LTCG Tax on Mutual Funds & Property (2026): How to Calculate & Legally Save on Capital Gains

How the 2025-2026 Budget Updates Affect Your LTCG Tax Liability

If you sold equity mutual funds, a property, or even a piece of land during FY 2025–26 and walked away with a healthy profit, there’s a second number waiting quietly in the background: your potential tax bill. That’s where LTCG tax on mutual funds enters the picture. It’s one of those parts of personal finance that people hear about often, yet many only start digging into it once a sale actually happens. And by then, confusion usually arrives first.

The rules have also shifted again. With updates introduced through the Union Budget 2025 and the Finance Bill 2026, some calculations, exemptions, and tax treatments now work differently than they did a couple of years ago. A strategy that made perfect sense earlier may not necessarily be the smartest route today.

This guide is designed for people across the spectrum: salaried employees trying to understand a one-time investment gain, experienced investors managing multiple assets, first-time property sellers, and anyone who simply wants a clearer answer to one question: How much tax do I actually owe, and is there a legal way to reduce it?

To put this together, we’ve relied on official material from the Income Tax Department, technical interpretations from accounting professionals, and analysis from leading Indian financial platforms. The idea is simple: instead of jumping between ten tabs and three conflicting explanations, you get one place that pulls the moving pieces together.

At A Glance: LTCG Tax On Mutual Funds

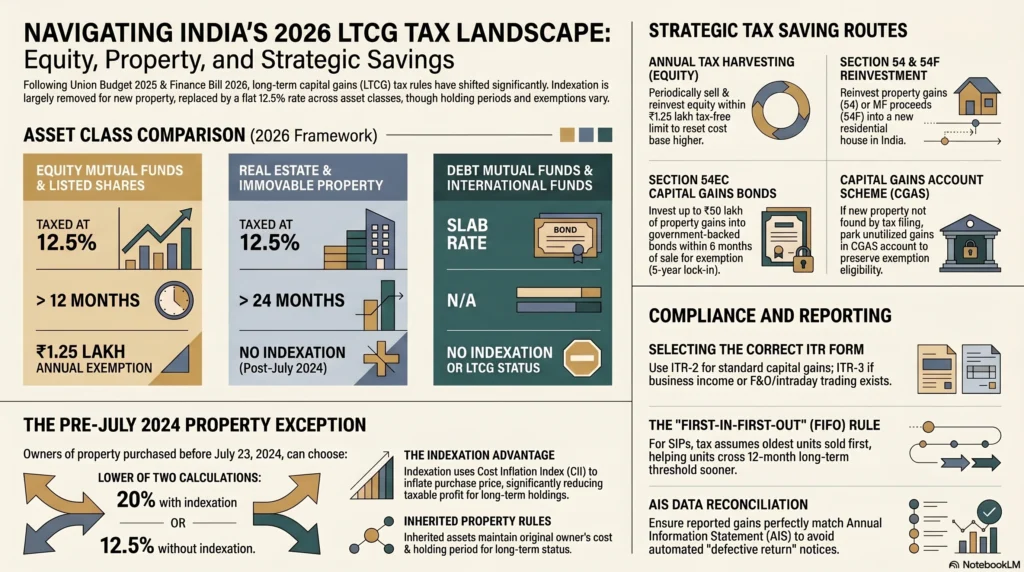

- Equity Mutual Funds & Shares: Long-Term Capital Gains (LTCG) are now taxed at 12.5%, but only on gains exceeding the new ₹1.25 lakh annual exemption limit. The required holding period remains more than 12 months.

- Property & Real Estate: The new standard LTCG rate is 12.5% without indexation for properties held over 24 months.

- The Pre-July 2024 Property Exception: If you purchased a property before July 23, 2024, you have a choice. You can calculate your tax under both systems—the old 20% rate with indexation and the new 12.5% rate without indexation—and pay whichever is lower.

- Debt Mutual Funds: Capital gains are taxed entirely at your applicable income tax slab rate, regardless of how long you hold the investment. The old indexation benefits are no longer available.

- Smart Tax Saving Strategies: You can legally reduce your tax burden by utilizing tax harvesting for the ₹1.25 lakh equity exemption, claiming Section 54 or 54F when reinvesting in residential property, or investing in Section 54EC capital gains bonds.

- ITR Filing Accuracy: Avoid defective return notices by choosing the correct form (typically ITR-2 for capital gains) and ensuring your reported gains perfectly match your Annual Information Statement (AIS).

Understanding Capital Gains Tax in India (2026 Framework)

What is Long-Term Capital Gains (LTCG) Tax?

A capital gain is simply the profit earned when you sell an asset for more than what you originally paid for it. Sounds straightforward on paper. In practice, though, things become layered very quickly because the tax treatment depends on what you sold and how long you owned it.

Under Indian tax rules, capital assets cover a fairly broad territory. They include equity shares, mutual fund units, property and real estate, gold, debentures, and even certain intellectual property rights.

The Income Tax Act broadly splits these gains into two categories: Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG). The dividing line isn’t based on how large the profit is. It comes down to one thing only: the holding period — how long you kept the asset before selling it. The Income Tax Department explains the framework in detail on its official page.

For listed shares and equity-oriented mutual funds, crossing the one-year mark matters. Hold them for more than 12 months, and the gain generally moves into long-term territory. Sell earlier, and it becomes short-term.

Property works differently. For land and residential or commercial real estate, the long-term threshold is generally 24 months today, though older rules used different timelines in certain periods. Debt mutual funds and unlisted securities also follow separate holding requirements, and debt fund taxation in particular changed significantly beginning FY 2023–24, something we’ll come back to later because it altered the old playbook for many investors.

One reason investors pay close attention to LTCG is simple: long-term gains are typically taxed at more favorable rates than ordinary income. That difference can materially affect your returns over time. The government’s tutorial on LTCG concepts, available here, gives a useful foundational explanation and works well as a reference alongside this guide.

What is the difference between STCG and LTCG?

This is probably the question most people run into first, and understandably so. The difference between STCG and LTCG isn’t really about the size of the profit you made. You could earn a small gain or a very large one — that part doesn’t decide the category. Two things matter: how long you held the asset and the tax rate attached to it.

| Feature | STCG | LTCG |

| Holding period (Equity/Eq. MF) | Up to 12 months | More than 12 months |

| Holding period (Property/Debt MF) | Up to 24 months | More than 24 months |

| Tax rate (Equity/Eq. MF) | 20% (post-Budget 2024) | 12.5% above ₹1.25 lakh |

| Tax rate (Property) | Slab rate | 12.5% (without indexation, post-July 2024) |

| Indexation benefit | Not applicable | Previously available on property; now largely removed for new sales |

The broad takeaway is fairly simple: holding an investment longer often leads to a more favourable tax outcome. That isn’t accidental; the structure is designed to encourage longer-term investing rather than frequent buying and selling.

Recent changes have made that contrast even more noticeable. The Finance Act 2024 increased the STCG tax rate on equity investments from 15% to 20%, while revising the LTCG rate from 10% to 12.5%. On first glance, both rates moved upward or shifted around. But the larger story is that holding investments longer can still work out more efficiently from a tax perspective than repeatedly booking short-term gains.

A detailed analysis of these changes has been documented by Taxmann.

Key Budget Updates to Capital Gains Taxation (FY 2025–26)

The capital gains rules have gone through a fairly active stretch of revisions over the last couple of years. If you feel like the rules changed, then changed again, and then needed clarification after that, you are not imagining it. The Finance Act 2024 reshaped parts of the system, and the Finance Bill 2026 added further explanations and adjustments that taxpayers now need to keep in mind while filing returns for AY 2026–27.

Here’s where things stand in practical terms:

LTCG on equity shares and equity-oriented mutual funds

Long-term gains on equity investments are taxed at 12.5%, but only after crossing the annual exemption threshold of ₹1.25 lakh. Gains within that limit remain exempt. As before, these investments do not receive any indexation benefit.

LTCG on property sales

Property taxation saw one of the biggest shifts. Long-term gains from immovable assets now generally attract 12.5% tax without indexation. When this change arrived in July 2024, it sparked considerable debate because indexation had long been a key tax-saving tool for property owners.

To soften the transition, the government introduced limited relief for properties purchased before July 23, 2024. In those cases, taxpayers can compare two methods and pay whichever produces the lower tax:

- Old system: 20% LTCG with indexation

- New system: 12.5% LTCG without indexation

That choice can make a meaningful difference depending on when the property was bought and how much inflation affected its value over time. A more detailed breakdown is available here.

Debt mutual funds

Debt fund taxation continues under the framework introduced in FY 2023–24. Gains are taxed according to the investor’s income tax slab rate rather than receiving separate LTCG or STCG treatment. For many investors, this effectively changed the way debt funds are evaluated from a tax-efficiency perspective.

Equity grandfathering provisions remain in place

Investors holding equity assets from before February 2018 still benefit from the existing grandfathering rule. Gains accumulated up to January 31, 2018 continue to remain outside the taxable LTCG calculation. For long-time investors who have held positions for years, this provision can still matter quite a bit.

Surcharge cap for high-income taxpayers

There is also an important concession that often gets overlooked: surcharge on LTCG from equity and mutual fund investments remains capped at 15%, regardless of overall income levels. For high earners, this can materially reduce the effective tax burden. A detailed explanation of surcharge and cess treatment for AY 2026–27 can be found here.

At a broader level, the direction of these changes is becoming clearer. Equity investing still receives favourable long-term treatment, debt investments no longer enjoy the same tax advantages they once did, and property taxation has shifted into a more simplified, though sometimes controversial, structure.

LTCG Tax on Mutual Funds: Rules, Rates, and Calculations

Equity Mutual Funds vs. Debt Mutual Funds: The Tax Divide

When people talk about mutual fund taxation, there is a common assumption that tax treatment depends on the fund house, returns, or how popular a scheme is. It doesn’t. The factor that matters most is the underlying nature of the fund itself, specifically, whether it is classified as an equity fund or a debt fund.

That distinction sounds small. Tax-wise, it changes a lot.

Equity-Oriented Mutual Funds are funds that invest at least 65% of their portfolio in domestic equities. This bucket includes diversified equity funds, ELSS funds, index funds, ETFs, and many balanced advantage funds that maintain the required equity allocation, and thematic or sector-based funds.

If these investments are held for more than 12 months, gains are treated as long-term capital gains and taxed at 12.5%, after accounting for the annual ₹1.25 lakh exemption. The treatment is confirmed by the official guidance available here.

Debt Mutual Funds, on the other hand, follow a different path. These funds primarily invest in fixed-income assets such as bonds, government securities, treasury instruments, and money market products.

Beginning April 1, 2023, the tax equation changed significantly. Gains from debt mutual funds no longer receive the older long-term tax treatment with indexation benefits. Instead, regardless of whether you held the investment for one year or ten years, gains are now taxed according to your applicable income tax slab rate.

For investors in higher tax brackets, this removed one of the major tax advantages debt funds historically enjoyed. The implications of these changes have been examined in detail in this analyses.

Then there are the categories that sit somewhere in the middle.

Hybrid funds and certain fund-of-funds structures do not automatically qualify as equity funds. If they fail to maintain the required 65% domestic equity allocation, they are generally treated under rules similar to debt funds. A conservative hybrid strategy, for example, may look partly equity-focused on the surface but still receive debt-style taxation.

International funds create another point of confusion. Even if they invest in equities, if those investments are primarily outside India, they usually do not qualify as equity-oriented under Indian tax rules. Their gains are generally taxed according to slab rates as well.

The takeaway here is fairly simple: two mutual funds may appear similar in performance charts or investment style, yet their tax treatment can be very different. Looking at returns without understanding the tax side sometimes gives an incomplete picture.

How to Calculate LTCG on Equity Mutual Funds (The ₹1.25 Lakh Exemption)

For equity mutual funds, calculating LTCG follows a fairly defined process. The formula itself isn’t difficult. What usually trips people up are the smaller details — SIP installments, older holdings, grandfathering rules, and the annual exemption limit. Miss one of those and the final tax number can look very different.

Here’s a step-by-step approach.

Step 1: Identify your long-term transactions

Start by listing all equity mutual fund units sold during the financial year that were held for more than 12 months.

For SIP investors, this is where things become a little less straightforward. Every SIP instalment is treated as a separate purchase with its own acquisition date. So, if you’ve been investing monthly for years, some units in the same fund may qualify as long-term while others may still fall under short-term treatment.

Step 2: Apply the grandfathering rule (for holdings before 2018)

For units purchased before February 1, 2018, the cost of acquisition is determined using a special rule. The acquisition cost becomes whichever is higher:

- Actual purchase cost, or

- Fair Market Value (FMV) of the units as of January 31, 2018

This provision exists for a reason: gains accumulated until January 31, 2018, are effectively shielded from taxation.

To determine the appropriate value, investors can usually refer to historical NAV data from the fund house or fund statements.

Step 3: Calculate the gain

The basic calculation works like this:

LTCG = Sale Value − Cost of Acquisition

(using grandfathered cost wherever applicable)

Step 4: Apply the ₹1.25 lakh exemption

After arriving at the total gain:

Taxable LTCG = Total LTCG − ₹1,25,000

Tax = 12.5% × Taxable LTCG

Now let’s put actual numbers behind it.

Practical Example

Suppose you invested ₹5,00,000 into an equity mutual fund in March 2022. In April 2025, after holding it for three years, you redeem the investment for ₹8,00,000.

Your gain calculation would look like this:

- LTCG = ₹8,00,000 − ₹5,00,000 = ₹3,00,000

- Less annual exemption = ₹1,25,000

- Taxable LTCG = ₹1,75,000

- Tax at 12.5% = ₹21,875

- Plus 4% cess = ₹22,750

The calculation method is explained in the Income Tax Department tutorial and is also covered with practical examples on Zerodha Varsity.

One small but important detail often gets missed: the ₹1.25 lakh exemption applies per financial year, not per investment.

So, if gains come from multiple equity mutual funds, shares, or eligible equity assets, they are combined first. The exemption is then applied to the total long-term gain amount, not individually to each investment.

How is LTCG calculated on SIPs?

This is one of the areas where investors often get caught off guard. A lot of people assume an SIP is treated as a single investment because the money goes into the same fund every month. Tax rules don’t see it that way.

Each SIP instalment is treated as a separate purchase lot, with its own purchase date and holding period. Which means every contribution starts its own clock independently.

The concept itself is simple. The paperwork behind it can feel a little less friendly.

Here’s how it works in practice:

- Suppose you began investing ₹10,000 per month in January 2023 through an SIP and decided to redeem everything in February 2025.

- The instalments invested before February 2024 would have completed the required 12-month holding period, so those units would qualify as long-term.

- The January and February 2024 instalments, however, would still fall under short-term treatment because they haven’t crossed that one-year threshold.

Another important piece of the puzzle is the method used during redemption.

Mutual funds generally apply FIFO (First-In-First-Out). In plain language, the oldest units are assumed to be sold first.

For long-term investors, that often works in their favor. Older units have had more time to cross into LTCG territory and may also have been purchased at lower prices. So when redemption happens, there is a good chance those units qualify for long-term treatment before newer investments do.

Zerodha’s support documentation explains in detail how capital gains reports for SIP investors are prepared and how FIFO is applied during calculations. Fund houses and brokers also provide annual capital gains statements through platforms such as CAMS and KFintech, making it easier to separate long-term and short-term gains.

Tax Harvesting for SIP Investors

There’s also a strategy many long-term investors use quietly in the background: tax harvesting.

The basic idea is straightforward. Instead of allowing gains to pile up for years, investors periodically redeem units that are approaching the ₹1.25 lakh annual LTCG exemption limit, then reinvest the proceeds immediately.

By doing this, they lock in gains that fall within the exempt threshold and reset the purchase cost for future calculations. Over long investing periods, that can gradually reduce the eventual tax burden in a meaningful way.

We’ll go deeper into this strategy later because it deserves its own section.

LTCG Tax on Real Estate & Property Transactions

Current LTCG Tax Rate on Property Sales in 2026

Real estate taxation has traditionally moved at a slower pace than many other tax rules. Then, on July 23, 2024 happened.

That date marked one of the biggest shifts property taxation has seen in years, because the Finance (No. 2) Act, 2024, removed the indexation benefit for most future property transactions. For many investors and property owners, indexation had long been one of the most useful tools for reducing tax liability, so the change immediately sparked debate.

But the transition wasn’t completely abrupt. The government introduced a limited relief mechanism for certain sellers.

For properties purchased before July 23, 2024, and sold after that date:

Taxpayers have the option to calculate tax under both systems and choose whichever results in a lower liability:

- Old system: 20% LTCG tax with indexation benefit

- New system: 12.5% LTCG tax without indexation

That choice can make a surprisingly large difference.

For example, someone who bought property decades ago, perhaps in the late 1980s or 1990s, may find that indexation significantly increases the adjusted purchase cost, which reduces taxable gains. In many such cases, the old regime may still end up being cheaper overall.

On the other hand, if the property was purchased relatively recently and inflation has not had much time to affect the cost base, the lower 12.5% rate without indexation could work out better.

The RAAAS analysis walks through detailed examples showing situations where one route may be more beneficial than the other.

For properties purchased on or after July 23, 2024:

The flexibility disappears.

Property buyers after this date generally have a single tax framework available:

- 12.5% LTCG tax without indexation for assets held longer than 24 months

No alternate calculation. No comparison exercise.

Another point that remains important: holding period still matters.

If a property is sold before completing 24 months, the gain does not qualify as long-term. It becomes a short-term capital gain, which is taxed according to the individual’s applicable income tax slab rate. For high-income taxpayers, that can mean an effective rate considerably higher than the long-term rate after adding surcharge and cess.

So while the calculation rules have changed, one underlying principle remains intact: time still plays a major role in determining the final tax outcome.

How to calculate indexation on property?

Even though indexation no longer applies to newly purchased properties, it hasn’t completely disappeared from the conversation. If the property was purchased before July 23, 2024, sellers can still compare the old and new tax systems and choose whichever leads to a lower tax outflow. Because of that, understanding how indexation works is still useful, sometimes very useful.

At its core, indexation is meant to account for inflation.

Think about it this way: a property purchased years ago for ₹30 lakh is not really comparable to ₹30 lakh today. Prices, costs, and purchasing power shift over time. Indexation attempts to recognize that change by adjusting the purchase cost using the Cost Inflation Index (CII) published annually by the Central Board of Direct Taxes (CBDT).

The formula works like this:

Indexed Cost of Acquisition = Original Cost × (CII of Sale Year ÷ CII of Purchase Year)

Once that adjusted cost is calculated:

LTCG (Old Regime) = Sale Value − Indexed Cost − Indexed Cost of Improvement

Tax = 20% × LTCG

Now let’s see what this looks like with real numbers.

Example

Suppose you purchased a residential property in FY 2010–11 for ₹30,00,000, and later sold it during FY 2025–26 for ₹1,20,00,000.

Assume:

- CII for FY 2010–11 = 167

- CII for FY 2025–26 = approximately 363

(final figures are notified separately by CBDT)

The calculation becomes:

- Indexed Cost = ₹30,00,000 × (363 ÷ 167)

- Indexed Cost ≈ ₹65,21,000

Now under the old system:

- LTCG = ₹1,20,00,000 − ₹65,21,000

- LTCG ≈ ₹54,79,000

- Tax at 20% ≈ ₹10,95,800

Now compare that with the new framework:

New Regime

- LTCG = ₹1,20,00,000 − ₹30,00,000

- LTCG = ₹90,00,000

- Tax at 12.5% = ₹11,25,000

Interesting part? Even with a lower tax rate under the new system, the final tax payable is actually slightly higher here.

That’s exactly why running both calculations matters.

For properties purchased much earlier, particularly those bought decades ago, inflation-adjusted costs can become substantially larger under indexation. In some cases, the difference is not small at all; it can reduce taxable gains by several lakhs.

The official list of CII values is available here and is updated annually before the relevant assessment year begins.

Inherited Property and Capital Gains

Receiving inherited property can feel complicated from a tax perspective because many people assume a tax obligation starts the moment ownership transfers. In most cases, it doesn’t.

Simply inheriting a property, whether through a Will or through succession laws, does not trigger capital gains tax at the time of inheritance. The tax event generally happens later, when the person inheriting the asset decides to sell it.

That distinction matters because the tax calculation follows a few rules that often surprise people.

For calculating capital gains on inherited property:

- Cost of acquisition: The purchase cost is not based on the property’s market value at the time you inherited it. Instead, you inherit the original owner’s purchase cost.

- Holding period: You also inherit the original owner’s holding period. This is an important benefit that many taxpayers overlook.

So, imagine your parent purchased a property twenty years ago, and you inherited it recently. If you decide to sell it shortly after inheriting it, the holding period does not suddenly reset to a few months. The original ownership period continues to count, which means the gain could still qualify for long-term capital gain treatment immediately.

- Indexation treatment: Where indexation remains available for eligible pre–July 23, 2024 purchases, the relevant base year is tied to the original purchase date, not the inheritance date.

This can make a noticeable difference in tax calculations because older properties often benefit more significantly from inflation adjustments.

The rules surrounding inherited assets, gifts, and similar transfers are covered in this exemption tutorial, which explains situations where ownership changes hands without creating an immediate tax liability.

Proven Strategies to Legally Save LTCG Tax on Property

Section 54: Exemption by Reinvesting in Residential Property

For many property sellers, Section 54 ends up being one of the most useful tax-saving provisions available under the Income Tax Act. The idea behind it is fairly straightforward: if you sell a residential property and put the gains back into another residential property, the government allows you to reduce or even eliminate part of the capital gains tax liability.

Simple in concept. The details, though, matter.

To claim the exemption, certain conditions have to be satisfied:

1. Asset being sold

The property sold must be a residential house property. Vacant land on its own or commercial property generally does not qualify under Section 54.

2. Type of reinvestment

The new investment must be made in one residential property located in India.

3. Time window for reinvestment

Timing is important here:

- Purchase a new house up to one year before the sale, or within two years after the sale

- If constructing a house instead of purchasing one, construction must be completed within three years from the sale date

4. Amount eligible for exemption

The exemption available will be the lower of:

- The total LTCG amount, or

- The cost of the new property purchased

So reinvesting does not automatically wipe out the entire tax bill. The amount invested still matters.

5. Maximum exemption cap

Beginning FY 2023–24, Section 54 exemptions are capped at ₹10 crore. Any gains beyond that limit remain taxable even if additional amounts are reinvested.

6. Lock-in requirement

The newly purchased property cannot be sold within three years. Selling it earlier can reverse the exemption already claimed, causing the previously exempt amount to become taxable in the year of sale.

For many taxpayers, Section 54 acts almost like a bridge, allowing them to move from one property investment to another without taking an immediate tax hit. But because the timelines and documentation requirements are fairly specific, even a small oversight can create issues later.

Detailed conditions and technical guidance are available here.

Section 54EC: Saving Tax Through Capital Gains Bonds

Not everyone who sells a property wants to jump straight back into real estate. Maybe the timing doesn’t feel right. Maybe there’s no suitable property available. Or maybe the idea of taking on another property purchase simply isn’t appealing.

That’s where Section 54EC can become useful.

Instead of reinvesting in another property, this provision allows taxpayers to save on long-term capital gains tax by investing gains from the sale of immovable property into specified capital gains bonds, provided the investment is made within six months from the date of sale.

Here are the important points to understand:

• Eligible issuers

These bonds are issued by government-backed institutions such as:

- National Highways Authority of India (NHAI)

- Rural Electrification Corporation (REC)

- Power Finance Corporation (PFC)

- Indian Railway Finance Corporation (IRFC)

Because these are generally AAA-rated entities with government support, they are often viewed as relatively stable investment options.

• Maximum investment limit

The investment cap is ₹50 lakh per financial year.

In certain cases, because the sale and investment period may overlap two financial years, taxpayers could potentially invest up to ₹1 crore by splitting investments across years. However, this area has seen differing interpretations and legal discussions over time, so professional advice may be useful before relying on that approach.

• Lock-in period

These bonds come with a five-year lock-in period.

Selling them early, redeeming them before the permitted period, or even using them as collateral for a loan can lead to the reversal of the tax exemption.

• Interest earnings

Current returns are generally around 5.25% annually, paid once a year.

There is an important catch, though: while the capital gains exemption itself helps reduce tax liability, the interest earned is taxable according to your income tax slab rate. For higher-income investors, this can reduce the effective post-tax return.

• Treatment on maturity

The bonds themselves do not receive indexation treatment, but investors receive their principal amount back at maturity.

For many sellers, Section 54EC works well because it avoids the pressure of buying another property simply to save tax. It offers a cleaner route: invest, comply with the lock-in requirement, and claim the exemption.

Details on available bond options can be found here, while banks such as HDFC and ICICI also facilitate subscriptions through branches and online channels.

What is the Capital Gains Account Scheme (CGAS)?

Selling a property and claiming a tax exemption under Section 54 sounds straightforward until real life enters the picture.

You sell the property. The capital gain is sitting in your account. The ITR filing deadline is getting closer. But the replacement property? Still not found.

Maybe you’re comparing locations. Maybe a deal fell through. Maybe the right property simply hasn’t shown up yet.

That situation is exactly why the Capital Gains Account Scheme (CGAS), 1988, exists.

The scheme allows taxpayers to temporarily park unutilized capital gains and still claim an exemption, even if the actual purchase or construction of a new property has not happened yet.

Here’s how it works:

1. Deposit the unutilized gains into a CGAS account

Before the due date for filing your income tax return, you can place the unutilized amount into a designated CGAS account through an eligible bank.

There are generally two types:

- Type A: Savings account style structure

- Type B: Term deposit structure

2. Claim the exemption while filing your ITR

Once the amount is deposited, you can claim the relevant exemption in your tax return as though the investment has already been made.

3. Use the funds within the prescribed timeline

The deposited amount should later be used for the intended purpose:

- Within 2 years for purchasing a property

- Within 3 years for constructing one

4. Unused money eventually becomes taxable

If the deposited amount remains unused after the permitted period expires, the unspent portion is treated as long-term capital gains in the year of expiry, and tax becomes payable accordingly.

In practical terms, CGAS acts like a holding space. It gives taxpayers breathing room. Instead of rushing into a property purchase simply because the tax deadline is approaching, you get time to make a more considered decision without immediately losing the exemption benefit.

Most nationalised banks, including those listed at https://dbs.bank.in, offer CGAS facilities. Additional explanations and practical guidance are also available through PwC India’s tax resources and Deloitte India’s tax references.

Smart Ways to Save Tax on Mutual Fund Gains

Tax Harvesting: Exploiting the ₹1.25 Lakh Annual Exemption

A surprising number of investors focus heavily on choosing funds, tracking returns, and timing entries, but quietly overlook one of the simplest tax-saving opportunities already built into the system: the ₹1.25 lakh annual LTCG exemption for equity-oriented investments.

That’s where tax harvesting comes in.

Despite the intimidating name, the idea is not particularly complicated. It’s essentially a method of periodically booking gains within the exempt limit so they never accumulate into a larger taxable amount later.

Think of it as trimming a growing hedge before it turns into something difficult to manage.

Here’s how the process works.

Imagine you’ve been investing ₹10,000 every month into a Nifty 50 index fund for the past five years. Over time, your investments have appreciated, and your portfolio is now carrying a sizable amount of unrealized long-term gains.

Instead of waiting ten or fifteen years and redeeming everything at once, you review your portfolio every year — say around March.

If your total long-term gains have reached or are close to ₹1.25 lakh, you redeem enough units to realize gains up to that limit.

Because those gains remain within the exemption threshold:

- You pay zero LTCG tax

- You immediately reinvest the money

- Your purchase price gets reset to the new value

That reset matters because future gains are then calculated from the new cost base rather than the original one.

Over time, the impact can become meaningful.

If someone consistently harvests ₹1.25 lakh of gains annually for ten years, that potentially removes ₹12.5 lakh of future taxable gains entirely.

Now scale that across multiple eligible investors within a household. A family where each member invests separately could potentially multiply that benefit considerably.

A few practical points still matter:

- Hold units for more than 12 months, otherwise gains may fall into STCG treatment at 20%

- Remember that STT (Securities Transaction Tax) applies at redemption and is automatically deducted

- Consider exit load provisions before redeeming, since some funds impose charges if units are sold too early (although many equity funds waive exit loads after one year)

Tax harvesting isn’t about finding a loophole or bending the rules. It simply uses an exemption that already exists — deliberately, instead of accidentally.

Section 54F: Selling Mutual Funds to Buy a House

Most investors associate property-related capital gains exemptions with property sales. But Section 54F works a little differently. It casts a wider net.

This provision allows taxpayers to claim an LTCG exemption when they sell a long-term capital asset other than a residential house and use the proceeds to buy or construct a residential property in India.

Which means mutual funds can absolutely enter the picture.

So if you redeem long-term mutual fund units, sell shares, dispose of gold ETFs, or sell another qualifying long-term asset and then use the sale proceeds for a house purchase, you may be able to claim an exemption under Section 54F.

Here are the important conditions:

1. Asset being sold

The asset sold must be a long-term capital asset other than a residential house property.

Mutual funds fit neatly into this category, which is why this section can be particularly useful for long-term investors.

2. Investment requirement

There is an important distinction here that many people miss.

The law generally requires investment of the net sale consideration, not merely the capital gain portion.

That means the amount expected to be reinvested is based on the overall sale proceeds.

3. Time limits

The timelines broadly mirror those under Section 54:

- Purchase a property within one year before the sale, or within two years after the sale

- If constructing a property, complete construction within three years

4. Ownership restriction

On the date of sale, the taxpayer should not own more than one residential house, excluding the new property being acquired.

This condition sometimes catches people unexpectedly, particularly those with multiple residential holdings.

5. Partial reinvestment means proportional exemption

If only part of the sale proceeds is invested, the exemption does not disappear entirely. Instead, it is calculated proportionately:

Exemption = LTCG × (Investment ÷ Net Sale Consideration)

So if only half the required amount is reinvested, only part of the gain receives the exemption.

Section 54F often flies under the radar because investors naturally connect capital gains exemptions with real estate transactions alone. But for someone already planning to move money from financial assets into property, it can become a useful planning tool.

This can be especially relevant for long-term investors, NRIs, or individuals with large accumulated equity portfolios who were considering a property purchase anyway.

The full text and technical interpretation of Section 54F are discussed in the ICAI guide.

Set-Off and Carry Forward of Capital Losses

Most investors naturally focus on gains. Gains feel good. Gains get attention. Losses usually get pushed aside as something to forget and move on from.

Tax rules look at them differently.

A capital loss is not simply a disappointing investment outcome; it can also become a tool that reduces future tax liability. Used correctly, losses can soften the impact of taxes on gains and keep more money in your pocket over time.

The tax law allows losses to be adjusted against certain categories of gains and, if they cannot be fully used immediately, carried forward into future years.

Here’s how the rules work:

• Long-term capital losses (LTCL)

Long-term losses can be adjusted only against long-term capital gains.

They cannot be used against:

- Short-term gains

- Salary income

- Business income

- Any other income category

• Short-term capital losses (STCL)

Short-term losses receive broader treatment.

They can be adjusted against:

- Short-term capital gains

- Long-term capital gains

That flexibility makes STCL somewhat more useful from a planning perspective.

• Carry-forward provisions

If losses remain unused after adjustments within the same year, they do not automatically disappear.

Unabsorbed capital losses may generally be carried forward for up to 8 assessment years.

However:

- Carried-forward long-term losses can only offset future long-term gains

- Carried-forward short-term losses continue to retain broader set-off flexibility

• Filing timelines matter

This part gets overlooked surprisingly often.

To preserve the right to carry forward losses, your income tax return must generally be filed within the prescribed due date (typically July 31 for applicable taxpayers).

Missing the deadline can mean losing the ability to use those losses later.

Practical Example for Mutual Fund Investors

Suppose in FY 2025–26 you book:

- LTCG of ₹3,00,000 from Fund A

- LTCL of ₹1,00,000 from Fund B

Your calculation would look like this:

- Net LTCG after set-off = ₹3,00,000 − ₹1,00,000

- Remaining LTCG = ₹2,00,000

- Less annual exemption = ₹1,25,000

- Taxable gain = ₹75,000

- Tax at 12.5% = ₹9,375

Without setting off the loss, the tax would have been ₹21,875.

That’s a meaningful difference.

One additional point worth remembering: gains that were protected under the older grandfathering rules for pre-2018 equity holdings cannot be artificially matched against losses. Only genuine realized losses for the applicable year can be considered.

Filing Your Income Tax Return (ITR) for Capital Gains

Choosing the Right ITR Form (ITR-2 vs. ITR-3)

A lot of capital gains issues begin before tax calculations even start. The problem? Filing under the wrong ITR form.

It sounds like a small administrative detail, but choosing the incorrect return form can lead to defective return notices, correction requests, and the not-so-fun process of filing revised returns later.

Here’s a cleaner way to understand where each form fits.

ITR-1 (Sahaj)

This is the most basic return form and is intended for individuals with relatively straightforward income sources:

- Salary income

- Income from one house property

- Interest income and certain other limited sources

Capital gains generally do not belong here.

Even if you’ve made something as small as ₹1 of capital gain from a mutual fund redemption, ITR-1 stops being the correct option.

ITR-2

For many salaried individuals who invest, this is usually the form that enters the picture.

ITR-2 is designed for individuals and HUFs who have:

- Salary income

- Income from multiple house properties

- Capital gains (both LTCG and STCG)

- Foreign income or foreign assets

If you earn a salary and also invest in mutual funds, equities, or have sold property during the year, there is a strong chance ITR-2 is the form you’ll need.

The official filing guide is available here.

ITR-3

ITR-3 comes into play when investment activity moves into business territory.

For example:

- Intraday trading income

- Futures and options (F&O) trading

- Professional or business income alongside capital gains

Intraday trading is generally treated as speculative business income rather than capital gains, which changes the reporting requirements.

If your investment activity is simply long-term delivery-based investing in stocks or mutual funds, ITR-2 is usually sufficient. But if active trading or business income enters the mix, ITR-3 generally becomes necessary.

Within ITR-2 and ITR-3, Schedule CG is where capital gains are reported. It contains separate sections for:

- LTCG from equity investments (including the ₹1.25 lakh exemption calculation)

- STCG from equity

- LTCG from property transactions

- LTCG from other capital assets

- Exemptions claimed under Sections 54, 54B, 54EC, and 54F

Before filing, it also helps to keep supporting documents organized — purchase details, sale statements, exemption records, and capital gains reports. The tax planning checklist provides additional guidance on documentation requirements.

Choosing the right form may not feel like the most exciting part of tax filing, but it often prevents bigger headaches later.

Frequently Asked Questions (FAQs): LTCG tax on mutual funds

For the 2026-27 tax year, the Long-Term Capital Gains (LTCG) tax rate on equity-oriented mutual funds and listed shares is 12.5%. This rate applies only to gains that exceed the annual exemption limit of ₹1.25 lakh. Investments must be held for more than 12 months to qualify for this long-term rate.

It depends on when you bought the property. For properties purchased on or after July 23, 2024, the LTCG tax rate is a flat 12.5% without any indexation benefit. However, if you purchased the property before July 23, 2024, you can calculate your tax under both regimes (20% with indexation vs. 12.5% without indexation) and choose the option that results in a lower tax payout.

The ₹1.25 lakh exemption is a combined annual limit for all your long-term equity investments (stocks and equity mutual funds). If your total long-term equity profits for the financial year are ₹2 lakhs, the first ₹1.25 lakh is completely tax-free. You will only pay the 12.5% tax on the remaining ₹75,000. Smart investors use “tax harvesting” to book profits up to this limit every year to reset their purchase costs.

Following recent tax reforms, debt mutual funds purchased after April 1, 2023, are no longer eligible for long-term capital gains benefits or indexation. Regardless of your holding period, all gains from debt funds are added to your taxable income and taxed according to your applicable income tax slab rate.

Yes. Under Section 54F of the Income Tax Act, if you sell long-term assets like mutual funds or shares and reinvest the net sale proceeds into purchasing or constructing a single residential house in India, you can claim a proportional exemption on your capital gains tax.

| Asset Category | Holding Period (Long-Term Threshold) | LTCG Tax Rate (2026) | Annual Exemption Limit | Indexation Benefit | Applicable Exemptions |

| Equity Mutual Funds & Listed Shares | > 12 months | 12.5% | ₹1.25 lakh | No | Sec 54F, Grandfathering, Tax Harvesting |

| Property (Bought before July 23, 2024) | > 24 months | 12.5% or 20% | None | Optional (under 20% regime) | Sec 54, 54EC, 54F, CGAS |

| Property (Bought on or after July 23, 2024) | > 24 months | 12.5% | None | No | Sec 54, 54EC, 54F, CGAS |

| Debt Mutual Funds | Not Applicable | Applicable Slab Rate | None | No | None |

Common Mistakes to Avoid When Reporting LTCG

Getting the calculations right is important, but accurate numbers alone don’t guarantee a smooth filing experience. Reporting mistakes create problems too, and sometimes the issue isn’t the tax itself, it’s the mismatch between what you filed and what tax systems already know about you.

Over the last few years, reporting systems have become more connected. Mutual fund transactions, property registrations, broker reports, and third-party disclosures increasingly find their way into government records. Small oversights that once slipped through quietly are now much easier to detect.

Here are some of the most common mistakes taxpayers make:

Ignoring small SIP redemptions or minor gains

Many investors assume small transactions don’t matter.

They do.

Every redemption should be reported, even if the gain is tiny or falls below the ₹1.25 lakh exemption limit, resulting in zero tax payable. If your AIS (Annual Information Statement) reflects a transaction and your return does not, that mismatch can trigger scrutiny.

Assuming index funds are fully tax-free

This creates confusion surprisingly often.

Index funds and ETFs that track equity indices are generally considered equity-oriented investments, which means they follow the same tax rules as actively managed equity funds.

That means:

- Gains are not automatically exempt

- The ₹1.25 lakh annual exemption still applies

- Gains beyond that threshold are taxed at 12.5%

Passive investing does not mean tax-free investing.

Treating STT as a deductible expense

Securities Transaction Tax (STT) is a cost incurred during transactions, but it does not work like deductible brokerage expenses.

You generally cannot subtract STT from capital gains calculations.

Deductible costs are typically limited to items such as:

- Purchase price

- Brokerage and eligible acquisition-related expenses

Missing the grandfathering calculation

If you held equity shares or mutual fund units before February 1, 2018, ignoring the grandfathering provision can become an expensive mistake.

The January 31, 2018 NAV or market value benchmark exists to protect gains accumulated before the LTCG rules changed.

Failing to apply it can lead to paying tax on gains that are legally outside the taxable calculation.

Automatically choosing one property tax regime

If the property sold was purchased before July 23, 2024, you may be eligible to calculate tax under both systems:

- Old regime: 20% with indexation

- New regime: 12.5% without indexation

Many taxpayers simply default to one option without comparing both outcomes. Sometimes that decision ends up increasing the tax bill unnecessarily.

Missing the CGAS deadline

If you’re planning to claim Section 54 benefits but haven’t purchased the replacement property before the ITR due date, depositing the unutilized amount into a CGAS account becomes important.

Missing that requirement can invalidate the exemption claim.

Claiming exemptions without documentation

Large exemption claims increasingly attract closer examination.

Documents worth maintaining include:

- Purchase agreements

- Registration records

- Payment proofs

- Construction or completion documents where applicable

Keeping records may feel tedious in the moment. Trying to reconstruct them years later usually feels much worse.

Ignoring AIS and Form 26AS mismatches

AIS now captures information from multiple reporting channels, including:

- Mutual fund redemptions

- Property transactions

- Third-party financial reporting

If those details do not align with what appears in your return, automated discrepancy notices can follow.

Checking AIS before filing often saves time later. Access is available through the income tax portal.

For deeper analysis on reporting requirements and filing practices, the ICAI publications and detailed resources at Clear Tax provide additional guidance.

Maximizing Returns Through Smart Tax Planning

LTCG tax isn’t something investors can simply wish away. But treating it as an unavoidable expense with no room for planning leaves money on the table. The difference often isn’t between paying tax and paying no tax; it’s between paying more than necessary and paying only what the law actually requires.

The recent changes in capital gains rules have made some areas simpler and others more nuanced. Property taxation, for example, now looks different after the shift away from indexation, while equity investments continue to retain meaningful long-term tax advantages. The rules have moved, but the underlying principle remains familiar: understanding the framework usually leads to better decisions.

Here’s a quick recap of the key takeaways:

For equity mutual fund investors

- Use the ₹1.25 lakh annual LTCG exemption strategically through tax harvesting

- Consider setting off long-term losses against gains where applicable

- Explore Section 54F if purchasing a house is already part of your plans

For property sellers

- Compare both calculation methods for eligible pre–July 2024 purchases:

- 20% with indexation

- 12.5% without indexation

- Evaluate reinvestment options under Section 54

- Consider Section 54EC bonds if buying another property is not the preferred route

- Use CGAS when additional time is needed before reinvestment

For all investors

- File returns within the prescribed deadline to preserve loss carry-forward benefits

- Select the correct ITR form

- Reconcile AIS details before filing

- Maintain records for purchase costs, improvements, and exemption-related investments

For SIP investors

- Download annual capital gains statements from CAMS, KFintech, or your broker

- Understand how FIFO affects taxation

- Review annual LTCG figures and determine whether tax harvesting makes sense

One thing worth remembering: tax planning works best when it isn’t treated as a last-minute March activity.

Investors who consistently build long-term wealth usually don’t look at tax as a once-a-year formality. They fold it into the larger process — reviewing investments periodically, understanding exemptions before they become relevant, and making decisions with both returns and tax efficiency in mind.

Whether you work with a Chartered Accountant (find a registered CA at The Institute of Chartered Accountants of India, use a filing platform like Clear Tax, or manage your returns independently, the starting point remains the same: understand the rules, know your numbers, and stay ahead of the deadlines instead of reacting to them.

Even after the changes introduced through the 2024 and 2026 updates, India’s capital gains system still tends to reward patience, informed decisions, and long-term thinking.

And over time, those small advantages have a way of compounding.

Disclaimer

This article is for informational purposes only and does not constitute tax or financial advice. Tax laws are subject to change and individual circumstances vary. Please consult a qualified Chartered Accountant or tax professional before making financial decisions.

Discussion (1)

Leave a Reply