The Complete Guide to the Section 80-IAC Income Tax Exemption for Startups (2026–2030)

Unlocking the Section 80-IAC Income Tax Exemption for Startups

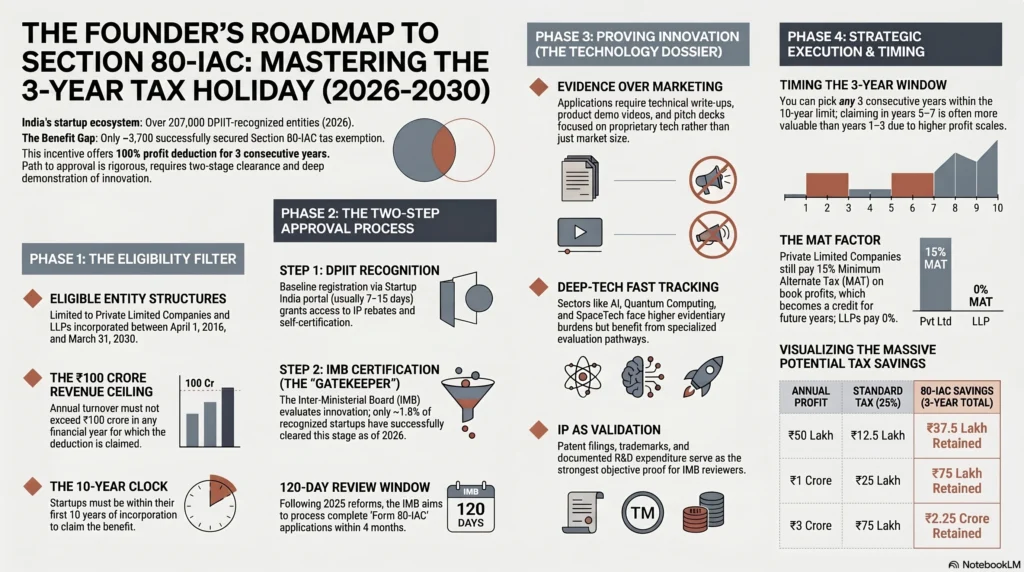

India’s startup ecosystem has grown at a remarkable pace, crossing 207,000 DPIIT-recognised startups by April 2026. Yet a surprisingly small number, roughly 3,700, have successfully accessed one of the most valuable tax benefits available to founders: the three-year, 100% income tax exemption under Section 80-IAC of the Income Tax Act.

That disparity is not accidental.

While the benefit itself is generous, getting there is far from straightforward. Founders must secure two separate government approvals, demonstrate genuine innovation through detailed documentation, and carefully choose the right time to claim the exemption. Many startups either remain unaware of the process or assume the requirements are simpler than they actually are.

This guide is designed to make that journey clearer. It breaks down the eligibility criteria applicable from 2026 to 2030, explains the DPIIT recognition and Inter-Ministerial Board (IMB) approval process, outlines the required documentation, and walks through the filing procedure step by step. It also explores the strategic considerations that can significantly influence the amount of tax a startup ultimately saves.

At A Glance: Section 80-IAC Income Tax Exemption For Startups)

- 100% Income Tax Holiday: Eligible Indian startups can claim a complete tax deduction on business profits for any 3 consecutive assessment years within their first 10 years of operations.

- Extended Incorporation Deadline: To qualify, the startup must be incorporated between April 1, 2016, and March 31, 2030.

- Two-Step Mandatory Approval: Founders must first secure DPIIT Recognition (Step 1), followed by a rigorous Inter-Ministerial Board (IMB) Certification (Step 2) to officially unlock the tax exemption.

- Strict Entity Eligibility: The benefit is exclusively available to Private Limited Companies (which remain subject to 15% Minimum Alternate Tax) and Limited Liability Partnerships / LLPs (which have zero MAT liability).

- Annual Turnover Limit: The startup’s overall business turnover must not exceed ₹100 crore during any financial year the deduction is claimed.

- Proof of Genuine Innovation: IMB approval heavily depends on a technology dossier proving technological innovation, high scalability, and market potential. Businesses formed by splitting or reconstructing an existing entity are strictly rejected.

- Angel Tax Abolished: Fundraising is now much simpler for recognized startups, as the Angel Tax was permanently abolished effective April 1, 2025.

What is the Startup India Tax Exemption (Section 80-IAC)?

Section 80-IAC of the Income Tax Act, 1961 was introduced on 1 April 2017 as a key tax incentive under the Startup India initiative. Its purpose is simple in theory but highly valuable in practice: eligible startups can claim a 100% deduction on profits from their business for any three consecutive assessment years within the first ten years of incorporation. The complete legal provisions and official notifications can be accessed at the official website of the Income Tax Department.

What makes this benefit stand out is that it is not a reduced tax rate or a limited deduction. For qualifying profits, it effectively creates a tax-free period for the chosen years. However, access to the exemption depends on clearing two separate requirements. A startup must first obtain DPIIT recognition and then secure certification from the Inter-Ministerial Board (IMB).

Core Benefits of 80-IAC Registration

The numbers can be significant, especially for startups entering a growth phase.

For example, a startup generating ₹50 lakh in annual profit and otherwise paying tax at the standard 25% corporate rate could save approximately ₹12.5 lakh per year. Over the full three-year exemption period, that translates to around ₹37.5 lakh retained within the business. For startups producing cumulative profits of ₹3 crore during the exemption window, the savings can climb to roughly ₹75-90 lakh. As explained in this guide, this is capital that can be redirected into hiring, product development, market expansion, or simply extending runway during critical growth stages.

Beyond the income tax holiday itself, several related benefits may also become available:

- ESOP tax deferral under Section 192(1C): Employees of IMB-certified startups can defer tax on stock options for up to five years, until sale of shares, or until an exit event, whichever occurs first.

- Relaxed loss carry-forward rules under Section 79: Eligible startups may continue carrying forward losses despite changes in shareholding, subject to prescribed conditions.

- Patent and trademark fee rebates: DPIIT-recognised startups can receive an 80% reduction in patent filing fees and a 50% reduction in trademark fees through the official Startup India.

- Reduced advance tax burden: Where the Section 80-IAC deduction reduces taxable income to nil, advance tax liability may effectively disappear during the exemption years.

One important consideration often overlooked by founders is the interaction between Section 80-IAC and concessional corporate tax regimes. A startup generally has to choose between claiming the 80-IAC exemption or opting for lower corporate tax rates under Sections 115BAA (22%) and 115BAB (15% for eligible manufacturing companies). These benefits cannot be used together, and the choice is typically irreversible. As discussed in this guide, many fast-growing startups find that three years of complete exemption deliver greater value than a permanent reduction to 22%, though the answer ultimately depends on future profitability projections.

The 3-Year 100% Tax Holiday Explained

The deduction applies only to profits and gains generated from the startup’s eligible business activities. Understanding what falls inside and outside that definition is crucial.

Covered under the exemption:

- Profits earned from qualifying business operations.

Not covered under the exemption:

- Interest income

- Capital gains

- Dividend income

- Other non-business income streams

These categories continue to be taxed under normal provisions.

Another point that catches many founders off guard is timing. The ten-year eligibility clock starts from the date of incorporation, not from the date of DPIIT recognition or IMB approval. Within that ten-year period, startups may choose any three consecutive assessment years for the deduction. There is no requirement to begin claiming immediately after incorporation.

In practice, this flexibility can be extremely valuable. A startup may choose to claim the benefit in Years 5-7 rather than Years 1-3 if profitability is expected to be substantially higher later in its growth cycle.

There is, however, one technical limitation for private limited companies. Minimum Alternate Tax (MAT) under Section 115JB continues to apply at 15% of book profits, even during the 80-IAC holiday period. While this means companies do not achieve a completely tax-free position in the strictest sense, the MAT paid creates a credit that can be carried forward and adjusted against future tax liabilities for up to fifteen assessment years.

LLPs operate differently. Since they are not subject to MAT, eligible LLPs can achieve a genuine zero-tax position on qualifying business profits during the exemption period. For some founders, this creates an interesting trade-off between the tax efficiency of an LLP and the fundraising advantages typically associated with a private limited company.

Understanding the Extension to March 2030

Until recently, startups had to be incorporated before 1 April 2025 to qualify for Section 80-IAC. The Finance Act, 2025 extended that deadline by five years, moving it to 1 April 2030. According to reporting by PIB, this expansion substantially increases the number of founders who can potentially benefit from the scheme.

To put that into perspective, a startup incorporated during FY 2027-28 can still access the exemption and retain the flexibility to choose its three-year deduction window at any point within its first decade of operations.

The extension arrives alongside broader changes introduced under the revised DPIIT startup framework in 2026. Among the most notable developments is the creation of a dedicated deep-tech startup category covering sectors such as artificial intelligence, machine learning, quantum computing, biotechnology, advanced materials, and space technology. These businesses face a higher evidentiary burden when demonstrating innovation, but they may also benefit from faster processing and increased policy attention. Additional details are available here.

Eligibility Criteria for Startup Tax Exemption (2026–2030)

The eligibility requirements for Section 80-IAC are not optional checkboxes where meeting most conditions is enough. Every criterion must be satisfied. Missing even one requirement can result in rejection at the IMB stage, regardless of how promising the business may be. The official conditions are published by the Income Tax Department and are also outlined on the Startup India portal.

Entity Types Qualified for Exemption (Private Limited & LLPs)

Section 80-IAC is available only to specific business structures.

| Entity Type | 80-IAC Eligible? | Notes |

| Private Limited Company | Yes | Subject to MAT under Section 115JB |

| Limited Liability Partnership (LLP) | Yes | No MAT liability |

| Registered Partnership Firm | No | May obtain DPIIT recognition but not 80-IAC |

| One Person Company (OPC) | No | Not covered under the provision |

| Sole Proprietorship | No | Not covered under the provision |

| Public Limited Company | No | Not covered under the provision |

This restriction is strict and leaves little room for interpretation. Founders operating through a sole proprietorship, partnership firm, or public company cannot access the exemption, even if the business itself is highly innovative.

An area that occasionally creates confusion involves businesses that began as an OPC and later converted into a private limited company. In many cases, the original incorporation date remains relevant for determining eligibility. Since this can affect the ten-year claim window, founders should seek professional advice before assuming the conversion resets the clock, particularly in light of the legislative restructuring introduced under the Income Tax Act, 2025.

Age of the Business and Incorporation Deadlines

To qualify, a startup must satisfy two separate age-related conditions at the same time.

First, the entity must have been incorporated on or after 1 April 2016 and before 1 April 2030.

Second, the startup must still be within its first ten years of existence when claiming the deduction.

These timelines work together rather than independently.

For example, a startup incorporated on 1 March 2020 would need to complete its chosen three-year exemption period before reaching the ten-year limit. Likewise, a startup incorporated close to the final deadline in December 2029 would still receive a full ten-year window from its incorporation date, but no extension beyond that period is available under the law.

In simple terms, incorporation before 2030 opens the door. Remaining within the first ten years determines whether the benefit can actually be claimed.

Annual Turnover Limits and Financial Thresholds

Another key condition relates to turnover.

A startup’s annual turnover must not exceed ₹100 crore in any financial year for which it intends to claim the deduction. The threshold applies to the overall business and is not limited to revenue generated from a particular product, service, or division.

Two practical points are worth keeping in mind:

- The ₹100 crore threshold is evaluated year by year.

- Turnover refers to business revenue and generally excludes non-business income such as interest earnings or capital gains.

Many founders mistakenly assume that crossing ₹100 crore once permanently eliminates eligibility. In reality, the assessment is tied to the relevant year. However, exceeding the threshold during a claim year can create problems for that year’s deduction, making careful financial planning important as the business scales.

Notably, this same ₹100 crore benchmark is also used within the broader Startup India framework, helping maintain consistency across startup-related benefits and compliance requirements. Further details are available here.

Definition of an “Eligible Business” (Innovation and Scalability)

This is often the most heavily scrutinised part of the entire application.

The law requires that the startup be engaged in either:

- Innovation, development, or improvement of products, services, or processes; or

- Building a scalable business model capable of generating significant employment or wealth creation.

On paper, the wording appears broad. In practice, the IMB typically applies a much stricter standard than many founders expect.

Simply operating a digital business or offering a modern service is rarely enough. The application must demonstrate a meaningful degree of innovation, differentiation, or scalability. The strongest submissions clearly explain what makes the startup different, why the solution is difficult to replicate, and how it creates measurable value beyond existing alternatives.

Operational guidance regarding IMB expectations is available here.

The revised 2026 DPIIT framework also introduced a dedicated deep-tech category covering sectors such as artificial intelligence, machine learning, quantum computing, biotechnology, advanced materials, and space technology. These startups often face greater documentation requirements but may benefit from specialised evaluation pathways. Additional discussion can be found here.

Excluded Business Structures and Reconstructions

The government designed Section 80-IAC to support genuinely new ventures, not businesses that simply repackage existing operations under a fresh legal entity.

As a result, the exemption is generally unavailable to startups formed through:

- Splitting up an existing business.

- Reconstructing an existing business under a new entity.

- Transferring previously used plant and machinery into the startup as its primary asset base.

A common example would be shutting down an existing company and reopening substantially the same operation under a new startup registration. Such arrangements are unlikely to qualify.

There is, however, a limited exception. Businesses that are re-established following extraordinary events such as floods, earthquakes, riots, accidental fires, civil disturbances, or war may still qualify under the relief provisions of Section 33B. In these situations, detailed evidence linking the business interruption to the relevant event is typically required.

Because reconstruction-related issues are among the easiest grounds for rejection, founders should evaluate their corporate history carefully before investing significant time in the application process.

The Mandatory DPIIT Recognition Process

DPIIT recognition is the foundation of the entire Section 80-IAC journey. Without it, a startup cannot move forward with an application for the income tax exemption. That said, receiving DPIIT recognition does not automatically grant the tax holiday. Many founders assume the two are the same thing, but they are separate stages.

Think of DPIIT recognition as the first checkpoint. The actual tax exemption comes only after obtaining approval from the Inter-Ministerial Board (IMB). The recognition process, eligibility criteria, and application portal are available at the Startup India portal..

Registering on the Startup India Portal

The application for DPIIT recognition is completed online through https://startupindia.gov.in. Founders can also access the process through the National Single Window System which integrates several business registration services into a single platform.

The application generally requires the following:

- Registration using the startup’s PAN and registered mobile number.

- Basic incorporation details, including entity type, sector, and date of incorporation.

- A description of the startup’s business model and innovative aspects.

- Upload of the Certificate of Incorporation for private limited companies or the LLP Certificate for LLPs.

- A brief explanation of how the product, service, or process introduces innovation, improvement, or scalability.

Most complete applications are processed relatively quickly. In many cases, DPIIT recognition is granted within 7 to 15 working days, provided there are no missing documents or inconsistencies.

One encouraging aspect for founders is that there is no government fee for DPIIT recognition. The government has repeatedly clarified, including through the PIB notification, that no external agency, consultant, or franchise has been authorised to process applications on its behalf. Startups can submit applications directly without paying intermediaries.

Documents Required for DPIIT Approval

While the documentation burden at this stage is lighter than the later IMB application, certain records must still be prepared carefully.

| Document | Notes |

| Certificate of Incorporation / LLP Certificate | Issued through MCA records |

| PAN of the Entity | Must match incorporation details |

| Aadhaar-linked Mobile Number | Required for OTP verification |

| Innovation Write-up | Brief explanation of innovation or scalability |

| Board Resolution (for Companies) | Authorisation for the application |

| Website or App URL | Optional but helpful if available |

Among these documents, the innovation write-up often carries the most weight.

It does not need to read like a technical research paper. At the same time, it should go beyond generic marketing language. Reviewers want to understand what the startup is building, what problem it solves, and why the solution is meaningfully different from what already exists in the market.

Many successful applications keep this explanation concise but specific. A clear description of the innovation usually performs better than pages of broad claims about disruption or transformation.

Timeline and Tracking Your DPIIT Status

Once submitted, the application enters the DPIIT review process.

For complete and accurate applications, decisions are commonly issued within 7 to 15 working days. Where information is missing or clarification is required, DPIIT may raise queries that must typically be addressed within 30 days.

Founders can monitor progress directly through the Startup India dashboard by checking the recognition status section. Status updates generally move through stages such as submission, review, query resolution, and final approval.

After approval, the startup receives a DPIIT Certificate of Recognition containing a unique recognition number and approval date. This certificate becomes an important document for future benefits and should be retained carefully as part of the company’s compliance records.

Obtaining DPIIT recognition unlocks several advantages beyond tax-related incentives. Recognised startups may access patent and trademark fee rebates, self-certification benefits under selected labour laws, and participation opportunities through the Government e-Marketplace (GeM).

However, founders should remember one crucial point: DPIIT recognition alone does not activate the Section 80-IAC tax exemption. The next and most challenging stage is securing certification from the Inter-Ministerial Board (IMB), which ultimately determines whether the startup qualifies as an eligible business for the income tax holiday.

The Inter-Ministerial Board (IMB) Certification

The Inter-Ministerial Board (IMB) certification is where the Section 80-IAC process becomes significantly more demanding. While DPIIT recognition confirms that a business qualifies as a startup, IMB certification determines whether that startup is innovative enough to receive the income tax exemption.

In practical terms, this is the stage that separates startups that merely qualify as startups from those that qualify for the tax holiday.

The IMB operates under DPIIT and reviews applications to determine whether a business meets the definition of an “eligible business” under Section 80-IAC. Information about the board, its framework, and application process is available here. Following reforms introduced after the 80th IMB meeting in April 2025, complete applications are now expected to receive a decision within 120 days.

Why IMB Approval is the Most Critical Step

The numbers tell the story.

India has crossed 2,07,000 DPIIT-recognised startups, yet only around 3,700 have obtained IMB certification. That alone highlight how selective the process is. According to this analysis, roughly half of the startups that submitted IMB applications were approved, while the other half were rejected.

This means the biggest obstacle is not obtaining DPIIT recognition. It is preparing an application strong enough to convince the IMB that the startup delivers genuine innovation, scalability, and economic value.

Another factor that raises the stakes is the absence of a straightforward appeals process. If an application is rejected, there is no dedicated statutory appellate mechanism. Challenging the decision generally requires approaching the High Court through a writ petition, an option that is often impractical for early-stage founders due to cost and time considerations.

As a result, most startups are far better served by investing additional effort into preparing a strong application from the outset rather than treating the first submission as a trial run.

Preparing the Technology Innovation Dossier

The IMB application is submitted through Form 80-IAC on the Startup India portal.

At the heart of the application is what many practitioners refer to as the technology innovation dossier. This is not a single document but a collection of materials that together demonstrate innovation, commercial viability, and growth potential.

A typical dossier includes:

Business innovation write-up

This is the cornerstone of the application. It should clearly explain:

- The problem being solved.

- Why the problem matters.

- The technology, methodology, or process behind the solution.

- How the solution differs from existing alternatives.

- Why competitors cannot easily replicate the approach.

The strongest write-ups tend to be detailed, founder-driven, and technically specific. Generic statements about disruption or market opportunity rarely carry much weight on their own.

Product demonstration

The IMB generally expects evidence that the product actually exists.

For technology businesses, this may include:

- Product walkthrough videos.

- Prototype demonstrations.

- Live platform access.

- Functional software demonstrations.

Startups offering software products should be prepared to show a working solution rather than simply describing future plans.

Pitch deck

The pitch deck should provide a structured overview of the business, including:

- Problem and solution.

- Market opportunity.

- Revenue model.

- Competitive positioning.

- Team credentials.

- Financial projections.

- Growth strategy.

Unlike an investor deck designed primarily to raise capital, an IMB deck should place greater emphasis on innovation and scalability.

Video pitch

Most applicants are also required to submit a short video introducing the startup, its mission, and its technology. This is typically a concise presentation lasting two to three minutes and should follow the guidelines published by Startup India.

Market traction evidence

Innovation alone is rarely enough.

The IMB also wants evidence that the market is responding positively. Useful supporting materials may include:

- Customer testimonials.

- Contracts and purchase orders.

- User growth metrics.

- Reviews and ratings.

- Pilot programme results.

- Case studies.

Together, these documents help demonstrate that the innovation is creating real-world value rather than remaining a purely theoretical concept.

Parameters Checked by the Inter-Ministerial Board

Although the IMB does not publish a formal scoring matrix, its evaluation generally focuses on four key areas.

| Parameter | What the IMB Evaluates |

| Technological Innovation | Original technology, proprietary processes, patents, research efforts |

| Market Potential | Size of opportunity, demand validation, competitive advantage |

| Scalability | Ability to grow without proportional increases in cost |

| Employment & Wealth Creation | Job creation, revenue growth, funding raised, economic contribution |

These categories are interconnected.

A startup with strong technology but no market validation may struggle. Likewise, a business with strong sales but little evidence of innovation may face challenges. The strongest applications demonstrate a balanced case across all four areas.

The revised review framework introduced in 2025 specifically encouraged rejected applicants to strengthen evidence relating to innovation, scalability, market potential, and employment generation. That guidance offers one of the clearest indicators of what the board prioritises during evaluation.

Dealing with IMB Queries and Rejections

Receiving a query from the IMB should not automatically be viewed as a negative outcome.

In many cases, it simply means the reviewers need additional clarification before making a decision.

When a query arrives, startups should:

- Designate a single responsible person to monitor communications.

- Respond within the stated deadline, typically 15 to 30 working days.

- Provide updated supporting evidence where available.

- Address every point raised in the query directly and clearly.

One common mistake is resubmitting the original materials without adding new information. Reviewers usually expect additional proof, clarification, or updated documentation.

For example, if the startup has filed a patent application, secured a major client, received a technology certification, or achieved significant growth after the original submission, those developments should be included in the response.

If the application is ultimately rejected, a startup may submit a stronger application in the future. There is no formal cooling-off period. However, founders should avoid treating reapplication as a simple administrative exercise.

A rejection often signals that the underlying innovation case was not sufficiently convincing. Revisiting the business narrative, strengthening evidence, and addressing weaknesses identified during review can dramatically improve the quality of a future submission. As noted in this guide, startups that substantially improve their innovation documentation and supporting evidence often have a far better chance of success on a subsequent application.

Complete Document Checklist for 80-IAC Exemption

By the time a startup reaches the Form 80-IAC stage, the focus shifts from eligibility to evidence. The IMB does not approve applications based on claims alone. Every statement about innovation, growth, turnover, ownership, or financial performance must be backed by supporting documentation.

The official upload requirements and declaration format are available here. The checklist below also draws from the this guide by Clear Tax and by Arthsetu.

A well-organised documentation package can significantly reduce queries, shorten review timelines, and improve the overall strength of the application.

Mandatory Corporate and Financial Documents

The IMB expects a complete set of corporate, ownership, and financial records that establish the startup’s legal identity and operating history.

| Document | Format | Remarks |

| Certificate of Incorporation / LLP Certificate | Issued through MCA | |

| Memorandum of Association (MoA) / LLP Agreement | Latest version | |

| Articles of Association (AoA) | Applicable to companies only | |

| Board Resolution for 80-IAC Application | PDF on company letterhead | Signed by authorised directors |

| PAN of the Entity | Scanned Copy | Must match company records |

| Shareholding Pattern | PDF on company letterhead | Current ownership structure |

| Directorship Details in Other Organisations | PDF on company letterhead | Required for all directors or partners |

| Audited Financial Statements | For all financial years since incorporation or the latest three years | |

| Income Tax Returns with Acknowledgements | For all financial years since incorporation or the latest three years |

Many founders focus heavily on innovation documentation while overlooking basic corporate records. In practice, missing board resolutions, outdated shareholding patterns, or incomplete financial statements are among the most common reasons applications receive additional queries.

Before submission, every document should be reviewed for consistency. The shareholding structure, director information, PAN details, MCA filings, and financial records should all align.

Proof of Innovation and Intellectual Property (IPR)

This is often the most influential category within the application.

Innovation can be subjective. Intellectual property and technical documentation help make it measurable.

The IMB generally places considerable weight on evidence that independently validates the startup’s technology, research efforts, or unique processes.

Useful supporting materials include:

- Patent application acknowledgements.

- Patent publication records.

- Patent grant certificates.

- Trademark registration certificates.

- Copyright registrations.

- Accelerator or incubator participation certificates.

- Research collaboration agreements.

- Technology licensing arrangements.

- Documented R&D expenditure records.

- Academic or institutional partnerships.

For startups that have not yet filed patents or formal IP applications, alternative evidence can still be presented.

Examples include:

- Proprietary software architecture.

- Unique datasets developed internally.

- Documented research projects.

- Original source code repositories.

- Internal technical papers.

- Product development timelines.

The key objective is to demonstrate that the startup has created something genuinely distinctive rather than simply repackaging existing solutions.

The more specific and verifiable the evidence, the stronger the innovation case becomes.

Pitch Deck and Business Model Documentation

The pitch deck submitted to the IMB serves a different purpose from a fundraising deck prepared for investors.

Investors may focus heavily on growth potential and returns. The IMB wants to understand innovation, scalability, and economic impact.

A strong 80-IAC pitch deck should clearly address:

- The market problem being solved.

- The startup’s unique solution.

- The technology or methodology behind the solution.

- Market size and opportunity.

- Business model and revenue generation.

- Unit economics.

- Competitive differentiation.

- Founding team expertise.

- Financial projections.

- Current traction and validation.

Founders often make the mistake of keeping the discussion too high level. The IMB generally expects technical depth. If a startup claims to have proprietary technology, the deck should explain what makes that technology different and defensible.

Alongside the deck, startups are expected to provide evidence that the product is operational.

Acceptable supporting materials may include:

- Product walkthrough videos.

- Demo recordings.

- Prototype links.

- Platform access credentials.

- Screenshots of customer activity.

- User reviews and ratings.

- Case studies and testimonials.

For digital products, showing actual customer engagement is often far more persuasive than presenting future projections.

Certifications Required from Chartered Accountants

Financial certifications play an essential role in the application because they provide independent verification of key eligibility conditions.

The IMB expects several financial declarations to be supported by a practicing Chartered Accountant.

Common CA certifications include:

- Turnover Certificate confirming that annual turnover has not exceeded ₹100 crore in any relevant financial year.

- Non-Reconstruction Certificate confirming that the startup was not formed through the splitting or reconstruction of an existing business.

- CA-Certified Financial Statements bearing the auditor’s signature, stamp, and membership number.

- Net Worth Certificate, where specifically requested during the review process.

Accuracy matters.

Even minor discrepancies can create avoidable complications. Differences between turnover figures reported in financial statements, tax returns, and CA certificates frequently trigger IMB queries.

Common documentation issues include:

- Incorrect membership numbers.

- Missing signatures.

- Unsigned annexures.

- Mismatched turnover figures.

- Incomplete certification pages.

Because financial records form the backbone of eligibility verification, every certified document should be reviewed carefully before submission.

All certifications must be prepared by a practicing Chartered Accountant registered with ICAI, and the figures reported should match the startup’s filed tax returns and audited accounts. Additional guidance on certification practices is available here.

A useful rule of thumb is this: if the innovation dossier is the heart of the application, the financial documentation is its foundation. Strong innovation evidence may attract attention, but incomplete or inconsistent financial records can still derail an otherwise compelling application.

Step-by-Step Guide to Filing the 80-IAC Application

Once a startup has secured DPIIT recognition and assembled its documentation, the next step is filing the Section 80-IAC application itself. At this stage, attention to detail matters. Even strong startups can face delays when forms are incomplete, documents are inconsistent, or supporting materials are uploaded incorrectly.

The application is submitted through the Startup India portal and reviewed by the Inter-Ministerial Board. While the process is fully digital, it requires careful preparation rather than simply filling in a few fields and clicking submit.

Navigating the Tax Exemption Section on Startup India

After obtaining DPIIT recognition, log in to https://startupindia.gov.in using the credentials linked to the startup’s account.

From the dashboard, navigate to the Tax Exemptions section. Here, startups will generally see two options:

- Section 80-IAC (Income Tax Exemption)

- Section 56(2) exemption (Angel Tax related provisions, although angel tax has since been abolished, some references may still appear within the portal interface)

Select Section 80-IAC and proceed to the application form.

Before starting, it is worth gathering all required documents into a single folder. Many applicants lose time moving back and forth between the portal and their internal records while trying to locate certificates, financial statements, or supporting documents.

A little preparation upfront can make the submission process much smoother.

Filling the Online Form Accurately

Form 80-IAC is divided into several sections that collectively build the startup’s eligibility profile.

The primary sections include:

1. Entity Details

Basic information is typically auto-populated from the DPIIT recognition database.

Applicants should still review every field carefully. Small errors in addresses, incorporation dates, or entity names can create unnecessary complications later.

2. Incorporation Information

This section captures:

- Date of incorporation

- Registered office address

- State of registration

- Entity structure (Private Limited Company or LLP)

The information should match MCA records exactly.

3. Financial Information

Applicants must provide annual turnover figures for each financial year since incorporation.

Consistency is critical. Figures entered in the form should align with:

- Audited financial statements

- Income tax returns

- CA certificates

Any mismatch may trigger queries during review.

4. Shareholding Structure

This section requires details relating to ownership and control.

Information generally includes:

- Names of shareholders or partners

- PAN details

- Percentage holdings

- Director or partner information

The data should reflect the latest cap table and corporate records.

5. Business Description

This is arguably the most important narrative section of the entire application.

Rather than using broad marketing language, founders should explain:

- The problem being addressed.

- The innovation behind the solution.

- The underlying technology or methodology.

- How the startup differs from existing alternatives.

- Why the business has meaningful growth potential.

Reviewers are looking for substance, not slogans.

A clear technical explanation will almost always outperform generic claims about disruption or market leadership.

6. Declaration and Verification

The final section requires confirmation that:

- The information submitted is accurate.

- The startup has not been formed through reconstruction or splitting of an existing business.

- The turnover threshold has not been breached.

- Supporting documents are genuine and complete.

The declaration carries legal significance, so applicants should review it carefully before submission.

The complete form structure and declaration language can be viewed here.

Uploading PDF Attachments and Dossiers

Supporting documents form the backbone of the application.

Every claim made in the form should be supported by evidence uploaded through the portal.

Some practical considerations include:

- Financial statements should be audited and CA-certified before upload.

- Corporate documents should be current and legible.

- Product demonstrations should be accessible and easy to review.

- File names should follow any naming conventions specified by the portal.

For product demonstrations, startups commonly submit:

- Recorded product walkthroughs

- Loom videos

- Hosted demos

- YouTube links

- Prototype access links

The goal is simple: make it easy for reviewers to understand the product without requiring additional explanations.

Language can also become an issue for some applicants. Documents prepared in regional languages should generally be accompanied by certified English translations to avoid delays during evaluation.

When uploading a pitch deck, a PDF version is usually preferable. Unlike editable cloud-based presentations, PDFs remain accessible throughout the review period and reduce the risk of broken links or permission issues.

Post-Submission Review Process

After submission, the application moves into the IMB review queue.

The startup can monitor progress directly through the Startup India dashboard, where application statuses typically progress through stages such as:

- Submitted

- Under Review

- Query Raised

- Decision Communicated

Under the revised framework introduced after the 80th IMB meeting in April 2025, DPIIT committed to processing complete applications within approximately 120 days.

That timeline applies to complete submissions. Applications requiring clarification, additional evidence, or corrected documents may take longer.

If the IMB raises a query, the startup will usually receive an email notification along with an update on the portal. Responses must be submitted through the same system within the prescribed timeframe.

Founders should treat queries seriously. A detailed and well-supported response often determines whether the application moves toward approval or rejection.

When the application is approved, the startup receives a Certificate of Eligible Business, commonly referred to as the IMB Certificate. This document can be downloaded from the portal and serves as the formal basis for claiming the Section 80-IAC deduction in the Income Tax Return.

Without this certificate, the tax holiday cannot be claimed, regardless of DPIIT recognition status.

Additional process details and guidance are available here.

Strategic Timing: When Should You Claim the 3-Year Exemption?

One of the most valuable features of Section 80-IAC is also one of the most misunderstood.

Many founders assume the tax holiday must be claimed immediately after incorporation or as soon as the startup becomes eligible. In reality, the law provides far more flexibility. Choosing the right three-year period can dramatically increase the value of the exemption, sometimes by tens of lakhs of rupees.

The difference between claiming too early and claiming at the right time can have a meaningful impact on cash flow, growth capital, and long-term financial planning.

Understanding the “Any 3 Consecutive Years” Rule

Section 80-IAC allows eligible startups to claim a 100% deduction on qualifying business profits for any three consecutive assessment years within the first ten years from incorporation.

That phrase, “any three consecutive years,” is where the planning opportunity lies.

The exemption is not restricted to:

- The first three years after incorporation.

- The first three profitable years.

- The period immediately following DPIIT recognition.

- The years immediately after IMB approval.

Instead, startups can choose the three-year block that delivers the greatest tax advantage.

Consider two simplified scenarios:

Scenario A

A startup earns:

- ₹10 lakh profit in Year 2

- ₹15 lakh profit in Year 3

- ₹20 lakh profit in Year 4

Claiming the exemption during this period produces some tax savings, but the overall benefit remains modest.

Scenario B

The same startup scales successfully and earns:

- ₹75 lakh profit in Year 5

- ₹1.2 crore profit in Year 6

- ₹2 crore profit in Year 7

Using the exemption during Years 5-7 would generate substantially larger savings because the deduction applies to a much larger profit base.

The principle is simple: the value of the exemption rises as profits rise.

This flexibility is one of the reasons Section 80-IAC is often viewed as a strategic tax-planning tool rather than merely a compliance benefit. Additional discussion on this planning approach can be found here.

Aligning Exemption with Peak Profitability Cycles

Choosing the ideal claim window requires an honest assessment of the startup’s growth trajectory.

A useful framework is outlined below:

| Scenario | Recommended Approach |

| Startup is pre-revenue or loss-making | Wait. There is no value in using the exemption when taxable profits do not exist. |

| Startup has just become modestly profitable | Consider securing IMB approval but delaying the claim period. |

| Startup is growing rapidly with increasing margins | Activating the exemption may help capture the highest-profit years. |

| Startup expects a one-time profit spike | Ensure the high-profit year falls within the chosen three-year block. |

| Startup is approaching Years 8-10 | Consider claiming sooner rather than risking expiry of the eligibility window. |

The key is balancing patience with practicality.

Waiting too long can be risky if profitability arrives later than expected. Claiming too early can leave substantial tax savings on the table.

Many experienced advisors encourage founders to model multiple scenarios before making a decision. A simple financial forecast showing expected profits over the next five years can often reveal the most advantageous exemption window.

Cash Flow Management During the First 10 Years

The tax holiday can improve cash flow significantly, but founders should still understand how the broader tax framework affects their business structure.

For private limited companies, Minimum Alternate Tax (MAT) remains relevant.

Even during the Section 80-IAC exemption period, companies may still be required to pay MAT at 15% of book profits under Section 115JB. While this reduces the immediate cash-flow benefit, the amount paid is not necessarily lost. MAT generates a credit that can be carried forward for up to fifteen assessment years and used against future tax liabilities.

In practical terms, MAT functions more like a deferred tax benefit than a permanent cost.

LLPs operate differently.

Since LLPs are not subject to MAT, eligible LLPs can enjoy a cleaner tax outcome during the exemption period, with qualifying business profits effectively escaping income tax altogether.

This does not automatically make an LLP the superior structure. Private limited companies continue to offer advantages in areas such as venture capital fundraising, ESOP implementation, and institutional investment. However, founders weighing entity structure choices should include MAT implications in their financial analysis rather than focusing solely on incorporation costs or compliance obligations.

Further discussion on the interaction between MAT and the Section 80-IAC exemption is available here.

Ultimately, the most successful startups tend to approach the 80-IAC benefit proactively. They secure DPIIT recognition early, prepare for IMB approval well before profitability peaks, and align their exemption window with the period when the tax savings will have the greatest impact on growth.

Common Reasons for 80-IAC Application Rejection

Even startups with strong products, paying customers, and valid DPIIT recognition can find themselves facing rejection at the IMB stage. That reality often surprises founders.

The reason is simple: DPIIT recognition and IMB approval evaluate different things. DPIIT primarily confirms that a business qualifies as a startup. The IMB, on the other hand, examines whether the startup meets the much narrower standard required for the Section 80-IAC tax exemption.

Understanding why applications fail can be just as valuable as understanding why they succeed.

Insufficient Proof of True Innovation

The most common reason for rejection is a failure to demonstrate genuine innovation.

This does not necessarily mean the startup lacks value. In many cases, the business may have strong commercial potential but fails to provide convincing evidence that its product, process, or technology is meaningfully differentiated from existing alternatives.

Some recurring patterns appear across rejected applications:

- A SaaS platform built using widely available tools without any proprietary technology, algorithm, or technical advantage.

- A consulting or service-based business describing itself as innovative without demonstrating a unique process, platform, or methodology.

- Applications that explain the market problem clearly but provide little detail about how the solution actually works.

- Pitch decks focused almost entirely on growth, funding, or marketing while offering limited discussion of technology or innovation.

- Broad claims such as “industry first” or “revolutionary” without supporting evidence.

One challenge for founders is that innovation is not assessed through a strict numerical formula. The IMB evaluates applications qualitatively, which means the quality of explanation often matters as much as the innovation itself.

A startup may have developed something genuinely valuable, but if reviewers cannot clearly understand what makes it unique, the application may struggle.

According to this analysis, a significant proportion of historical rejections were linked to concerns around innovation, differentiation, or insufficient supporting evidence. Although transparency has improved in recent years, the standard remains demanding.

The strongest applications typically answer one fundamental question: Why could this not be easily replicated by an ordinary competitor?

Errors in CA Certification and Financials

Not every rejection stems from innovation concerns.

A surprising number of applications encounter problems because of financial inconsistencies, documentation errors, or certification issues.

Common examples include:

- Turnover figures in CA certificates that do not match filed tax returns.

- Audited financial statements missing signatures, stamps, or membership details.

- Missing financial years in the document set.

- Outdated shareholding information.

- Inconsistencies between MCA filings and submitted ownership records.

- Incorrect PAN details or corporate information.

From the IMB’s perspective, these issues raise concerns about accuracy and reliability.

Even when the underlying business is eligible, discrepancies create additional scrutiny and often trigger clarification requests. If those inconsistencies remain unresolved, rejection becomes far more likely.

Many founders invest weeks refining their innovation narrative but spend very little time reviewing financial documentation. In practice, both areas deserve equal attention.

Before submission, it is worth conducting a thorough reconciliation exercise to ensure:

- Financial statements match tax filings.

- Turnover figures remain consistent across all documents.

- Shareholding information aligns with MCA records.

- Every certification contains the required signatures, stamps, and supporting schedules.

Small administrative errors can create disproportionately large problems.

Split-Up or Reconstruction Violations

Another recurring reason for rejection relates to the reconstruction restrictions built into Section 80-IAC.

The objective of the provision is to encourage genuinely new businesses. It is not intended to provide tax holidays for existing businesses operating under a different legal structure.

As a result, the IMB pays close attention to situations where a startup appears to be a continuation of an older enterprise.

Potential red flags include:

- The same promoters previously operated an almost identical business.

- The customer base is substantially the same as that of an earlier company.

- The previous business closed shortly before the new startup was incorporated.

- The startup uses the same assets, technology, employees, or infrastructure as an earlier entity.

- Business objects and operational activities are nearly identical to those of a predecessor organisation.

None of these factors automatically guarantee rejection. However, they can lead reviewers to question whether the startup is truly a new venture or simply a restructured version of an existing business.

This issue becomes particularly relevant for founders who have reorganised operations following fundraising, ownership changes, or business restructuring exercises.

Where any ambiguity exists, obtaining a formal legal opinion before filing can be a prudent step. Guidance on reconstruction-related issues can be found here.

A Common Theme Across Rejections

Looking across most rejected applications, a consistent pattern emerges.

The IMB is rarely looking for perfection. What it wants is evidence.

Evidence that the startup is genuinely innovative.

Evidence that the business is new rather than reconstructed.

Evidence that the financial information is accurate.

Evidence that the product has real-world relevance and growth potential.

Founders who approach the application as a documentation exercise often struggle. Those who treat it as a process of building a compelling, evidence-backed case generally stand a much stronger chance of success.

In many ways, the application resembles an investor due-diligence process. The difference is that instead of convincing investors to deploy capital, the startup is convincing the government that it deserves access to one of the most valuable tax incentives available under the Startup India framework.

Navigating Angel Tax Relief and Section 54EE Together with 80-IAC

For many startups, Section 80-IAC is only one piece of a much larger tax and fundraising puzzle. Founders raising external capital often need to understand how various tax provisions interact with one another, particularly when equity investments, capital gains exemptions, and startup incentives come into play.

The good news is that several reforms introduced in recent years have simplified parts of this landscape. However, understanding the broader framework remains important, especially for startups preparing for fundraising rounds while also planning to claim the Section 80-IAC exemption.

Recent Reforms in Angel Tax for DPIIT-Recognised Startups

For years, angel tax was one of the most controversial issues facing Indian startups.

Under Section 56(2)(viib), companies could be taxed on the premium received when issuing shares above their fair market value. The provision was originally intended to prevent abuse, but in practice it often created uncertainty for startups raising capital based on future growth potential rather than current revenues.

This was particularly challenging for early-stage ventures. A startup with limited revenue but strong investor confidence could receive funding at a valuation that tax authorities later questioned.

That concern has now largely been removed.

The Finance Act, 2024 abolished Section 56(2)(viib) with effect from 1 April 2025, eliminating angel tax for all companies rather than restricting relief only to DPIIT-recognised startups.

For founders raising capital today, this represents a significant simplification. New funding rounds no longer face the same valuation-related tax uncertainty that previously complicated startup fundraising.

That said, startups involved in funding rounds completed before 1 April 2025 may still need to address historical angel tax notices or assessments. In such situations, businesses that held valid DPIIT recognition at the time of fundraising should ensure that recognition forms part of their response strategy.

Additional discussion on these reforms can be found here.

Co-Structuring Foreign Investment and Tax Holidays

As startups grow, tax planning increasingly overlaps with fundraising strategy.

Several provisions operate alongside Section 80-IAC and can influence both investor behaviour and company structuring decisions.

Section 54EE

Section 54EE provides capital gains relief to individual taxpayers and Hindu Undivided Families (HUFs) who reinvest long-term capital gains into government-notified startup-focused funds.

Key features include:

- Maximum eligible investment of ₹50 lakh.

- Three-year lock-in period.

- Benefit available to the investor rather than the startup itself.

While the startup does not directly receive a tax exemption through Section 54EE, the provision can make startup-focused investment vehicles more attractive to investors.

Section 54GB

Section 54GB is often more directly relevant to startup fundraising.

It allows individuals and HUFs to claim exemption from long-term capital gains tax when proceeds from the sale of long-term assets, including residential property, are invested into eligible startups.

To qualify:

- The investor must acquire at least 50% equity in the startup.

- Shares must generally be held for a minimum of five years.

- The startup must deploy the funds toward qualifying assets that are also retained for the prescribed period.

Although the conditions are detailed, the provision can encourage investors to allocate capital toward startup ventures while obtaining tax relief on gains from other assets.

Section 79: Carry-Forward of Losses

Rapidly growing startups often experience multiple funding rounds, each of which may dilute founder ownership.

Ordinarily, substantial changes in shareholding can affect the ability to carry forward business losses.

However, DPIIT-recognised startups receive more favourable treatment under Section 79, allowing eligible losses from earlier years to remain available despite ownership changes, subject to prescribed conditions.

This protection can be particularly valuable during seed, Series A, and later-stage fundraising rounds where cap tables evolve significantly.

FEMA and Foreign Investment Considerations

Most foreign direct investment into Indian startups continues to fall under the automatic route, making capital inflows relatively straightforward in many sectors.

However, founders should remain mindful of broader compliance considerations when structuring foreign investments.

Areas that often require careful review include:

- Convertible instruments.

- Foreign portfolio investments.

- Shareholding structures.

- Sector-specific investment restrictions.

- Entity type selection.

While these issues do not automatically affect Section 80-IAC eligibility, poorly structured transactions can create complications later when claiming tax benefits or demonstrating compliance.

For startups actively raising international capital, tax and regulatory planning should ideally occur together rather than as separate exercises.

Additional insights on startup tax planning and fundraising structures are available here.

Looking at the Bigger Picture

Founders sometimes view Section 80-IAC in isolation, focusing only on the immediate tax savings.

In reality, the most effective planning often comes from understanding how multiple provisions work together.

The abolition of angel tax has reduced friction in fundraising. Sections 54EE and 54GB can encourage investor participation. Section 79 helps preserve valuable tax losses through ownership changes. Meanwhile, Section 80-IAC remains one of the most powerful direct tax incentives available to eligible startups.

When these provisions are considered collectively rather than individually, founders are often better positioned to balance fundraising objectives, tax efficiency, and long-term growth planning.

Compliance and Reporting During the Tax Holiday Period

Receiving the IMB certificate and successfully claiming the Section 80-IAC deduction is a major milestone, but it is not the finish line.

A common misconception among founders is that once the exemption is approved, the compliance burden largely disappears. In reality, the tax holiday comes with ongoing responsibilities. Startups must continue maintaining accurate records, filing returns correctly, and ensuring that all financial reporting remains consistent throughout the exemption period.

The tax benefit may reduce the income tax payable, but it does not reduce the need for compliance.

Maintaining Accurate Books and Audits

Every startup claiming the Section 80-IAC deduction must maintain proper books of account and comply with applicable audit requirements under the Income Tax Act.

This becomes especially important during the exemption years because the deduction is directly linked to the startup’s reported profits.

A robust accounting system serves several purposes:

- It establishes the profit figure on which the deduction is calculated.

- It helps distinguish eligible business income from taxable non-business income.

- It supports MAT calculations for private limited companies.

- It provides evidence in the event of future assessments or scrutiny.

From a practical perspective, founders should avoid treating accounting as a year-end exercise. Businesses that maintain organised records throughout the year generally experience fewer compliance issues and spend less time responding to queries from auditors or tax authorities.

Consistency is critical.

Revenue, expenses, and profit figures should align across:

- Audited financial statements.

- Income tax returns.

- GST filings.

- Internal accounting records.

Even small discrepancies can raise questions during assessments.

Guidance on compliance and labour-law self-certification for DPIIT-recognised startups is available through the Sharm Suvidha portal.

Aligning Books, GST Returns, and ITR Before Filing

Before filing the Income Tax Return for any year in which the Section 80-IAC deduction is claimed, startups should perform a comprehensive reconciliation exercise.

Many scrutiny notices originate not from fraud or major errors, but from simple inconsistencies between different government filings.

A practical review generally covers three areas:

1. GST vs. Books

Revenue reported in GST returns should reconcile with turnover reported in the audited Profit and Loss Account.

Differences can occur for legitimate reasons, including:

- Export revenue.

- Exempt supplies.

- Timing adjustments.

- Credit notes and reversals.

However, these differences should be documented clearly and supported by working papers.

2. Books vs. Income Tax Return

The taxable income calculation should flow logically from the audited financial statements.

Typically, the process involves:

- Starting with accounting profit.

- Adjusting for tax-related additions and disallowances.

- Calculating taxable income.

- Applying the Section 80-IAC deduction where eligible.

A clear computation sheet helps demonstrate how the final tax position was reached.

3. TDS Credits vs. Form 26AS / AIS

Any tax deducted at source on business receipts should appear correctly in the startup’s tax records.

Founders should verify that:

- TDS credits claimed in the return match Form 26AS.

- AIS records are consistent with reported income.

- No deductions have been omitted or duplicated.

System-generated notices are frequently triggered by mismatches in this area, even when the underlying tax position is otherwise correct.

For eligible entities, returns are generally filed using:

- ITR-6 for companies.

- ITR-5 for LLPs.

The IMB certificate details, including certificate number and approval date, should be reported in the relevant deduction schedules.

One point cannot be overstated: the deduction is available only if the return is filed within the due date prescribed under Section 139(1). Missing the filing deadline can jeopardise the benefit for that assessment year.

Further information is available at the official portal of the Income Tax Department.

Triggers for Income Tax Scrutiny in Startups

Claiming the tax holiday does not automatically place a startup under scrutiny. However, certain patterns are more likely to attract attention from tax authorities.

Common scrutiny triggers include:

Large deductions relative to turnover

A startup claiming a substantial deduction compared with its turnover profile may attract limited verification. This does not imply wrongdoing, but authorities may seek confirmation that the claim has been calculated correctly.

Significant cash transactions

Large cash receipts or payments can generate alerts within reporting systems and may result in requests for additional explanation.

GST and Income Tax mismatches

One of the most common triggers remains inconsistencies between turnover reported under GST and turnover reported in the Income Tax Return.

Even legitimate differences should be fully documented.

Historical share premium transactions

Although angel tax has been abolished for recent years, share issuances completed under earlier rules may still be examined during assessments.

Related-party transactions

Transactions involving promoters, group companies, family-owned entities, or connected parties often receive additional attention, particularly where pricing appears inconsistent with market conditions.

The existence of a scrutiny notice should not automatically be viewed as a problem. Many notices simply request clarification or supporting documents.

What matters is the startup’s ability to produce a clear compliance trail.

For DPIIT-recognised startups, support mechanisms remain available through Startup India initiatives and the broader e-assessment framework administered by the CBDT. Additional guidance can be found in this PIB release.

Building a Strong Compliance Trail

The startups that navigate assessments most smoothly tend to follow the same pattern: they maintain organised records from the beginning.

A strong compliance trail typically includes:

- DPIIT Recognition Certificate.

- IMB Certificate.

- Audited financial statements.

- GST reconciliations.

- Filed Income Tax Returns.

- CA certifications.

- Supporting documentation for major transactions.

Think of these records as insurance for the future.

The Section 80-IAC tax holiday can create substantial savings, but those savings rest on the startup’s ability to demonstrate continued compliance year after year. Accurate books, timely filings, and consistent reporting do more than satisfy regulatory requirements. They help protect one of the most valuable tax benefits available to eligible Indian startups.

Quick Reference Summary

For founders looking for a fast overview, the table below captures the key Section 80-IAC rules and thresholds in effect as of June 2026.

| Parameter | Position as of June 2026 |

| Section governing exemption | Section 80-IAC of the Income Tax Act, 1961 (renumbered under the Income Tax Act, 2025 from AY 2027-28 onwards) |

| Eligible entities | Private Limited Companies and LLPs only |

| Incorporation window | 1 April 2016 to 31 March 2030 |

| Maximum age at claim | Must be within 10 years of incorporation |

| Turnover limit | ₹100 crore in any financial year |

| Deduction amount | 100% of eligible business profits |

| Exemption period | Any 3 consecutive assessment years within the first 10 years |

| First approval required | DPIIT Recognition via Startup India |

| Second approval required | IMB Certification through Form 80-IAC |

| IMB review timeline | Approximately 120 days for complete applications |

| Angel tax status | Abolished from 1 April 2025 |

| MAT applicability | Applicable to Private Limited Companies at 15% of book profits; not applicable to LLPs |

| Approved startups | Approximately 3,700 startups approved since inception (as of April 2026) |

| Official application portal | startupindia.gov.in/content/sih/en/form80iac.html |

FAQ: Section 80-IAC Income Tax Exemption For Startups

Section 80-IAC provides eligible Indian startups with a 100% income tax exemption on business profits for any three consecutive assessment years within their first ten years of incorporation. It allows founders to reinvest capital during critical scaling and growth stages.

Startups must be incorporated between April 1, 2016, and March 31, 2030. Additionally, the startup’s overall annual business turnover must not exceed ₹100 crore during any financial year in which the tax deduction is actively claimed.

No. DPIIT recognition is only the preliminary step. To successfully claim the income tax exemption, a startup must submit a detailed technology dossier and secure Inter-Ministerial Board (IMB) certification by proving genuine technological innovation, market potential, and high scalability

No. Startups formed by splitting up or reconstructing an existing business are strictly ineligible. The exemption is heavily scrutinized by the IMB and reserved solely for genuinely new ventures.

No. The 3-year tax holiday applies exclusively to profits generated from eligible business operations. It does not cover non-business income streams like interest income, capital gains, or dividend income, which remain fully taxable under standard provisions.

Yes, Private Limited Companies are still subject to 15% MAT on book profits during the holiday, though this generates a carry-forward tax credit. LLPs, however, have no MAT liability and can achieve a genuine zero-tax position.

Key Takeaways for Founders

If there is one theme that runs through the entire Section 80-IAC framework, it is preparation.

The tax holiday is one of the most valuable incentives available to Indian startups, but accessing it requires more than simply registering as a startup. Founders must successfully navigate two separate approval stages, demonstrate genuine innovation, maintain accurate financial records, and make thoughtful decisions about when to activate the exemption.

A few practical lessons stand out:

- DPIIT recognition is necessary, but it is only the first step.

- IMB approval is where most applications succeed or fail.

- Innovation must be demonstrated with evidence, not just described.

- Strong documentation often matters as much as the underlying business idea.

- Timing the three-year exemption window strategically can significantly increase the value of the benefit.

- Compliance remains important even after the exemption is granted.

For startups expecting substantial profitability within their first decade, the potential tax savings can be transformative. Properly used, the exemption can free up capital that would otherwise be paid as tax and redirect it toward hiring, product development, expansion, and growth.

The founders who benefit most are usually not the ones who apply the fastest. They are the ones who prepare thoroughly, build a strong innovation case, organise their documentation early, and align the exemption with the period when it will have the greatest financial impact.

Disclaimer:

This article is for informational purposes only and does not constitute legal or tax advice. Eligibility conditions, section numbering under the Income Tax Act 2025, and official processes may be updated after the publication date. Consult a qualified Chartered Accountant or tax advisor before filing any application or ITR claim under Section 80-IAC.

Leave a Reply