Who Can File ITR Till August 31: ITR Due Date for Non-Audit Cases 2026

Navigating the ITR Due Date for Non-Audit Cases 2026

For decades, income tax return filing in India revolved around a single date: July 31. Whether you were a salaried employee, a freelancer, a doctor running a private practice, or a small shop owner, everyone was working toward the same deadline. Predictably, that created a familiar annual rush. The Income Tax portal would slow down under heavy traffic, taxpayers would scramble to submit returns at the last minute, and errors often slipped through in the process. Herein comes the issue of ITR due date for non-audit cases in 2026.

The scale of the problem wasn’t small. In one widely reported instance, 49.29 lakh ITRs were filed on a single deadline day, pushing the system to its limits and leaving many taxpayers frustrated. Beyond the technical issues, the compressed timeline often led to costly mistakes that took months to correct.

For years, tax professionals, industry groups, and business associations argued that the problem needed a long-term fix. Temporary deadline extensions helped in the short run, but they didn’t address the underlying issue. What was needed was a structural change built into the law itself.

Assessment Year 2026-27 marks that shift.

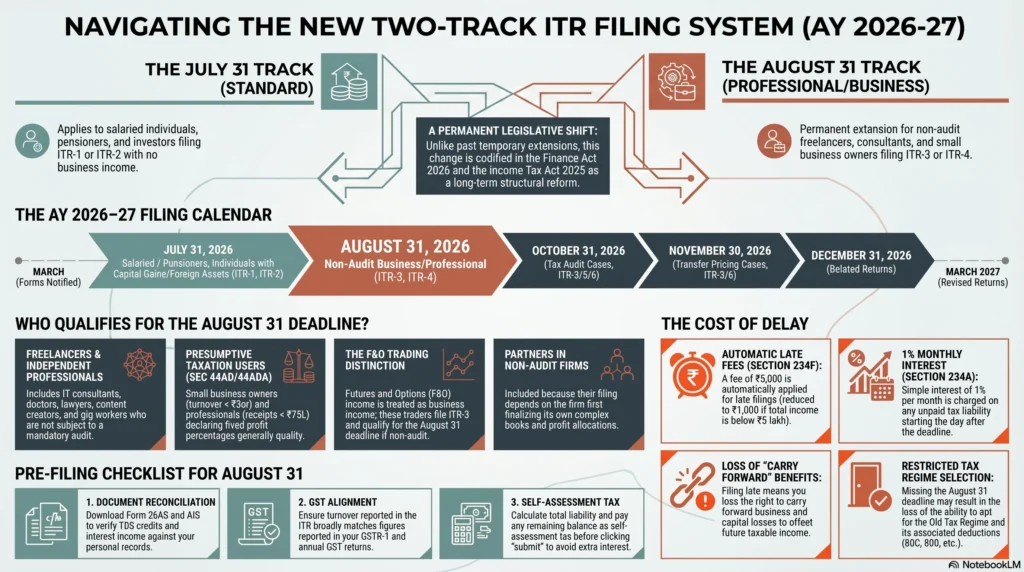

For the first time, the filing calendar now follows a formal two-track system. July 31 remains the due date for simpler returns, such as those filed by salaried individuals, pensioners, and investors with straightforward income profiles. Meanwhile, August 31 has been designated for freelancers, self-employed professionals, small business owners, and partners in non-audit firms who file ITR-3 or ITR-4.

Importantly, this is not a temporary relaxation or a one-off concession. The change has been incorporated into the Finance Act, 2026 and is intended to remain part of the filing framework going forward.

The reasoning is fairly straightforward. A salaried employee often receives a largely complete Form 16 and can file with relatively little preparation. A freelancer, consultant, or small business owner usually has a very different set of responsibilities. Before filing, they may need to reconcile accounts, match GST records, verify TDS deductions, prepare financial statements, and review multiple sources of income. That process naturally takes more time.

If you’re part of this second group and still assuming July 31 is your filing deadline, it’s worth understanding how the new rules work. In the sections ahead, we’ll look at who qualifies for the August 31 deadline, who doesn’t, the consequences of filing late, how audit-case deadlines fit into the picture, and what the new Income Tax Act 2025 means and doesn’t mean for your current return.

At a Glance: ITR Due Date For Non-Audit Cases 2026

- The Deadline: The ITR due date for non-audit cases 2026 is officially and permanently set for August 31, 2026.

- Eligible Filers: Freelancers, independent professionals, small business owners, and partners in non-audit firms.

- Applicable Forms: Primarily ITR-3 and ITR-4, covering taxpayers utilizing presumptive taxation schemes (Sections 44AD, 44ADA, and 44AE).

- Who is Excluded: Salaried employees (ITR-1/ITR-2) and taxpayers with pure capital gains must still file by July 31. Mandatory tax audit cases remain at October 31.

- Late Filing Risks: Missing this deadline triggers Section 234F penalties (up to ₹5,000), 1% monthly interest under Section 234A, and forfeits your right to carry forward business losses or opt into the old tax regime.

The Big Shift: Why Did the ITR Deadline Move to August 31?

The Permanent Change in Finance Act 2026

Unlike the deadline extensions taxpayers have become accustomed to over the years, this change is not a temporary relief measure. It is a permanent amendment to the tax filing framework.

As confirmed in this guide, the Finance Act, 2026 amended Section 139(1) of the Income Tax Act, 1961, along with corresponding provisions under the Income Tax Act, 2025. The amendment formally shifts the due date for non-audit ITR-3 and ITR-4 filers from July 31 to August 31 of the relevant assessment year. The official Memorandum to the Finance Bill 2026 makes it clear that this is intended to be a long-term structural reform rather than a one-year accommodation.

The rationale is difficult to argue with. As highlighted here, the government introduced the change to give business owners, professionals, partners of non-audit firms, and similar taxpayers more time to complete their compliance obligations before filing.

The reality is that a self-employed professional’s tax preparation process looks very different from that of a salaried employee.

A salaried taxpayer typically receives Form 16 from their employer and works with information that is already largely compiled. A freelancer, consultant, or small business owner often starts from a completely different place. They may need to finalise books of account, reconcile GST data, verify TDS credits from multiple clients, prepare financial statements, review expense claims, and ensure all income has been properly reported before they can even begin filing.

In practice, that work frequently extends well beyond July. The additional month recognises that difference and aligns the filing calendar more closely with how business and professional taxpayers actually operate.

July 31 vs. August 31: The New Split Deadline System

Assessment Year 2026-27 (Financial Year 2025-26) introduces a clear separation of filing deadlines based on the nature of the taxpayer and the complexity of their return.

According to the official deadline summary the filing calendar now works as follows:

| Taxpayer Category | ITR Form | Due Date |

| Salaried individuals, pensioners (income up to ₹50 lakh and one house property) | ITR-1 (Sahaj) | 31 July 2026 |

| Individuals/HUFs with capital gains, multiple house properties, or foreign income | ITR-2 | 31 July 2026 |

| Non-audit business and professional taxpayers | ITR-3 / ITR-4 | 31 August 2026 |

| Tax audit cases | ITR-3 / ITR-5 / ITR-6 | 31 October 2026 |

| Transfer pricing cases | ITR-3 / ITR-6 | 30 November 2026 |

| Belated returns | Applicable ITR | 31 December 2026 |

| Revised returns | Applicable ITR | 31 March 2027 |

| Updated Return (ITR-U) | ITR-U | 31 March 2031 |

One change that deserves particular attention is the revised return deadline. Previously, taxpayers had a shorter window to correct mistakes in already filed returns. For AY 2026-27, returns can now be revised until March 31, 2027, giving individuals and businesses additional time to fix genuine errors without unnecessary pressure.

The most important takeaway, however, is surprisingly simple: the August 31 extension is not universal.

Only non-audit taxpayers filing ITR-3 or ITR-4 benefit from the additional month. Salaried taxpayers, investors, and most individuals filing ITR-1 or ITR-2 continue to follow the familiar July 31 deadline. Audit cases and transfer pricing cases also remain on their existing timelines.

In other words, while the filing calendar has evolved, it has done so in a targeted way. The extra time is aimed specifically at taxpayers whose returns involve business or professional income and therefore require significantly more preparation before submission.

Who Exactly Qualifies for the August 31 ITR Deadline?

The August 31 deadline isn’t based on how much tax you pay or how high your income is. Instead, it depends largely on the nature of your income and the ITR form you’re required to file.

At its core, the extension is designed for taxpayers whose returns involve business or professional income but who are not subject to a mandatory tax audit. As explained in this guide, these taxpayers generally need more time to organise financial records, reconcile transactions, and prepare accurate returns.

Let’s look at the main groups that qualify.

Freelancers and Independent Professionals (ITR-3 & ITR-4)

Freelancers and independent professionals make up one of the largest categories benefiting from the August 31 deadline.

This includes a wide range of occupations, such as:

- Management consultants, IT consultants, and financial advisors

- Chartered accountants, lawyers, doctors, architects, engineers, and interior designers

- Writers, designers, video editors, content creators, and social media professionals

- Independent contractors and gig workers earning income outside traditional payroll systems

Many professionals fall under the presumptive taxation scheme provided by Section 44ADA. If your gross professional receipts do not exceed ₹75 lakh (or ₹37.5 lakh where cash receipts exceed the prescribed limit), you may be eligible to file ITR-4 instead of maintaining detailed books of account.

As explained in this filing guide ITR-4 allows eligible professionals to declare a fixed percentage of their receipts as profit rather than calculating actual profits and expenses in detail. For professionals covered under Section 44ADA, 50% of gross receipts is treated as taxable profit.

This significantly simplifies compliance. There’s no requirement to prepare a detailed balance sheet or profit-and-loss account. However, accuracy still matters. Before filing, taxpayers should verify their receipts against Form 26AS, AIS records, and TDS data reported by clients.

Professionals who do not use the presumptive scheme or whose receipts exceed the eligibility limits must generally file ITR-3. That process requires substantially more financial reporting, including detailed business figures, financial statements, and disclosures. For these taxpayers, the additional month until August 31 can make a meaningful difference in preparing a complete and accurate return.

Small Business Owners Without Tax Audit

Small business owners who are not required to undergo a tax audit are another major group covered by the August 31 deadline.

Under Section 44AB, a tax audit generally becomes mandatory when:

- Business turnover exceeds ₹1 crore during the financial year (or ₹10 crore where at least 95% of transactions are digital)

- Professional receipts exceed ₹50 lakh

Businesses operating below these thresholds are typically classified as non-audit cases and can take advantage of the August 31 filing deadline.

Many small businesses also choose the presumptive taxation scheme under Section 44AD. Under this framework, eligible businesses with turnover up to ₹3 crore (or ₹2 crore where cash receipts exceed the prescribed limit) can declare income at a prescribed percentage of turnover rather than maintaining detailed accounting records.

For these taxpayers, ITR-4 is usually the applicable return form.

Business owners who are not using the presumptive scheme but remain below audit thresholds generally file ITR-3. Although they avoid the audit requirement, they still need to prepare financial statements and reconcile their records before filing.

In practical terms, that process often involves:

- Reconciling sales and purchase records

- Matching GST returns with turnover figures

- Verifying TDS credits reflected in Form 26AS

- Identifying eligible business deductions

- Calculating depreciation on business assets

- Finalising profit-and-loss accounts and balance sheets

Even relatively small businesses can spend several weeks completing these tasks. The shift from July 31 to August 31 acknowledges this reality and gives taxpayers a more realistic compliance window.

For a practical understanding of which business code to use when reporting your nature of business on the ITR, see this explainer.

Presumptive Taxation Scheme Users (Section 44AD, 44ADA)

The presumptive taxation system sits at the heart of the August 31 extension because many eligible taxpayers fall within these simplified schemes.

The three key provisions are:

Section 44AD – Applies primarily to eligible businesses such as traders, contractors, and other small enterprises with turnover up to ₹3 crore. Profit is presumed at 8% of turnover, or 6% for qualifying digital receipts.

Section 44ADA – Applies to specified professionals including doctors, lawyers, chartered accountants, architects, engineers, and consultants with gross receipts up to ₹75 lakh. Profit is presumed at 50% of gross receipts.

Section 44AE – Applies to taxpayers engaged in the business of operating goods transport vehicles, subject to prescribed limits.

As explained in this , taxpayers using these presumptive schemes generally file ITR-4 and qualify for the August 31 deadline.

However, there is an important exception. If you have capital gains income, even from a relatively small transaction involving shares, mutual funds, or property, you typically become ineligible for ITR-4. In such situations, you may need to file ITR-3 or ITR-2 depending on your overall income profile.

Where business or professional income is present, ITR-3 generally becomes the appropriate form, and the August 31 deadline still applies for non-audit cases.

One additional point worth noting is advance tax compliance. Taxpayers covered under Sections 44AD and 44ADA enjoy a simplified advance tax schedule. Instead of paying tax in four instalments throughout the year, they can discharge their advance tax liability in a single payment by March 15.

Further details on advance tax obligations are available Tax Buddy.

Partners in Non-Audit Firms

Partners in partnership firms that are not subject to tax audit also benefit from the August 31 deadline.

Although a partner’s share of profit from a partnership firm is exempt in their hands under Section 10(2A), the income must still be disclosed appropriately in the return. In addition, information relating to the partnership firm and the partner’s involvement must be reported correctly.

Because a partner’s return often depends on the firm first finalising its books, determining profits, and allocating shares among partners, additional preparation time is often necessary.

This dependency is one of the reasons partners of non-audit firms were specifically included in the rationale for the extension. As noted in this guide, the Finance Act 2026 recognises that partners frequently cannot complete their own filings until the firm’s financial information has been finalised.

Similarly, Hindu Undivided Families (HUFs) earning business or professional income and not subject to audit requirements also fall within the August 31 filing category.

The broader theme remains consistent: where income depends on business records, financial statements, or professional accounts rather than straightforward salary data, taxpayers have been given an additional month to file accurately and with greater confidence.

Who Must Still File by July 31, 2026?

Salaried Individuals (ITR-1 and ITR-2)

While the August 31 deadline has received a great deal of attention, it’s important to understand that it does not apply to most salaried taxpayers.

Individuals earning primarily salary or pension income will generally continue to follow the familiar July 31, 2026 deadline. Depending on their income profile, they will typically file either ITR-1 (Sahaj) or ITR-2.

ITR-1 (Sahaj) is available to resident individuals who have:

- Salary or pension income

- Income from one house property

- Income from other sources such as bank interest or dividends

- Total income of up to ₹50 lakh

ITR-2 is meant for individuals and HUFs who do not qualify for ITR-1, usually because they have:

- Capital gains income

- More than one house property

- Foreign income or foreign assets

- Total income exceeding ₹50 lakh

However, these taxpayers must not have any business or professional income. Once business or professional income enters the picture, the filing requirements change.

As confirmed in this blog post , the August 31 extension was introduced specifically for freelancers, consultants, professionals, and small business owners filing non-audit ITR-3 or ITR-4 returns. Salaried taxpayers remain on the traditional July 31 schedule.

The distinction reflects the practical realities of tax compliance. Most salaried employees receive Form 16 from their employer by mid-June. Combined with data already available through Form 26AS, AIS, and TIS, much of the information needed for filing is already organised and pre-filled.

For someone with a straightforward salary profile, completing an income tax return can often be done in a relatively short amount of time. The government’s view appears to be that an additional month is far more valuable for taxpayers whose returns depend on business records, professional receipts, and financial statement preparation.

Capital Gains and Multiple House Property Owners

One area that often causes confusion is the treatment of taxpayers with capital gains or more complex investment portfolios.

Many people assume that because their return is more complicated than a standard salary return, they automatically qualify for the August 31 deadline. That isn’t the case.

An individual who earns capital gains from selling shares, mutual funds, real estate, or other investments but has no business or professional income will generally file ITR-2 and remain subject to the July 31 deadline.

The same principle applies to taxpayers who own multiple house properties. While having more than one property may move you from ITR-1 to ITR-2, it does not move you into the August 31 category. The extension is linked to business and professional income, not simply to the complexity of the return.

There is, however, one notable exception that catches many taxpayers by surprise: Futures and Options (F&O) trading.

Under income tax rules, F&O income is treated as business income, not capital gains. As a result, individuals actively engaged in F&O trading are generally required to file ITR-3 rather than ITR-2.

If such a taxpayer falls below the applicable audit thresholds and qualifies as a non-audit case, they become eligible for the August 31 deadline. This distinction can be significant because many investors incorrectly assume all market-related income falls under the capital gains category.

A detailed explanation of the tax treatment of F&O transactions can be found here.

The simplest way to remember the rule is this:

- Salary, pension, investments, capital gains, and house property income generally remain under the July 31 deadline.

- Business or professional income reported through ITR-3 or ITR-4 (non-audit cases) generally qualifies for the August 31 deadline.

For taxpayers unsure which form applies to their circumstances, this guide provides a useful overview of each ITR form and its eligibility requirements. Choosing the correct form from the outset can save considerable time and reduce the need for revisions later.

What Happens if You Miss the August 31 Deadline?

The extension to August 31 provides valuable breathing room for non-audit business and professional taxpayers. But it should not be mistaken for an open-ended grace period.

Once the due date passes, the consequences begin to accumulate. Some are immediate and visible, while others can have a much larger financial impact over time. Understanding these implications can help taxpayers avoid costly mistakes and plan their filing schedule more effectively.

Belated Return Deadline: December 31, 2026

Missing the August 31 deadline does not mean you lose the ability to file your return altogether.

Taxpayers can still submit a belated return up to December 31, 2026. However, filing after the original due date comes with certain penalties and restrictions that make it far less attractive than filing on time.

As noted in this guide, taxpayers who miss their original deadline can continue to file a belated return until December 31, 2026. After that, regular filing options close for AY 2026-27, although the Updated Return (ITR-U) mechanism remains available in certain situations.

The key point is simple: a belated return is a fallback option, not an alternative deadline. The longer you wait, the greater the risk of additional costs and compliance complications.

Late Filing Penalties Under Section 234F

One of the first consequences of filing after August 31 is the late filing fee under Section 234F of the Income Tax Act.

The fee structure currently works as follows:

- ₹5,000 if the return is filed after the applicable due date but on or before December 31, 2026

- ₹1,000 if your total income does not exceed ₹5 lakh

At first glance, these amounts may not seem particularly severe. However, the important thing to remember is that the fee is automatic. There is no separate notice, assessment, or discretionary approval involved. The amount is simply calculated and collected during the filing process itself.

As confirmed here, taxpayers who miss the August 31 deadline are generally liable for the Section 234F fee of ₹5,000, subject to the reduced amount for lower-income taxpayers.

For many business owners and professionals, though, the filing fee is only the beginning of the financial impact.

Interest on Unpaid Tax (Section 234A)

Late filing can also trigger interest under Section 234A if tax remains payable after adjusting TDS credits and advance tax payments.

This provision applies when:

- The return is filed after the due date, and

- There is an outstanding tax liability remaining at the time of filing.

Interest is charged at 1% per month (simple interest) on the unpaid tax amount. The calculation begins from the day immediately following the due date and continues until the date the return is filed.

For example, imagine a non-audit taxpayer still owes ₹50,000 after accounting for TDS and advance tax. If the return is filed three months late, the additional interest under Section 234A would amount to ₹1,500.

Importantly, this interest is separate from the Section 234F late filing fee. Both can apply simultaneously.

Depending on the circumstances, taxpayers may also face interest under Sections 234B and 234C for inadequate advance tax payments. While presumptive taxpayers under Sections 44AD and 44ADA benefit from a simplified advance tax schedule, they are not entirely insulated from interest consequences if tax obligations remain unpaid.

For a detailed explanation of advance tax requirements and related interest provisions, see this guide.

The practical lesson is straightforward: filing late becomes increasingly expensive when outstanding taxes are involved.

The Hidden Cost: Losing the Ability to Carry Forward Losses

While the late filing fee tends to attract the most attention, it is often not the most expensive consequence of missing the deadline.

A far more significant issue is the loss of the right to carry forward certain types of losses into future years.

Under the Income Tax Act, several categories of losses can generally be carried forward and set off against future income, but only if the return is filed within the prescribed due date.

These include:

- Non-speculative business losses

- Speculative business losses, such as certain intraday trading losses

- Short-term capital losses

- Long-term capital losses

- Certain specialised categories of losses permitted under the Act

One notable exception is house property losses, which can generally still be carried forward even when filing a belated return.

For taxpayers who have incurred substantial losses during the year, this distinction can have a major long-term tax impact.

Consider a freelance professional who records a business loss of ₹1.5 lakh during FY 2025-26. If the return is filed on or before August 31, that loss can typically be carried forward and used to offset future taxable business income. Over time, the tax savings from that carried-forward loss may be worth far more than the ₹5,000 late filing fee.

If the return is filed after the due date, however, that future tax benefit may disappear entirely.

As highlighted in this blog post, delayed filing can result not only in penalties and interest but also in the loss of valuable tax benefits, including the ability to carry forward eligible losses.

There is also a practical downside that many taxpayers overlook: refund processing may take longer for belated returns. Returns filed within the prescribed timeline are generally processed earlier, meaning delayed filers often wait longer for refunds that may be due to them.

The broader takeaway is that the true cost of late filing is rarely limited to the statutory penalty. For many business owners, freelancers, and professionals, the indirect financial consequences can be substantially larger.

Tax Audit Cases: The October 31 Deadline

To fully understand the revised filing calendar for AY 2026-27, it’s important to look beyond the August 31 deadline and examine the third category of taxpayers: those whose accounts are subject to a tax audit.

For these taxpayers, the due date remains October 31, 2026.

Unlike non-audit filers, businesses and professionals falling within the tax audit framework must complete an additional compliance process before filing their return. That process takes time, which is why the law continues to provide a longer filing window.

When Does a Tax Audit Become Mandatory?

A tax audit under Section 44AB is generally required when a taxpayer crosses specified turnover or receipt thresholds.

Broadly speaking, an audit becomes mandatory when:

- A business has turnover exceeding ₹1 crore during the financial year (or ₹10 crore where at least 95% of transactions are conducted through banking channels and other non-cash modes)

- A professional’s gross receipts exceed ₹50 lakh

- Certain taxpayers opting out of presumptive taxation declare income below the prescribed presumptive rates while their income exceeds the basic exemption limit

The purpose of the audit is not merely procedural. A practising Chartered Accountant must review the books of account, verify financial records, examine compliance requirements, and submit the prescribed audit report electronically.

Only after this audit process is completed can the taxpayer proceed with filing the income tax return using the audited figures.

Because of these additional requirements, the October 31 deadline remains necessary even after the introduction of the August 31 extension for non-audit cases.

The Audit Process and Why More Time Is Needed

For many taxpayers, the term “tax audit” sounds similar to filing an ordinary return. In practice, the two processes are very different.

Before a return can be filed, the auditor typically reviews:

- Books of account

- Bank reconciliations

- Revenue and expense records

- Statutory compliance documents

- Depreciation schedules

- Tax deductions and reporting requirements

The Chartered Accountant then prepares and uploads the prescribed audit report forms, including Form 3CA or Form 3CB along with Form 3CD, depending on the taxpayer’s circumstances.

Only after these reports have been finalised can the taxpayer complete the return filing process.

Given the amount of review and documentation involved, it would be unrealistic to expect audit cases to follow the same deadline as non-audit taxpayers. The October 31 due date reflects that practical reality.

The Important Section 44AD Lock-In Rule

Business owners using the presumptive taxation scheme under Section 44AD should pay particular attention to one rule that often gets overlooked.

If you opt for Section 44AD and later choose to declare profits below the prescribed presumptive rate, you may lose eligibility to use the scheme for the next five assessment years.

This can have significant consequences.

During that lock-out period, taxpayers are generally required to maintain detailed books of account and may become subject to tax audit requirements depending on their turnover and income levels.

For a small business owner, this isn’t just a compliance technicality. It can substantially increase accounting, record-keeping, and professional costs over several years.

As a result, taxpayers considering an exit from the presumptive scheme should evaluate the long-term implications carefully rather than focusing solely on the current year’s tax position.

What the August 31 Extension Does Not Change

One point worth emphasising is that the Finance Act 2026 has not altered the filing timeline for audit cases.

As noted at in this guide, the change applies specifically to non-audit ITR-3 and ITR-4 filers. Audit cases remain subject to the October 31 deadline, just as they were under the previous framework.

This distinction matters because some taxpayers assume that filing ITR-3 automatically entitles them to the August 31 deadline. That is not always true.

The determining factor is not the form itself but whether the taxpayer falls into the audit or non-audit category.

For example:

- A freelancer filing ITR-3 without audit requirements generally gets until August 31.

- A business owner filing ITR-3 whose accounts require audit generally gets until October 31.

The same return form can therefore carry different deadlines depending on the taxpayer’s compliance obligations.

A Note on Future Compliance Changes

Taxpayers should also be aware that broader compliance reforms continue to evolve under the new legislative framework.

For example, the Commissioner’s revision powers under Section 263 have been updated under the Income Tax Act, 2025. While these changes do not directly affect the filing of FY 2025-26 income for AY 2026-27, they form part of the broader compliance environment that businesses and professionals will operate within going forward.

A discussion of the updated Section 263 framework is available here.

For the current filing season, however, the key takeaway remains straightforward:

- Non-audit ITR-3 and ITR-4 filers generally have until August 31, 2026.

- Audit cases continue to have until October 31, 2026.

- The introduction of the August extension does not change the audit framework or audit deadlines.

Can I opt for the Old Tax Regime if I file after August 31?

This is one of the most important questions for freelancers, consultants, and small business owners because the answer can have a direct impact on how much tax they ultimately pay.

The old tax regime still offers access to popular deductions and exemptions such as:

- Section 80C investments

- Section 80D health insurance deductions

- House Rent Allowance (HRA)

- Home loan interest benefits

- Various other exemptions and deductions available under the Income Tax Act

However, the rules differ depending on the type of income you earn.

For salaried taxpayers filing ITR-1 or ITR-2, choosing between the old and new tax regimes remains relatively flexible. Even if they file a belated return, they can generally make the regime selection while filing.

The situation is very different for taxpayers earning business or professional income.

As explained in thus blog post , taxpayers with business or professional income face stricter rules when it comes to switching between tax regimes. Their flexibility is considerably more limited than that of salaried individuals.

More importantly, business and professional taxpayers who wish to opt for the old tax regime must generally complete the required declaration process before the due date of filing.

If a taxpayer covered by ITR-3 or ITR-4 misses the August 31 deadline and files a belated return, the ability to choose the old tax regime for that year may be lost altogether. In practical terms, the return would then be governed by the new tax regime.

This is why the August 31 deadline carries significance beyond late filing fees and interest. For many professionals and small business owners who actively use deductions and exemptions, missing the deadline could result in a noticeably higher tax outflow.

In some cases, the tax impact of losing access to the old regime can exceed the statutory penalty for late filing by a substantial margin.

For a detailed comparison of both regimes, see this guide.

Does the new Income Tax Act 2025 affect my FY 2025-26 return?

Given the extensive discussion surrounding the new Income Tax Act, 2025, this is a question many taxpayers are asking.

The short answer is straightforward:

No. Your AY 2026-27 return for income earned during FY 2025-26 continues to be governed by the Income Tax Act, 1961.

As clarified here, the new Income Tax Act, 2025, does not apply to income earned during FY 2025-26. Taxpayers filing returns for AY 2026-27 will continue to operate under the provisions of the existing 1961 legislation.

This means that familiar provisions remain unchanged for the current filing season, including:

- Section 80C deductions

- Section 80D deductions

- HRA benefits under Section 10(13A)

- Home loan interest deductions under Section 24(b)

- Existing presumptive taxation provisions, such as Sections 44AD, 44ADA, and 44AE

- The current ITR form structure, including ITR-1, ITR-2, ITR-3, and ITR-4

In other words, taxpayers should approach this filing season much the same way they approached previous years, while keeping the revised filing deadlines in mind.

The new Income Tax Act, 2025, is expected to become relevant when taxpayers file returns relating to income earned under the new framework in future years. For AY 2026-27, however, the existing system remains fully in force.

As discussed in this article, the government’s objective is to ensure a structured transition rather than create confusion by applying two different legal frameworks to the same income period.

For now, the focus should remain on FY 2025-26 income, the rules under the Income Tax Act, 1961, and the filing deadlines applicable to your category of taxpayer.

A Complete Compliance Checklist for August 31 Filers

The August 31 deadline may provide an extra month, but the smartest approach is still to treat filing as a process rather than a last-minute task.

A well-prepared return is less likely to attract notices, trigger reconciliation issues, or require revision later. Before submitting your ITR-3 or ITR-4 for AY 2026-27, work through the following checklist to ensure everything is in order.

Step 1 — Verify Your Income Sources

The first step is determining which ITR form actually applies to your situation.

If you’re using a presumptive taxation scheme under Sections 44AD, 44ADA, or 44AE, you may be eligible for ITR-4. If your income profile falls outside those conditions, you’ll likely need to file ITR-3.

Pay special attention to factors that can affect eligibility. For example, capital gains income, certain foreign assets or income, non-resident status, or directorship in a company may require a different form altogether.

Getting the form right at the beginning saves considerable time and helps avoid the need for corrections later.

Step 2 — Download Form 26AS and AIS

Before preparing your return, obtain both Form 26AS and the Annual Information Statement (AIS).

These documents serve as important checkpoints because they contain information reported by employers, banks, clients, financial institutions, mutual funds, registrars, and other reporting entities.

Review them carefully and compare the figures against your own records.

Look for:

- Missing TDS credits

- Incorrect income reporting

- Duplicate entries

- Interest income not reflected in personal records

- Transactions that may require clarification

Resolving discrepancies before filing is significantly easier than explaining them after the return has been submitted.

For guidance on accessing and understanding AIS, see this guide.

Step 3 — Close Your Books of Accounts

For taxpayers filing ITR-3, this is often the most time-consuming part of the process.

Your books of account should be finalised before you begin preparing the return. That means ensuring income records, expense vouchers, invoices, bank statements, and supporting documents are complete and properly organised.

The objective isn’t merely to satisfy compliance requirements. Accurate books form the foundation of an accurate return.

Rushing this step often creates downstream issues that become much harder to fix later.

Step 4 — Reconcile GST Returns

If you are registered under GST, your income tax return should broadly align with the turnover reported through GST filings.

Large mismatches between GSTR-1, GST returns, and income tax disclosures can attract unwanted scrutiny and lead to additional queries from tax authorities.

Before filing, compare:

- Reported turnover under GST

- Business receipts reflected in books

- Income figures proposed for the ITR

Any differences should be identified, documented, and explained where necessary.

Step 5 — Determine Your Tax Regime

One of the most important decisions before filing is choosing between the old and new tax regimes.

There is no universally correct answer.

For some taxpayers, lower slab rates under the new regime result in lower tax liability. For others, deductions and exemptions available under the old regime produce a better outcome.

The right choice depends on factors such as:

- Section 80C investments

- Health insurance premiums

- Housing loan benefits

- HRA claims

- Other eligible deductions and exemptions

Running both calculations before filing can prevent expensive mistakes.

You can compare scenarios using tools such as https://vakilsearch.com/article/income-tax-calculator/.

Business and professional taxpayers should be particularly careful because regime selection rules are stricter than those applicable to salaried individuals.

Step 6 — Calculate and Pay Any Remaining Tax

Once your total income has been computed, calculate the final tax liability and compare it with taxes already paid through:

- TDS deductions

- Advance tax payments

- Other eligible tax credits

If a balance remains payable, it should be discharged as self-assessment tax before filing the return.

Ignoring this step can result in additional interest under Sections 234A, 234B, and 234C, increasing the overall cost of compliance.

A few minutes spent reviewing the final tax computation can save unnecessary interest expenses later.

Step 7 — File on the Income Tax Portal

After completing all reconciliations and calculations, the return can be submitted through the official Income Tax e-filing portal.

The CBDT has already enabled filing facilities and utilities for the applicable ITR forms, including ITR-1 and ITR-4, through:

https://www.incometax.gov.in/iec/foportal/help/all-topics/e-filing-services/income-tax-returns

Before clicking submit, take one final review of:

- Personal information

- Bank account details

- Income disclosures

- Tax credits

- Deductions claimed

A final review often catches small mistakes that might otherwise require a revised return.

Step 8 — Verify the Filed Return

Key Dates of AY 2026-27

When it comes to tax compliance, knowing the right dates is half the battle. Missing a deadline can trigger penalties, interest, or the loss of valuable tax benefits, while staying ahead of the calendar makes the entire filing process far less stressful.

Here’s a quick snapshot of the key dates every taxpayer should keep in mind for AY 2026-27:

| Event | Date |

| ITR forms notified by CBDT | March 30, 2026 |

| ITR filing window opens | April 1, 2026 |

| Deadline for ITR-1 and ITR-2 (salaried/non-business taxpayers) | July 31, 2026 |

| Deadline for ITR-3 and ITR-4 (non-audit business and professional taxpayers) | August 31, 2026 |

| Deadline for tax audit cases | October 31, 2026 |

| Transfer pricing cases deadline | November 30, 2026 |

| Belated return deadline | December 31, 2026 |

| Revised return deadline | March 31, 2027 |

| Updated Return (ITR-U) filing window closes | March 31, 2031 |

Looking at the timeline as a whole, one thing becomes clear: the filing calendar is now more structured than before. Instead of a single deadline serving every category of taxpayer, the system now recognises the different compliance requirements faced by salaried individuals, professionals, business owners, audit cases, and transfer pricing cases.

For non-audit ITR-3 and ITR-4 filers, August 31 is now the key date to circle on the calendar. While the additional month provides welcome flexibility, it’s still wise to complete the filing process well before the deadline rather than relying on the final few days.

A little planning in June and July can prevent a lot of scrambling in late August.

Frequently Asked Questions: ITR Due Date For Non-Audit Cases 2026

The August 31 deadline strictly applies to taxpayers filing ITR-3 or ITR-4 whose accounts do not require a mandatory tax audit. This primarily includes freelancers, independent professionals, small business owners, and partners in non-audit firms. Taxpayers utilizing presumptive taxation schemes (Sections 44AD, 44ADA, and 44AE) also fall under this extended deadline.

No. If your income consists solely of salary, pension, house property, or capital gains, you must file ITR-1 or ITR-2 by the July 31 deadline. The August 31 extension is exclusively triggered by the presence of business or professional income. However, trading in Futures and Options (F&O) is classified as business income, which qualifies you for the August 31 deadline via ITR-3.

Filing after August 31 triggers an automatic late fee under Section 234F of up to ₹5,000 (reduced to ₹1,000 if total income is below ₹5 lakh). More critically, you accrue 1% monthly interest on unpaid taxes under Section 234A and permanently lose the right to carry forward business and capital losses to future assessment years.

Generally, no. Taxpayers with business or professional income (ITR-3/ITR-4) must file their return and the requisite declaration form on or before the original due date to opt into the old tax regime. Filing a belated return usually defaults your assessment to the new tax regime, potentially resulting in a higher tax liability.

| Taxpayer Category | Prescribed ITR Form | Official Filing Deadline | Statutory Audit Cutoff | Primary Income Types Covered | Late Filing Penalties & Consequences (Section 234F & 234A) |

| Salaried Individuals & Pensioners | ITR-1 (Sahaj) | 31 July 2026 | None | Salary, pension, domestic bank interest, and dividends (Total income $\le$ ₹50 lakh, single house property). | ₹5,000 late fee (₹1,000 if gross income $\le$ ₹5 lakh)1% simple interest/month on unpaid taxForfeiture of loss carry-forwardLoss of Old Tax Regime option |

| Investors & Multiple Property Owners | ITR-2 | 31 July 2026 | None | Capital gains, multiple house properties, foreign income, or offshore assets (No business income). | ₹5,000 late fee (₹1,000 if gross income $\le$ ₹5 lakh)1% simple interest/month on unpaid taxForfeiture of loss carry-forwardLoss of Old Tax Regime option |

| Non-Audit Businesses & Freelancers | ITR-3 / ITR-4 | 31 August 2026 | Exempt (Turnover $\le$ ₹1cr, or ₹10cr if 95% digital; Professional receipts $\le$ ₹50 lakh) | Business profits, professional fees, freelance gig income, F&O trading, and partnership firm shares. | ₹5,000 late fee (₹1,000 if gross income $\le$ ₹5 lakh)1% simple interest/month on unpaid taxForfeiture of loss carry-forwardLoss of Old Tax Regime option |

| Tax Audit Cases | ITR-3 / ITR-5 / ITR-6 | 31 October 2026 | Mandatory (Turnover $>$ ₹1cr/₹10cr or Professional receipts $>$ ₹50 lakh) | Corporate income, large-scale commercial business or professional revenue exceeding thresholds. | ₹5,000 late fee (₹1,000 if gross income $\le$ ₹5 lakh)1% simple interest/month on unpaid taxForfeiture of loss carry-forwardLoss of Old Tax Regime option |

| Transfer Pricing Cases | ITR-3 / ITR-6 | 30 November 2026 | Mandatory (International or specified domestic transactions) | Cross-border corporate transactions, international entity trade, or specified domestic transactions. | ₹5,000 late fee (₹1,000 if gross income $\le$ ₹5 lakh)1% simple interest/month on unpaid taxForfeiture of loss carry-forwardLoss of Old Tax Regime option |

Final Thoughts: Use the Extra Month Wisely

The introduction of the August 31 deadline is more than just a calendar adjustment. It reflects a long-overdue recognition that freelancers, professionals, and small business owners operate under very different compliance realities than salaried taxpayers.

For years, many self-employed taxpayers found themselves racing against a July 31 deadline while still reconciling accounts, collecting documents, matching GST data, and finalising financial statements. The additional month offers a more practical timeline and, for many, a less stressful filing season.

That said, the extension shouldn’t be viewed as an invitation to delay everything until the last week of August.

The most effective approach is to use the extra time strategically:

- Finalise books of accounts as early as possible.

- Review Form 26AS and AIS carefully.

- Reconcile GST data with turnover figures.

- Compare the old and new tax regimes before making a decision.

- Clear any outstanding tax liability before filing.

- Complete verification immediately after submission.

A good rule of thumb is to treat August 31 as the legal deadline, but aim to finish well before it. Filing a week or two early leaves room to address unexpected issues, portal slowdowns, missing documents, or last-minute corrections.

It’s also worth remembering that the consequences of missing the deadline extend beyond a simple late fee. Depending on your circumstances, a delayed return could result in interest costs, restrictions on carrying forward losses, refund delays, and even the loss of certain tax planning opportunities available only through timely filing.

The bottom line is simple: the extra month is most valuable when it’s used to improve accuracy, not postpone action.

For professional guidance on filing ITR-3 or ITR-4 for AY 2026-27, or for help navigating the presumptive taxation framework, complete compliance timelines and key rules are available here.

Disclaimer

This article is intended for general informational purposes only and does not constitute legal or financial advice. Tax rules and thresholds are subject to change. Consult a qualified Chartered Accountant or tax professional for advice specific to your situation.

Discussion (1)

Leave a Reply