overhaul.

The new framework gives the corporation greater operational flexibility in certain areas. As India Briefing notes, LIC has been granted additional freedom to establish zonal offices, manage overseas operations more efficiently, and align certain activities with international regulatory requirements.

In other words, LIC gains some of the benefits of modernisation without being exposed to full foreign ownership.

From a policy perspective, this reflects a balancing act.

On one hand, the government wants more competition, more capital, and greater innovation across the insurance industry. On the other, it wants to preserve a large public-sector institution that continues to serve strategic and social objectives.

That role becomes especially visible in parts of India where insurance penetration remains low.

LIC’s distribution network reaches towns and villages that many private insurers still struggle to serve profitably. Its extensive agent network and longstanding presence have allowed it to build relationships in regions where private-sector competition remains relatively limited.

This matters because expanding insurance coverage is not only about attracting investment. It’s also about reaching people who have historically remained outside the formal insurance system.

By retaining control of LIC while opening the broader market, policymakers appear to be pursuing a dual-track strategy:

- Encourage competition and innovation through private and foreign-owned insurers.

- Preserve a strong public-sector insurer capable of supporting long-term policy goals and broad-based financial inclusion.

That combination is not unusual internationally.

Several advanced economies maintain large state-linked financial institutions even while allowing substantial competition in the private sector. The idea is that public institutions can provide stability and continuity while private players drive innovation and efficiency.

In India’s case, LIC remains that anchor institution.

The broader insurance market may become more global, more competitive, and more technologically advanced over the coming years. Yet LIC’s position as a government-controlled insurer remains largely intact.

For policyholders, that means greater choice without losing the option of a state-backed insurer. For the market as a whole, it creates an interesting dynamic: a protected public giant competing alongside increasingly sophisticated domestic and international players.

How that competition evolves may ultimately shape the next phase of India’s insurance story.

New Insurance Products and InsurTech Innovations in 2026

The 100% FDI reform is often discussed in terms of ownership and investment, but for most consumers, the more interesting question is this: What new products and services will actually become available because of it?

That’s where the real transformation could happen.

Insurance reforms matter most when they change what people can buy, how easily they can access coverage, and whether products are designed for the realities of their lives. The 2026 framework has the potential to do all three.

Two developments stand out in particular:

- The growth of micro-insurance and sachet-sized products for underserved populations.

- The introduction of more sophisticated underwriting models powered by global expertise and technology.

Together, these shifts could make insurance more accessible, more personalised, and more relevant to millions of Indians who have traditionally been left out of the market.

The Rise of Micro-Insurance and Sachet Products

One of the biggest challenges facing India’s insurance sector is not competition. It’s access.

Despite years of growth, a large portion of the population remains uninsured or underinsured. Many people simply do not fit the customer profile around which traditional insurance products were built.

Conventional policies often assume stable monthly incomes, long-term financial planning, and the ability to commit to annual premiums. For daily-wage earners, migrant workers, small farmers, and informal-sector employees, those assumptions frequently break down.

The new regulatory framework aims to address that gap.

As explained by the Jindal Policy Research Lab, the Act replaces the old one-size-fits-all ₹100 crore capital requirement with a more flexible structure. This makes it easier for specialised insurers, micro-insurance providers, cooperatives, and niche players to enter the market.

That may sound like a technical change, but it has significant practical implications.

When smaller insurers can operate sustainably, they can build products around the needs of specific communities rather than trying to serve everyone through a standardised model.

This is where sachet insurance comes into the picture.

Think of it as insurance designed to match how people actually live and spend.

Examples could include:

- A farmer purchasing crop protection for a particularly high-risk week during monsoon season for ₹50 through a mobile app.

- A traveller adding accident coverage for a single flight during the booking process.

- A migrant worker activating short-term hospitalisation coverage that renews automatically through UPI.

- A flood insurance product that pays out automatically when rainfall exceeds a predefined threshold, without requiring a traditional claim process.

These products may seem unconventional when compared with traditional annual policies, but they address a basic reality: many people need affordable, flexible protection rather than long-term commitments.

Global insurers have already developed similar models in several emerging and developed markets. With the removal of ownership restrictions, they can now bring those product structures into India more efficiently and adapt them to local conditions.

The introduction of composite licensing strengthens this opportunity even further.

An insurer can now offer multiple types of coverage through a single customer interaction. A rural customer purchasing crop insurance, for example, could also be offered a low-cost life cover or health product through the same distribution channel.

That creates efficiencies for insurers and greater convenience for customers.

How Global Underwriting Expertise Will Change Risk Assessment

Insurance pricing is ultimately a prediction exercise.

Every premium reflects an insurer’s estimate of how likely a future claim might be.

The more accurately an insurer can assess risk, the more precisely it can price a policy.

Historically, Indian insurers have often relied on relatively broad risk categories. That approach works, but it can also result in customers paying premiums that do not fully reflect their individual circumstances.

The next phase of innovation is likely to change that.

Global insurers entering India bring decades of experience in advanced underwriting, predictive analytics, and data-driven risk assessment.

Some of the technologies already used extensively in mature insurance markets include:

| Technology | Application | Consumer Benefit |

| Telematics | Motor insurance based on actual driving behaviour | Safer drivers can pay lower premiums |

| Wearable integration | Health pricing linked to activity levels and wellness metrics | Healthy behaviour can be rewarded financially |

| Satellite monitoring | Agricultural risk assessment and verification | Faster and more accurate crop claims |

| AI claim triage | Automated review of straightforward claims | Faster settlements |

| Predictive health analytics | Early identification of health risks | Better prevention and potentially lower long-term costs |

As noted in the IPMI Global analysis, full ownership makes it easier for global insurers to deploy their proprietary technology platforms and underwriting systems in India without the governance complexities that often accompany joint ventures.

The practical impact for consumers could be substantial.

A customer who exercises regularly, maintains good health indicators, or demonstrates safer driving habits may increasingly be rewarded through lower premiums or enhanced benefits.

In other words, insurance pricing may become more personalised.

That shift also benefits the broader market.

When insurers can distinguish risk more accurately, low-risk customers are less likely to subsidise higher-risk customers. Pricing becomes more efficient, and insurers can expand coverage without exposing themselves to excessive uncertainty.

Composite licensing may amplify this trend.

An insurer that provides both life and health coverage can develop a more complete understanding of a customer’s risk profile, subject to appropriate consent and data protection requirements. That broader perspective can support more competitive bundled products and create stronger incentives for insurers to invest in preventive health and wellness programmes.

A healthier customer is, after all, a better customer from an insurer’s perspective.

China’s experience offers an interesting comparison.

As highlighted by Aranca, the removal of foreign ownership caps in China’s insurance sector enabled global insurers to introduce their full technology ecosystems into the market. Domestic insurers remained dominant, but innovation accelerated significantly and customer expectations evolved alongside it.

India’s insurance market is different in many respects, but the underlying lesson remains relevant.

Ownership reform by itself does not improve insurance products.

What matters is what follows: new ideas, new technology, better risk assessment, and products designed around customer needs rather than legacy structures.

That is where policyholders are likely to feel the most meaningful effects of the 2026 reforms over the years ahead.

Foreign Ownership and Employment: What the Reform Means for Jobs

Whenever a sector opens up to greater foreign investment, the conversation eventually turns to jobs.

Will more investment create employment? Will automation replace workers? Will global companies bring opportunities or simply make existing businesses leaner?

The reality is more nuanced than either extreme.

In India’s insurance sector, the overall employment outlook appears positive. The reason is fairly straightforward: expanding insurance coverage across a country of more than a billion people requires people. Lots of them. New capital and technology will change how insurers operate, but they are also likely to accelerate growth in areas where human relationships and local knowledge remain essential.

The effects, however, will not be evenly distributed across every part of the industry.

Distribution and Agency Networks

One of the clearest beneficiaries of increased insurance penetration is the distribution ecosystem.

Insurance remains a relationship-driven business, particularly outside major metropolitan areas. While digital platforms continue to grow, a large share of customers still rely on agents, advisors, and intermediaries to explain products, compare options, and guide them through the purchasing process.

As foreign-owned insurers enter the market or existing players expand their operations, demand for distribution capacity is likely to rise.

This is particularly true in underserved regions.

Reaching customers in rural and semi-urban India is rarely as simple as launching an app. It often requires people who understand local communities, speak regional languages, and can explain insurance concepts in ways that resonate with first-time buyers.

Micro-insurance products are a good example.

Selling a ₹50 crop insurance product or a short-term health policy may generate smaller commissions than traditional policies, but reaching millions of previously uninsured individuals requires a vast distribution network. That expansion naturally creates opportunities for agents, advisors, and local insurance intermediaries.

The introduction of composite licensing could strengthen this trend.

Rather than selling a single type of policy, agents may increasingly be able to offer multiple insurance solutions through one customer relationship. A customer discussing crop coverage, for example, might also explore health or life insurance options during the same interaction.

That makes insurance distribution more productive and potentially more profitable for agents operating in smaller markets.

Demand for Skilled Professionals

Beyond frontline distribution, the reform is expected to create opportunities for highly skilled professionals across the insurance ecosystem.

Global insurers entering India do not simply bring capital. They bring operating models, compliance requirements, technology platforms, and risk-management frameworks that require specialised expertise.

As a result, demand is likely to increase for:

- Actuaries

- Data scientists

- Risk analysts

- Compliance specialists

- Legal professionals

- Cybersecurity experts

- Technology implementation teams

- Product development specialists

In particular, the transition toward a Risk-Based Capital framework creates new technical demands that were less prominent under the previous regulatory structure.

Modern insurance increasingly relies on advanced analytics and sophisticated risk modelling. As insurers become more data-driven, professionals capable of interpreting and managing that data become increasingly valuable.

For young professionals considering careers in insurance, the sector may look very different over the next decade than it did over the previous one.

The Automation Question

Of course, not every employment trend points in the same direction.

One concern often raised is that global insurers tend to be highly technology-driven. Automated underwriting, AI-assisted claims processing, digital servicing tools, and advanced analytics can reduce the need for certain back-office functions.

There is some truth to that concern.

Tasks that once required large teams can often be completed more efficiently through automation. Claims verification, document processing, customer onboarding, and routine administrative functions are all areas where technology is increasingly taking over repetitive work.

But context matters.

India is not a mature insurance market struggling to maintain growth. It is a rapidly expanding market with a significant protection gap.

That distinction changes the equation.

While automation may reduce staffing requirements in certain operational functions, overall industry growth is expected to create demand elsewhere. Expanding into underserved regions, launching new products, building distribution channels, and supporting millions of first-time policyholders requires substantial human involvement.

In many cases, technology changes jobs rather than eliminates them.

The industry may need fewer people performing repetitive administrative tasks, but more people focused on customer engagement, risk management, analytics, compliance, and product innovation.

The Bigger Picture: Insurance for All by 2047

The government’s broader objective provides important context for understanding the employment impact of these reforms.

The vision of “Insurance for All by 2047” is ambitious. Achieving it would require dramatically increasing insurance penetration from current levels and extending meaningful coverage to populations that have historically been underserved.

That kind of expansion does not happen through investment alone.

It requires:

- Larger distribution networks

- More trained insurance professionals

- Better claims infrastructure

- Localised product development

- Expanded customer education efforts

- Greater presence in Tier 2 and Tier 3 cities

Each of those areas generates employment opportunities.

For that reason, most analysts expect the net employment effect of the reform to be positive, even as technology reshapes certain functions within the industry.

The jobs created may not look exactly like the jobs of the past. They are likely to be more technology-enabled, more specialised, and more closely integrated with data and digital tools.

But if the reforms succeed in expanding insurance coverage at the scale policymakers envision, the sector’s workforce is likely to grow alongside it.

In that sense, the employment story is closely tied to the broader insurance story. More customers, more products, and more distribution inevitably require more people, even in an increasingly digital world.

Can a Foreign Company Fully Own an Indian Insurance Business Now?

The short answer is yes.

As of 5 February 2026, a foreign company can own 100% of an Indian insurance company without obtaining prior approval from the central government. That marks one of the most significant changes in the history of India’s insurance sector and removes a restriction that had shaped the industry for more than two decades.

But while the headline is simple, the details are worth understanding.

This is not a free-for-all where ownership comes without obligations. Full foreign ownership is now permitted, but insurers must still operate within a carefully structured regulatory framework designed to protect policyholders and maintain financial stability.

What Exactly Changed?

Under the previous regime, foreign investors could hold up to 74% of an Indian insurance company. The remaining stake had to be owned by Indian investors or promoters.

That requirement often created a balancing act.

Many global insurers wanted greater control over strategy, technology deployment, capital allocation, and long-term planning, but they still needed local partners to satisfy ownership rules. In some cases, those partnerships worked extremely well. In others, differing priorities created friction and slowed decision-making.

The 2026 reforms removed that ownership ceiling.

Today, a foreign insurer can establish or acquire an Indian insurance business and own the entire company, provided it complies with applicable regulations.

The change applies across much of the insurance ecosystem, including:

- Life insurance companies

- General insurance companies

- Health insurers

- Reinsurers

- Insurance brokers

- Corporate agents

- Third-party administrators (TPAs)

- Web aggregators and digital insurance platforms

In practical terms, global insurers now have the same ownership flexibility in India that they enjoy in many other major markets.

How Does the Process Work?

One reason the reform has attracted so much attention is that ownership is now permitted through the automatic route.

That means investors do not need to seek prior government approval before completing an investment.

Instead, they must comply with relevant regulations and complete the required reporting and notification procedures after the investment takes place.

For global companies evaluating opportunities across multiple countries, this significantly simplifies the process.

It also reduces uncertainty.

Investment decisions that might previously have taken months to navigate can now move forward much more quickly, making India a more attractive destination for long-term insurance capital.

What Conditions Still Apply?

Although ownership restrictions have been removed, several important safeguards remain.

Foreign-owned insurers must continue to comply with all applicable laws and regulatory requirements, including:

- At least one of the chairperson, managing director, or CEO must be a resident Indian citizen.

- The insurer must maintain prescribed solvency margins and comply with all IRDAI regulations.

- Premium income collected in India must remain invested within India.

- Material ownership changes remain subject to regulatory oversight, with IRDAI approval required for significant share transfers.

These requirements reflect the broader philosophy behind the reform.

India has chosen to liberalise ownership without weakening supervision. The focus has shifted from controlling who owns insurers to regulating how insurers operate.

For policyholders, that distinction is important.

A company may be foreign-owned, but it remains subject to Indian law, Indian regulatory oversight, and Indian consumer-protection requirements.

The Major Exception: LIC

There is one notable exception to the 100% ownership framework.

LIC continues to operate under a separate regime.

As SCC Times documents, foreign investment in LIC remains capped at 20% under the automatic route.

That means the country’s largest insurer remains firmly under government control, even as the rest of the private insurance sector becomes fully open to foreign ownership.

For private insurers, however, the landscape has fundamentally changed.

Why This Matters Beyond Ownership

The significance of 100% ownership goes beyond who appears on a company’s share register.

Control influences how quickly insurers can make decisions, how much capital they are willing to invest, and how aggressively they pursue growth.

According to AZB & Partners, the reforms represent the most extensive overhaul of India’s insurance framework in roughly two decades.

Industry observers are already seeing increased interest from foreign insurers that previously held minority stakes in Indian joint ventures. As Grant Thornton Bharat notes, several international insurers are evaluating whether full ownership now makes strategic sense.

That interest is not merely theoretical.

S&P Global Market Intelligence reported that India and Japan emerged as major insurance M&A hubs in the Asia-Pacific region during 2025, a trend expected to continue as the new framework matures.

For consumers, this means ownership changes, acquisitions, and strategic restructuring may become increasingly common over the coming years.

The important point is that these developments are occurring within a regulated framework designed to preserve policyholder protections.

So, can a foreign company fully own an Indian insurance business now?

Absolutely.

The more interesting question is what those companies choose to do with that freedom. The answer to that question will shape the next chapter of India’s insurance industry and determine how much of the reform’s promised benefits ultimately reach policyholders.

Frequently Asked Questions : 100% FDI in Indian insurance Sector

No, your existing policy remains entirely unaffected. The transition to 100% foreign ownership does not alter your current premiums, maturity values, claim rights, or existing coverage terms. Your current contract with your insurer remains legally binding and protected.

Yes, your funds are highly secure. The IRDAI strictly mandates that all premiums collected in India must be reinvested within India. Furthermore, 100% foreign-owned insurers must maintain the exact same rigorous solvency margins as domestic companies to guarantee claims are paid.

The automatic route removes bureaucratic delays, allowing global insurers to deploy capital faster. For policyholders, this translates to quicker access to innovative products, advanced AI-driven claims processing, and more competitive pricing fueled by an influx of fresh foreign investment.

No, LIC remains strictly capped at 20% FDI. The Life Insurance Corporation of India continues to operate under separate legislation. It retains its sovereign backing and government control to serve broader financial inclusion goals across India.

No, strict domestic governance rules apply. Regardless of the foreign ownership percentage, the law requires that at least one top executive (Chairperson, MD, or CEO) must be a resident Indian citizen, ensuring direct, local accountability to Indian regulators.

While immediate price drops are not guaranteed, increased market competition typically drives down premiums over time. You can expect better pricing precision and value, particularly in health and term life insurance, as global insurers introduce highly advanced underwriting technology to the Indian market.

What 100% FDI in Indian insurance Sector Means for You as a Policyholder

At its heart, the move to 100% FDI in India’s insurance sector is a bet on growth. More specifically, it’s a bet that greater access to global capital, technology, and expertise can help close the country’s enormous protection gap faster than the existing system could on its own.

For policymakers, the logic is fairly straightforward. India remains one of the world’s most underinsured large economies. Insurance penetration is still well below global averages, and hundreds of millions of people either have no coverage at all or rely on limited forms of protection. Reaching the government’s “Insurance for All by 2047” goal will require far more capital, innovation, and distribution capacity than the sector currently possesses.

The 2026 reforms are designed to unlock those resources.

For existing policyholders, however, the immediate takeaway is reassuringly uneventful.

Your current policy does not change because foreign ownership limits have changed. The benefits you signed up for remain the same. Your premium does not suddenly increase or decrease. Your rights as a policyholder remain protected by the same regulatory framework that existed before the reforms.

The more meaningful effects are likely to emerge gradually.

Over the coming years, policyholders may begin to notice:

- More competition among insurers

- Faster and more digital claim experiences

- A wider choice of products

- More personalised pricing in certain segments

- Greater investment in customer service and technology

- New forms of coverage tailored to underserved communities

These improvements will not appear overnight. Insurance is a long-cycle industry. New entrants need time to establish operations, recruit teams, secure distribution partnerships, and build customer trust.

But the direction of travel is clear.

The reform is particularly significant for people who have historically been excluded from traditional insurance markets. Daily-wage earners, migrant workers, small farmers, and individuals in rural areas often fall outside the reach of conventional insurance models. The emergence of micro-insurance providers, sachet products, parametric covers, and more flexible distribution channels could help bring protection to millions of people who previously had few realistic options.

That may ultimately become the most important legacy of the reform.

It’s also worth remembering that the Sabka Bima Sabki Raksha Act goes far beyond foreign investment.

The legislation introduces a series of structural changes that work together:

- Composite licensing allows insurers to offer multiple categories of insurance through a single entity.

- A differentiated capital framework lowers barriers for specialised and micro-insurance providers.

- Expanded intermediary definitions create room for new business models and distribution channels.

- Perpetual registrations reduce regulatory friction.

- The Policyholders’ Education and Protection Fund strengthens consumer protection and awareness initiatives.

Viewed together, these changes form a broader modernisation effort rather than a standalone FDI policy.

Just as importantly, the government has paired liberalisation with safeguards.

The resident leadership requirement, solvency regulations, premium reinvestment rules, enhanced IRDAI enforcement powers, and continued protection of LIC all reflect an attempt to balance openness with accountability.

As Alvarez & Marsal observed, the framework allows full foreign ownership while preserving safeguards specifically intended to protect policyholders.

That balance may prove critical.

India has not simply opened the doors and stepped aside. Instead, it has created a framework in which insurers, whether domestic or foreign-owned, must compete under regulatory oversight for the trust of Indian consumers.

And competition, more often than not, benefits customers.

When a public-sector giant like LIC competes with a global insurer bringing decades of specialised expertise, and both are challenged by agile private players and digital-first InsurTech firms, policyholders gain leverage. Companies have stronger incentives to improve service, streamline claims, innovate products, and price risk more effectively.

The winners are unlikely to be the insurers themselves.

The winners will be the individuals and families who gain access to better financial protection.

That said, the story is not finished.

Several implementation steps are still unfolding. As Nishith Desai Associates notes, harmonisation between the revised FDI policy and certain FEMA-related provisions remains a work in progress. At the same time, IRDAI is expected to introduce additional regulations covering areas such as composite licensing, risk-based capital, and product frameworks.

According to the Angel One report, those regulations are expected to take shape within the months following the Act’s implementation.

In many ways, the legislation has laid the foundation rather than completed the project.

The framework is now in place. The capital can enter. The ownership restrictions have been removed. The regulatory architecture has been redesigned.

What happens next will depend on how insurers, regulators, investors, and consumers respond.

But if the reforms deliver on their intended objectives, the long-term outcome should be a more competitive, more innovative, and more accessible insurance market. One that serves not only the customers who already have coverage, but also the millions who still need it.

That, ultimately, is what the 2026 reforms are trying to achieve. A larger insurance sector, certainly. But more importantly, a more inclusive one.

Disclaimer:

This article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Policy terms, premium calculations, and regulatory conditions are subject to change. Readers should consult a qualified insurance advisor or IRDAI-registered professional for guidance specific to their situation.

Discussion (2)

Leave a Reply