Crypto Tax India 2026: The Complete 30% VDA, 1% TDS & ITR Filing Guide

Navigating India’s Crypto Tax Landscape in 2026

If you’ve been around the Indian crypto space for a few years, you’ll remember how messy things used to feel. Half-rules, circulars, speculation, and the occasional panic every budget season. That phase is mostly over now.

India’s approach to crypto taxation has settled into something far more structured. Since the Finance Act 2022 introduced Sections 115BBH and 194S, the system hasn’t just existed; it’s been enforced, repeated, and baked into every tax filing cycle. By FY 2025–26, there’s very little ambiguity left on the basics: a flat 30% tax on gains from Virtual Digital Assets (VDAs), a 1% TDS on qualifying transactions, and mandatory disclosure through Schedule VDA in your Income Tax Return.

What’s interesting, sometimes frustrating, depending on who you ask, is how blunt the framework is. There’s no nuance around holding periods, no distinction between short-term and long-term gains and no comforting ability to offset a bad trade against a good one. Every gain stands alone, taxed cleanly at 30%, like the system refuses to acknowledge that portfolios are messy in real life.

And this applies across the board. It doesn’t matter if you’re someone holding Bitcoin long-term, dabbling in DeFi for yield, minting NFTs, or trading actively with dozens (or hundreds) of swaps a month. The law doesn’t really care about your “style.” It just sees transactions.

This guide tries to pull everything into one place, not just the rules, but how they actually play out when money is involved. Definitions, mechanics, filing steps, real examples, compliance risks, even the slightly murky territory around NRIs. The idea is simple: if you’re interacting with crypto in India in 2026, you shouldn’t be guessing.

If you want to understand how India even got here, the legal back-and-forth, the hesitation, the slow tightening, this guide is for you.

And if you’re more curious about where things might go next (because honestly, this still feels like a midpoint, not an endpoint), this is worth a read.

At a Glance: Indian Crypto Tax Rules for 2026

If you are short on time, here are the absolute essentials you need to know before filing your taxes this year:

- Flat 30% Tax on Gains: All profits from Virtual Digital Assets (VDAs) are subject to a strict 30% tax under Section 115BBH, plus a 4% health and education cess and applicable surcharges.

- 1% TDS on Crypto Transfers: Under Section 194S, a 1% Tax Deducted at Source (TDS) is levied on transactions to track trading activity. You can adjust this against your final tax liability or claim a refund when filing your ITR.

- No Loss Offsets Allowed: You cannot offset crypto losses against crypto gains or any other form of income. Furthermore, crypto losses cannot be carried forward to future financial years.

- No Expense Deductions: The only allowable deduction is the purchase price (cost of acquisition). Gas fees, exchange fees, and brokerage costs are completely ignored by the tax system.

- Crypto Swaps are Taxable Events: Exchanging one cryptocurrency for another (e.g., swapping ETH for SOL) is considered a transfer and triggers the 30% tax based on the INR value at the moment of the swap.

- Strict ITR Reporting Requirements: All crypto activity must be distinctly reported in Schedule VDA. If you hold crypto in offshore wallets or foreign exchanges, it must be declared in Schedule FA (Foreign Assets) to avoid severe penalties under the Black Money Act.

Understanding Virtual Digital Assets (VDAs) and the 2026 Legal Framework

What Qualifies as a VDA? (Bitcoin, NFTs, and Beyond)

At some point, the government had to answer a deceptively simple question: What exactly are we taxing?

Section 2(47A) of the Income Tax Act, added via the Finance Act 2022, is where they landed. And instead of drawing tight boundaries, they went wide.

A Virtual Digital Asset, as defined here, is basically any digitally generated token or code that represents value, can be transferred or traded, and exists electronically. That’s the clean version. The real implication is this: if something behaves like a crypto asset, there’s a good chance it falls into this net.

The definition is intentionally flexible and almost future-proof. Which sounds clever on paper, but in practice, it means the law is always a step ahead of whatever new token model shows up next.

So, what clearly falls under VDAs?

- Cryptocurrencies—everything from Bitcoin and Ethereum to the more obscure tokens you probably forgot you even hold

- NFTs, but only if they’ve been officially notified (that small detail matters more than people think)

- DeFi tokens, governance tokens, yield tokens, essentially anything tied to a protocol economy

- Stablecoins like USDT or USDC—yes, even though they feel “stable,” they’re still treated as crypto-issued value

On the flip side, there are a few clean exclusions. The Indian Rupee isn’t a VDA. Foreign currencies aren’t either. And interestingly, the Digital Rupee, the RBI’s own central bank digital currency, sits outside this framework because it’s legal tender, not a speculative asset.

There’s also a quiet but important clause tucked into Section 2(47A): the government can expand this definition whenever it wants, just by issuing a notification. There is no need for a new law. Which means the scope of what counts as a taxable digital asset isn’t fixed, but it can stretch, sometimes without much warning.

Stablecoins are a good example of that grey zone. They’re widely used, but their regulatory identity in India still feels unsettled.

The Core Tax Sections Every Investor Must Know

If Section 2(47A) tells you what a VDA is, the next few sections tell you what happens once you touch one—buy it, sell it, swap it, receive it.

There are three main pillars here. Everything else kind of branches out from them.

Section 2(47A) is the gatekeeper. If your asset doesn’t fall under this definition, the rest doesn’t apply. It’s simple, but foundational.

Section 115BBH is where the actual tax bite comes in. This is the section that imposes the 30% flat tax on gains from transferring VDAs. It also quietly shuts a lot of doors—no deductions beyond purchase cost, no setting off losses, and no carrying them forward. It’s a very “clean ledger only” kind of rule.

Section 194S works differently. It’s not about how much tax you owe, but it’s about tracking you in the system. The 1% TDS gets deducted during transactions themselves, creating a trail. Think of it less as tax and more as a breadcrumb system that the Income Tax Department can follow later.

Then there’s a fourth piece that tends to catch people off guard: Section 56(2)(x). This one pulls VDAs into the “income from other sources” category when they’re received as gifts or airdrops. Which means, depending on how you got your crypto, you might not even be in the 30% regime initially. You could be taxed at your slab rate instead.

It’s a bit of a layered system. Not complicated in isolation, but when these sections overlap, say airdrops that later get sold, it starts to feel like a relay race where the baton keeps changing hands.

Section 115BBH Simplified: The 30% Flat Tax on Crypto Gains

How the 30% Crypto Tax Works in Practice

On paper, Section 115BBH is almost aggressively simple. No layered rates, no holding period logic and no “if this then that.” Just one rule, applied bluntly: if you make money from transferring a VDA, 30% of that gain goes to tax.

It doesn’t matter if you held Bitcoin for three years like a patient investor or flipped it in three days because the chart looked promising. The system doesn’t reward patience here. It doesn’t penalize speed either. It just ignores both.

The calculation itself is straightforward enough that you could scribble it on the back of a receipt:

Taxable VDA Income = Sale Price – Purchase Price

That’s it. That’s the whole formula.

But, and this is where people usually pause, only the purchase price is allowed as a deduction. Nothing else gets to come along for the ride.

Exchange fees? Ignored.

Brokerage? Ignored.

Even if you’ve actively spent money just to execute the trade, the law treats those as irrelevant. It’s a bit like being taxed on your salary without accounting for your commute, your tools, or your time. Clean, yes. Fair? Depends who you ask.

Then there’s the add-ons. The base 30% isn’t the final number.

A 4% health and education cess sits on top. And if your total income crosses certain thresholds, a surcharge kicks in:

- 10% if your income crosses ₹50 lakh

- 15% beyond ₹1 crore

- 25% beyond ₹2 crore

- 37% beyond ₹5 crore

For most people, the effective rate lands somewhere around 31.2%. Not catastrophic, but not exactly gentle either. And if you’re in a higher income bracket, it creeps up further, quietly, but noticeably.

What’s missing is just as important as what’s there.

There’s no indexation benefit. Inflation doesn’t get factored in. Holding long-term doesn’t earn you a lower rate. There’s no grandfathering for early adopters who entered before the rules even existed. The system treats every gain as if it happened in a vacuum, disconnected from time or context.

The Strict Rule on Crypto Losses (No Set-Offs, No Carry Forwards)

This is the part that tends to sting a little. Or a lot, depending on how your year went.

Under the specific provisions of Section 115BBH(2)(b), losses from crypto aren’t just limited; they are effectively ignored. Three separate statutory restrictions come into play, and together they make the system unusually rigid by completely isolating Virtual Digital Assets from all other income heads.

First, you can’t offset losses within crypto itself.

So if you made ₹2,00,000 on Bitcoin but lost ₹1,50,000 on some altcoin experiment that didn’t go as planned, you might expect to be taxed on the net ₹50,000.

That’s not how this works.

You’ll be taxed on the full ₹2,00,000 gain. The ₹1,50,000 loss? It just sits there, doing nothing. No relief and no adjustment.

Second, you can’t use crypto losses to reduce any other income. Not your salary, not stock market gains, and not business income. It’s like the loss exists in a sealed compartment—visible, but unusable.

Third, you can’t carry those losses forward either. In most areas of taxation, there’s at least some memory; you can take a bad year and soften a future good one. Here, there’s no memory. Once March 31 passes, that loss effectively expires.

It’s a hard reset every year.

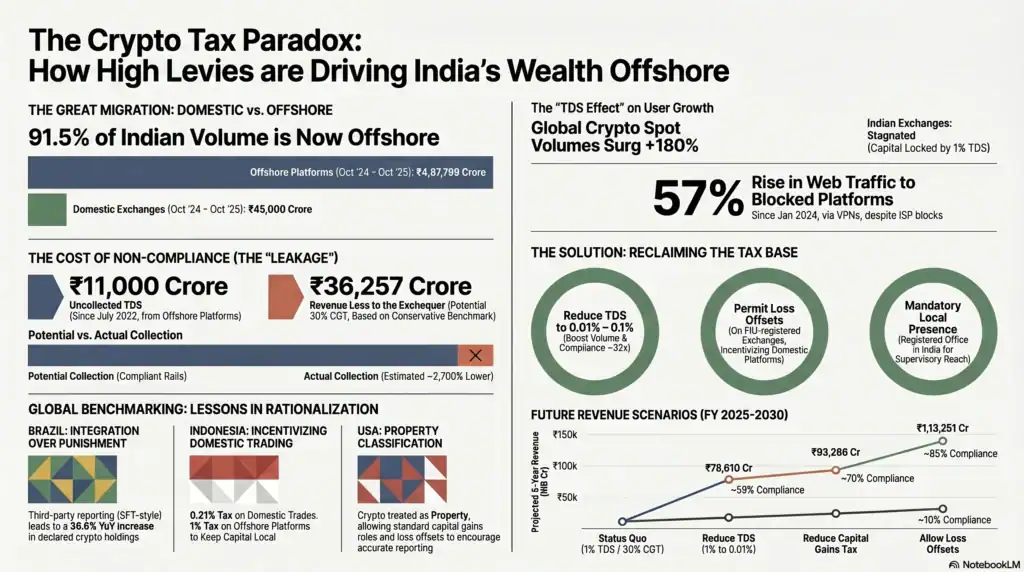

This design has been controversial, to put it mildly. Industry groups, like the Bharat Web3 Association, have been pushing for more flexibility, especially allowing intra-VDA set-offs and reducing the 1% TDS, arguing that the current structure has nudged serious traders toward offshore platforms where these frictions don’t exist.

Decoding the 1% TDS on Crypto Transactions (Section 194S)

Why the Government Deducts 1% TDS

When Section 194S came in, a lot of people misunderstood it as “another tax.”

Think of it more like a tracking mechanism that happens to involve money.

Before 2022, crypto transactions were, let’s be honest, fairly invisible unless you voluntarily reported them. There wasn’t a built-in way for the government to see trades as they happened. Section 194S changes that. Every qualifying transaction now leaves a trace.

Here’s how it works in practice:

When you sell a crypto asset, 1% of the total transaction value gets deducted right then and there. If you’re using an Indian-registered exchange, the platform usually handles this automatically. If not, such as in Peer-to-Peer (P2P) cases or decentralized off-ramp transactions, the buyer is statutorily required to deduct the tax, deposit it to the government using Form 26QE within 30 days from the end of the month in which the deduction is made, and issue a Form 16E TDS certificate to the seller.

You don’t lose that 1%. It’s credited to your tax account, almost like an advance payment. When you file your ITR later, this amount gets adjusted against your final tax liability.

But here’s the catch, and it’s a quiet one.

The deduction is on the gross transaction value, not your profit.

So even if you’re barely breaking even, or even trading at a loss, that 1% still gets sliced off. For casual investors, that’s mildly annoying. For high-frequency traders, it can start to feel like friction in the system, capital getting locked up in small chunks across dozens or hundreds of trades.

And yes, if your total tax liability ends up being lower than the TDS already deducted, you can claim a refund. But that means waiting, filing and reconciling. It’s not instant.

TDS Thresholds (Rs 10,000 vs. Rs 50,000)

Now, not every transaction gets hit with TDS right away. There’s a threshold system, but it’s slightly more nuanced than it looks at first glance.

There are two categories:

- ₹50,000 per year for “specified persons”

- ₹10,000 per year for everyone else

Most individual investors fall into the “specified person” bucket. That basically means you’re either not running a business, or your business turnover is below ₹1 crore (₹50 lakh for professionals). In plain terms, typical retail investors get the higher ₹50,000 cushion before TDS kicks in.

But once you cross that threshold, even by a small amount, the rule flips.

TDS doesn’t just apply to the excess. It applies to the entire value of that transaction and every transaction after that for the rest of the financial year.

That’s the part people often miss.

So, you might go months trading casually with no TDS, cross ₹50,000 in aggregate value, and suddenly every subsequent trade starts getting chipped by 1%. Furthermore, transacting parties must remain vigilant regarding Section 206AB; if the seller has failed to file their Income Tax Return (ITR) for the preceding financial year, the TDS rate under Section 194S escalates punitively from 1% to 5%, significantly impacting trading liquidity.

For businesses, active traders operating through firms, or individuals with higher turnover, the lower ₹10,000 threshold means this kicks in much earlier, sometimes almost immediately.

TDS on P2P Crypto Trading in India

This is where things get a bit hands-on.

If you’re trading through an exchange, most of the compliance burden is invisible. The platform deducts TDS, files it, and reports it. You barely notice.

But in peer-to-peer (P2P) trades, there’s no middle layer to absorb that responsibility. It lands directly on the participants—specifically, the buyer.

So, if you’re buying crypto directly from someone, whether through a P2P platform, a Telegram group, or a private deal, you’re legally required to:

- Deduct 1% of the transaction value

- Deposit it with the government using Form 26QE

- Pay the remaining 99% to the seller

Miss this, and things can escalate quickly.

The law treats failure to deduct or deposit TDS seriously. You could be labelled an “assessee in default,” which brings along interest penalties, 1% per month for not deducting, 1.5% per month for not depositing after deduction. And on top of that, a penalty equal to the TDS amount itself.

It’s not the kind of oversight you want to discover later during a notice.

Also worth noting: even if TDS isn’t deducted properly, the transaction might still show up in data systems. That mismatch, between what the system sees and what you report, can create complications down the line.

How to Claim Your Crypto TDS Refund in ITR

Eventually, all those small 1% deductions need to be accounted for.

When you file your ITR, this is where everything gets reconciled.

Your exchange (if you used one) reports TDS deductions to the government. This shows up in your Form 26AS and your Annual Information Statement (AIS). Ideally, what you see there should match what was actually deducted from your trades.

When filing:

- You report your VDA income in Schedule VDA

- Cross-check TDS entries in Form 26AS

- Claim that TDS as credit in your return

At the end of it, one of two things happens:

- If your total tax liability is higher than the TDS already deducted → you pay the difference

- If it’s lower → you get a refund

Simple in theory, but slightly tedious in practice, especially if there are discrepancies.

And those discrepancies do happen. Sometimes exchanges delay filings, sometimes entries don’t match perfectly. If you file without reconciling, it can slow down refunds, or worse, trigger notices.

Step-by-Step Guide: How to File ITR for Crypto Income

Which ITR Form to File for Crypto? (ITR-2 vs. ITR-3)

This sounds like a small decision, but picking the wrong ITR form is one of those mistakes that quietly comes back later as a “defective return” notice.

At a high level, it comes down to how your crypto activity fits into your overall income picture.

If you’re someone with a salary (or maybe some capital gains) and crypto is just another investment on the side, ITR-2 is usually your lane. It covers capital gains, includes Schedule VDA for crypto reporting, and doesn’t assume you’re running any kind of business.

That’s most people, honestly. Salaried folks who bought some BTC, maybe experimented with ETH or a couple of altcoins, sold a bit during the year—that’s ITR-2 territory.

Now, if your crypto activity starts looking more like a business, frequent trades, systematic strategy, maybe even alongside another business or professional income, then things shift.

That’s where ITR-3 comes in.

ITR-3 is designed for individuals or HUFs with business or professional income. If you’re treating crypto trading like an active operation (not just occasional investing), or you already have a business and crypto is part of that broader financial picture, this is the form you’re expected to use.

Both forms include Schedule VDA and Schedule FA (for foreign assets), so you’re not losing functionality either way, it’s more about classification than capability.

How to Fill Out Schedule VDA

Schedule VDA is where all your crypto activity gets exposed, for lack of a softer word.

This schedule was introduced specifically for VDAs, and it’s not optional if you’ve made any transfers during the year.

For each transaction, or at least each grouped set of transactions, you need to report:

- What asset you sold (Bitcoin, Ethereum, specific NFT, etc.)

- When you acquired it

- When you sold or transferred it

- What it cost you (in INR)

- What you received (again, in INR—this matters even for crypto-to-crypto swaps)

- The resulting gain

If you’ve only done a handful of trades, this is manageable. Slightly tedious, but manageable.

If you’ve been actively trading, it can get messy fast.

Most people in that situation don’t enter every single trade manually. They aggregate by asset, calculate total cost, total sale value, and net gain per asset, and report that. That’s generally acceptable, as long as you can back it up.

And that “back it up” part matters.

The expectation is that you maintain detailed records, transaction history, INR conversions, timestamps, for at least seven years. Not because you’ll definitely be audited, but because if you are, reconstruction after the fact is painful.

Once you fill Schedule VDA, the income flows into your tax computation automatically and gets taxed at the flat 30%. It doesn’t mix with your slab-rate income. It sits in its own compartment.

Reporting Foreign Crypto Assets in Schedule FA

This is the section people tend to underestimate, and sometimes regret underestimating.

If you’re an Indian resident and you hold crypto on a foreign exchange, or even in a wallet that’s considered “overseas,” you’re required to disclose it in Schedule FA (Foreign Assets).

Even if you didn’t sell anything. Even if there’s zero income.

That’s the key point: this is about ownership, not just profit.

You’ll need to provide:

- The country where the asset or exchange is based

- The type of asset (BTC, NFT, etc.)

- Peak value during the year (converted to INR)

- Value as of March 31

- Any income earned from it

Now, here’s where the tone shifts a bit, because the consequences here are heavy.

Non-disclosure of foreign assets doesn’t fall under the usual penalty framework. It triggers the Black Money Act, which is much harsher—30% tax on the value, a 90% penalty, and a minimum ₹10 lakh penalty per asset.

It’s the kind of rule that feels distant until you realise how many people casually use offshore exchanges without thinking of them as “foreign assets.”

And enforcement has tightened. Data-sharing agreements, FIU actions, exchange-level reporting—it’s not as opaque as it used to be.

Calculating Your Crypto Tax: Real-World Scenarios and Examples

Scenario 1: Profitable Trade (Buying & Selling for INR)

Let’s start simple. Clean trade and no complications.

Arun (name only for example), a fairly typical example, honestly, buys 0.5 BTC for ₹16,00,000. Holds it for a while. Sells it later for ₹24,00,000. Straightforward profit story.

Now the math:

- Sale value: ₹24,00,000

- Cost: ₹16,00,000

- Profit: ₹8,00,000

That ₹8,00,000 is fully taxable.

Apply 30% → ₹2,40,000

Add 4% cess → ₹9,600

Total tax → ₹2,49,600

Then comes TDS. The exchange would’ve already deducted 1% on the sale value (₹24,00,000), which is ₹24,000.

So, the final amount Arun actually pays at filing:

₹2,49,600 – ₹24,000 = ₹2,25,600

And here’s the slightly irritating detail—if he paid trading fees (say ₹5,000), they don’t reduce his taxable profit. The system just ignores that expense.

Scenario 2: Crypto-to-Crypto Swaps (Taxable Events)

This is where people usually pause and go, wait, that’s taxable too?

Yes. It is.

Swapping one crypto for another, say ETH for SOL, is treated as a transfer, which means it triggers tax under Section 115BBH. Even though no INR touches your bank account.

Take Meera’s (name only for example) case:

- She buys 2 ETH for ₹3,00,000 total

- Later swaps that 2 ETH for SOL when it’s worth ₹5,40,000

From a user perspective, it feels like a reshuffle. From a tax perspective, it’s a sale.

So:

- Deemed sale value: ₹5,40,000

- Cost: ₹3,00,000

- Profit: ₹2,40,000

Tax:

- 30% → ₹72,000

- 4% cess → ₹2,880

- Total → ₹74,880

And here’s the part that catches people off guard: Meera owes ₹74,880 in tax… even though she didn’t receive cash. Just SOL tokens.

So, unless she has liquidity elsewhere, she might actually need to sell some crypto just to pay the tax on a swap. Slightly ironic, but common.

Also important is that her new cost basis for the SOL becomes ₹5,40,000. That number matters later when she eventually sells.

This is why serious traders obsess over INR valuations at the moment of every swap. Not because they enjoy spreadsheets—but because without that data, tax filing becomes guesswork.

Scenario 3: Mixed Portfolio with Gains and Losses

This one feels the most “real life.”

Not every trade works out. Some go up, some don’t. You’d expect the system to recognise that balance.

It doesn’t.

Deepak’s (name only for example) year looks like this:

- Bitcoin: +₹3,00,000

- Ethereum: –₹1,20,000

- MATIC: +₹60,000

- Governance token: –₹40,000

Naturally, you’d think:

Total gain = ₹3,60,000

Total loss = ₹1,60,000

Net = ₹2,00,000 taxable

But that’s not how Section 115BBH works.

Losses don’t offset gains.

So, the taxable amount becomes:

₹3,00,000 (BTC) + ₹60,000 (MATIC) = ₹3,60,000

Tax:

- 30% → ₹1,08,000

- Cess → ₹4,320

- Total → ₹1,12,320

The ₹1,60,000 loss? It’s just disregarded. There is no carry forward and no adjustment.

For active traders, this is the rule that hurts the most. Not because losses are unusual, but because they become tax-irrelevant.

Edge Cases: DeFi, Airdrops, Staking, and NFTs

Tax on Crypto Airdrops and Gifts in India

Airdrops are one of those things that feel like free money. Tokens just appear in your wallet—no purchase, no effort (sometimes not even awareness).

The tax system doesn’t see it that way.

Under Section 56(2)(x), these are treated as income from other sources, not as capital gains which changes the entire tax treatment.

So, the moment you receive an airdrop, its fair market value in INR becomes taxable at your slab rate.

But it’s not 30%, your normal income tax slab.

This means that if you’re in the higher brackets, the initial tax hit could already be significant before you’ve sold anything.

Then, when you do sell those tokens later, Section 115BBH steps in:

- Sale value minus the value at the time you received the airdrop

- That gain gets taxed at 30%

So effectively, two tax events:

- At receipt (slab rate)

- At sale (30% on appreciation)

It’s a bit of a double-layer system. Not technically double taxation—but it can feel like it.

Gifts follow a similar logic.

If you receive crypto as a gift from a non-relative and the total value exceeds ₹50,000 in a year, it’s taxable as income from other sources. Same slab-rate treatment.

But there are exceptions—important ones:

- Gifts from close relatives (spouse, parents, siblings, etc.) are exempt

- Gifts received during marriage are exempt

- Inheritance is exempt

So, context matters here more than the asset itself.

How Crypto Staking Rewards are Taxed

Staking is still a bit of a grey area.

Not completely undefined, but not neatly settled either.

As of early 2026, there’s no specific CBDT circular that directly spells out how staking rewards should be taxed. So, what we have is a kind of practitioner consensus, the interpretation most tax professionals seem to agree on.

That interpretation goes like this:

When you receive staking rewards, they’re treated as income from other sources.

So again:

- You calculate the fair market value (in INR) at the time you receive the reward

- That value is taxed at your slab rate in that year

Then, later when you sell those reward tokens:

- Section 115BBH applies

- You pay 30% tax on the gain (sale price minus the value already taxed earlier)

So yes, staking can also create that two-step taxation effect:

- First when you earn

- Then when you exit

And because rewards often come in small, frequent distributions, tracking becomes tedious. You’re not just logging trades, but you’re logging every reward event with its INR value at that moment.

If you don’t, reconstructing it later is like trying to remember the price of coffee on 47 different mornings.

Given the lack of formal guidance, this is one of those areas where documentation matters even more than usual, and where getting professional advice isn’t overkill if the numbers are meaningful.

NFT Taxation Under VDA Rules

NFTs sit in an interesting spot.

Conceptually different from cryptocurrencies, but from a tax perspective, they’re mostly treated the same, as long as they’ve been officially notified as VDAs.

So, if you buy and sell NFTs:

- Profit = Sale price – Cost

- Tax = 30% (plus cess, surcharge if applicable)

No deductions beyond cost, no loss set-off. Same rules but different asset.

Where it gets slightly more nuanced is for creators.

If you’re minting NFTs and selling them regularly, say you’re an artist or running a digital collectibles project, you might expect that income to be treated as business income.

And in a way, it is.

But Section 115BBH overrides the rate.

So even if your activity looks like a business, the 30% tax still applies to the gains. You don’t get to fall back on slab rates or typical business deductions to reduce the burden.

And yes, the 1% TDS under Section 194S applies here too. Buyers (or marketplaces) are required to deduct it once thresholds are crossed.

Tax Notices, Audits, and FIU Compliance

How the FIU Regulates Crypto Exchanges in India

If crypto once felt like a slightly off-grid system, that illusion doesn’t really hold anymore.

The Financial Intelligence Unit of India (FIU-IND) now sits right in the middle of this ecosystem. It operates under the Ministry of Finance, and since March 2023, crypto platforms, exchanges, custodians, and transfer services have been officially classified as reporting entities under the Prevention of Money Laundering Act (PMLA).

Which sounds bureaucratic, but the implications are pretty concrete.

These platforms are now required to:

- Register with the FIU

- Run full KYC checks on users

- Monitor transactions continuously

- Flag and report suspicious activity

- Comply with international norms like the FATF Travel Rule

In other words, crypto platforms are being treated a lot more like banks than the loosely regulated tech platforms they once resembled.

By FY 2024–25, around 49 exchanges had registered with the FIU. Most of them India-based. And through the data they’ve been reporting, especially Suspicious Transaction Reports (STRs), authorities have already identified patterns linked to things like fraud, unaccounted transactions, and money laundering.

That data doesn’t just sit in a file somewhere. It gets shared with tax authorities.

There’s also been a noticeable push on enforcement.

In October 2025, the FIU issued show-cause notices to offshore exchanges that hadn’t registered or complied. Penalties have ranged widely, from lakhs to several crores.

Received an Income Tax Notice for Crypto? (Section 148A)

Getting a tax notice, especially one mentioning crypto, has a way of making things feel suddenly urgent.

Section 148A notices are typically issued when the Income Tax Department believes some income might have “escaped assessment.” In simpler terms, something in their data doesn’t line up with what you reported.

And with crypto, that data usually comes from:

- TDS filings under Section 194S

- Exchange-level transaction reporting

- FIU intelligence inputs

So, if you’ve traded actively but underreported (or not reported at all), there’s a decent chance the system already has a version of your activity.

The process itself has two stages:

First, under Section 148A(b), you receive a show-cause notice. It asks you to explain why reassessment shouldn’t happen. You get a chance to respond—this is important.

Then, under Section 148A(d), the department decides whether to proceed. Only if they decide yes does a formal reassessment notice follow under Section 148.

So it’s not an immediate penalty, it’s more like a warning shot with a chance to clarify.

If you do receive one, the practical steps are fairly grounded:

- Pull your complete transaction history from exchanges

- Reconcile it with what the notice is pointing to

- Identify gaps or mismatches

- Prepare a structured response

And, this is one of those moments where it genuinely helps, loop in a tax professional who understands VDAs. Not just general tax, but crypto-specific nuances.

In straightforward cases—say, an honest omission—you might still be able to correct things through a revised or updated return before it escalates.

Penalties for Non-Reporting

This is where the tone shifts slightly again, not alarmist, but definitely firm.

The penalty framework around crypto non-compliance isn’t vague. It’s structured, and in some cases, quite steep.

A few key ones:

- Under-reporting of income → 50% of the tax amount

- Misreporting or concealment → 200% of the tax amount

- Failure to file ITR → up to ₹5,000, plus interest on unpaid tax

- Undisclosed foreign crypto assets → minimum ₹10 lakh per asset + 90% penalty under the Black Money Act

- Wilful tax evasion → prosecution, including possible imprisonment (3 months to 7 years)

That last one tends to sound distant, but it exists for a reason. Especially in cases where non-compliance is seen as intentional.

What’s worth keeping in mind is that the system still leaves room to correct mistakes—if you act early.

Revised returns can be filed within the allowed window (currently up to two years from the end of the assessment year). Beyond that, voluntary disclosure, along with paying tax, interest, and penalties, is usually the safer route than waiting for a notice.

NRI Crypto Tax Rules and FEMA Implications

Does the 30% Crypto Tax Apply to NRIs?

This is one of those questions where people expect a yes/no answer. But the reality is a bit more conditional.

In India, crypto tax doesn’t depend on your passport. It depends on your residential status under the Income Tax Act.

So, the first step isn’t “Are you an NRI?”

It’s “How many days did you spend in India this year—and in previous years?”

Broadly:

- 182 days or more in a financial year → Resident

- Or 60 days + 365 days over the past 4 years → also Resident (with some nuances)

If you don’t meet those, you’re treated as a Non-Resident.

Now here’s where it splits.

If you’re a resident, India taxes your global income. That includes crypto gains—no matter where the exchange is, where the wallet is, or where the trade happened.

If you’re a non-resident, India only taxes income that has a connection to India—what the law calls “accrues or arises in India.”

So, for NRIs:

- If you bought and sold crypto entirely outside India, using foreign exchanges, and the money never touched India → generally not taxable in India

- But if there’s an Indian link—say, you used an Indian exchange, or funds moved through an Indian bank account—then the gain can fall within India’s tax net and be taxed at 30% under Section 115BBH

That “Indian nexus” idea is where most of the ambiguity sits. It’s not always obvious, and small details—like where the transaction was executed or where the funds landed—can change the outcome.

Also worth noting: people who move back and forth (especially returning NRIs) can fall into the RNOR (Resident but Not Ordinarily Resident) category, which has its own quirks. It’s not always intuitive, and assumptions here can go wrong quickly.

FEMA Rules for Offshore Trading

Now layer FEMA on top of all this, and things get a bit more philosophical.

Because FEMA doesn’t define “resident” the same way the Income Tax Act does.

Under FEMA, if you’ve been in India for more than 182 days in the preceding financial year, you’re generally treated as a resident. Slightly different lens. Which means you could be a non-resident for tax purposes but still fall within FEMA’s scope.

And FEMA isn’t about tax—it’s about movement of money. Capital flows. Foreign exchange.

Under the Liberalised Remittance Scheme (LRS), Indian residents can send up to USD 2,50,000 abroad each year for permitted uses, including investments.

Here’s the complication: crypto isn’t explicitly classified under LRS rules.

So, when you use an overseas exchange:

- Is that treated as an overseas investment?

- Is it something else entirely?

There’s no perfectly settled answer yet. The RBI has historically taken a cautious stance on crypto, and as of 2026, the FEMA treatment of offshore crypto holdings still feels unresolved.

But some things are clearer:

- If you’re a resident, you still have to declare foreign crypto holdings in Schedule FA

- Tax obligations apply regardless of FEMA ambiguity

- If you bring money back into India (from selling crypto abroad), it has to go through proper banking channels—typically NRE/NRO accounts—with documentation

So even if the regulatory framework isn’t fully stitched together, compliance expectations still exist.

Frequently Asked Questions (FAQs) About Crypto tax India 2026

You pay a flat 30% tax on all crypto profits under Section 115BBH, plus a 4% health and education cess. Additionally, a 1% TDS is deducted on transfers under Section 194S. Your regular income tax slab does not reduce this flat 30% VDA rate.

Crypto is not illegal, but it remains unregulated. The government taxes it strictly as a Virtual Digital Asset (VDA) but does not recognize it as legal tender. You can legally trade on FIU-registered exchanges, provided you report all holdings and gains in your Income Tax Return.

Yes. The tax department tracks crypto activity through the 1% TDS mechanism (visible in your Form 26AS/AIS). Furthermore, under the Prevention of Money Laundering Act (PMLA), all FIU-compliant exchanges are legally mandated to report high-value and suspicious transactions directly to the government.

No. You cannot offset crypto losses against gains from other crypto assets or any other income source. If you make a ₹1 lakh profit on Bitcoin and a ₹50,000 loss on Ethereum, you still pay 30% tax on the full ₹1 lakh Bitcoin gain. Losses also cannot be carried forward to future years.

Failing to declare crypto can trigger an Income Tax Notice under Section 148A. Penalties range from 50% to 200% of the evaded tax. Crucially, hiding crypto held on foreign exchanges or offshore wallets can trigger severe penalties (up to ₹10 lakh per asset) under the strict Black Money Act.

| Regulatory Section | What it Applies To | Rate / Penalty | Key Rule for Investors (2026) |

| Section 115BBH (Income Tax) | All profits from trading or selling VDAs (Crypto/NFTs) | 30% Flat Tax (+ Surcharge & Cess) | No deductions allowed except purchase cost. No offsetting or carry-forward of losses. |

| Section 194S (TDS) | Any transfer of VDAs | 1% Deducted at Source | Deducted automatically by exchanges. For P2P trades, the buyer is liable to deduct and deposit. |

| Section 56(2)(x) (Gift Tax) | Crypto received as gifts or Airdrops | Taxed at your Income Slab Rate | Fully taxable as “Income from Other Sources” if the value exceeds ₹50,000 (unless from a relative). |

| PMLA / FIU-IND Guidelines | Crypto Exchanges & Custodians | Account Freezes / URL Blocks | Your exchange reports your trades directly to the government. Trading on non-compliant offshore platforms risks asset freezing. |

| Schedule VDA & Schedule FA | Income Tax Return (ITR) Filing | Up to ₹10 Lakh Penalty (Black Money Act) | Must declare all VDA trades in Schedule VDA. Must declare foreign exchange wallets in Schedule FA. |

| GST Rules | Exchange Fees / Brokerage | 18% GST | Levied on the platform’s trading fees, increasing your overall transaction costs. |

Final Checklist for Safe Crypto Tax Filing in India (2026)

India’s crypto tax framework in 2026 isn’t ambiguous anymore. That phase is over. What exists now is something far more structured, arguably rigid, definitely comprehensive, and increasingly backed by data.

The key pillars don’t really leave much room for interpretation:

- A flat 30% tax under Section 115BBH

- A 1% TDS under Section 194S that tracks transactions as they happen

- No loss set-offs, no carry forwards

- Mandatory disclosures through Schedule VDA and Schedule FA

Put together, it creates a system where almost every meaningful crypto action, buying, selling, swapping, receiving, leaves a tax footprint.

And once you’ve seen a few real calculations (those earlier scenarios tend to do that), it becomes clear this isn’t something you can “figure out later.” The margin for casual tracking is small.

So, what actually helps, in practical terms?

Not anything fancy. Just discipline, mostly.

Keep a record of every transaction—date, cost, sale value, all in INR. Especially for swaps, where there’s no obvious cash value unless you record it at the moment.

Check your TDS entries in Form 26AS before filing and not after. Fixing mismatches later is possible, but unnecessarily frustrating.

If you’re using foreign exchanges or even just holding assets there, don’t skip Schedule FA. That’s one of those areas where the downside of getting it wrong is disproportionate.

And maybe the less obvious one: don’t rely on memory. Crypto activity stacks up faster than you think. What feels like “a few trades” often turns into a long trail by year-end.

At the same time, this framework isn’t frozen.

There’s ongoing pressure, from industry groups, from platforms, from users, for changes. Loss set-offs, lower TDS, clearer rules on staking and DeFi none of these are fringe concerns anymore. They’re being discussed seriously.

Whether those changes come soon or not is another question.

Until they do, though, the current rules apply in full. No partial compliance, no “close enough.”

So, the real takeaway isn’t dramatic, it’s just steady:

If you’re in crypto in India right now, you’re operating inside a system that expects visibility. And the easiest way to deal with that is to stay ahead of it, not catch up to it.

Disclaimer

The content on this page is intended for informational and educational purposes only and should not be construed as professional financial, tax, or legal advice. India Policy Hub and its authors are not certified financial planners, registered investment advisors, or practicing Chartered Accountants (CAs). Tax laws, particularly regarding international assets and compliance, are complex and subject to change. Always consult a qualified professional or Chartered Accountant regarding your specific financial situation, tax liabilities, or legal compliance before making any financial decisions or submitting tax declarations.

Leave a Reply