ITR e-Filing 2026: A Step-by-Step Guide for AY 2026-27 (New Rules)

ITR e-Filing 2026: Essential Updates and New Rules for AY 2026-27

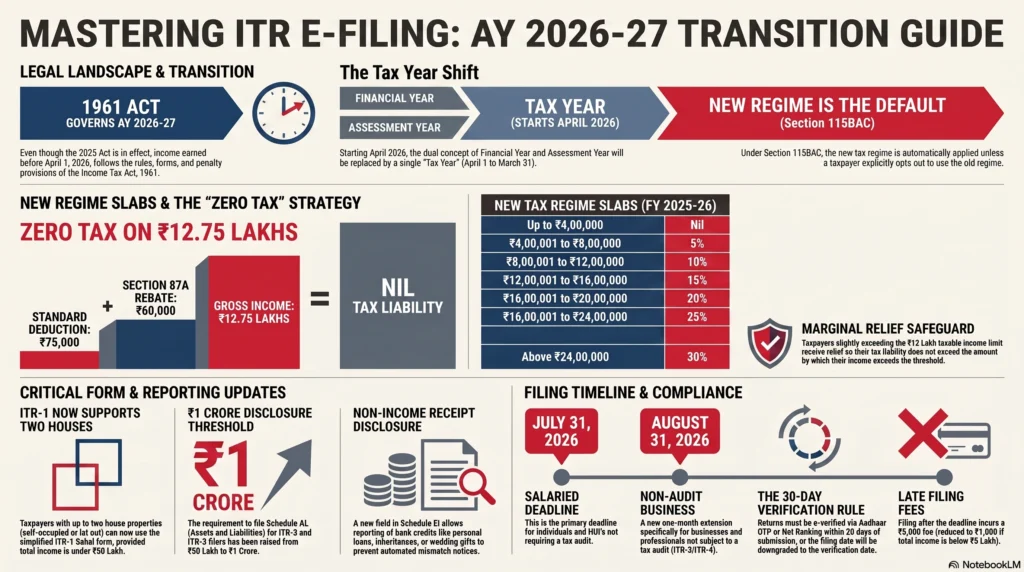

Filing your income tax return for Assessment Year 2026-27 comes with a few more twists than usual. India’s tax system is in the middle of a significant transition and hence there are certain key facts about ITR e-Filing 2026 which you should know. While the new Income Tax Act, 2025 has officially come into effect, the return you’re filing this year for income earned during FY 2025-26 is still governed by the old law.

That alone has created plenty of confusion. Add to it the expanded scope of ITR-1, a higher threshold for reporting assets and liabilities, and a brand new disclosure field for receipts that aren’t considered income, and it’s easy to see why many taxpayers are looking for clarity before they begin.

This guide breaks everything down in plain English. You’ll learn what’s changed for AY 2026-27, how to choose the right ITR form based on your income, and how to complete the entire e-filing process, from logging into the portal to successfully e-verifying your return.

At A Glance: ITR e-Filing 2026

· Applicable Law: AY 2026-27 (FY 2025-26) returns are still governed by the Income Tax Act, 1961, despite the introduction of the new 2025 Act.

· Zero Tax Threshold: The New Tax Regime is the default option, enabling zero tax on a ₹12.75 lakh salary by combining the ₹75,000 standard deduction with the Section 87A rebate.

· Expanded ITR-1 Eligibility: Taxpayers can now report income from up to two house properties using the simplified ITR-1 (Sahaj) form.

· AIS Mismatch Prevention: A new form field for “Receipts not in the nature of income” allows taxpayers to declare non-taxable credits (e.g., gifts, loans) to prevent automated scrutiny.

· Schedule AL Relaxation: The mandatory asset and liability reporting threshold (for ITR-2 and ITR-3) has been increased from ₹50 lakh to ₹1 crore.

· Key Filing Deadlines: Returns must be filed by July 31, 2026 for salaried individuals and August 31, 2026 for non-audit businesses to avoid Section 234F penalties.

· Strict 30-Day e-Verification: Submitted returns are only legally valid once verified via Aadhaar OTP or Net Banking within 30 days of upload.

Understanding the Income Tax Landscape for AY 2026-27 (FY 2025-26)

This filing season is slightly unusual because two different income tax laws are technically in force at the same time. The important thing to remember is that only one of them applies to the return you’re filing now. Understanding that distinction will save you a lot of unnecessary confusion before you even open the ITR utility.

The Shift from Assessment Year to “Tax Year” Under Income Tax Act 2025

For decades, taxpayers in India have worked with two separate terms: the Financial Year, when income is earned, and the Assessment Year, when that income is reported and taxed. The Income Tax Act, 2025 simplifies this system by replacing both with a single term called the “Tax Year,” which runs from 1 April to 31 March. The change is explained in detail by ClearTax. Going forward, income earned from April 2026 onwards will simply be reported for “Tax Year 2026-27,” without the separate assessment year that traditionally followed a year later.

That said, this new terminology does not affect the return you’re filing now. Income earned between April 2025 and March 2026 continues to follow the existing Financial Year and Assessment Year framework, so it must still be filed as Assessment Year 2026-27. The Income Tax Department has clarified this transition in its official FAQ.

In simple terms, if you’re filing your return during 2026, you can continue using the familiar Financial Year and Assessment Year terminology. The new “Tax Year” concept only comes into play for income earned from FY 2026-27 onwards, with those returns being filed in 2027.

Disclaimer: This article is intended for general informational purposes only and does not constitute tax or legal advice for any individual’s specific circumstances. Tax rules, thresholds, and portal procedures are subject to revision through CBDT notifications, so readers should verify current details on the official e-filing portal or consult a qualified chartered accountant before filing. Neither the author nor the publication accepts liability for decisions made solely on the basis of this guide.

Which Law Applies? Income Tax Act 1961 vs. Income Tax Act 2025

Although the Income Tax Act, 2025 officially replaced the Income Tax Act, 1961 from 1 April 2026, that doesn’t mean every return filed after that date falls under the new law. For AY 2026-27, the position is straightforward. Since the income being reported was earned before 1 April 2026, the entire return continues to be governed by the Income Tax Act, 1961, even though the filing itself happens after the new legislation has come into force. The Income Tax Department has clarified this point.

This distinction goes beyond the filing process. Every aspect of your return for AY 2026-27, including the applicable ITR forms, section references, penalty provisions, and procedures for filing revised or belated returns, continues to follow the 1961 Act. Even if you receive a scrutiny notice or a defective return notice after 1 April 2026, it will still be dealt with under the old law because the income belongs to FY 2025-26.

The introduction of the new Act has generally been viewed as a welcome attempt to simplify India’s direct tax framework, a view reflected in this commentary . Behind the scenes, however, there have been several structural changes. Many familiar forms have been renumbered under the new legislation. For example, Form 16 now has a different corresponding form number under the Income Tax Act, 2025. The e-filing portal has also separated downloadable forms into two categories, one for the Income Tax Act, 2025 and another for the Income Tax Act, 1961. The official form mapping is available here.

For taxpayers filing AY 2026-27 returns, though, these backend changes don’t require any action. Every notified return form, from ITR-1 to ITR-7, continues to operate under the provisions of the Income Tax Act, 1961. In other words, while the tax law has changed on paper, your filing process for this assessment year remains largely the same as in previous years.

New Tax Regime vs. Old Tax Regime: Which Should You Choose?

Before your tax liability is calculated, there’s one important choice to make: should you file under the new tax regime or stick with the old one?

For AY 2026-27, the new tax regime continues to be the default option under Section 115BAC. That means if you don’t actively choose otherwise, your return will automatically be processed under the new regime. If you believe the old regime offers greater tax savings because of the deductions and exemptions available to you, you’ll need to opt out while filing your return.

Income Tax Slabs and Rates for FY 2025-26 (New Regime)

The income tax slabs announced in Budget 2025 continue to apply for FY 2025-26, and there have been no changes to the tax rates in Budget 2026. This means taxpayers filing returns for AY 2026-27 will use the same slab structure, as confirmed by ClearTax.

| Income Slab | Tax Rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

A 4% Health and Education Cess is payable in addition to the tax calculated under these slabs. The same rates are also listed in this detailed overview.

While seven tax slabs may seem more complicated than before, most salaried taxpayers don’t need to memorise every bracket. In practice, the bigger takeaway is that resident individuals with taxable income up to ₹12 lakh can effectively pay no income tax under the new regime because of the rebate available under Section 87A. We’ll look at how that works in the next section.

Standard Deduction and the Section 87A Rebate Explained

The new tax regime offers two major benefits that significantly reduce the tax burden for salaried employees and pensioners.

The first is the standard deduction of ₹75,000. Every salaried employee and pensioner is entitled to this deduction automatically. You don’t need to submit bills, receipts, or proof of investment. The amount is simply deducted from your gross salary before your taxable income is calculated.

The second benefit is the rebate available under Section 87A. For FY 2025-26, resident individuals whose net taxable income does not exceed ₹12,00,000 can claim a rebate of up to ₹60,000. This rebate can eliminate the entire tax liability if the calculated tax falls within that limit, making it one of the most significant relief measures introduced through Budget 2025, as discussed here.

Here’s how it works in practice. Once your taxable income is calculated, tax is computed using the applicable slabs. If that tax comes to ₹60,000 or less and your taxable income does not exceed ₹12 lakh, the rebate offsets the entire amount. As a result, your final tax liability becomes zero.

However, it’s important to understand one limitation. The rebate is available only for income taxed under the normal slab rates. Income that is taxed at special rates, such as certain short-term or long-term capital gains on listed equity shares, does not qualify for this benefit. There’s also another point to remember. By default, the rebate stops once taxable income crosses ₹12 lakh, although marginal relief helps soften that impact for taxpayers who exceed the limit by a small amount. We’ll cover that shortly.

How a ₹12.75 Lakh Salary Attracts Zero Tax Under the New Regime

The ₹12 lakh rebate limit often grabs the headlines, but salaried employees actually benefit from a slightly higher zero-tax threshold. That’s because the standard deduction and the Section 87A rebate work together.

Here’s the sequence. If your gross annual salary is ₹12,75,000, you first claim the standard deduction of ₹75,000. That reduces your taxable salary to exactly ₹12,00,000. Since your taxable income now falls within the eligibility limit for the Section 87A rebate, you can claim the full rebate and bring your tax liability down to zero.

The calculation looks like this:

- Gross salary: ₹12,75,000

- Less: Standard deduction: ₹75,000

- Taxable income: ₹12,00,000

- Tax as per applicable slabs: ₹60,000

- Less: Section 87A rebate: ₹60,000

- Final tax payable: Nil

This is why ₹12.75 lakh has become the figure many salaried taxpayers pay attention to during this filing season, rather than ₹12 lakh.

The same benefit extends to pensioners whose pension is taxed as salary income because they, too, are eligible for the standard deduction. Income from other sources, however, is treated differently. Earnings such as bank interest or rental income do not qualify for the ₹75,000 standard deduction and are added to your taxable income when determining whether you remain eligible for the Section 87A rebate.

Understanding Marginal Relief Calculation

Without marginal relief, a taxpayer earning just a little more than ₹12 lakh could end up paying far more tax than someone earning slightly less. To prevent that from happening, the tax law includes a safeguard known as marginal relief.

Take a simple example. Suppose your taxable income is ₹12,10,000. That’s only ₹10,000 above the rebate threshold. Under the normal slab calculation, once your income crosses ₹12 lakh, the entire Section 87A rebate is no longer available. As a result, your tax liability could jump to around ₹61,500 before cess.

Clearly, paying more than ₹61,000 in tax because your income increased by only ₹10,000 would be unfair. That’s where marginal relief steps in.

Instead of charging the full slab-based tax, marginal relief limits your tax liability to the amount by which your income exceeds ₹12 lakh. In this example, your tax would be capped at ₹10,000 before adding the applicable cess.

As income increases further, the benefit of marginal relief gradually reduces. Once taxable income reaches roughly ₹12.7 lakh to ₹12.75 lakh, the normal slab calculation becomes more favourable than the capped amount, and marginal relief effectively phases out. From that point onwards, tax is calculated under the regular slab rates without any additional adjustment.

Old Tax Regime Slabs and Available Deductions

Although the new tax regime is now the default, it isn’t automatically the better choice for everyone. Taxpayers who claim substantial deductions, such as home loan interest, House Rent Allowance (HRA), or investments under Chapter VI-A, may still find the old regime more tax-efficient.

For AY 2026-27, the old regime tax slabs remain unchanged and continue to apply as follows:

| Income Slab | Tax Rate |

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

A 4% Health and Education Cess is payable over and above the calculated tax.

The rebate under Section 87A is much smaller under the old regime. It is available only if your taxable income does not exceed ₹5,00,000, with the maximum rebate capped at ₹12,500.

Where the old regime continues to stand out is the range of deductions and exemptions it allows. Taxpayers can still claim benefits such as:

- HRA exemption

- Home loan interest deduction under Section 24(b)

- Section 80C deductions up to ₹1.5 lakh

- Section 80D deduction for health insurance premiums

- Standard deduction of ₹50,000 for salaried employees

Most of these deductions are not available under the new tax regime.

If you are a salaried employee or a pensioner without business income, you can choose between the old and new regimes every year while filing your return. Taxpayers with business or professional income have additional compliance requirements. They must submit Form 10-IEA to opt for the old regime and face stricter rules if they later decide to switch back.

Major Rule Changes and Updates for ITR Filing in 2026

Apart from deciding between the old and new tax regimes, taxpayers also need to be aware of several changes introduced in the ITR forms themselves. Some of these updates make filing easier for salaried individuals, while others are aimed at improving reporting accuracy and reducing unnecessary notices from the Income Tax Department.

ITR-1 Expanded Scope: Reporting Two House Properties

One of the most useful changes for AY 2026-27 is the expansion of ITR-1’s eligibility. Until last year, owning a second house property usually meant moving from the simple ITR-1 form to the more detailed ITR-2. That is no longer the case.

For this assessment year, taxpayers can report income from up to two house properties through ITR-1, whether those properties are self-occupied or let out. This is in addition to salary, pension, and other eligible income sources, as confirmed in the Income Tax Department’s filing manual.

This change is particularly helpful for individuals who own a second flat that has been inherited, purchased for family members, or jointly owned with someone else. As long as the other ITR-1 conditions are satisfied, including total income not exceeding ₹50 lakh and agricultural income staying within ₹5,000, there’s no need to switch to ITR-2 simply because of a second property.

That said, the eligibility limits haven’t disappeared altogether. You’ll still need to use ITR-2 if you own more than two house properties, have capital gains, hold unlisted equity shares, receive income covered under Section 194N, or if your total income exceeds ₹50 lakh. The same applies to taxpayers who fall under the high-value transaction reporting requirements, such as foreign travel expenses above ₹2 lakh, electricity bills exceeding ₹1 lakh, or current account deposits over ₹1 crore.

The New “Receipts Not in the Nature of Income” Field

Another notable addition this year is a new disclosure field within Schedule EI called “Receipts not in the nature of income.”

Its purpose is fairly straightforward. Not every amount credited to your bank account is taxable income, yet large credits often appear in the Annual Information Statement (AIS), which can sometimes trigger automated mismatch notices. This new field allows taxpayers to clearly distinguish genuine non-income receipts from taxable earnings.

Examples include:

- Personal loans received from banks or individuals

- Money inherited through a will

- Sale proceeds from personal belongings

- Gains from the sale of rural agricultural land

- Wedding gifts

- Gifts received from specified relatives

None of these receipts become taxable simply because they are reported here. The field is designed to improve transparency and help explain significant credits that may otherwise appear unexplained during automated processing.

At present, this disclosure option is available through the online filing portal and JSON-based utilities. It has not yet been incorporated into the notified PDF versions of the ITR forms. Even so, taxpayers should maintain proper supporting documents such as loan agreements, gift deeds, inheritance records, or wills. Keeping these records handy can make responding to any future query much easier.

Updated Allowances and HRA Exemption Cities (2026 Rules)

The Income Tax Rules, 2026 have also expanded the list of cities eligible for the higher House Rent Allowance exemption.

Previously, only Delhi, Mumbai, Kolkata, and Chennai qualified for the higher 50% HRA exemption limit. From 2026 onwards, Bengaluru, Pune, Hyderabad, and Ahmedabad have been added to that list, increasing the total number of eligible metro cities to eight. The revised list is detailed in this guide.

Taxpayers living in cities outside these eight metros will continue to calculate their HRA exemption using the existing 40% limit.

Another important compliance change relates to HRA claims themselves. Taxpayers must now disclose their relationship with their landlord while claiming HRA exemption. This additional disclosure is intended to discourage false or inflated rent claims, particularly where rent is shown as being paid to close family members.

The same set of rule changes has also increased the limits for several other allowances and perquisites, including:

- Children’s education allowance

- Hostel allowance

- Tax-free non-cash gifts from employers

- Employer-funded overseas medical treatment

These revisions are also covered here.

It’s worth remembering, however, that these benefits are relevant mainly for taxpayers who opt for the old tax regime. The new regime does not allow HRA exemption or most other salary-related exemptions, so these enhanced limits won’t affect taxpayers who continue under the default regime.

Higher Disclosure Threshold for Assets and Liabilities (Schedule AL)

Another welcome change affects taxpayers who file ITR-2 or ITR-3.

Earlier, anyone with total income above ₹50 lakh had to complete Schedule AL by disclosing details of assets such as property, vehicles, jewellery, investments, bank balances, and related liabilities. For AY 2026-27, that threshold has been increased to ₹1 crore.

As a result, taxpayers with annual income between ₹50 lakh and ₹1 crore are no longer required to furnish these disclosures, reducing the compliance burden for a sizeable group of individual filers.

Those whose income exceeds ₹1 crore must still complete Schedule AL. The information should reflect the position as on the last day of the financial year and include both movable and immovable assets, along with the liabilities attached to them. If an asset is jointly owned, only the taxpayer’s share needs to be reported.

Enhanced AIS and TIS Pre-Filled Data Integration

The Annual Information Statement (AIS) has become one of the most important documents to review before filing your return.

Unlike Form 26AS, which mainly captures tax deducted at source and tax collected at source, AIS brings together a much wider range of financial information. According to the Income Tax Department’s FAQ, it includes personal details, TDS and TCS records, Statement of Financial Transactions (SFT), tax payments, and various financial transactions reported by banks, employers, mutual funds, registrars, and other institutions.

Alongside AIS, taxpayers also receive the Taxpayer Information Summary (TIS). While AIS provides detailed transaction-level information, TIS consolidates those figures into summary amounts that are used for pre-filling your income tax return.

Even though much of the return is pre-populated, it should never be accepted without verification. Compare every entry with your Form 16, bank statements, interest certificates, dividend records, and broker statements before submitting your return.

If you notice an incorrect entry in AIS, you can submit feedback directly through the portal. The Department records both the original value and your modified value, and you can revise your feedback if needed. This process is explained in detail here..

Taking a few extra minutes to reconcile AIS and TIS before filing can save a great deal of trouble later. Tax professionals routinely recommend this step because mismatches between reported income and AIS data remain one of the most common reasons taxpayers receive notices after filing. Similar guidance is also available here.

Document Checklist: What You Need Before Filing Your ITR

A little preparation before you log into the e-filing portal can make the entire filing process much smoother. Having the necessary documents within reach means you won’t have to pause midway to hunt for a certificate or verify a figure. Since several fields in the return are validated against official records, keeping everything ready also reduces the chances of making avoidable mistakes.

Mandatory Identification and Bank Details

Before you begin filing, make sure you have the essentials in place.

Every taxpayer must have an active PAN linked with their Aadhaar. You’ll also need at least one bank account that has been pre-validated on the Income Tax Department’s e-filing portal so that any eligible refund can be credited without delay. These requirements are listed in the Department’s ITR-1 filing manual.

It’s equally important to ensure that your registered mobile number and email address are up to date. Many verification methods, especially Aadhaar OTP, rely on these details, and outdated contact information can slow down the filing process when you’re ready to submit your return.

Income Proofs: Form 16, Form 16A, and AIS/TIS

Your income documents form the backbone of your tax return, so it’s worth taking a few minutes to gather them before you start.

If you’re a salaried employee, keep your Form 16 issued by your employer ready. It contains details of your salary, tax deducted at source, and other important information required for filing. If tax has been deducted on income other than salary, such as bank interest or professional fees, you’ll also need Form 16A. Both documents are discussed here.

You should also download the following from the income tax portal before filing:

- Form 26AS

- Annual Information Statement (AIS)

- Taxpayer Information Summary (TIS)

Comparing these records with your bank statements, interest certificates, and investment statements is one of the best ways to spot discrepancies before the Department does. This reconciliation process is strongly recommended in this guide because it significantly reduces the likelihood of receiving a mismatch notice later.

Depending on your sources of income, you may also need:

- Interest certificates from banks or post offices

- Dividend statements

- Capital gains statements issued by your broker or mutual fund house

Having these documents ready makes it much easier to report every income source accurately.

Investment Proofs and Deduction Certificates (If Opting for Old Regime)

If you’ve chosen the old tax regime, you’ll need documents to support every deduction you claim.

For example, keep investment proofs for Section 80C deductions such as ELSS investments, PPF contributions, or life insurance premiums. If you’re claiming deductions under Section 80D, retain your health insurance premium receipts. Homeowners claiming interest on a housing loan should have the lender’s interest certificate ready under Section 24(b). Similarly, taxpayers claiming HRA exemption should keep rent receipts and, where applicable, the landlord’s PAN details. These deductions are outlined in this guide.

The good news is that you don’t have to upload these documents while filing your return. However, that doesn’t mean you can discard them. If the Income Tax Department seeks clarification or selects your return for verification, you’ll be expected to produce supporting evidence. Keeping your records organised from the outset is far easier than trying to collect them months after filing.

Selecting the Correct ITR Form for Your Income Profile

Choosing the right ITR form is more important than many taxpayers realise. Filing with the wrong form doesn’t simply delay processing. It can make your return defective. If the mistake isn’t corrected within the time allowed by the Income Tax Department, the return may be treated as though it was never filed. That’s why it’s worth spending a few minutes confirming which form matches your income profile before you begin. The Department’s guidance on this is explained here.

| ITR Form | Broadly Suited To |

| ITR-1 (Sahaj) | Resident individuals with salary or pension income, up to two house properties, income from other sources, and total income up to ₹50 lakh |

| ITR-2 | Individuals or HUFs with capital gains, foreign assets, more than two house properties, or total income above ₹50 lakh without business income |

| ITR-3 | Individuals or HUFs earning business or professional income, including partners in firms |

| ITR-4 (Sugam) | Individuals, HUFs, and firms (excluding LLPs) opting for presumptive taxation with total income up to ₹50 lakh |

ITR-1 (Sahaj): For Salaried Individuals and Pensioners

ITR-1 continues to be the simplest return form available and is the one used by most salaried taxpayers. Much of the information, including salary details from Form 16 and TDS credits from Form 26AS, is pre-filled, making the filing process relatively straightforward.

For AY 2026-27, you can use ITR-1 if all of the following conditions are met:

- You are a resident individual.

- Your total income does not exceed ₹50 lakh.

- Your income comes from salary or pension.

- You have income from up to two house properties.

- Your other income consists of sources such as savings account interest, fixed deposit interest, or family pension.

- Agricultural income does not exceed ₹5,000.

These eligibility conditions are confirmed in the official filing manual.

However, ITR-1 isn’t suitable for every taxpayer. You’ll need to move to another form if you:

- Are a non-resident or resident but not ordinarily resident.

- Are a director in a company.

- Hold unlisted equity shares.

- Have any capital gains during the financial year.

- Need to carry forward or set off losses.

- Cross the prescribed thresholds for specified high-value transactions, such as foreign travel, electricity consumption, or current account deposits.

Even a small capital gain from redeeming a mutual fund or selling a few shares is enough to make ITR-1 inapplicable. In such cases, ITR-2 becomes the correct form regardless of how simple the rest of your income may be.

ITR-2: For Capital Gains, Buyback Losses, and Foreign Income

ITR-2 is meant for individuals and Hindu Undivided Families (HUFs) who don’t have business or professional income but don’t qualify for ITR-1 either.

This form generally applies if you have:

- Capital gains from property, shares, mutual funds, or other assets.

- More than two house properties.

- Foreign assets or foreign income.

- Total income above ₹50 lakh without business income.

- Unlisted equity shares.

- Company directorships.

- Non-resident or resident but not ordinarily resident status.

These eligibility rules are outlined in this guide.

One area that deserves special attention this year is share buybacks.

For FY 2025-26, buyback proceeds continue to be treated as deemed dividend and taxed according to the shareholder’s applicable slab rate. At the same time, the original purchase cost of the shares becomes a capital loss that can be reported through ITR-2 and, where permitted, adjusted against other capital gains.

This treatment changes only from FY 2026-27 onwards, when buyback proceeds will instead be taxed directly as capital gains. Since you’re filing for AY 2026-27, the earlier rules still apply. More details are available here.

Compared with ITR-1, ITR-2 includes additional schedules for reporting short-term and long-term capital gains, foreign assets, foreign income, and Schedule AL where the asset disclosure threshold of ₹1 crore is applicable.

ITR-3 and ITR-4 (Sugam): For Business and Professional Income

Taxpayers earning income under the head “Profits and Gains of Business or Profession” generally need to file ITR-3.

This includes business owners, freelancers, consultants, doctors, lawyers, architects, and partners who receive salary or profit share from a partnership firm. Depending on the size and nature of the business, ITR-3 may also require profit and loss statements, balance sheets, and audit-related disclosures. The eligibility criteria are explained here.

ITR-4, also known as Sugam, offers a much simpler alternative for eligible taxpayers who opt for the presumptive taxation scheme.

Broadly, it can be used by:

- Businesses with turnover up to ₹3 crore under Section 44AD, provided the prescribed proportion of receipts is digital.

- Professionals with gross receipts up to ₹75 lakh under Section 44ADA.

- Eligible taxpayers covered under Section 44AE, including qualifying goods carriage operators.

These limits are confirmed in this guide.

It’s worth noting that taxpayers who become ineligible for presumptive taxation, either because they exceed the turnover limits or choose to opt out, will generally have to shift to ITR-3 for AY 2026-27. Once you exit the presumptive scheme, switching back isn’t always straightforward, so it’s a decision that should be made carefully.

Step-by-Step Guide to e-Filing Your ITR on the Income Tax Portal

Once you’ve selected the correct ITR form and gathered all the necessary documents, the actual filing process is fairly straightforward. Whether you choose to file directly on the e-filing portal or use the offline JSON utility, the overall flow remains much the same.

Step 1: Logging in to the e-Filing Portal

The process starts on the Income Tax Department’s e-filing portal. Existing users can log in using their PAN as the user ID along with their password, while first-time users will need to complete a one-time registration using their PAN before they can proceed. The Department explains the login process.

Once you’re logged in, it’s worth checking the latest notifications on the portal. The homepage confirms that ITR-1 to ITR-4 for AY 2026-27 are available for both online filing and through the Excel and JSON utilities, as shown at https://www.incometax.gov.in/iec/foportal/.

Step 2: Selecting the Assessment Year and Filing Mode

After logging in, navigate to e-File > Income Tax Returns > File Income Tax Return.

When prompted, select Assessment Year 2026-27, since you’re reporting income earned during FY 2025-26. You’ll then be asked whether you want to file your return online or use the offline Excel or JSON utility. The official filing manual.

If you choose the offline option, you’ll first need to download the appropriate utility, complete the return on your computer, generate the JSON file, and upload it back to the portal. Choosing the online option allows you to continue filling out the return directly in your browser without any downloads.

Step 3: Verifying Pre-Filled Data from AIS/TIS

Once you’ve selected the appropriate ITR form and your filing status, the portal automatically fills in much of your information using data from AIS, TIS, and Form 26AS.

This can save a significant amount of time, but it shouldn’t replace a careful review. Always compare the pre-filled figures with your Form 16, bank statements, interest certificates, and investment records. Since the information comes from third-party reporting, occasional errors, omissions, or duplicate entries are still possible. This verification step is strongly recommended in this guide.

If you notice an incorrect entry in your AIS, avoid simply overwriting the amount in your return. Instead, submit feedback through the AIS portal itself. That creates an official record of the discrepancy and helps explain any differences if the Department later reviews your return.

Step 4: Declaring Additional Income and Exempt Receipts

Not every source of income appears automatically in the pre-filled return.

If you’ve earned additional bank interest, rental income, or any other taxable income that hasn’t been reported through AIS or Form 26AS, you’ll need to enter those details manually.

This is also the stage where you should use the new “Receipts not in the nature of income” field in Schedule EI, wherever applicable. Amounts such as loans received, inheritances, or gifts that are not taxable income should be disclosed here rather than being reported under an income head. Doing so helps present a more accurate picture of your finances and can reduce the chances of unnecessary queries later.

Step 5: Claiming Deductions and Calculating Tax Liability

If you’ve opted for the old tax regime, this is where you’ll enter deductions under Chapter VI-A, including claims under Sections 80C, 80D, 80G, HRA, and other eligible provisions, using the supporting documents you’ve already gathered.

Taxpayers filing under the new regime will notice that most deduction fields are unavailable. Only a limited number of deductions, such as the employer’s contribution to NPS under Section 80CCD(2) and contributions to the Agniveer Corpus Fund under Section 80CCH, remain eligible. These restrictions are explained in the ITR-1 filing manual.

After all the required information has been entered, the portal automatically calculates your tax liability based on the regime you’ve selected. It applies the relevant tax slabs, rebate, cess, and any eligible deductions before displaying the final amount payable or refundable.

Step 6: Paying Self-Assessment Tax (If Applicable)

If the final calculation shows that tax is still payable after adjusting TDS and any advance tax already paid, the portal gives you the option to pay immediately through the integrated e-Pay Tax facility.

Although you can choose “Pay Later,” paying the outstanding amount before submitting your return is generally the better approach. Filing without clearing the balance can result in interest being charged under Sections 234B and 234C for late or short payment of tax. The Department highlights this in its filing manual.

Step 7: Submitting the Income Tax Return

Before the return is submitted, the portal displays a complete preview for your review. Take a few moments to go through every section carefully. If the system detects any missing information or validation errors, you’ll be asked to correct them before you can continue.

Once all validations are cleared, you can submit the return. An acknowledgement is generated immediately, and you’ll be taken to the verification screen.

It’s important to remember that submission alone doesn’t complete the filing process. Your return is considered complete only after it has been successfully verified. The Department’s filing guide describes this sequence at https://www.incometaxindia.gov.in/tax-services/file-income-tax-return.

How to e-Verify Your ITR (And Why It Is Mandatory)

Submitting your income tax return is only part of the process. Your return isn’t treated as valid until it has been successfully verified. In fact, if you skip this final step, the Income Tax Department considers the return as not filed at all, regardless of whether every other detail was filled in correctly.

That’s why it’s a good idea to complete e-verification immediately after submission instead of leaving it for later.

e-Verification via Aadhaar OTP

For most taxpayers, Aadhaar OTP is the quickest and easiest way to verify an ITR.

Once you choose this option, an OTP is sent to the mobile number linked with your Aadhaar. Enter the OTP on the verification screen, and your return is verified within minutes. The Income Tax Department lists Aadhaar OTP as one of the approved verification methods.

Before you begin filing, make sure the mobile number registered with UIDAI is active and accessible. A surprising number of taxpayers discover only at the last moment that their registered number has changed, which can delay verification and create unnecessary stress close to the filing deadline.

e-Verification via Net Banking and EVC

If Aadhaar OTP isn’t convenient, there are several other approved ways to verify your return.

You can generate an Electronic Verification Code (EVC) through:

- Net banking

- A pre-validated bank account

- A pre-validated demat account

Taxpayers who already use a Digital Signature Certificate (DSC) can also verify their returns using that method. These options are explained by the Department.

There’s also an “e-Verify Later” option, but it should be used carefully. Selecting it allows you to submit the return without completing verification immediately. However, you’ll still need to verify the return within the prescribed time limit. If electronic verification isn’t possible, you can print the signed ITR-V acknowledgement and send it by speed post to the Centralised Processing Centre (CPC) in Bengaluru.

The 30-Day Verification Deadline Rule

Whichever verification method you choose, the deadline remains the same. Your return must be verified within 30 days of uploading it.

Under Notification No. 2 of 2024, the timing of verification also determines the official filing date. If you complete verification within the 30-day window, your original upload date is treated as the date on which the return was furnished.

However, if verification happens after those 30 days, the verification date itself becomes the official filing date. This can have serious consequences because any delay is measured from that later date, potentially triggering late filing implications. The Department explains this rule in its ITR-1 filing manual.

The most important takeaway is simple: don’t postpone verification. It’s one of the easiest steps in the filing process, yet it’s also one of the most commonly overlooked. Completing it immediately after submitting your return ensures your filing is legally valid and allows the Income Tax Department to begin processing your return without unnecessary delay.

Due Dates, Late Fees, and Penalties for AY 2026-27

Missing an income tax deadline can cost more than just a late fee. Depending on when you file, you could also lose certain tax benefits, face interest on unpaid taxes, or limit your options for correcting mistakes later. Knowing the important dates in advance makes it much easier to avoid these issues.

Important Filing Deadlines Based on Taxpayer Category

Different categories of taxpayers have different filing deadlines. Here’s a quick reference for AY 2026-27:

| Taxpayer Category | Applicable Forms | Due Date |

| Individuals/HUFs, salaried, no audit | ITR-1, ITR-2 | 31st July 2026 |

| Business/profession, non-audit cases | ITR-3, ITR-4 | 31st August 2026 |

| Taxpayers requiring tax audit | ITR-3, ITR-5, ITR-6 | 31st October 2026 |

| Transfer pricing cases | ITR-3, ITR-5, ITR-6 | 30th November 2026 |

| Belated return | All forms | 31st December 2026 |

| Revised return | All forms | 31st March 2027 |

| Updated return (ITR-U) | ITR-U | Within 48 months from end of AY |

These due dates are confirmed in this guide.

One notable change this year benefits business owners and professionals who are not subject to a tax audit. They now have until 31st August 2026 to file ITR-3 or ITR-4, giving them an additional month compared with salaried taxpayers. The extension recognises that business income returns generally require more detailed preparation.

Section 234F Penalties for Missing the Deadline

If you miss the original due date, you can still file a belated return until 31st December 2026. However, doing so comes with financial consequences.

Under Section 234F:

- Taxpayers with total income above ₹5 lakh may have to pay a late filing fee of ₹5,000.

- Taxpayers with total income up to ₹5 lakh may have to pay a reduced late filing fee of ₹1,000.

These penalties are confirmed here.

The late fee isn’t the only cost. If any tax remains unpaid after the original due date, Section 234A also levies interest at 1% per month or part of a month until the outstanding tax is paid.

Filing late can affect more than your immediate tax bill. In most cases, you lose the ability to carry forward business losses and capital losses to future years, although house property losses continue to enjoy more favourable treatment. A delayed filing history may also create practical difficulties when applying for loans or visas, where financial compliance is often reviewed. These consequences are discussed at https://cleartax.in/s/due-date-tax-filing.

FAQ: ITR e-Filing 2026

Even though the new Income Tax Act, 2025 is active, your returns for AY 2026-27 (FY 2025-26) are still strictly governed by the Income Tax Act, 1961. The new “Tax Year” rules only apply to income earned from April 2026 onwards.

By claiming the ₹75,000 standard deduction, your gross salary drops to a taxable income of exactly ₹12,00,000. This makes you fully eligible for the Section 87A rebate, which completely offsets your tax liability, bringing your final tax payable to zero.

Yes. Starting this filing season, the eligibility rules have been expanded. You can now safely report income from up to two house properties (whether self-occupied or rented out) using ITR-1, provided your total income remains under ₹50 lakh without any capital gains.

For salaried individuals and HUFs whose accounts do not require a tax audit, the mandatory filing deadline is July 31, 2026. Missing this critical date will attract late filing penalties under Section 234F of up to ₹5,000, plus interest on unpaid dues.

For AY 2026-27, the mandatory asset disclosure threshold for taxpayers filing ITR-2 and ITR-3 has been significantly relaxed. You are now only required to report your assets and liabilities if your total annual income exceeds ₹1 crore.

Absolutely. Your income tax return is not considered legally filed until it is verified. You must complete this step using Aadhaar OTP, EVC, or Net Banking within a strict 30-day window of submitting your return.

How to File a Revised Return or Updated Return (ITR-U)

Finding a mistake after submitting your return doesn’t necessarily mean you’re stuck with it.

If you’ve already filed your return, you can submit a revised return under Section 139(5) any time up to 31st March 2027, or before the assessment is completed, whichever happens first. This option is available whether your original return was filed on time or as a belated return. The timelines are confirmed here.

The process is relatively simple. Log in to the e-filing portal, choose the option to file a revised return under Section 139(5), enter the acknowledgement number of your original return, make the necessary corrections, submit the revised return, and complete e-verification within the prescribed 30-day period. A step-by-step explanation is also available here.

If the window for filing a revised return has already closed, there’s still another option in some cases.

An Updated Return (ITR-U) under Section 139(8A) can generally be filed for up to 48 months from the end of the relevant assessment year. For AY 2026-27, that means taxpayers can usually file an updated return until 31st March 2031, subject to the applicable conditions and payment of additional tax, which increases depending on how late the update is filed.

It’s important to remember that ITR-U isn’t meant to reduce your tax liability or increase a refund. It cannot be used to claim a fresh refund, declare a lower tax payable, or increase previously reported losses. It also becomes unavailable once certain assessment or search proceedings have begun. For that reason, it’s best viewed as a corrective measure rather than a substitute for filing an accurate return the first time.

Disclaimer

This article is intended for general informational purposes only and does not constitute tax or legal advice for any individual’s specific circumstances. Tax rules, thresholds, and portal procedures are subject to revision through CBDT notifications, so readers should verify current details on the official e-filing portal or consult a qualified chartered accountant before filing. Neither the author nor the publication accepts liability for decisions made solely on the basis of this guide.

Leave a Reply