How Direct Benefit Transfer (DBT) Saved ₹3.48 Lakh Crore in India

How DBT Transformed Welfare Efficiency in India

If you zoom out and look at India’s public finance story over the last decade or so, the Direct Benefit Transfer (DBT) system stands out, not because it’s flashy, but because it quietly fixed something that had been leaking for years.

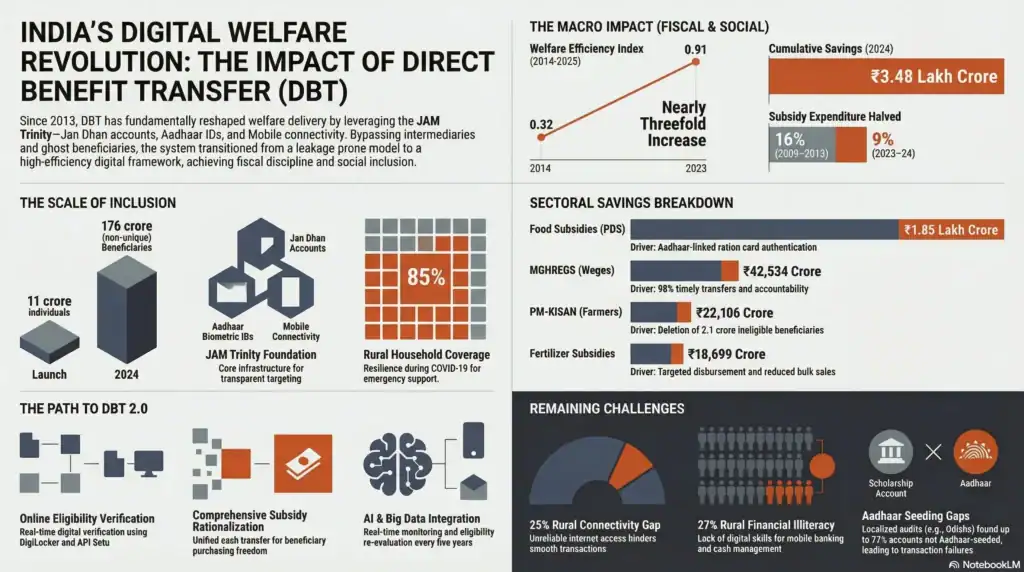

As of early 2025, the system has saved about ₹3.48 lakh crore. That’s not a small rounding error; it’s roughly 1.5% of the national budget that would’ve otherwise slipped away into the usual cracks. And importantly, this wasn’t achieved by cutting welfare or tightening the purse strings.

The money was always being spent. It just wasn’t reaching the right people.

For a long time, welfare delivery in India moved through layers like middlemen, local officials, informal “fixers.” Somewhere along that chain, funds would thin out. Sometimes a little and often, a lot. Duplicate entries, ghost beneficiaries, inflated lists, it all added up to a system that bled quietly but constantly.

So, when people ask, DBT saved how much money? There’s now a clear, evidence-backed answer: ₹3.48 lakh crore and still rising, as reported by the Ministry of Electronics and Information Technology and supported by analysis from the BlueKraft Digital Foundation.

But the number, big as it is, almost feels like the less interesting part.

What really changed is how the state interacts with people. DBT stripped out the intermediaries and replaced them with something far less visible but far more reliable, digital infrastructure. Money now moves straight from government accounts into verified bank accounts, without any detours or quiet deductions along the way.

And there’s a human side to that shift that doesn’t show up neatly in data tables. Before DBT, getting what you were entitled to often meant negotiating, waiting, sometimes even paying a bribe for your own benefit. That’s not just inefficiency, but that’s indignity. The new system, at least in principle, removes that layer. You don’t ask, but you receive.

This post takes a closer look at that transformation, not just the headline savings, but the machinery underneath it: how DBT is built, how it performs, where it still falls short, and what its next phase might look like.

India’s DBT Revolution: At a Glance

I. The Scale & Impact

- Q1. What is Direct Benefit Transfer (DBT)?

A “logistical marvel” (per the IMF) that transfers subsidies and welfare directly into beneficiaries’ bank accounts using the JAM Trinity (Jan Dhan, Aadhaar, Mobile), cutting out middlemen. - Q2. How much has DBT saved the Indian exchequer?

As of 2025, DBT has saved ₹3.48 lakh crore by eliminating leakages, ghost beneficiaries, and systemic inefficiencies. - Q3. What is the total volume of funds transferred?

Over ₹43.95 lakh crore has been successfully disbursed across 300+ central schemes since 2013. - Q4. Which sectors saw the most significant savings?

- PDS (Food): ₹1.85 lakh crore (53% of total savings) by deleting 5.87 crore fake ration cards.

- PAHAL (LPG): ₹73,846 crore saved through 4.23 crore eliminated duplicate connections.

- MGNREGS: ₹58,059 crore saved by removing 1.26 crore invalid job cards.

II. Efficiency & Growth

- Q5. How has welfare efficiency improved?

The Welfare Efficiency Index (WEI)—which measures beneficiary growth against subsidy costs—jumped from 0.32 (2014) to 0.91 (2023). - Q6. How many people does DBT cover today?

Coverage has expanded 16-fold, from roughly 11 crore beneficiaries in 2014 to over 176 crore (cumulative enrollments) today. - Q7. Has DBT reduced the government’s subsidy burden?

Yes. Subsidies as a percentage of total government expenditure dropped from 16% (pre-2013) to 9% (2024), allowing for better fiscal management without cutting benefits.

III. Challenges & The Road Ahead

- Q8. What are the primary hurdles remaining?

Key challenges include transaction failure rates (approx. 1.47%), data silos between departments, and ensuring biometric “exclusion risks” are minimized for the elderly or manual labourers. - Q9. What is “DBT 2.0”?

The shift toward online eligibility verification, using platforms like DigiLocker to eliminate physical paperwork for citizens. - Q10. What is the vision for “DBT 3.0”?

Moving toward a National Social Registry for “proactive outreach”—where the government identifies and delivers benefits automatically to eligible citizens before they even apply. - Q11. What is the key takeaway?

DBT has transformed India’s welfare from a “leaky bucket” into a precision-targeted system, ensuring that ₹1 sent by the government results in ₹1 reaching the intended bank account.

The Transformation: Pre-DBT vs. Post-DBT

| Metric | Pre-DBT (Traditional Welfare) | Post-DBT (The Digital Revolution) |

| Primary Mechanism | Cash, cheques, or physical goods through local offices. | Direct electronic bank transfers via the JAM Trinity. |

| Intermediary Involvement | High: Multiple middlemen, contractors, and local officials. | Zero: Direct Government-to-Person (G2P) transfers. |

| Beneficiary Verification | Manual, paper-based records (vulnerable to tampering). | Digital authentication via Aadhaar/Biometrics. |

| Beneficiary Base | ~11 Crore (2014) | ~176+ Crore (2024 cumulative) |

| Subsidy Burden | ~16% of total Government Expenditure. | ~9% of total Government Expenditure (2024-25). |

| Efficiency (WEI) | 0.32 Welfare Efficiency Index (2014). | 0.91 Welfare Efficiency Index (2023). |

| Systemic Leakage | High: Millions of ghost/duplicate accounts. | ₹3.48 Lakh Crore saved through leakage elimination. |

Evolution of DBT in India: From Pilot to Nationwide System

The Direct Benefit Transfer (DBT) system didn’t arrive fully formed. It started, somewhat quietly, on January 1, 2013, when the United Progressive Alliance government rolled out pilot programs across 43 districts. The idea was straightforward—almost deceptively so: instead of pushing welfare funds through a long administrative chain, just send the money directly to people’s bank or postal accounts.

Simple in theory. Messy in execution, at least at the beginning.

Before DBT, India’s welfare system had a reputation that economists summed up rather bluntly: a “leaking bucket.” One estimate from the 2017–18 Economic Survey suggested that only about 15 paise of every rupee actually reached the intended beneficiary. The rest drifted. Sometimes siphoned off, sometimes stuck in bureaucratic delays, sometimes just lost in a system no one fully controls.

And if you’ve ever spoken to someone who depended on those benefits back then, the stories tend to sound the same—partial payments, unexplained delays, or being told to “come back next week” until the process itself wore you down.

The real push came after 2014, when the National Democratic Alliance government expanded DBT far more aggressively. What began as a pilot started turning into infrastructure. By 2023, the system had scaled to cover more than 300 Central Government schemes and over 2,000 State schemes. That’s not incremental growth but saturation-level expansion.

In total, DBT transfers have crossed ₹43.3 lakh crore, placing India among the largest direct welfare transfer systems anywhere in the world.

Now here’s the part that’s easy to miss unless you stop and think about it.

Back in 2009–10, India’s welfare budget was about ₹2.1 lakh crore. Fast forward to 2023–24, and that number has jumped to ₹8.5 lakh crore, roughly four times larger. You’d expect inefficiencies to scale with it. Historically, they usually do.

But instead, the share of spending lost to subsidies actually dropped. Not because subsidies disappeared, but because they became tighter, cleaner, harder to game. That shift is directly tied to DBT’s expansion.

So, the story here isn’t just “we spent more” or “we saved money.” It’s that India managed to expand welfare significantly while reducing waste—a combination that, honestly, most systems struggle to pull off.

And it didn’t happen overnight. It came from slowly replacing an old, human-heavy distribution model with something more system-driven with less discretion and fewer choke points. Still imperfect, obviously, but structurally different.

JAM Trinity and India Stack: The Digital Backbone of DBT

If DBT is the visible part-the thing people experience as “money coming into my account”-then the real story sits underneath it. Quiet, technical, and mostly invisible unless something breaks.

At the center of it all is what policymakers like to call the JAM Trinity: Jan Dhan accounts, Aadhaar, and mobile connectivity. Three pieces that, taken together, solve a very basic but stubborn problem: how do you make sure money reaches the right person, directly, and that they actually know it arrived?

Before this, at least one of those pieces was usually missing. People didn’t have bank accounts, or they had accounts but no reliable ID. Or they had both, but no way of being notified or verified in real time. DBT didn’t invent these components, but it stitched them together into something usable.

Take Jan Dhan Yojana, for instance. When it launched in 2014, there was skepticism—quiet, but real. Zero-balance accounts? For millions of people who’d never interacted with formal banking? It sounded ambitious. Maybe too ambitious.

And yet, over time, it worked. More than 53 crore accounts were opened. For many, it was the first time they had something resembling a financial identity, something with their name on it that the system recognized.

Then there’s Aadhaar. If Jan Dhan gave people accounts, Aadhaar gave them a way to prove, consistently, that they are who they say they are. Not with paper documents that could be duplicated or forged, but with biometric data—fingerprints, iris scans. Imperfect, yes, but far harder to game at scale.

What this did, almost immediately, was collapse a long-standing loophole: duplication. Earlier, it wasn’t uncommon for the same individual (or identity) to appear multiple times across welfare databases, sometimes within the same scheme, sometimes across states. Add in completely fake entries, names that existed only on paper, and you had a system that was padded from the inside.

Aadhaar didn’t fix everything, but it made that kind of duplication structurally difficult. Ghost beneficiaries, arguably one of the biggest drains on public funds, started disappearing from the rolls.

Then comes the part most people never see: the pipes that actually move the money.

Two systems do most of the heavy lifting here. The Aadhaar Payment Bridge (APB) essentially routes funds using Aadhaar numbers instead of traditional bank details. And the Public Financial Management System (PFMS), which tracks where the money is going, is almost like a live ledger for government spending.

Together, they turn what used to be a fragmented process into something closer to a closed loop. Funds leave government accounts, travel through a defined pathway, and land only in verified accounts. There’s less room for detours now. Not zero, but much less.

And this whole setup doesn’t exist in isolation. It’s part of a larger ecosystem, India Stack. Things like UPI, DigiLocker, and the Account Aggregator framework all sit in the same universe. DBT is just one application running on top of that infrastructure.

Which is interesting, if you think about it.

Because it means DBT isn’t a one-off reform. It’s more like a use case, one way of applying a broader digital foundation that India has been building, piece by piece, over the last decade.

And like most foundations, you don’t really notice it when it works but only when it doesn’t.

DBT Performance Analysis: Savings, Efficiency, and Impact Metrics

If the earlier sections were about what DBT is and how it works, this is where we ask a harder question: Does it actually hold up when you put numbers against it?

One of the more detailed attempts to answer that comes from the BlueKraft Digital Foundation. The study, authored by Dr. Shakil Bhat, looks at roughly 15 years of data, from 2009 to 2024. That time span matters, because it captures both the messy pre-DBT years and the more structured period after its expansion.

The headline number is the one you’ve already seen: ₹3.48 lakh crore saved. But when you sit with it for a moment, the more interesting part is where that saving actually comes from. It’s not some abstract efficiency gain, but it’s very specific leakages being cut off, leakages that stemmed from duplicate beneficiaries and ghost entries. Funds that would’ve quietly disappeared somewhere between allocation and delivery are now tracked from disbursal till receipt.

Then there’s subsidy rationalization, which sounds like policy jargon until you translate it. Before DBT, subsidies took up about 16% of total government expenditure. By 2023-24, that number had dropped to around 9%.

At first glance, that might sound like the government pulled back on welfare. But that’s not really what’s happening. The spending is still there, but what’s changed is that less of it is being wasted along the way. More of each rupee actually lands where it’s supposed to, and that distinction matters a lot.

Another shift that stands out is scale. The number of beneficiaries didn’t just grow, but it exploded from about 11 crores in the early phase to over 176 crores by 2023, 16 times larger.

And yet, and this is the part that feels slightly counterintuitive, this expansion happened alongside a reduction in per-unit costs. There were more people covered, but less leakage per person. Usually, systems get sloppier as they scale. Here, it seems to have gone the other way.

The study also introduces something called the Welfare Efficiency Index (WEI). Think of it as a composite score—one number trying to capture how well the system performs across multiple dimensions. It weighs savings (50%), subsidy efficiency (30%), and beneficiary coverage (20%).

Back in 2014, the score was 0.32. Which, put bluntly, is not great. By 2023, it had climbed to 0.91, almost as high as the scale allows.

Now, indices can sometimes feel a bit constructed. You can tweak weights, redefine variables, but even with that caveat, the direction here is hard to ignore. Something clearly shifted, and shifted quite dramatically.

The study goes a step further and tries to answer a tricky question: was DBT actually the cause of these improvements, or just correlated with them? Using statistical tools like Granger causality tests, it argues that DBT implementation is the primary driver and not broader economic trends or political cycles.

That’s a bold claim, but the pattern does line up: as DBT coverage increased, leakages consistently dropped, not perfectly, not instantly, but steadily.

There’s also a useful way to contextualize the ₹3.48 lakh crore savings figure. Total DBT transfers have crossed ₹43.3 lakh crore. So, the system isn’t just saving money, but it’s handling an enormous volume of transfers while keeping losses relatively low.

If earlier estimates suggested leakages as high as 85%, what we’re seeing now is something closer to single-digit loss rates. That’s not perfection, but it’s a different league entirely.

And maybe that’s the takeaway from this section.

Not that DBT is flawless, it clearly isn’t, but that when you actually measure it, across multiple dimensions, the system doesn’t just look better. It performs better in ways that are hard to dismiss as coincidence.

Sector-Wise DBT Savings: Where India Reduced Welfare Leakages

Public Distribution System (PDS): Cutting Food Subsidy Leakages

The Public Distribution System (PDS) is, by far, the biggest contributor, about 53% of total savings, roughly ₹1.85 lakh crore.

That’s huge but also not surprising, if you remember how PDS used to function.

For years, ration cards were easy to duplicate. Entire “families” existed only on paper. Grain meant for low-income households would quietly get diverted and sold in the open market. Everyone sort of knew it was happening, but the system didn’t have a clean way to stop it.

What DBT (combined with Aadhaar) did was introduce biometric authentication at Fair Price Shops. You show up, authenticate yourself, and only then can you collect your entitlement. In a nutshell: no matching identity, no grain.

It sounds basic, but that one layer, verification at the point of delivery, closed off a major leakage channel. But not completely, though. In areas with poor connectivity or where biometric machines fail, gaps still exist. But compared to the earlier setup, it’s a different level of control.

PM-KISAN Agricultural Support

The PM Kisan Samman Nidhi scheme is simpler in structure-₹6,000 a year to eligible farmer families-but it still had its own share of creative entries.

When the beneficiary database was cleaned up- linked with Aadhaar and cross-checked against land records- it turned out a fair number of recipients weren’t actually eligible. Some were government employees; others were income taxpayers, and a few weren’t even individual farmers in the intended sense.

Removing those entries led to savings of about ₹22,106 crore. Not because benefits were cut, but because they were redirected away from people who shouldn’t have been receiving them in the first place.

MGNREGS Wage Payments

MGNREGS is a different beast altogether—large-scale, rural, and heavily dependent on local administration.

Before DBT integration, wage payments often moved through layers of contractors and local officials. That created room for delays, skimming, and even entirely fake “workers” on payrolls.

With DBT, wages now go straight into workers’ bank accounts. As no intermediary handled the cash, that alone changed incentives.

The result? About 98% of wages are now paid on time, and cumulative savings are estimated at ₹42,534 crore. A big chunk of that comes from eliminating ghost workers and reducing local-level diversion.

PAHAL LPG Subsidy

This one’s interesting because it didn’t just tighten the system but it flipped it.

Earlier, LPG cylinders were sold at subsidized prices. Which meant there was always an incentive to divert them—sell subsidized cylinders to commercial users at higher rates.

PAHAL changed the model entirely. You pay the full market price upfront, and the subsidy gets credited directly to your bank account afterward.

No subsidized product floating around means there is nothing to divert.

It’s a small conceptual shift, but it removed the problem at its root. Add to that the “Give It Up” campaign– where about 1.1 crore relatively well-off consumers voluntarily gave up their subsidy- and you get a system that’s not just tighter, but also a bit more self-aware.

Scholarships and Education Transfers

This is the quieter category, less headline-grabbing, but still important.

Earlier, scholarship funds often moved through institutions—colleges, schools, and administrative bodies. Somewhere along that chain, delays and diversions would creep in. Sometimes students got partial payments, and sometimes nothing at all.

With DBT, the money goes directly into the student’s account. Cleaner, faster, and harder to intercept.

The National Scholarship Portal has also helped standardize things across more than 100 schemes, which, if you’ve ever dealt with fragmented application systems, is a relief in itself.

DBT Implementation Challenges: CAG Audit Findings and System Gaps

Up to this point, DBT can start to sound like a clean success story. Numbers improving, leakages shrinking, systems tightening and a lot of that is true.

But it’s not the whole picture.

If you really want to understand how a system is working, you look at where it fails. And in India’s case, the most credible window into those failures comes from the Comptroller and Auditor General (CAG).

In December 2024, CAG Sanjay Murthy pointed out something that cuts right to the core of DBT’s promise: thousands of crores are still being transferred without proper verification or cross-checks. That’s not a minor glitch—that’s the system slipping on one of its foundational principles.

The underlying issue, as the CAG framed it, is surprisingly old-fashioned: silos.

Different departments, even within the same ministry, are maintaining their own beneficiary databases. There are no shared backbone and no consistent cross-referencing. So, a person removed from one scheme might still exist, perfectly active, in another.

It’s a bit like cleaning one room in a house while the others remain untouched. The system looks better in parts, but not as a whole.

Then there are the more granular, human-level issues—the kind that don’t show up neatly in dashboards.

For instance, there are biometric failures. Elderly beneficiaries whose fingerprints have worn down over time sometimes can’t authenticate themselves at Fair Price Shops. Imagine showing up for your rations and being turned away because your own body doesn’t “match” the system anymore.

Or payments continuing to go into the bank accounts of people who have passed away, simply because death records haven’t been updated quickly enough across systems.

Or Aadhaar-linked accounts that were seeded but never properly authenticated, still sitting in the pipeline.

And then there’s a quieter, but arguably more serious problem: exclusion.

A parliamentary standing committee flagged that certain groups-tribal populations, migrant workers, people without stable documentation-are more likely to fall through the cracks. Not because they’re ineligible, but because they can’t consistently meet the system’s requirements. KYC norms, active bank accounts, updated records—it all assumes a level of stability that not everyone has.

So, while DBT reduces leakage, it can, if not carefully managed, increase exclusion. And those two problems don’t cancel each other out, but they coexist.

Now, it’s important not to overcorrect the narrative here.

These gaps don’t mean DBT has failed. In fact, the very existence of detailed audits like this suggests the opposite, that there’s enough structure in the system to examine it critically.

But they do serve as a reminder that digitization isn’t a magic fix. You can remove intermediaries, tighten flows, build robust pipelines, but if the underlying data is messy, or if systems don’t talk to each other, problems find a way back in, just in different forms.

And maybe that’s the uncomfortable truth of this section: DBT solved a big class of problems, but it introduced a new set that are less visible, more technical, and in some cases, harder to fix.

Future of DBT in India: DBT 2.0 and DBT 3.0 Roadmap

DBT 1.0: Establishing the Foundation

DBT hasn’t been static. It’s evolved in phases, each one trying to fix the blind spots of the previous version. And if you trace that progression, you start to see a pattern: first fix delivery, then fix eligibility, and eventually try to anticipate need itself.

That’s where things get interesting and a little uneasy, if we’re being honest.

The first phase- roughly 2013 to 2019- was about getting the basics right.

Stop cash leakages and cut out intermediaries. Make sure money actually reaches a bank account tied to a real person, and that was the mission.

And by that measure, DBT 1.0 worked. Most of the ₹3.48 lakh crore in savings can be traced back to this period. It built the rails—Aadhaar-linked accounts, direct transfers, identity verification. Nothing fancy, but foundational.

You could almost think of it as plumbing. Not glamorous, but once it’s in place, everything else depends on it.

DBT 2.0: Enhancing Eligibility and Verification

Once the pipes were working, the next question naturally followed: Are we sending money to the right people in the first place?

That’s what DBT 2.0 is trying to address.

Here, the focus shifts from delivery efficiency to eligibility accuracy. Two different problems, really. One is about leakage; the other is about correctness.

Technologies like DigiLocker and API Setu come into play here. Instead of people submitting physical documents that may or may not be verified properly, everything moves into a digital, interconnected flow. Documents get pulled directly from source databases, land records, tax filings, employment registries, and verified in real time.

In theory, this reduces both kinds of errors:

• Inclusion errors (people getting benefits they shouldn’t)

• Exclusion errors (people being left out despite being eligible)

There’s also a quieter but important addition: account health checks. Before funds are sent, the system verifies whether the account is active and capable of receiving transfers. It sounds minor, but it prevents a lot of silent failures.

And crucially, DBT 2.0 tries to deal with the “silo problem” flagged by the CAG. The idea is to move toward interoperable databases, where different departments aren’t operating in isolation, but referencing a shared or at least connected system of records.

That’s easier said than done, of course. Government systems don’t merge overnight. But the intent is clear: one citizen, one consolidated welfare profile (with appropriate privacy safeguards… ideally).

DBT 3.0: Suo Motu Benefit Delivery

And then there’s DBT 3.0, which feels less like an upgrade and more like a conceptual leap.

The idea here is “suo motu” delivery. In plain terms: the system figures out you’re eligible and sends you the benefit without you having to apply.

No forms, no queues, and no “please come back with additional documents.”

It flips the traditional model on its head.

Instead of citizens proving eligibility to the state, the state identifies eligibility on its own by using data: Aadhaar records, tax data, land ownership, employment history, and even health data.

You can see the appeal immediately. Think of a household that suddenly loses its primary earner. In the current system, they’d have to navigate paperwork at exactly the moment they’re least equipped to do so. In a DBT 3.0 world, the system would detect that shock and automatically enroll them into relevant support schemes.

That’s the promise, but it also raises questions that don’t have easy answers.

How accurate are these determinations going to be? What happens when the system gets it wrong? Who corrects it and how quickly? And then there’s the bigger one: privacy. When eligibility depends on stitching together multiple layers of personal data, the safeguards need to be more than just theoretical.

Because once a system like this exists, it doesn’t just serve people, it also sees them. In ways that earlier welfare systems never could.

Still, this is the direction policy thinking is moving in. DBT 3.0 is tied closely to the broader Viksit Bharat 2047 vision, where welfare isn’t reactive but anticipatory.

And if it works, it could remove one of the most persistent barriers in welfare delivery: the burden placed on the beneficiary to navigate the system.

There’s a quiet shift across these three phases. From sending money efficiently, to sending it correctly, to eventually sending it without being asked.

Each step sounds logical on its own. Together, they point to something much bigger, a system that doesn’t just deliver welfare but actively manages it.

Whether that’s empowering or unsettling probably depends on how well it’s governed.

International Recognition and the Global Blueprint

At some point, DBT stopped being just a domestic reform story. It started getting noticed from the outside and not in a casual, “that’s interesting” way, but as something other countries might actually try to replicate.

The International Monetary Fund, for instance, has pointed to India’s DBT framework as a practical example of how to make social spending more efficient. Their 2025 analysis essentially says: if you’re an emerging economy struggling with subsidy leakages, this kind of identity-linked, direct transfer model is worth paying attention to.

The World Bank takes a slightly broader view. It connects DBT to India’s overall digital infrastructure push, arguing that this investment hasn’t just improved delivery, but also created fiscal space. In simpler terms, by wasting less, the government has more room to spend where it actually matters. And, according to their South Asia analysis, this has played a role in reducing multidimensional poverty faster than traditional systems would have allowed.

Then there’s the UNDP, which frames DBT a bit differently, not just as an efficiency tool, but as part of a larger Digital Public Infrastructure (DPI) story. In its 2025 India report, DBT shows up as a working example of how digital systems can push forward goals like poverty reduction and inequality. It’s less about the mechanics, more about the outcomes.

What’s interesting, though, is the shift in India’s role here.

For a long time, India was on the receiving end of development models—borrowing frameworks, adapting ideas, implementing recommendations from global institutions. Now, at least in this domain, it’s starting to export one.

There’s a symbolic moment tied to that shift. During the AI Action Summit in Paris in February 2025, Prime Minister Narendra Modi explicitly positioned India’s digital welfare stack as something that could be adapted globally—not proprietary, not locked down, but more like a public good.

And it’s not just rhetoric. Countries across Sub-Saharan Africa, Southeast Asia, and parts of South America have sent delegations to study how DBT and the broader India Stack actually work on the ground.

Of course, replication isn’t straightforward. India’s scale, its Aadhaar infrastructure, its banking penetration—these aren’t easily mirrored elsewhere. What works in a country of 1.4 billion doesn’t always translate neatly to smaller or structurally different economies.

But still, the interest is real.

And maybe that’s the bigger takeaway here—not that DBT is a perfect model, but that it’s credible enough to be studied, adapted, and debated globally.

Which, if you think about where India stood a couple of decades ago in the development conversation, is a pretty significant shift.

The Essential DBT FAQ: 5 Key Questions

Direct Benefit Transfer (DBT) is India’s digital welfare system that sends subsidies directly to bank accounts. It relies on the JAM Trinity: Jan Dhan (the account), Aadhaar (the identity), and Mobile (the gateway). This “India Stack” architecture eliminates middlemen and ensures money reaches the right person instantly.

As of 2025, DBT has saved a massive ₹3.48 lakh crore (approx. 1.5% of GDP) by purging “ghost” beneficiaries. This includes removing 5.87 crore fake ration cards (PDS) and 1.26 crore invalid job cards (MGNREGS). Total transfers have now surpassed the ₹43.95 lakh crore milestone.

The WEI is the ultimate proof of DBT’s success. It measures how much of every ₹1 spent actually reaches the citizen. India’s WEI score skyrocketed from 0.32 in 2014 to 0.91 in 2023-24, meaning 91% of welfare funds now reach their destination without leakage.

While 1.47% of transactions still fail due to technical issues, the government is introducing Face Authentication and Iris Scans for those who struggle with fingerprints. For those excluded by “data silos,” DBT 2.0 is integrating real-time API verification to ensure no eligible citizen is left behind.

The next evolution is DBT 3.0. Instead of a citizen applying for a scheme, the government will use a National Social Registry to automatically identify eligible households and deliver benefits suo motu (on its own motion). This shifts the burden of proof from the citizen to the system.

Troubleshooting: Why Haven’t I Received My DBT Payment?

If your welfare benefits haven’t arrived, it is usually due to a technical mismatch in how your bank account is linked to the central system. Use this quick 3-step guide to identify and fix the issue.

1. Check Your Aadhaar-Bank Seeding Status

Linking your Aadhaar to a bank for KYC is not the same as “seeding” it for DBT. Seeding tells the government exactly which account should receive your funds.

- How to Check: Visit the official UIDAI website or use the mAadhaar App. Log in to see if your status is “Active” and which bank is currently mapped.

- Mobile Shortcut: Dial *99*99*1# from your registered mobile number to get an instant status update via SMS.

2. Track Your Payment on the PFMS Portal

The Public Financial Management System (PFMS) allows you to track the exact stage of your transaction.

- Go to the PFMS website and use the “Know Your Payment” tool.

- Common Error Messages:

- “Aadhaar Not Seeded”: You must visit your bank and submit an NPCI Mapping/Consent form.

- “Account Dormant”: Your account may be frozen due to inactivity. Make a small deposit or withdrawal to reactivate it.

- “Invalid IFSC”: Often happens after bank mergers. You may need to update your bank details on the specific scheme’s portal (like PM-KISAN).

3. Critical Fixes for Common Errors

- Name Mismatch: Ensure the name on your Aadhaar card matches the name on your bank account exactly. Even a small spelling difference can cause a transfer to fail.

- Multiple Accounts: DBT funds are always sent to the last bank account you seeded. If you have multiple accounts, check all of them before assuming the payment failed.

- Biometric Issues: If your fingerprints aren’t working at a kiosk (common for elderly beneficiaries), ask your bank about Face Authentication or Iris scan options.

A Global Blueprint for Welfare Delivery

That ₹3.48 lakh crore figure, it’s tempting to treat it like the headline and move on. Big number and clear win.

But if you sit with it for a bit, it starts to feel like a proxy for something larger. Not just money saved, but a system that was fundamentally reworked.

For decades, welfare in India depended heavily on people—local officials, intermediaries, and informal networks. Sometimes that worked, often it didn’t. What DBT has done, at its core, is shift that dependence toward infrastructure. There is less discretion and more design.

Money now moves through systems that are, at least in principle, resistant to interference. Not immune, but resistant. And that alone changes the equation.

The Welfare Efficiency Index captures part of that shift—from 0.32 to 0.91 in about a decade. Numbers like that can feel abstract, but what they’re really pointing to is a system that went from barely functioning to something that, most of the time, does what it’s supposed to do at scale for over 176 crore beneficiaries.

But, and this matters, the story doesn’t end on a clean, triumphant note.

The CAG findings linger in the background: exclusion errors, outdated data, and departments not talking to each other. These aren’t edge cases; they’re structural issues that affect real people and usually the ones least equipped to navigate a system when it fails them.

Fixing that isn’t just about better tech. It’s about coordination, accountability, and something less tangible—administrative will. Systems don’t integrate themselves.

Looking ahead, DBT 2.0 and 3.0 lay out a fairly ambitious path. Better verification, interoperable databases, and eventually even automatic benefit delivery. A system that doesn’t wait for you to apply, but identifies you and acts.

It sounds efficient. It also raises questions—about privacy, about errors, about what happens when a system makes decisions on your behalf and gets them wrong.

Still, the direction is clear. A national social registry. Continuous fraud detection. Near-zero exclusion as a design goal, not an afterthought. Technically, none of this is out of reach anymore. The harder part is making sure it works fairly, not just efficiently.

For other countries watching this unfold, there are a few quiet lessons embedded here.

That financial inclusion isn’t optional—it’s foundational.

That identity systems, however debated, can dramatically reduce duplication.

That plugging leakages doesn’t have to mean cutting welfare—it can actually expand it.

And that is when digital infrastructure is treated as a public good, not a proprietary asset; it can scale in ways that are hard to replicate through private systems alone.

India’s DBT story isn’t perfect. It’s still evolving, still uneven in places. But it’s no longer experimental—it’s operational, measurable, and increasingly, influential.

And maybe that’s the real takeaway.

This isn’t just about saving ₹3.48 lakh crore. It’s about showing what happens when you rebuild welfare delivery from scratch—with modern tools, yes, but also with a willingness to rethink how the state shows up in people’s lives.

The next decade will test whether that momentum holds. Whether the gaps close. Whether the system becomes not just efficient, but genuinely inclusive.

Because in the end, the goal isn’t just that the money moves correctly.

It’s that it reaches everyone it’s supposed to—without them having to fight for it.

Disclaimer

The content provided on this page is designed as an educational explainer to help simplify complex topics and is for general informational purposes only. While we make every effort to ensure the accuracy, completeness, and reliability of the information presented at the time of publication, facts and circumstances can change. The information provided here is on an “as is” basis and does not constitute professional, technical, or legal advice. This explainer should be used as a foundational guide for understanding the topic, and readers are encouraged to conduct their own independent research or consult with relevant professionals before taking any action based on this content.

Leave a Reply