What is the ONDC Framework? The 2026 E-commerce Guide for India

How the Open Network for Digital Commerce is Changing Indian Retail

India’s e-commerce story has grown fast and almost uncomfortably fast, if you pause and look at it. The market crossed $60 billion in gross merchandise value (GMV) in 2024, and projections throw around numbers like $170-$190 billion in GMV by 2030 as if that’s inevitable. Maybe it is. But here’s the part people don’t linger on enough: most of that activity flows through just two platforms-Amazon and Flipkart-which together handle over 60% of online retail.

That concentration creates a quiet kind of imbalance.

Because while the top layer looks glossy and efficient, underneath it sits a very different reality. Around 63 million micro, small, and medium enterprises-the actual backbone of India’s economy-are still, in many ways, standing outside the digital storefront. Not because they don’t want in, but because the doors aren’t exactly easy to walk through. High commissions eat into already thin margins. Platform algorithms-opaque, shifting-decide visibility. And building an independent online presence? That’s expensive enough to discourage most before they even begin.

So, the “e-commerce revolution” hasn’t really been a universal one. Not yet.

This is where the Open Network for Digital Commerce (ONDC) comes in. Not as another marketplace trying to compete for attention, but as a structural intervention, something closer to infrastructure than a product. It’s the government’s attempt to change the rules underneath the system, not just rearrange players within it.

Launched in 2021 under the Department for Promotion of Industry and Internal Trade, ONDC has been expanding steadily rather than loudly. By 2026, it has onboarded over 900 participants and is already handling millions of transactions across categories—grocery, fashion, electronics, food delivery, even mobility and financial services. The scale is still modest compared to dominant platforms, but the direction is interesting. Maybe even disruptive, if it holds.

ONDC At A Glance: Key Takeaways

Market Impact: While it won’t immediately replace giants like Amazon and Flipkart, ONDC is rapidly gaining traction in B2B commerce and hyperlocal delivery, shifting the e-commerce battleground from “platform control” to “service quality.”

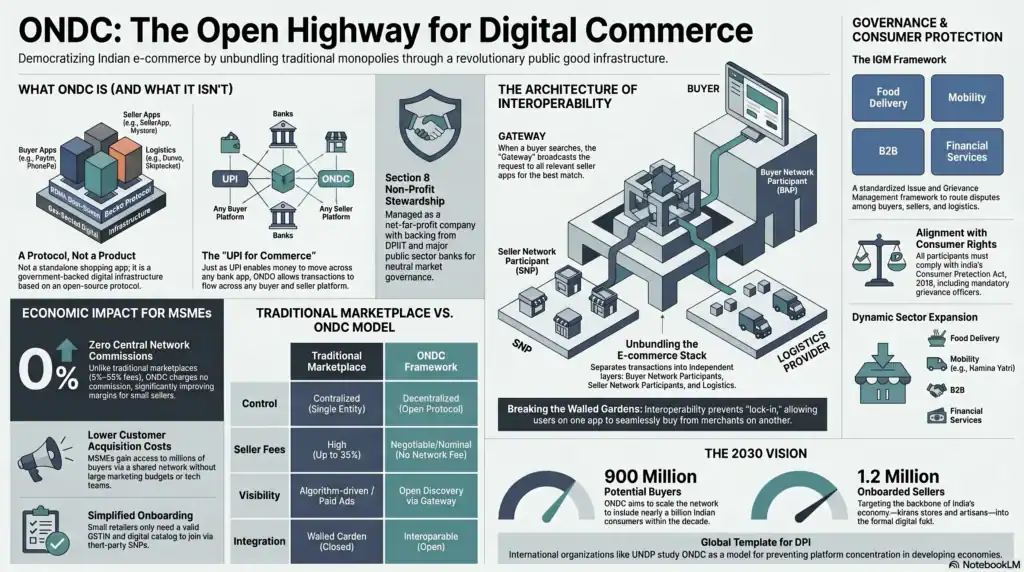

What ONDC Is: The Open Network for Digital Commerce (ONDC) is a government-backed infrastructure protocol—not a standalone shopping app. It is designed to democratize Indian e-commerce and break the walled-garden monopolies of major platforms.

How It Works: Built on the open-source Beckn Protocol, ONDC creates true interoperability. It allows a consumer using one buyer app (like Paytm) to seamlessly purchase from a merchant registered on a completely different seller app.

Zero Network Commissions: Unlike traditional marketplaces that charge heavy fees, ONDC does not charge a central network commission. This dramatically lowers customer acquisition and operational costs for MSMEs.

Easy MSME Integration: Small businesses and local retailers can easily plug into the network through Seller Network Participants (SNPs) without needing a dedicated tech team. A valid GSTIN is the primary regulatory requirement.

Unified Consumer Protection: Disputes involving multiple parties (buyer app, seller app, logistics) are streamlined through ONDC’s standardized Issue and Grievance Management (IGM) framework, ensuring compliance with India’s Consumer Protection Act.

How Does ONDC Work?

ONDC, short for Open Network for Digital Commerce, sounds abstract at first. And honestly, it is. At least until you anchor it to something familiar.

The simplest way to think about it is this: ONDC allows any buyer app to connect with any seller app, even if they’ve never “integrated” with each other in the traditional sense. No closed ecosystems, no exclusive partnerships quietly shaping who gets visibility, but just interoperability.

If that still feels fuzzy, think about email. You can send a message from Gmail to Yahoo without stopping to wonder if the two systems are compatible. They just are. ONDC is trying to bring that same kind of openness to buying and selling online, where the platform you use doesn’t quietly dictate who you can transact with.

Under the hood, this works through something called the Beckn Protocol—an open specification developed to create a shared “language” for digital commerce. Any platform that adopts this protocol effectively becomes a node in the network. And once you’re a node, you can talk to every other node. No one-off integrations, no endless API negotiations.

So in practice, a buyer using Paytm could browse products listed by a seller who’s operating through PhonePe’s merchant app—or even a completely different seller platform like SellerApp. The transaction flows through a common set of rules for ordering and fulfilment, without either side needing to directly plug into the other beforehand.

That shift, small on the surface, changes the nature of competition in a big way.

Because now, platforms aren’t competing to “own” users in a closed loop. Instead, they compete on how well they serve them. Better discovery, smoother checkout, faster delivery, cleaner interfaces—those become the battleground and not exclusivity.

And it doesn’t stop at buyers and sellers. Logistics providers, cataloguing services, financing tools, last-mile delivery networks—they can all plug into this shared system. Instead of building fragile, one-to-one integrations with a handful of dominant players, they’re building once and participating everywhere.

It’s a bit like shifting from private roads to a public highway system. Messier, maybe, but a lot more accessible.

Is ONDC a government-owned app?

Short answer: no. And this is where a lot of early confusion crept in.

When ONDC was first announced, plenty of people, including some media reports, assumed it would turn into a government-run shopping app. Something like GeM, but for everyone. Scroll, click and buy, simple.

But that’s not what ONDC is trying to be.

ONDC isn’t an app at all. It doesn’t have a storefront, it doesn’t sell products, and you don’t “open ONDC” the way you open Amazon or Flipkart. Instead, it sits behind the scenes as a kind of shared infrastructure, a framework that other apps plug into.

Structurally, it’s set up as a Section 8 not-for-profit company under the Companies Act, with backing from DPIIT, the Quality Council of India, and a mix of public sector banks and financial institutions like State Bank of India and Bank of Baroda. So yes, the government is involved, but not in the way people usually assume. It’s more about stewardship than operation.

The actual consumer experience? That happens elsewhere.

If you’ve used apps like Magicpin, Paytm, or NAMMA Yatri, you may have already interacted with ONDC without realizing it. These private platforms integrate the Beckn Protocol and act as the front-end layer. They handle discovery, browsing, ordering, all the visible parts of the experience.

ONDC itself stays in the background, doing the less glamorous but more critical work: setting the rules, defining how participants interact, handling dispute mechanisms, and maintaining the technical standards that keep the network functioning smoothly.

So, if you’re looking for a neat mental model, this helps: ONDC is closer to something like UPI than to an app store. You don’t “use” UPI directly, you use apps that run on it.

Same idea here.

What is the main purpose of the ONDC network?

At its core, ONDC is trying to do something deceptively simple: make digital commerce feel less like a gated community and more like shared infrastructure.

Right now, e-commerce in India isn’t just big, it’s concentrated. A handful of platforms sit at the centre, and if you’re a small seller trying to reach customers online, you more or less have to go through them. That dependency comes with trade-offs—fees, visibility constraints, limited control over how your business shows up.

ONDC is an attempt to rebalance that equation.

The idea is to treat the underlying infrastructure of e-commerce, the pipes through which buying and selling happen, as a kind of public good. Not owned by one company, not locked behind proprietary systems, but open enough that anyone, small retailers, street vendors, artisans, even informal businesses, can plug in and participate without needing permission from a dominant platform.

This isn’t just a philosophical stance. DPIIT explicitly framed the concentration of e-commerce power as a structural barrier to inclusion. ONDC is the policy response to that diagnosis—a way to lower the walls rather than just regulate what happens inside them.

The ONDC Strategy Paper breaks this down into three fairly clear objectives, but they land differently when you read them slowly.

First, unbundle e-commerce. Instead of one platform controlling everything-buyer interface, seller onboarding, logistics, payments-each layer becomes its own competitive space. Different players, different specializations, all connected through a shared protocol.

Second, reduce the cost of entry. Because for most MSMEs, kirana stores, and self-help groups, the problem isn’t demand, it’s access. If getting online is expensive or complicated, adoption just stalls.

Third, encourage a market for value-added services. Once the base layer is open, you start to see competition not for control, but for quality—better logistics, smarter cataloguing, more flexible financing.

And then there’s the long game. ONDC isn’t thinking in small increments, but it’s aiming for scale that sounds almost absurd at first glance: 900 million buyers and 1.2 million sellers on open networks by 2030. Whether that number is realistic or aspirational is still up for debate, but it tells you how this is being positioned, not as a niche fix, but as foundational infrastructure.

If it works, the shift won’t feel dramatic day-to-day. People will still browse, click and order. But underneath, the power dynamics would be different. Less centralized and a bit more evenly distributed.

That’s the intent, at least.

Breaking Digital Monopolies in India

If there’s one place where ONDC feels less like a technical project and more like a policy statement, it’s here.

Because the issue it’s trying to address isn’t subtle. Over time, e-commerce markets tend to tilt toward concentration—what economists like to call “winner takes all” dynamics. The more buyers a platform has, the more sellers it attracts. The more sellers it has, the more buyers show up. That loop feeds itself, and eventually, a few large players become very hard to displace.

India’s e-commerce ecosystem has been moving in that direction for a while.

Researchers studying ONDC have pointed out how these network effects don’t just reward scale, but they reinforce it. New entrants struggle to break in, not necessarily because they lack better ideas, but because the cost of competing with an entrenched platform, on logistics, visibility, and discounts, is just too high.

ONDC’s response is almost counterintuitive.

Instead of trying to build a bigger platform to compete with the existing ones, it tries to dissolve the advantage of platform size altogether. The idea is that the network effect, the thing that makes dominant platforms so powerful, should belong to the network itself, not to any single company sitting on top of it.

So, if there’s a large base of buyers, that demand becomes accessible to all sellers on the network. Not just the ones who can afford higher commissions or better ad placements.

It’s a subtle shift, but it changes who benefits from scale.

This also ties into concerns that regulators have already raised. The Competition Commission of India, for instance, has flagged practices like deep discounting and preferential treatment of private labels as potential antitrust issues. These aren’t random behaviours but they’re outcomes of platforms having too much control over both supply and demand.

ONDC doesn’t try to regulate those behaviours directly. Instead, it goes after the underlying structure that enables them.

If no single platform controls access to buyers, then the leverage to push those kinds of practices weakens. It doesn’t disappear entirely, but weakens enough to change incentives.

Of course, whether this actually “breaks” monopolies is still an open question. Systems don’t always behave the way policy designers expect them to. But as an approach, it’s interesting. It shifts the conversation from policing outcomes to redesigning the system itself.

And that’s a harder thing to do.

The Viksit Bharat Digital Economy Vision

ONDC doesn’t exist in isolation, but it’s part of a much bigger story the government has been telling about India’s digital future.

The phrase “Viksit Bharat” gets used a lot in that context. A developed India by 2047. It sounds distant, almost abstract, until you start looking at the building blocks being put in place now. Digital public infrastructure sits right at the centre of that plan—quiet systems that don’t always get attention, but end up shaping how entire markets function.

ONDC is one of those systems.

There’s already some early evidence of what this could unlock. A NASSCOM report, for instance, pointed out that when MSMEs participate in e-commerce through open networks, their cost of acquiring customers tends to drop. That matters more than it sounds. For a small business, customer acquisition isn’t just a metric, but it’s often the difference between scaling and stalling out completely.

And then there’s the broader narrative the government has been building.

Prime Minister Narendra Modi has repeatedly positioned ONDC alongside systems like Aadhaar, UPI, and DigiLocker—as part of a larger “DPI stack.” The idea is that instead of letting critical digital infrastructure be owned and controlled by private platforms, India builds shared layers that anyone can use. Payments, identity, document storage and now, commerce.

What’s interesting is that this model isn’t just being watched domestically.

International organizations-UNDP, among others-have started looking at India’s digital public infrastructure as something that could be adapted in other developing economies. ONDC, in that sense, is becoming more than just a local experiment. It’s being treated as a potential template, especially for countries trying to avoid the kind of platform concentration seen elsewhere.

Of course, visions are always cleaner than execution.

Building infrastructure is one thing. Getting millions of businesses-many of them small, informal, resource-constrained-to actually use it is another. Adoption tends to move unevenly, sometimes frustratingly slowly.

But if you step back a bit, ONDC fits into a pattern. India isn’t just digitizing services, it’s trying to standardize the rails those services run on.

And if that works, the impact won’t be loud or immediate. It’ll show up gradually—in lower costs, wider access, more competition in places where there used to be very little.

Not dramatic, but meaningful.

What is the difference between ONDC and a traditional marketplace?

The easiest way to understand this is to stop thinking in terms of apps for a second and think in terms of control.

A traditional marketplace like Amazon or Flipkart is tightly integrated. Everything sits under one roof. The app you browse on, the way sellers come onboard, how products are listed, how deliveries happen, how payments are processed-often even the products themselves through private labels-it’s all part of the same system.

That kind of setup has advantages. It’s efficient and predictable. Things tend to “just work.”

But it also means one entity sets the rules for everyone else.

ONDC flips that structure on its head.

Instead of one platform controlling the entire stack, it breaks that stack into separate layers, each operated by different players. The buyer app is one entity. The seller app is another. Logistics, payments, and credit—they’re all independent components that communicate through a shared protocol rather than a single owner’s system.

The comparison often used is a telephone network versus a telephone company, and its actually pretty apt. A telephone company owns and operates everything. A telephone network, on the other hand, lets different operators connect and communicate without needing to belong to the same system.

That’s what ONDC is trying to build for commerce.

So, in practice, a buyer might use one app, a seller might use another, and a completely different logistics provider might handle delivery. None of them need to belong to the same company, but they just need to “speak” the same protocol.

And that changes how competition plays out.

In a traditional marketplace, platforms compete to lock users into their ecosystem. The goal is to keep buyers and sellers inside your walls. On ONDC, that lock-in doesn’t really work the same way, because everyone is operating on shared infrastructure.

A BCG analysis described this as a shift from competing for control to competing for quality. If you’re a buyer app, you win by offering a better experience. If you’re a logistics provider, you win by being faster or more reliable. If you’re a seller platform, you win by making it easier for merchants to manage their business.

It’s closer, structurally, to how the internet itself works—lots of independent systems, loosely connected, constantly competing and cooperating at the same time.

Of course, that openness comes with trade-offs. Less control can mean more variability in user experience. More moving parts mean more chances for friction.

But that’s the bet ONDC is making—that the benefits of openness outweigh the comfort of control.

Understanding ONDC Buyer and Seller Nodes

Once you get past the big ideas behind ONDC, the actual structure comes down to something fairly simple: everything in the network is a “participant,” and each participant plays a specific role.

At the centre of it are two main types: Buyer Network Participants (BNPs) and Seller Network Participants (SNPs).

BNPs are the apps you and I would actually interact with. These are the platforms where you search for products, compare options, place orders, and track deliveries—the familiar front-end experience. SNPs, on the other hand, sit on the seller side. They’re the tools businesses use to list products, manage inventory, receive orders, and handle fulfilment.

So far, that sounds a lot like any marketplace setup. But the difference shows up in how these two sides talk to each other.

They don’t connect directly.

Instead, there’s an intermediary layer called the Gateway. And this is where things get a bit more interesting.

When a buyer searches for something, say, a pair of shoes, that request isn’t sent to one platform. It’s broadcast across the network through the Gateway. The Gateway then routes that request to all relevant seller apps (the SNPs), which respond with matching product listings. The buyer app gathers those responses and shows them to the user as if they came from one place.

From the user’s perspective, it feels seamless. But underneath, it’s a distributed conversation happening across multiple systems.

And it doesn’t stop at just buyers and sellers.

ONDC also allows for specialized participants—logistics providers who handle delivery, technology service providers who help smaller sellers get set up, and even credit providers offering financing at the point of sale. Each of these plays a role in the transaction, but none of them needs to belong to the same company.

It’s a layered system. Maybe a little messier than a closed platform, but also more flexible.

And that flexibility is what allows ONDC to stretch beyond just retail and into food delivery, mobility, healthcare, agriculture, and financial services. Basically, anywhere transactions can be standardized.

Which, if you think about it, is a lot of places.

How is ONDC different from UPI?

The comparison between ONDC and UPI comes up a lot, and to be fair, it’s not a bad starting point. Structurally, they’re trying to do something similar: create a shared layer that allows different apps to work with each other without needing one-to-one integrations.

UPI did that for payments. ONDC is trying to do it for commerce.

But once you go a level deeper, the differences start to show, and they’re not small.

A UPI transaction is relatively clean. Money moves from one account to another. There’s a clear start point, a clear end point, and not a lot of ambiguity in between.

But commerce is messier. Before a transaction even happens, there’s discovery: finding the product and comparing options. Then comes cataloguing, inventory checks, and pricing. After the order is placed, you’re dealing with logistics, delivery timelines, returns, refunds, and sometimes disputes. Each of those steps needs coordination, and each introduces its own set of variables.

ONDC has to account for all of that.

Which is why the Beckn Protocol, the system underlying ONDC, is significantly more complex than UPI’s payment rails. It isn’t just moving value; it’s orchestrating an entire chain of interactions between different participants.

There’s also a difference in how the two are expected to make money or not.

UPI, at least for consumers, is largely free. That decision played a big role in how quickly it scaled. ONDC, on the other hand, has indicated that it may introduce a small network fee once the ecosystem matures. Not immediately, but eventually. At the same time, individual buyer and seller apps are free to set their own pricing for the services they offer.

So yes, the analogy holds, but only up to a point.

If UPI is like a well-defined payment highway, ONDC is more like trying to map an entire city—roads, traffic rules, delivery routes, edge cases and all. It’s broader, more complicated, and probably harder to get perfectly right.

But if it works, the impact could be just as far-reaching, just in a very different way.

How can a small business or MSME join ONDC?

If you’d asked this question a couple of years ago, the answer would’ve been a bit complicated. There were more steps, more uncertainty, and honestly, a fair amount of hesitation from small businesses trying to figure out if it was worth the effort.

That’s changed.

As of 2026, getting onto ONDC is noticeably simpler, still not effortless, but far less intimidating than before. And there isn’t just one way to do it.

The most straightforward path is through a Seller Network Participant (SNP). Think of these as onboarding partners, platforms that have already built the tools and workflows needed to plug into ONDC. Instead of dealing with the technical side yourself, you go through them.

Platforms like Mystore, SellerApp, Biizd, and Digiit essentially walk you through the process. Catalogue creation, pricing, logistics setup, payment configuration—it’s all guided. For someone running a kirana store or a small handicraft business, this matters. Because the real barrier isn’t just technology but it’s unfamiliarity. Where do you even begin?

These SNPs fill that gap. And in many cases, they don’t charge upfront for onboarding. Instead, they make money through additional services—analytics, promotions and inventory tools. So, the entry point stays relatively low, at least compared to traditional marketplaces.

Now, if you’re a larger business, or a tech company, you might take a different route.

You can register as a Network Participant and build your own buyer or seller application directly on ONDC. But that’s a more involved process. It means integrating with the Beckn Protocol, going through testing in the ONDC sandbox, getting certified, signing participation agreements—the works. It’s less “onboarding” and more “building infrastructure.”

For most small businesses, though, that level of complexity isn’t necessary.

What matters is this: the door is no longer as narrow as it used to be. You don’t need a full tech team. You don’t need to build your own app. You just need a way in, and increasingly, there are people and platforms willing to provide that.

Whether businesses actually walk through that door in large numbers, that’s still unfolding.

What are the government rules for selling on ONDC?

Once you get past the excitement of “open networks” and easier onboarding, there’s a more grounded question waiting underneath: what rules do you actually have to follow?

Because ONDC may feel new, but it doesn’t exist outside the regulatory system. In fact, it sits right inside it, pulling from existing laws and adding its own layer on top.

At the base level, sellers on ONDC have to comply with the Consumer Protection (E-Commerce) Rules, 2020. These are the same rules that apply to any online seller in India. So, things like accurate product descriptions, transparent pricing, clear return and refund policies, and a working grievance mechanism aren’t optional, but they’re expected.

Nothing surprising there. But ONDC adds its own expectations, and this is where it gets a bit more specific.

For one, sellers need to keep their catalogues updated. Sounds basic, but in a network where multiple apps are pulling your data in real time, outdated inventory can quickly turn into failed orders and that reflects poorly across the system, not just on one platform.

Then there’s responsiveness. Seller apps are expected to respond to search queries within certain time thresholds. It’s a small technical detail, but it matters for keeping the network usable. If responses lag, the whole “open discovery” experience starts to break down.

There’s also the Issue and Grievance Management framework—ONDC’s own system for handling disputes. Every participant has to integrate with it, which means you can’t just ignore complaints or handle them informally. There’s a structured process, and repeated failures, like consistently not fulfilling orders or generating too many complaints, can actually get a seller delisted from the network.

And then there’s GST.

For most sellers, having a valid GSTIN is non-negotiable if you want to operate within ONDC’s formal ecosystem. There are some simplifications, like the Composition Scheme for smaller businesses, but you still need to be part of the tax system. The government has been working on making this smoother, even exploring ways to integrate GST data directly into onboarding flows, but it’s still a step you can’t skip.

So, in a way, ONDC lowers the barriers to entry, but not to accountability.

You get easier access to the market, but you’re also expected to play by clearly defined rules. For serious businesses, that’s probably a fair trade. For others, it might feel like friction.

Depends on where you’re standing.

Do sellers have to pay commission on ONDC?

This is usually the first question sellers ask, and for good reason.

If you’ve spent any time on traditional marketplaces, you already know how the math works. Commissions can range anywhere from 5% to 35%, depending on the category, and that’s before you factor in advertising spend just to stay visible. For businesses running on thin margins, it adds up quickly, sometimes to the point where growth doesn’t actually feel like progress.

ONDC takes a different approach.

At the network level, there is no commission charged on transactions. ONDC itself doesn’t take a percentage cut every time something is sold. And on paper, that’s a pretty big shift as it removes one of the biggest cost pressures sellers face on traditional platforms.

But, and this is where it helps to slow down a bit. However, that doesn’t mean selling on ONDC is completely free.

Sellers still interact with Seller Network Participants (SNPs), and those platforms may charge for the services they provide. Things like catalogue management, order processing, logistics coordination, analytics—these don’t just happen on their own. Someone builds and maintains those systems, and they need to be paid.

The difference is in how those costs are structured.

Instead of a fixed, platform-controlled commission, fees on ONDC are more flexible. They’re negotiated between the seller and the SNP, and because multiple SNPs are competing for the same sellers, there’s pressure to keep those costs reasonable.

In theory, that competition should push prices down.

And for certain categories, that difference really matters. Take grocery, for example, where margins can sit between 5% and 15%. On a traditional marketplace, commissions alone can wipe out profitability. ONDC’s model, by removing mandatory commissions, gives those businesses a bit more breathing room.

There’s also a broader structural angle here.

A McKinsey analysis pointed out that for many MSMEs, the real barrier to profitability in e-commerce isn’t demand, but it’s the combined weight of commissions and logistics costs. Open network models like ONDC try to chip away at both by introducing competition at each layer instead of bundling everything into one platform.

So, the honest answer?

No, there’s no commission in the traditional sense. But there are still costs, just distributed differently, and arguably more transparently.

Whether that ends up being significantly cheaper depends on how the ecosystem evolves. Early signs are promising. But like most things in ONDC, the real test is how it plays out at scale.

What is the ONDC grievance redressal mechanism?

One of the trickier parts of ONDC, and something people don’t always think about upfront, is what happens when things go wrong.

Because they will.

On a platform like Amazon or Flipkart, it’s relatively straightforward. You place an order, something goes wrong, and you go back to the same platform to fix it. There’s a single entity responsible, even if the seller is a third party.

ONDC doesn’t work like that.

A single transaction might involve three different players: a buyer app, a seller app, and a logistics provider—each run by a different company. So, when there’s a problem—say, a delayed delivery or a damaged product—it’s not immediately obvious who’s responsible, or where the complaint should even go.

That’s the gap ONDC is trying to solve with its Issue and Grievance Management (IGM) framework.

The Issue and Grievance Management (IGM) Framework

At a basic level, the IGM is a structured way to make sure complaints don’t get lost in that complexity.

When a buyer raises an issue, through the app they used to place the order, it gets assigned a unique ID and is pushed through the network. From there, it’s routed to whichever parties are involved: the seller, the logistics provider, and sometimes both. And all of this happens through the same underlying protocol that handles transactions, which keeps things consistent.

The framework categorizes issues into three broad buckets:

- Order-related (like non-delivery, wrong items, damaged goods)

- Payment-related (failed transactions, incorrect charges)

- Seller conduct (misrepresentation, fraudulent listings)

Each category comes with defined timelines and escalation paths. So ideally, issues don’t just linger, but they move through a process.

If the first level of resolution doesn’t work, say the buyer and seller can’t agree, the issue can be escalated to a network-level system. That escalation layer is important because without it, disputes in a decentralized system could easily become dead ends.

One genuinely useful aspect here: the buyer doesn’t need to figure out who’s at fault. You don’t have to chase the logistics provider separately or hunt down the seller’s details. You just raise the issue where you made the purchase, and the system handles the routing.

In theory, at least.

Alignment with the Consumer Protection Act

Now, ONDC’s system doesn’t replace existing legal protections, it sits alongside them.

The Consumer Protection Act, 2019, along with the E-Commerce Rules, still forms the backbone of consumer rights in India. That means if something isn’t resolved through the ONDC network within the expected timelines, buyers can still escalate the issue to consumer courts or the Central Consumer Protection Authority (CCPA).

Every network participant is also required to appoint a grievance officer, just like in traditional e-commerce setups. So, there’s accountability at both the platform level and the network level.

What ONDC is trying to do, essentially, is make sure that accountability travels with the transaction and is not tied to a single app, but embedded in the system itself.

Researchers looking at digital commerce governance have pointed out that this kind of protocol-level accountability might actually scale better than platform-based systems, especially as the number of participants grows. Because once you move beyond a handful of dominant platforms, centralized enforcement starts to strain.

That said, it’s still a complex setup.

And like most things in ONDC, the real test isn’t how it’s designed, but how smoothly it works when thousands of businesses and millions of users are all interacting at once.

Will ONDC replace Amazon and Flipkart in India?

This question comes up a lot. Almost instinctively.

And it makes sense, as whenever something new enters a space dominated by big players, the first instinct is to frame it as a replacement story.

But that framing doesn’t quite fit here.

ONDC isn’t really designed to replace Amazon or Flipkart. It’s trying to change the environment they operate in. That’s a quieter shift, but arguably a deeper one.

In fact, both Amazon and Flipkart could technically become participants on ONDC themselves. There’s nothing in the model that excludes them. The real question isn’t whether they’ll be pushed out, but it’s whether their current advantages hold up in a system where access to buyers is no longer tightly controlled.

And the honest answer is probably, at least for a while.

These platforms have spent years, billions of dollars, building logistics networks, refining user experience, and embedding themselves into consumer habits. That kind of momentum doesn’t just disappear because a new protocol exists. In categories like electronics or fashion, where returns, warranties, and after-sales service matter, tightly integrated systems still have a clear edge.

So no, ONDC isn’t likely to “replace” them in the near term. Maybe not even in the medium term.

But that doesn’t mean nothing changes.

Where ONDC starts to look more competitive is in categories that are less dependent on heavy infrastructure—grocery, hyperlocal delivery, and B2B transactions. These are areas where flexibility and access matter more than tightly controlled systems.

There are already signs of traction there. A Deloitte analysis, for instance, pointed out that ONDC’s B2B model could open up a significant market by allowing manufacturers and retailers to transact directly, cutting through layers of traditional distribution.

And that’s where the shift might actually happen, not through sudden displacement, but through gradual redistribution.

Less “one platform dominates everything,” more “different models coexist, each strong in different areas.”

Over time, that could erode some of the structural advantages dominant platforms hold today. Not eliminate them, but dilute them.

So maybe the better way to think about it is this:

ONDC isn’t trying to knock anyone off the throne. It’s trying to make sure there isn’t just one throne to begin with.

How does ONDC prevent e-commerce monopolies?

If you strip it down to one word, ONDC’s answer to monopolies is: interoperability.

That’s the lever everything else hangs on.

In a traditional marketplace, scale becomes power because access is controlled. If a platform has 200 million buyers, sellers don’t really have a choice—you go where the buyers are. And once you’re there, the platform gets to decide the terms: Pricing, visibility, commissions and all of it.

ONDC quietly removes that choke point.

On an open network, a buyer app with millions of users can’t lock those users into a closed system. By design, those buyers are accessible to any seller on the network, no matter which seller app they’re using. So, the advantage of “owning” demand starts to weaken.

It’s a subtle shift, but it changes the direction of power.

And it works both ways.

Even if a particular buyer app becomes dominant, which is entirely possible, it can’t easily turn that dominance into control over sellers. Sellers don’t lose access to buyers just because they’re using a different app. So, the usual playbook of extracting higher commissions or prioritizing certain sellers becomes harder to execute.

In that sense, ONDC isn’t just trying to fix today’s monopolies, but it’s trying to prevent future ones from forming in the same way.

Some analysts have described this as moving from a “permission-based” system to an “open access” one. Earlier, platforms decided who gets visibility and under what conditions. In ONDC’s model, access is built into the network itself.

There’s also a governance angle that’s easy to overlook.

ONDC isn’t owned by a single commercial entity. It’s a Section 8 not-for-profit with public sector involvement and DPIIT oversight. That structure doesn’t automatically guarantee neutrality, but it does make it harder for any one player to steer the network in their own favour. Policy changes require broader consensus, which slows things down, but also acts as a safeguard.

Of course, interoperability alone doesn’t magically eliminate market power. Strong players can still emerge. Some apps will be better, faster, more trusted, and users will gravitate toward them.

But the difference is this: success doesn’t automatically translate into control over the entire ecosystem.

And that’s really what ONDC is trying to redesign.

The Rise of B2B and Hyperlocal Delivery

If you’re trying to figure out where ONDC is actually gaining ground, not just in theory, but in practice, two areas keep coming up: B2B commerce and hyperlocal delivery.

And that’s not accidental.

These are spaces where the current system already feels a bit inefficient. Fragmented, sometimes opaque, and often dependent on informal relationships rather than structured systems.

Take B2B commerce.

For a lot of businesses, especially small retailers, procurement still happens through a patchwork of distributors, phone calls, WhatsApp orders, and long-standing relationships. It works, but it’s not exactly optimized. Pricing isn’t always transparent, discovery is limited, and scaling that model digitally has been harder than expected.

ONDC’s B2B layer tries to clean that up.

By standardizing how buyers and sellers discover each other and transact, it reduces some of that friction. Manufacturers, distributors, and retailers can interact through a shared protocol instead of relying on fragmented channels. In theory, that means better price discovery, fewer intermediaries, and a smoother flow of goods.

And there are early signs that larger players are paying attention.

HUL, for example, ran a pilot to help kirana stores access its distributor network through ONDC. That’s not a small signal. When a company of that scale starts experimenting with open networks, it suggests this isn’t just a policy sandbox anymore, but it’s becoming commercially relevant.

Then there’s hyperlocal delivery, which feels like a more immediate, visible use case.

Here, ONDC is enabling a different kind of competition. Instead of needing to build a full-stack app, inventory, logistics, and customer interface, new entrants can focus on one piece of the puzzle. A local seller can list inventory. A logistics provider can handle delivery. A buyer app brings in demand. None of them needs to own the entire chain.

That separation matters, especially in tier 2 and tier 3 cities.

Because in many of these places, local logistics players already exist—they know the routes, the neighbourhoods, the quirks of delivery. What they often lack is the technology layer to connect with demand at scale. ONDC bridges that gap without forcing them to become something they’re not.

So instead of a few dominant players expanding outward, you start to see smaller, localized ecosystems plugging into a larger network.

It’s still early. Not everything is smooth. But in these two areas-B2B and hyperlocal-you can start to see what ONDC looks like when it’s not just an idea, but something people are actually using.

And that’s where things usually get interesting.

Frequently Asked Questions (FAQs) About the ONDC Framework

No, ONDC is not a downloadable application or a government-owned e-commerce store. It is an open-source digital infrastructure protocol (built on the Beckn Protocol) backed by the Department for Promotion of Industry and Internal Trade (DPIIT). Think of it like UPI for e-commerce. It provides the underlying network that allows private buyer and seller apps to communicate with each other.

Since ONDC is a network and not an app, you cannot download “ONDC” from the App Store. To buy products or order food, you must use a Buyer Network Participant (BNP) app that is integrated with the ONDC network. Popular buyer apps include Paytm, Magicpin, Pincode (by PhonePe), and Mystore.

ONDC itself does not charge any central network commission for transactions. However, selling on the network is not entirely free. The Buyer Apps and Seller Apps (Network Participants) you use to connect to the network will charge nominal fees for their software, cataloging, and logistics services. These combined fees are generally significantly lower than the 20-30% commissions charged by traditional aggregators like Swiggy, Zomato, or Amazon.

Small businesses, kirana stores, and MSMEs can join the network by registering through a Seller Network Participant (SNP) like SellerApp, Mystore, or Digiit. To get onboarded, a seller typically needs a valid GSTIN, an active bank account, and a digital product catalog. The SNP handles the technical integration with the ONDC network on the seller’s behalf.

Disputes on the open network are handled through a standardized Issue and Grievance Management (IGM) framework. If a customer receives a damaged product or faces a delivery delay, they must raise a ticket on the buyer app they used to place the order. The IGM system automatically routes the complaint to the responsible party (the seller or the logistics provider) for resolution within defined legal timelines, fully complying with India’s Consumer Protection Act.

No, ONDC is not designed to replace existing platforms, but rather to break e-commerce monopolies and provide an alternative. Traditional marketplaces like Amazon and Flipkart rely on a “walled garden” or closed-loop system. ONDC democratizes the market by allowing smaller players to compete on a level playing field, driving growth particularly in B2B commerce, grocery, and hyperlocal delivery sectors.

Yes. ONDC has a rapidly growing B2B layer that allows manufacturers, wholesalers, and distributors to transact directly with local retailers (kirana stores) without relying on traditional, fragmented distribution networks. This streamlines procurement, improves price discovery, and reduces intermediary costs for Indian businesses.

Preparing Your Business for the Open Network for Digital Commerce 2026

By mid-2026, ONDC doesn’t really feel like an experiment anymore.

It’s crossed that slightly invisible line—from “interesting policy idea” to something that’s actually functioning in the real world. Transaction volumes are still smaller than the big marketplaces if you look at the aggregate, but they’re growing. Quietly, but consistently. And in certain categories-grocery, fashion, local services-early sellers are already seeing better unit economics than they’re used to elsewhere.

Which raises a slightly uncomfortable question: how long can you afford to wait?

Because the window for being early is, slowly, closing.

For MSMEs and small retailers, the immediate move is fairly straightforward—get onboarded. Not in a rushed, checkbox way, but deliberately. Find a Seller Network Participant that actually supports you well, not just one that signs you up quickly. The ONDC portal has a directory, and the process itself has been simplified to the point where, if you have a valid GSTIN and a basic catalogue, you can get started without too much friction.

The investment is low. The upside, at least in terms of access and cost efficiency, is hard to ignore.

For startups, this looks like a different kind of opportunity.

It’s rare to get in early on infrastructure that’s both open and government-backed. ONDC creates space for all sorts of niche plays—buyer apps focused on specific industries, seller tools tailored to particular segments, logistics solutions, analytics layers and embedded finance. You’re not starting from zero users; you’re plugging into an existing network.

That changes the risk equation.

There’s also a bigger economic angle here. The NASSCOM estimate, ₹1.7 lakh crore in additional MSME revenue by 2030, gets quoted a lot, and maybe it should. But numbers like that only materialize if the support systems around ONDC actually work. Digital literacy, simpler GST processes, access to credit—these aren’t side issues, they’re prerequisites.

And then there are established businesses—the ones already operating at scale.

For them, ONDC’s B2B layer is probably the most immediate lever. Procurement, distribution, wholesale, these are areas where inefficiencies quietly eat into margins. Moving even part of that flow onto a standardized digital network could mean better visibility, faster transactions, and fewer intermediaries. But more than that, it builds familiarity. And in systems like this, early familiarity tends to compound.

There’s also a geopolitical layer, oddly enough.

India has been actively positioning its Digital Public Infrastructure stack as something other countries can learn from—through the G20, through bilateral partnerships. ONDC is part of that story now. Not just as a domestic tool, but as a working example of how open commerce systems might be built elsewhere. The fact that organizations like the World Economic Forum and UNDP are studying it suggests this isn’t just internal experimentation anymore.

So, what happens next?

A lot depends on execution. Not in a vague sense, but very specifically:

- Do transaction volumes continue to grow in meaningful categories?

- Do large brands and logistics providers participate deeply, not just experimentally?

- Do buyer apps deliver an experience that people actually want to come back to?

If those pieces fall into place, ONDC could reshape Indian e-commerce in a way that feels gradual at first, and then, suddenly, obvious.

If they don’t it risks becoming another well-intentioned system that never quite reaches escape velocity.

Right now, it’s somewhere in between.

But one thing is clear: if you’re operating anywhere near retail, logistics, fintech, or digital platforms in India, ONDC isn’t something you can ignore anymore. It’s not just another trend to watch, but it’s infrastructure taking shape.

And infrastructure has a way of mattering, whether you pay attention to it or not.

Disclaimer

The content provided on this page is designed as an educational explainer to help simplify complex topics and is for general informational purposes only. While we make every effort to ensure the accuracy, completeness, and reliability of the information presented at the time of publication, facts and circumstances can change. The information provided here is on an “as is” basis and does not constitute professional, technical, or legal advice. This explainer should be used as a foundational guide for understanding the topic, and readers are encouraged to conduct their own independent research or consult with relevant professionals before taking any action based on this content.

Discussion (1)

Leave a Reply