FPI Tax Exemption on Indian Government Bonds: Impact on Domestic Yields and Debt Mutual Funds

Understanding the June 2026 FPI Tax Exemption on Indian Government Bonds

On 5 June 2026, India introduced what could prove to be one of the most significant capital market reforms in recent memory. The Ministry of Finance announced a complete exemption from income tax for Foreign Portfolio Investors (FPIs) on both interest income and capital gains earned from Government Securities (G-Secs), with retrospective effect from 1 April 2026.

This was far more than a routine tax amendment. It marked the removal of a long-standing barrier that had limited the appeal of Indian sovereign debt for many of the world’s largest pools of capital, including pension funds, insurance companies, and sovereign wealth funds. For years, India’s bond market offered attractive yields, but taxes reduced the after-tax returns available to foreign investors. The June 2026 reform changes that equation in a fundamental way.

The announcement was accompanied by an expansion of the Fully Accessible Route (FAR) and the removal of several operational restrictions governing General Route investments. Together, these measures signal a clear shift in policy thinking. India is actively positioning its sovereign debt market to attract larger and more stable foreign capital flows while strengthening its ability to finance growth and manage external-sector risks.

The implications are not limited to overseas investors. Domestic debt mutual fund investors could also feel the effects through changes in bond yields, portfolio valuations, market liquidity, and the long-term shape of India’s yield curve. What appears at first glance to be a tax reform has the potential to influence multiple layers of the financial system.

To understand the significance of this change, it helps to examine three interconnected questions:

- How exactly has the tax framework changed, and why did the government choose this moment to act?

- How do foreign bond inflows influence domestic Government Security yields?

- What are the likely consequences for debt mutual funds and the broader Indian economy?

This article explores each of these questions in detail and examines what the new zero-tax regime could mean for investors, policymakers, and India’s fixed-income markets in the years ahead.

At a Glance: FPI Tax Exemption on Indian Government Bonds

- Zero-Tax Era for FPIs: The June 2026 ordinance completely abolishes the 20% withholding tax and capital gains tax for Foreign Portfolio Investors on Indian Government Securities (G-Secs), effective retrospectively from April 1, 2026.

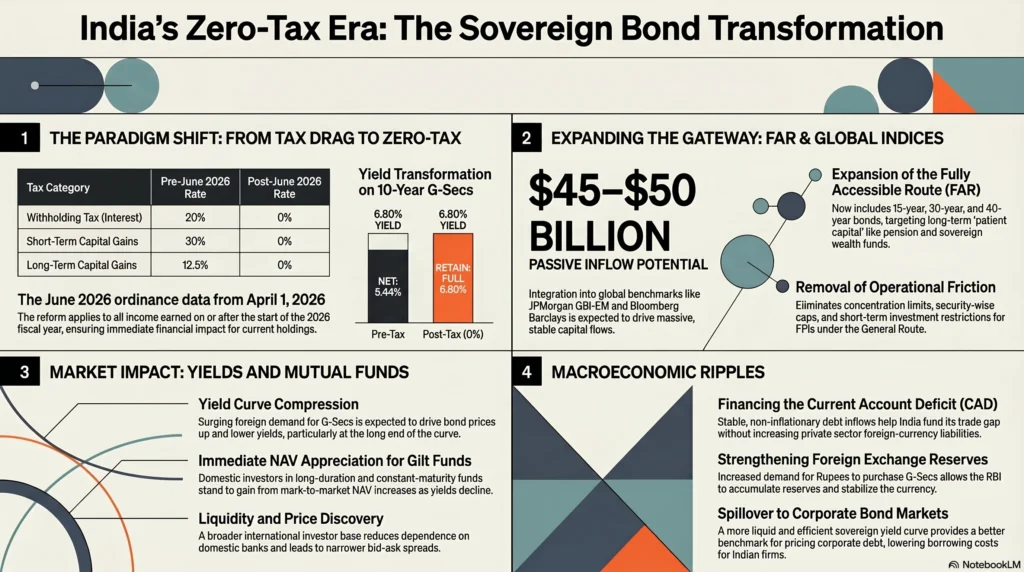

- FAR Universe Expanded: The Fully Accessible Route (FAR) now includes 15-year, 30-year, and 40-year government bonds, making India highly attractive to global pension and sovereign wealth funds seeking long-duration assets.

- $50 Billion Inflow Potential: By removing tax friction alongside the JPMorgan GBI-EM index inclusion, India is positioned to capture an estimated $45–$50 billion in passive capital inflows.

- Yield Curve Compression: Surging foreign demand for sovereign debt is expected to drive up bond prices and lower domestic yields, with the most significant impact anticipated at the long end of the curve.

- Debt Mutual Fund Gains: Domestic investors holding long-duration, gilt, and constant maturity mutual funds are primed for immediate mark-to-market NAV appreciation as bond yields decline.

- Macroeconomic Stability: Sustained, non-inflationary debt inflows will help finance India’s Current Account Deficit (CAD), strengthen foreign exchange reserves, and stabilize the Indian Rupee.

The June 2026 Ordinance: A Paradigm Shift for Foreign Portfolio Investors

The Removal of Capital Gains and Withholding Taxes on G-Secs

Before the June 2026 ordinance, foreign portfolio investors (FPIs) investing in Indian Government Securities (G-Secs) faced a tax structure that significantly reduced their net returns. Under Section 210 of the Income-tax Act, 2025, interest income from G-Secs was taxed at 20%, short-term capital gains at 30%, and long-term capital gains at 12.5%.

On paper, Indian sovereign debt already offered attractive yields. In practice, however, these taxes chipped away at returns and made India less competitive when compared with several developed markets that either imposed lower taxes or exempted foreign investors altogether. For large global institutions such as pension funds, insurance companies, and sovereign wealth funds, post-tax returns often matter more than headline yields. That distinction became a meaningful barrier to wider participation in India’s bond market.

The June 2026 reform changes that equation entirely. As confirmed in the PIB Backgrounder released on 6 June 2026, FPIs and FIIs are now exempt from tax on both interest income earned from G-Secs and capital gains arising from their sale, transfer, exchange, or redemption. The exemption applies retrospectively to income earned on or after 1 April 2026 through the Income-tax (Amendment) Ordinance, 2026.

The financial impact is easy to see. Consider a foreign institutional investor holding a 10-year G-Sec yielding 6.80%. Under the previous regime, a 20% withholding tax on interest would have reduced the effective yield to roughly 5.44%. Under the new framework, the investor keeps the entire 6.80%. When compared with sovereign bond yields in markets such as the United States or Germany, where yields remain considerably lower, India’s debt market suddenly looks far more attractive on a post-tax basis.

The government’s objective was stated clearly in the Ministry of Finance announcement on 5 June 2026. Policymakers want India’s sovereign bond market to be aligned with international norms and more accessible to long-term institutional capital. The reform specifically aims to attract stable investors such as pension funds, insurance companies, and sovereign wealth funds rather than short-term speculative money. The same tax exemption was also extended to investments made by the Bank for International Settlements (BIS), highlighting the broader ambition behind the policy.

Research from DSP Mutual Fund reinforced the investment case. According to its analysis, removing capital gains tax makes the Fully Accessible Route (FAR) significantly more appealing for global investors seeking exposure to Indian debt. Real yields on 10-year G-Secs remained comfortably positive during the March 2023 to February 2026 period, averaging around 6.8% while inflation hovered near 4%. Previously, withholding taxes diluted those real returns. With that drag removed, India now offers one of the more compelling combinations of yield and tax efficiency among major sovereign debt markets.

Expansion of the Fully Accessible Route (FAR) Universe

The tax exemption did not arrive in isolation. Alongside it, the government announced a significant expansion of the Fully Accessible Route (FAR), further opening India’s sovereign debt market to foreign investors.

Introduced by the RBI in 2020, the FAR was designed to give overseas investors unrestricted access to selected Government Securities without many of the constraints that applied under the General Route. Those restrictions included concentration limits, security-wise caps, and short-term investment thresholds, all of which added complexity and reduced flexibility for foreign investors.

The June 2026 reforms broaden the FAR universe by making the following new issuances eligible:

- 15-year Government Securities

- 30-year Government Securities

- 40-year Government Securities

- Sovereign Green Bonds (SGrBs) issued in FAR-eligible maturities

At first glance, this may seem like a technical adjustment. In reality, it represents a deliberate attempt to attract a very specific category of investor. Pension funds, insurance companies, and sovereign wealth funds typically seek long-duration assets that match their long-term liabilities. By extending FAR eligibility to longer-dated securities, India is effectively creating a larger runway for exactly the type of patient capital it wants to attract.

The existing ownership data already hints at how important the FAR has become. As of 12 May 2026, FPIs held Government Securities worth ₹3,75,171 crore, equivalent to 3.34% of the total outstanding stock of ₹112.42 lakh crore. However, most of that exposure was concentrated within the FAR segment. Holdings under FAR stood at ₹3,21,080 crore, representing 6.74% of the FAR-eligible universe, while the General Route accounted for only ₹54,091 crore, or 0.83% of its eligible stock.

That contrast tells an important story. Foreign investors have shown a clear preference for simplified access structures. The government’s response has been to expand the route that investors are already using most actively rather than creating entirely new frameworks.

The reforms also remove several longstanding restrictions under the General Route:

- Short-term investment limits have been removed.

- Concentration limits have been removed.

- Security-wise investment limits have been removed.

The overall investment caps remain unchanged at 6% of outstanding Central Government Securities and 2% of State Government Securities. In addition, the earlier distinction between “general” and “long-term” sub-limits has been consolidated into a single limit, reducing administrative complexity.

While these changes may not grab headlines in the same way as the tax exemption, they could prove equally important. Large institutional investors often evaluate not only returns but also operational efficiency. Rules that force constant monitoring, rebalancing, or compliance adjustments increase transaction costs and reduce attractiveness. By simplifying the framework, India is lowering those hidden barriers.

The scale of the opportunity is substantial. According to Legal500’s analysis of the RBI’s earlier 2025 relaxations, FPIs were using only about 14.3% of their available debt investment limits, in part because of operational frictions and regulatory constraints. In other words, a significant amount of capacity already exists within the system. The June 2026 reforms are designed to make it easier for that unused capacity to translate into actual capital inflows.

Why the Government Abolished the Tax: BoP Deficits and Rupee Stability

The decision to abolish taxes on FPI investments in Government Securities was not driven solely by a desire to make India’s bond market more attractive. At a deeper level, it reflects a broader macroeconomic objective: strengthening India’s ability to finance its external obligations while improving the stability of the Rupee.

India has long operated with a structural current account deficit (CAD). In simple terms, the country typically imports more goods, energy, and capital equipment than it exports. That gap must be financed through capital inflows. The challenge for policymakers is not just attracting capital, but attracting the right kind of capital.

Some forms of foreign money can be highly volatile. Equity flows, for example, often move rapidly in response to changes in global sentiment. Foreign direct investment tends to be more stable but can fluctuate with economic cycles and corporate investment plans. Debt inflows into sovereign bonds occupy an important middle ground. They are generally more predictable, particularly when they come from long-term institutions such as pension funds and insurance companies.

This is where the June 2026 reforms fit into the larger picture.

DSP Mutual Fund’s research highlighted that debt inflows can play a valuable role during periods when equity flows are weak or foreign direct investment slows. By attracting greater participation in Government Securities, India can help finance its current account deficit while reducing pressure on the Rupee and improving overall external-sector resilience.

The currency angle is particularly important.

When foreign investors purchase Indian Government Securities, they must first convert foreign currency into Rupees. A steady stream of such transactions creates sustained demand for the domestic currency. While this does not eliminate exchange-rate volatility, it can provide a stabilising force, especially during periods of global uncertainty.

A more stable Rupee delivers benefits that extend well beyond the bond market. It helps moderate imported inflation by reducing the cost of goods purchased from abroad, including critical imports such as crude oil. Lower imported inflation, in turn, gives the Reserve Bank of India greater flexibility when setting monetary policy. Policymakers can focus more on domestic economic conditions rather than constantly responding to currency pressures.

The government’s own assessment reflects this thinking. The PIB Backgrounder noted that the reforms are expected to strengthen India’s financial markets, support foreign exchange inflows, and attract long-term institutional investors such as pension funds, insurance companies, and sovereign wealth funds. The expectation is that these investors will provide more stable and sustained capital flows than shorter-term market participants.

Viewed through that lens, the tax exemption is about much more than bond market mechanics. It is part of a broader strategy to deepen India’s integration with global capital markets while improving the country’s ability to manage external vulnerabilities. If successful, the benefits could extend beyond lower borrowing costs and stronger bond demand to include a more resilient balance of payments position and a less volatile currency environment.

The Mechanics of FPI Inflows and Domestic Bond Yields

The Theoretical Inverse Relationship Between Bond Prices and Yields

To understand why the June 2026 reforms matter for debt markets, it helps to start with a fundamental principle of bond investing: bond prices and bond yields move in opposite directions.

When demand for a bond rises, investors compete to buy it, pushing its price higher. Since the bond’s coupon payments remain fixed, a higher purchase price naturally reduces the yield earned by new buyers. The reverse is also true. When demand weakens and prices fall, yields rise.

This relationship sits at the heart of the government’s expectation that increased foreign participation will eventually lower borrowing costs across the economy.

The theory is well established, but there is also strong empirical evidence behind it. Research by the International Monetary Fund examining 22 advanced economies between 2004 and 2012 found that a one-percentage-point increase in the share of government debt held by foreign investors was associated with a reduction of roughly 6 to 10 basis points in long-term sovereign bond yields. During the 2008-2012 period, foreign inflows were estimated to have lowered 10-year government bond yields by:

- 40-65 basis points in Germany

- 20-30 basis points in the United Kingdom

- 35-60 basis points in the United States

The same basic mechanism applies in emerging markets, including India. When foreign investors increase their allocation to Government Securities, bond prices tend to rise and yields tend to decline.

That said, emerging markets are rarely as straightforward as developed markets. Currency fluctuations, liquidity constraints, political developments, and global risk sentiment can all influence the pace and durability of yield movements. As a result, the impact of foreign inflows is often less predictable and can vary significantly over time.

The composition of those inflows also matters.

Passive flows tied to global bond indices tend to be more stable because they are driven by benchmark allocations rather than short-term market views. Once a country becomes part of a major index, funds tracking that benchmark often have little choice but to maintain exposure. Active managers, on the other hand, can increase or reduce positions quickly based on changing market conditions. Consequently, passive inflows generally exert a more persistent downward influence on yields than discretionary capital.

For India, the long-term significance of the June 2026 reforms lies not simply in attracting more money, but in attracting a larger share of this stickier, benchmark-driven capital.

Why Domestic Yields May Stay Elevated in the Short Term

Although the tax exemption and FAR expansion create a strong case for increased foreign participation, investors should not assume that Indian bond yields will fall sharply overnight.

Financial markets rarely move in a straight line. Even when a reform is clearly positive, other forces can offset or delay its impact.

One important factor is RBI intervention. If large foreign inflows create upward pressure on the Rupee, the RBI may choose to manage that impact through open market operations or liquidity measures. Such actions can partially offset the downward pressure that foreign buying would otherwise exert on bond yields.

Another consideration is the government’s borrowing programme.

India continues to finance substantial capital expenditure and development initiatives through bond issuance. If the supply of new Government Securities remains large, fresh foreign demand may be absorbed without causing a dramatic decline in yields. Put differently, increased demand does not automatically translate into sharply lower yields if there is also a steady stream of new bonds entering the market.

Liquidity management is another variable.

SBI Research noted in its July 2024 analysis that liquidity generated by bond index inclusion flows was expected to be absorbed over time, with the RBI carefully balancing the needs of both the debt market and the foreign exchange market. Similar dynamics could emerge as new inflows arrive under the tax-exempt framework.

As a result, the most likely outcome in the near term is gradual rather than dramatic yield compression. The effects may be felt most strongly at the longer end of the yield curve, where foreign institutional investors typically concentrate their purchases. Yields may drift lower, but a sudden collapse appears unlikely unless accompanied by other supportive factors such as easing inflation or a more accommodative monetary policy environment.

The Influence of Global Monetary Tightening on Emerging Market Debt

India’s bond market does not operate in a vacuum. No matter how attractive domestic reforms may be, global monetary conditions continue to play a major role in determining the flow of international capital.

When central banks in advanced economies raise interest rates, investors suddenly have access to higher returns in lower-risk markets. In those periods, emerging market debt often becomes less attractive on a relative basis, leading to slower inflows or even capital outflows.

This dynamic has been visible repeatedly over the past two decades. Periods of aggressive US Federal Reserve tightening have frequently coincided with pressure on emerging market currencies, rising bond yields, and reduced foreign participation.

According to DSP Mutual Fund’s research, foreign investors generally look for four conditions when allocating capital to emerging market debt:

- Positive real yields

- Stable or appreciating currency expectations

- Simple and efficient market access

- A supportive global risk environment

India currently scores well on several of these measures.

Real yields remain positive, the June 2026 reforms have significantly improved market accessibility, and currency stability has improved compared with several peer markets. These factors strengthen India’s competitive position in the global fixed-income landscape.

The challenge is that the fourth factor remains largely outside domestic control.

If global risk appetite deteriorates because of a recession scare in the United States, a major credit event elsewhere, or heightened geopolitical tensions, investors may still reduce exposure to emerging markets regardless of favourable local conditions. Even a highly attractive tax regime cannot completely shield a market from broader global forces.

Research from the Bank for International Settlements supports this view. Its analysis suggests that tax incentives and other policy measures can influence both the level and composition of capital flows, but they do not eliminate the influence of global monetary cycles.

The June 2026 reforms therefore improve India’s odds in the competition for global capital, but they do not guarantee uninterrupted inflows. The direction of global interest rates, investor sentiment, and international economic conditions will continue to shape how much foreign money ultimately finds its way into Indian Government Securities.

Integrating Indian G-Secs into Global Bond Indices

The Role of the JPMorgan GBI-EM Inclusion

The June 2026 tax exemption was not a standalone policy move. It forms part of a broader effort that has been unfolding for several years: integrating Indian Government Securities more deeply into global fixed-income markets.

A major milestone in that journey came in September 2023, when JPMorgan announced that Indian government bonds would be added to its GBI-EM Global index suite beginning in June 2024. For India’s bond market, this was more than a symbolic achievement. It represented recognition from one of the world’s most influential benchmark providers and opened the door to a vast pool of global capital that tracks emerging-market debt indices.

According to Manulife Investment Management’s October 2023 analysis, only FAR-designated bonds meeting specific eligibility requirements could be included in the index:

- FAR-designated bonds with a notional value of at least US$1 billion

- Securities with a remaining maturity of at least 2.5 years

- Inclusion within an index family tracking roughly US$236 billion in assets at the time

India’s weighting was structured to increase gradually, rising by one percentage point each month until reaching the maximum 10% allocation permitted under the index methodology.

That gradual inclusion process was important. It allowed markets to absorb inflows steadily rather than all at once, reducing the risk of excessive volatility while still ensuring meaningful foreign participation.

By the time the process was complete, India had become the second-largest country allocation in the index after China. Asia’s overall share of the benchmark also increased substantially, reinforcing the region’s growing importance in global fixed-income portfolios.

SBI Research estimated that the GBI-EM Global Diversified index alone had approximately US$213 billion in benchmarked assets under management as of August 2023. Based purely on index mechanics, India’s eventual 10% weighting implied passive inflows of roughly US$20-22 billion by March 2025.

The significance of the June 2026 tax reform becomes clearer when viewed against this backdrop.

Index inclusion may compel investors to buy Indian bonds, but taxes still affect how attractive those investments appear relative to competing markets. By eliminating capital gains and interest taxation on G-Secs, the government has removed a friction point that previously diluted post-tax returns. The goal is straightforward: ensure that the momentum created by global benchmark inclusion accelerates rather than loses force over time.

Projecting $45–$50 Billion in Passive Capital Inflows

India’s integration into global bond benchmarks has already moved beyond the JPMorgan inclusion.

Since then, Indian bonds have also entered the Bloomberg Barclays Emerging Market Local Currency Government Index, further expanding the universe of passive investors with exposure to Indian sovereign debt. As more benchmark providers embrace Indian bonds, the pool of capital automatically allocated to the market continues to grow.

Historically, some global index providers remained cautious. Manulife Investment Management noted that FTSE Russell had cited concerns related to taxation, registration requirements, and settlement processes as reasons for keeping India on its watch list rather than granting immediate inclusion.

The June 2026 tax exemption directly addresses one of the most significant of those concerns.

For global investors, taxation is not a minor detail buried in legal documents. It directly affects realised returns. By removing that obstacle, India strengthens its case for broader benchmark acceptance and potentially accelerates future inclusion decisions.

The numbers involved are substantial.

DSP Mutual Fund’s research showed that India attracted approximately US$34.5 billion in net FPI debt inflows between March 2023 and February 2026, despite operating under a regime that still imposed withholding. Those inflows occurred while 10-year G-Secs offered average yields around 6.8% and real yields near 2.8%.

With taxes now removed and the FAR universe expanded to include 15-year, 30-year, and 40-year maturities, India’s appeal to global fixed-income investors increases materially.

Market estimates increasingly suggest that full multi-index integration could generate an additional US$45-50 billion of passive inflows over the next few years. Active managers, attracted by the same yield and policy dynamics, could potentially contribute even more. While exact figures will depend on global conditions, the direction of travel appears clear: India is becoming increasingly difficult for international bond investors to ignore.

How Benchmark Integration Lowers Sovereign Borrowing Costs

The benefits of global bond index inclusion extend well beyond headline inflow numbers.

At the most basic level, benchmark-driven investment creates a persistent source of demand for eligible securities. Because passive funds are required to maintain exposure in line with index weights, their buying decisions are less sensitive to short-term market fluctuations.

This creates what policymakers value most: a stable demand base.

The impact operates through two primary channels:

- A direct effect, where sustained buying pressure supports bond prices and lowers yields.

- An indirect effect, where the government’s investor base becomes more diversified and less reliant on a relatively narrow group of domestic institutions.

Historically, Indian Government Securities have been heavily owned by domestic banks, insurance companies, and other local financial institutions. While this structure has provided stability, it also creates concentration risk. A broader mix of international investors can reduce that dependence and strengthen the overall resilience of the market.

Manulife Investment Management identified several additional benefits of greater foreign participation, including a larger pool of buyers, improved market liquidity, and stronger market discipline arising from increased global scrutiny.

The government’s own assessment reaches a similar conclusion. According to the PIB Backgrounder, the reforms are expected to improve liquidity, strengthen price discovery, support the development of a smoother yield curve, reduce borrowing costs, and enhance monetary policy transmission across the economy.

That last point deserves particular attention.

A well-functioning yield curve serves as the backbone of an entire financial system. It influences everything from corporate borrowing costs to mortgage rates and derivative pricing. When yields across maturities become more predictable and liquid, businesses can raise capital more efficiently, investors can price risk more accurately, and monetary policy decisions flow through the economy with greater effectiveness.

In that sense, global bond index integration is not simply about attracting foreign capital. It is also about improving the quality and efficiency of India’s broader financial architecture.

Direct Impact on Indian Debt Mutual Funds

Mark-to-Market Gains for Existing Debt Fund Holders

For investors already holding debt mutual funds, the June 2026 reforms could translate into tangible gains well before any long-term macroeconomic benefits become visible.

The funds most likely to feel the impact first are those with significant exposure to Government Securities, particularly:

- Gilt funds

- Dynamic bond funds

- Long-duration bond funds

- Constant maturity G-Sec funds

The reason is straightforward. When foreign investors buy Government Securities in large quantities, bond prices tend to rise and yields tend to fall. Since debt mutual funds mark their portfolios to market every day under SEBI’s valuation framework, any increase in bond prices immediately feeds through to the fund’s Net Asset Value (NAV).

This is where duration becomes critical.

A long-duration fund is far more sensitive to changes in interest rates than a short-duration fund. For example, a portfolio with a modified duration of roughly eight years could see its NAV rise by around 8% if yields fall by 100 basis points. Even a relatively modest decline of 25 to 30 basis points could generate NAV appreciation in the region of 2% to 2.5%, entirely from bond price movements rather than interest income.

That may not sound dramatic at first glance. Yet in fixed-income investing, where annual returns are often measured in single digits, a few percentage points of capital appreciation can make a meaningful difference to overall performance.

There is, however, an interesting contrast between foreign and domestic investors.

According to HDFC Life’s summary of current debt mutual fund taxation rules, gains from debt mutual funds continue to be taxed at the investor’s applicable slab rate following the Finance Act 2023 changes that removed indexation benefits. In other words, domestic investors do not receive the same tax-free treatment now available to FPIs investing directly in Government Securities.

That disparity may eventually spark policy discussions, particularly if foreign participation increases significantly. For now, though, the immediate benefit for domestic debt fund investors lies in potential NAV appreciation. Regardless of the tax treatment at redemption, rising bond prices can still enhance portfolio returns during the holding period.

Shifting Duration Strategies: Short-Term vs. Long-Term Funds

While the reform is broadly supportive for fixed-income markets, its benefits are unlikely to be distributed evenly across every category of debt mutual fund.

The strongest effects are expected to emerge at the longer end of the yield curve.

This is not accidental. The newly expanded FAR framework specifically includes 15-year, 30-year, and 40-year Government Securities, precisely the maturities that tend to attract pension funds, insurance companies, and sovereign wealth funds. These investors are often seeking duration rather than short-term trading opportunities.

As a result, some fund categories appear better positioned than others:

| Fund Category | Likely Impact | Primary Driver |

| Long-duration gilt funds | High | Compression in long-end yields |

| Constant maturity 10-year funds | High | Benchmark yield decline |

| Dynamic bond funds | Moderate to High | Ability to extend duration opportunistically |

| Short-duration and accrual funds | Low to Moderate | Indirect benefits from broader curve movements |

| Liquid and ultra-short funds | Minimal | Remain tied largely to RBI policy rates |

In the early stages, the yield curve could experience what market participants call a steepening effect. Foreign demand concentrates on longer-dated securities, causing those yields to fall faster than shorter-term yields.

Over time, however, the picture may evolve.

If a stronger Rupee helps contain imported inflation and creates room for monetary easing, the RBI could eventually lower policy rates. In that scenario, yield declines would spread more broadly across the curve, benefiting both short-duration and long-duration strategies.

For retail investors, this creates an interesting portfolio construction question.

Rather than making an all-or-nothing bet on long-duration funds, a balanced approach may be more sensible. Maintaining exposure to shorter-duration accrual-oriented funds can provide stability and income, while selectively allocating to long-duration funds offers the potential to benefit from bond price appreciation if foreign inflows continue to build.

SBI Research’s July 2024 analysis suggested that the benchmark 10-year yield could remain anchored around 6.80%, supported by foreign inflows, easing inflation, and fiscal consolidation. The June 2026 tax exemption introduces an additional source of demand that was not fully reflected in that earlier outlook, raising the possibility that long-term equilibrium yields could eventually settle below those levels.

Liquidity Enhancements and Reduced Portfolio Volatility

One of the most valuable consequences of deeper foreign participation may also be one of the least visible.

Liquidity.

When discussions focus on bond markets, attention usually centres on yields, returns, and interest rates. Yet market liquidity often determines how efficiently those outcomes are achieved.

A larger and more diverse investor base typically leads to:

- Narrower bid-ask spreads

- Greater trading depth across maturities

- More accurate market pricing

- Lower transaction costs for portfolio managers

These improvements may sound technical, but they have real consequences for mutual fund investors.

Consider a scenario where a debt fund manager needs to sell a large block of securities. In a shallow market with limited buyers, even routine transactions can move prices significantly. In a deeper market with a wider range of participants, large trades can be absorbed more efficiently, reducing market impact.

This becomes especially important during periods of stress.

Debt funds occasionally face redemption pressure during market uncertainty. In a market lacking sufficient liquidity, forced selling can amplify losses and create a negative feedback loop. A broader investor base, including long-term foreign institutions, can act as a stabilising force by providing additional demand when domestic participants become cautious.

The broader development benefits are also significant.

In its December 2025 report on India’s corporate bond market, NITI Aayog identified limited secondary market liquidity as one of the major obstacles to deeper bond market development . Expanding and diversifying the investor base was highlighted as a key solution.

The June 2026 reforms directly support that objective. While the immediate focus is on Government Securities, stronger liquidity and more active participation in the sovereign market can create positive spillover effects across the wider fixed-income ecosystem.

For debt mutual fund investors, those benefits may not show up in headline returns immediately. They are more subtle than a jump in NAV. Yet over time, improved liquidity, better pricing efficiency, and reduced market friction can contribute meaningfully to both portfolio stability and overall market health.

Broader Macroeconomic Ripples of the Zero-Tax Era

Financing the Current Account Deficit (CAD) with Non-Inflationary Capital

One of the less obvious but potentially most important benefits of the June 2026 reforms lies in how India finances its current account deficit.

India has historically run a current account deficit because it imports more goods, energy, and capital equipment than it exports. The size of that deficit varies from year to year, but the reality remains the same: the gap must be funded through foreign capital.

Not all capital is created equal.

Some sources of funding are inherently more volatile. Equity flows can reverse quickly when investor sentiment changes. Foreign direct investment tends to be stickier, but it depends on long-term corporate investment decisions and broader economic conditions. External commercial borrowings provide access to capital but also add foreign-currency liabilities to private-sector balance sheets.

Government bond inflows occupy a different space altogether.

When foreign investors purchase Indian Government Securities through the FAR framework, they are effectively helping finance the country’s external funding needs without increasing foreign-currency debt exposure for Indian companies. That makes these inflows particularly attractive from a macroeconomic perspective.

DSP Mutual Fund’s research highlighted how important debt inflows became between March 2023 and February 2026. During a period when equity FPI flows and foreign direct investment faced challenges, India still attracted approximately $34.5 billion of debt inflows, helping support the balance of payments and reduce pressure on the external sector.

The June 2026 reforms are designed to strengthen that stabilising mechanism.

By removing taxes and broadening access through the FAR route, policymakers are attempting to make sovereign debt inflows a larger and more reliable component of India’s capital account. The objective is not simply to attract more money, but to attract capital that can remain invested through market cycles.

Another important feature of bond inflows is that they tend to be less inflationary than some alternative forms of capital.

Large-scale infrastructure spending or investment-driven capital inflows often flow directly into economic activity, increasing demand across sectors. Bond inflows work differently. Their primary effects are felt through the exchange rate and the yield curve. They support the Rupee, help lower borrowing costs, and improve financial conditions without necessarily creating the same immediate demand-side inflation pressures.

Manulife Investment Management’s analysis suggested that stronger bond-related inflows could help narrow India’s current account deficit and, under favourable circumstances, even push the external balance closer to surplus territory. The tax exemption strengthens the likelihood of that outcome by making Indian sovereign debt more attractive to global investors.

Strengthening Foreign Exchange Reserves

A second major consequence of sustained bond inflows is their effect on India’s foreign exchange reserves.

Whenever foreign investors buy Indian Government Securities, foreign currency must first be converted into Rupees. Those transactions increase the supply of foreign currency within the domestic financial system and can contribute to reserve accumulation, particularly when the Reserve Bank of India intervenes to smooth exchange-rate movements.

The mechanics may seem technical, but the implications are significant.

Foreign exchange reserves function as a financial shock absorber. They provide confidence to investors, support currency stability, and give policymakers greater flexibility during periods of global uncertainty. Countries with strong reserve positions are generally viewed as more resilient because they have a larger buffer available to manage external disruptions.

This became especially clear during previous episodes of global market stress, when reserve strength often determined how effectively countries could defend their currencies and maintain financial stability.

The government expects the June 2026 reforms to contribute meaningfully to this objective. The PIB Backgrounder specifically notes that the changes are expected to strengthen foreign exchange reserves by attracting stable, long-term capital from institutions such as pension funds, insurance companies, and sovereign wealth funds.

Larger reserves also provide practical policy advantages.

A stronger reserve position gives the RBI more room to manage periods of currency volatility without exhausting resources. It can intervene more confidently when markets become disorderly and maintain liquidity conditions with greater flexibility. In effect, every additional layer of reserve strength increases the country’s ability to withstand external shocks.

For a fast-growing economy that remains deeply connected to global trade and capital markets, that resilience carries substantial value.

The Knock-On Effect for Corporate Bond Markets

Although Government Securities are the direct beneficiaries of the tax exemption, the longer-term impact could extend well beyond sovereign debt.

Corporate bond markets depend heavily on the sovereign bond market functioning efficiently.

Every corporate bond is priced relative to a government bond benchmark. Investors typically assess a company’s borrowing cost as the yield on a comparable Government Security plus an additional spread that compensates for credit risk. Because of this relationship, improvements in the sovereign market often ripple outward into the broader fixed-income ecosystem.

NITI Aayog’s December 2025 report identified the development of a liquid and reliable sovereign yield curve as one of the most important prerequisites for a stronger corporate bond market.

When sovereign bonds trade actively and price discovery improves, corporate issuers benefit in several ways:

- More accurate benchmark pricing

- Better liquidity across fixed-income markets

- Greater investor confidence

- Lower borrowing costs for high-quality issuers

India’s corporate bond market has expanded considerably over the past decade. Outstanding issuances increased from approximately ₹17.5 trillion in FY2015 to ₹53.6 trillion in FY2025, representing annual growth of nearly 12%.

Even so, the market remains relatively small compared with several Asian peers. Corporate bonds account for only around 15-16% of GDP, significantly below levels seen in countries such as South Korea, Malaysia, and China.

This gap represents both a challenge and an opportunity.

Earlier reforms had already begun addressing barriers to foreign participation. Legal500’s review of the RBI’s 2025 changes noted that restrictions such as short-term investment limits and concentration limits were removed for FPIs investing in corporate debt through the General Route.

The June 2026 G-Sec tax exemption builds on those earlier initiatives.

Taken together, the reforms create a more coherent framework for attracting global capital across India’s entire fixed-income market. Sovereign bonds become easier to access, pricing becomes more efficient, liquidity improves, and corporate debt markets stand to benefit from the stronger foundation underneath them.

The result may not be immediate, and it certainly will not happen overnight. But over time, the cumulative effect could be a deeper, more liquid, and more internationally competitive bond market that serves both government and corporate borrowers more effectively.

Strategic Takeaways for Retail and Institutional Investors

Recalibrating Fixed Income Portfolios for the New Yield Curve

The June 2026 FPI tax exemption is more than a policy announcement. It changes a key demand driver in India’s government bond market. For investors, that means reassessing how fixed-income portfolios are positioned for the years ahead.

The most obvious beneficiaries are likely to be long-duration strategies. If foreign participation continues to increase and bond yields gradually move lower, funds holding longer-maturity Government Securities stand to gain the most from price appreciation.

For investors with a time horizon of three years or longer, long-duration gilt funds and dynamic bond funds may warrant closer attention. The case here is not built solely on coupon income. It is based on the possibility of capital gains generated by falling yields and rising bond prices.

Retail investors in lower tax brackets may find this particularly attractive. In a declining yield environment, debt funds can potentially outperform fixed deposits on an after-tax basis because a portion of returns comes from NAV appreciation rather than periodic interest payments. The gap becomes less pronounced for investors in higher tax brackets, where the eventual tax treatment of gains remains an important consideration.

That does not mean shorter-duration funds should be ignored.

Short-duration and accrual-oriented funds continue to serve an important role in portfolio construction. They generally offer greater stability, lower sensitivity to interest-rate movements, and a more predictable return profile. For many investors, a balanced or “barbell” approach may be the most practical solution: maintaining exposure to short-duration funds for stability while allocating a portion of the portfolio to long-duration strategies that could benefit from structural changes in the bond market.

The key point is that the fixed-income landscape is evolving. A portfolio built for a market dominated almost entirely by domestic buyers may not be optimally positioned for a market increasingly influenced by global capital flows.

Monitoring Global Geopolitics vs. Domestic Tax Policy

While the tax reform improves India’s attractiveness, investors should resist the temptation to view it as a guarantee of uninterrupted foreign inflows.

Global capital rarely moves based on a single factor.

Even after the June 2026 changes, India’s bond market remains influenced by developments far beyond its borders. International investors continuously compare opportunities across countries, currencies, and asset classes. A favourable tax regime helps, but it does not eliminate broader market risks.

Several variables deserve close monitoring:

- The direction of US Federal Reserve policy

- Global liquidity conditions

- Inflation trends in major economies

- Geopolitical tensions and risk-off events

- Currency movements across emerging markets

Among these, US monetary policy remains particularly important. When US interest rates rise, investors can earn higher returns in dollar-denominated assets with relatively lower risk. That often reduces the appeal of emerging-market debt and can slow capital inflows.

Geopolitical shocks create a similar challenge. During periods of heightened uncertainty, investors often prioritise liquidity and safety over yield, leading to temporary withdrawals from emerging markets regardless of local fundamentals.

This is why institutional investors should view the reform as a supportive structural factor rather than a permanent guarantee of demand.

India’s advantages remain compelling: positive real yields, improving market access, and a large, growing economy. Yet foreign investors also care deeply about currency stability. If external developments place sustained pressure on the Rupee, some investors may reduce exposure despite the tax benefits now available.

The BIS research on capital flow management reaches a similar conclusion. Tax incentives and policy reforms can influence the average level of inflows and improve market attractiveness, but they cannot eliminate the cyclical nature of global capital movements.

In other words, the reform strengthens the foundation, but market cycles will still exist.

Navigating the Market in the Post-Tax G-Sec Environment

For investors actively positioning for the post-tax environment, the opportunity is likely to be found in understanding where foreign demand is most likely to concentrate.

The long end of the yield curve appears to be the most obvious candidate.

The newly FAR-eligible 15-year, 30-year, and 40-year Government Securities align closely with the needs of pension funds, insurance companies, and sovereign wealth funds. These institutions typically seek long-duration assets and are less focused on short-term trading opportunities. As a result, any yield compression driven by foreign buying could be most visible in these maturities.

Investors seeking to benefit from this trend may consider building exposure gradually rather than investing all at once. Bond markets can experience periods of volatility even within longer-term positive cycles, and staggered allocations help reduce timing risk.

Monitoring RBI actions will also remain important.

If the RBI chooses to absorb the effects of foreign inflows aggressively through open market operations, the downward pressure on yields may be less pronounced. On the other hand, if policymakers allow market forces to play a larger role, the benefits of increased foreign demand may be reflected more fully in bond prices.

Corporate bond funds deserve attention as well.

Although they are not the primary beneficiaries of the tax exemption, they could gain indirectly from improvements in the sovereign bond market. A deeper and more liquid Government Securities market creates a stronger benchmark for pricing corporate debt. Over time, this can contribute to narrower credit spreads and lower borrowing costs for high-quality issuers.

Perhaps the most important takeaway is the need for patience.

The history of foreign debt flows into India suggests that meaningful inflow cycles tend to unfold over several years rather than several quarters. DSP Mutual Fund’s data shows that India’s strongest five-year period for debt inflows, from March 2010 to February 2015, attracted approximately $46.5 billion while 10-year yields averaged 8.23%.

The current backdrop may be even more supportive. Real yields remain positive, access restrictions have been eased, benchmark inclusion is expanding, and the tax barrier has effectively been removed.

That does not mean the path will be smooth. Markets rarely move in straight lines. But it does suggest that investors should think in terms of multi-year structural shifts rather than short-term market fluctuations.

Frequently Asked Questions: FPI Tax Exemption on Indian Government Bonds

The Income-tax (Amendment) Ordinance, 2026, completely exempts Foreign Portfolio Investors (FPIs) from both the 20% withholding tax on interest income and capital gains tax (previously 30% STCG and 12.5% LTCG) on Indian Government Securities (G-Secs), applied retrospectively from April 1, 2026.

In the long term, large-scale foreign capital inflows increase demand for G-Secs, driving bond prices up and yields down (yield compression). However, short-term yields may stay elevated due to aggressive RBI liquidity absorption and heavy government borrowing schedules.

Long-duration gilt funds, constant maturity 10-year G-Sec funds, and dynamic bond funds benefit most. As foreign inflows drive down long-term yields, these high-duration portfolios experience immediate mark-to-market net asset value (NAV) appreciation.

No. The June 2026 tax exemption applies exclusively to direct G-Sec and FAR bond investments by FPIs, FIIs, and the Bank for International Settlements (BIS). Domestic debt fund capital gains continue to be taxed at the investor’s applicable income tax slab rate.

The framework expands the FAR universe to include 15-year, 30-year, and 40-year Government Securities, alongside Sovereign Green Bonds (SGrBs) issued within these long-dated maturity buckets.

Impact of the June 2026 FPI Tax Exemption on Indian Debt Markets

| Asset Class | Investment Route | Previous Tax | New Tax | Primary Macro Objective |

| Long-Dated G-Secs (15-40y) | Fully Accessible Route (FAR) | ~32.5% (WHT+LTCG) | 0% | Stabilize Rupee & Finance CAD |

| Sovereign Green Bonds (SGrBs) | Fully Accessible Route (FAR) | ~32.5% (WHT+LTCG) | 0% | Sustainable capital integration |

The Long-Term Outlook: How the Zero-Tax Era Reshapes India’s Fixed-Income Ecosystem

The June 2026 FPI tax exemption marks a turning point in India’s approach to global capital. More than a tax change, it signals a willingness to compete for international investment through market accessibility, policy consistency, and attractive real yields.

For the bond market, the implications are significant. Lower barriers to entry can encourage greater foreign participation, deepen liquidity, improve price discovery, and place gradual downward pressure on borrowing costs. For debt mutual fund investors, particularly those with exposure to longer-duration strategies, the reform creates the potential for meaningful mark-to-market gains as these dynamics play out.

The benefits extend beyond investment portfolios. Stronger bond inflows can help finance the current account deficit, support the Rupee, strengthen foreign exchange reserves, and contribute to the broader development of India’s fixed-income ecosystem.

Of course, no policy reform operates in isolation. Global interest rates, geopolitical developments, inflation trends, and investor sentiment will continue to influence the pace and direction of foreign capital flows. Yet by removing a longstanding tax friction and expanding market access, India has materially improved its position in the global competition for fixed-income capital.

The full effects are unlikely to emerge within a few quarters. They will unfold gradually, through changes in investor behaviour, market structure, and capital allocation patterns. But if the reform achieves its intended objectives, it could help reshape India’s sovereign debt market for years to come.

Disclaimer

This article is published for informational and educational purposes only and does not constitute investment advice, financial planning guidance, or a recommendation to buy or sell any security, mutual fund, or financial instrument. The analysis presented here is based on publicly available sources, regulatory notifications, and third-party research cited within the text; readers should independently verify all information before relying on it. Past performance of any asset class, flow data cited, or yield trends referenced is not indicative of future results. Investments in debt mutual funds, Government Securities, and fixed income instruments are subject to market risks, interest rate risk, credit risk, and liquidity risk. Please read all scheme-related documents carefully before investing. Readers are advised to consult a SEBI-registered investment adviser or qualified financial professional before making any investment decisions based on the information contained herein. The views expressed are those of the author and do not represent the official position of any regulator, government body, or financial institution.

Leave a Reply