What is the PF Ceiling Limit for 2026? A Complete Guide to the ₹25,000 Shift

Understanding the PF Ceiling Limit for 2026: Navigating the ₹25,000 EPF Wage Shift

If you’ve looked at your salary slip in 2026 and felt like something was off, you’re not imagining it. There’s a major shift underway in India’s provident fund system, one that could quietly change how much lands in your bank account every month, and how much waits for you years down the line. Herein comes the issue of the PF ceiling limit for 2026.

For over a decade, the EPF wage ceiling has sat at ₹15,000. It became the norm. Payroll systems adjusted to it. HR teams stopped thinking about it. Most employees barely noticed it.

But 2026 has cracked that old number open. With the government reportedly moving toward a revised framework, understanding the new PF ceiling limit for 2026 is no longer optional for the Indian workforce.

The government is now reportedly moving toward a revised EPF wage ceiling of ₹25,000, a change that, on paper, might look like just another compliance update. In reality? It touches almost everything: monthly deductions, employer contributions, pension eligibility, tax planning, and even long-term retirement math.

And this isn’t just relevant for finance teams or payroll managers. If you’re a salaried employee in India—whether you’re early in your career, somewhere in the middle, or planning retirement—this shift matters.

In this guide, we’ll break down what’s changing, why it’s happening now, what the legal background looks like, and how this could affect your money in practical terms. No jargon for the sake of jargon. Just the numbers, the rules, and what they actually mean in real life.

If you’ve looked at your salary slip in 2026 and felt like something was off, you’re not imagining it. There’s a major shift underway in India’s provident fund system, one that could quietly change how much lands in your bank account every month, and how much waits for you years down the line.

At a Glance: The 2026 PF Ceiling Shift

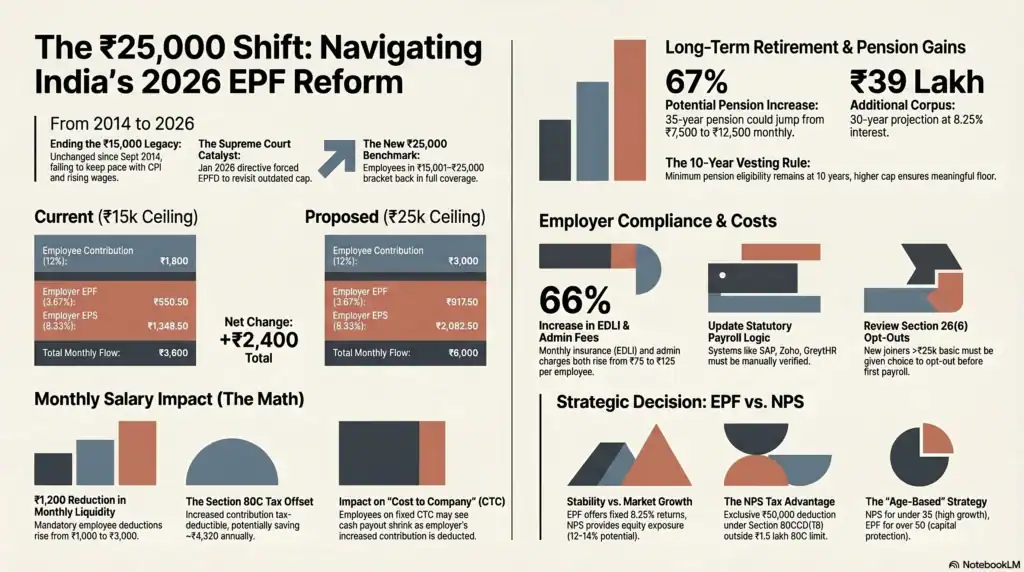

- The Threshold Hike: The statutory EPF wage ceiling is transitioning from ₹15,000 to ₹25,000, marking the first major adjustment in over a decade.

- Take-Home Impact: For employees earning above the old limit, the mandatory monthly deduction increases from ₹1,800 to ₹3,000, reducing immediate liquidity by ₹1,200 per month.

- Pension Potential: The shift significantly expands the EPS pensionable salary base, which can lead to a potential 60% increase in monthly pension payouts upon retirement.

- Opt-Out Eligibility: “Opt-Out Eligibility: Employees joining a new establishment with a basic salary above the proposed ₹25,000 threshold qualify as “excluded employees” under the EPF Act, granting them the option to opt out entirely. However, should they wish to participate, they must execute a formal joint declaration with their employer under Para 26(6) of the EPF Scheme, 1952, legally permitting them to voluntarily contribute on their actual higher wages rather than being restricted to the statutory limit.

- Employer Costs: Organizations face higher payroll burdens due to increased employer matching and higher EDLI and administrative charges calculated on the new base.

The Core Facts: What Is the Current EPF Wage Ceiling?

Before we get into what’s changing, it helps to understand what this wage ceiling actually does and why such a seemingly boring number has such an outsized impact on retirement savings in India.

Under the Employees’ Provident Fund & Miscellaneous Provisions Act, 1952, establishments employing 20 or more workers are required to enrol eligible employees under the EPF scheme. Both employer and employee contribute 12% of the employee’s basic wages every month.

Sounds simple enough.

But there’s a catch: that contribution isn’t calculated on your full salary indefinitely. It’s subject to a statutory wage ceiling, a cap that decides how much of your salary is considered for mandatory EPF contributions.

As things stand today, that ceiling remains ₹15,000 per month.

The ₹15,000 Legacy (2014 to Present)

That ₹15,000 limit has been around since September 2014, when the government raised it from the earlier ₹6,500 ceiling.

Back then, it made sense. Wages looked different. Inflation was lower. Salary structures across sectors were nowhere near where they are today.

The EPFO today manages retirement savings for more than 60 million active subscribers, making it one of the largest retirement fund institutions anywhere in the world. That’s not a niche policy issue. That’s the financial backbone of a huge slice of India’s workforce.

Here’s what the ceiling means in practice:

If your basic salary is ₹15,000, or even ₹50,000, your statutory EPF contribution is still calculated only on ₹15,000.

So:

12% × ₹15,000 = ₹1,800 per month.

That’s the mandatory employee contribution. Your employer’s matching obligation also stops there.

Anything above ₹15,000? Not automatically included.

Yes, employees can voluntarily contribute more through VPF. But unless the employer chooses otherwise, their mandatory contribution doesn’t rise beyond that ceiling.

And that’s where things start to feel outdated.

A worker earning ₹30,000, ₹50,000, or even more in basic wages may still be building retirement savings based on a wage benchmark set over ten years ago. Over time, that gap adds up—quietly, but significantly.

The Supreme Court Intervention (January 2026 Directive)

Interestingly, the real push for change didn’t come from payroll software companies, HR associations, or industry lobbying.

It came from the judiciary.

In January 2026, the Supreme Court of India directed the Employees’ Provident Fund Organisation to revisit the ₹15,000 wage ceiling, effectively signalling that the existing cap may no longer reflect present-day wage realities.

As stated in this report, the Court’s direction placed real pressure on the EPFO and the government to present an updated framework.

And that matters.

Because once a policy question moves from “under consideration” to “under judicial scrutiny,” things tend to accelerate.

Since that directive, policy circles and industry bodies have been actively discussing what the revised ceiling should look like. Some estimates floated numbers between ₹21,000 and ₹30,000.

But right now, ₹25,000 appears to be the number gaining the most traction.

The Proposed 2026 Hike: Moving the Goalposts to ₹25,000

After years of silence around the EPF wage ceiling, things are finally starting to move, and this time, not by a few hundred rupees.

The number currently being discussed most seriously inside policy circles is ₹25,000. This proposed PF ceiling limit for 2026 isn’t an arbitrary jump; it’s an inflationary correction long overdue.”

Nothing has been formally gazetted yet. That part matters. But by now, enough signals have emerged from government conversations, industry discussions, and labour-policy reporting to make one thing fairly clear: the ₹15,000 era is nearing its end.

And honestly, it was starting to feel overdue.

For employees, this isn’t just another bureaucratic revision buried in a government PDF. A higher ceiling changes the amount deducted from salary, increases employer contributions, affects pension calculations, and alters long-term retirement accumulation in ways many people haven’t fully processed yet.

So why ₹25,000? Why now?

Why the Shift from ₹15k to ₹25k? (Inflation and Real Wages)

A lot has changed since 2014.

Back when the EPF wage ceiling was raised to ₹15,000, that amount reflected a very different wage environment. Rent was lower. Grocery bills looked different. Fuel prices, well, you remember.

Twelve years later, that same number doesn’t stretch nearly as far.

Between 2014 and 2026, India’s Consumer Price Index (CPI) has climbed sharply. In practical terms, ₹15,000 in 2014 doesn’t buy what ₹15,000 buys today—not even close.

If the EPF ceiling had simply kept pace with inflation, estimates suggest it would now sit somewhere between ₹24,000 and ₹26,000.

Which makes the proposed ₹25,000 figure feel less like a policy experiment and more like a delayed correction.

According to reports in mainstream media, average salaries across organised sectors now significantly exceed the current ₹15,000 benchmark in most parts of India.

That creates a strange mismatch.

Millions of employees earn well above ₹15,000 in basic wages, yet their EPF contributions are still being calculated using a salary ceiling designed for a completely different economic climate.

Raising the ceiling to ₹25,000 would pull a large portion of those employees back into fuller mandatory coverage, especially workers sitting in that ₹15,000 to ₹25,000 salary band who have effectively been living in a policy grey zone.

And according to reports, the government also sees this as part of a broader effort to strengthen long-term social security under India’s evolving labour reforms.

Short-term deductions may rise. That’s the uncomfortable part.

But over a 20- or 30-year career? The retirement difference could be substantial.

Labour Codes vs. EPF: Addressing the ₹21,000 ESI Confusion

If you’ve spent any time discussing payroll changes with colleagues or honestly, even with some HR teams—you’ve probably heard the ₹21,000 number thrown around.

And that’s where confusion starts.

A lot of people assume ₹21,000 is somehow connected to EPF.

It isn’t.

That number belongs to ESIC—the Employees’ State Insurance Corporation scheme.

ESIC mainly covers health-related benefits like medical coverage, sickness benefits, maternity support, and disability-related protections. As of now, ESIC generally applies to employees earning up to ₹21,000 per month.

EPF is different.

EPF is retirement-focused. Different legislation. Different deductions. Different purpose.

So:

- ₹21,000 = ESIC wage ceiling

- ₹15,000 = Current EPF wage ceiling

- ₹25,000 = Proposed EPF wage ceiling for 2026

Simple on paper. Confusing in real payroll conversations.

For a deeper comparison of ESI and EPF applicability, see this guide.

Now add labour codes to the mix, and things get even messier.

India’s Code on Social Security, 2020 aims to bring multiple social security frameworks under one broader structure. In theory, that could eventually create more alignment between schemes like EPF and ESIC.

But theory and implementation are two different things.

As noted by here, the labour codes are still being rolled out across states and are not yet fully operational nationwide.

Which means, for now, the EPF Act of 1952 remains the law that actually governs provident fund contributions.

So yes, the ₹21,000 and ₹25,000 numbers may appear in the same payroll conversation.

But they’re solving completely different problems.

Financial Mechanics: How the New Ceiling Impacts Your Salary

This is the part most people actually care about.

Policy debates are one thing. Court directives, labour codes, government proposals—important, sure. But for most salaried employees, the real question usually comes down to something much simpler:

What happens to my salary?

Because if the EPF wage ceiling moves from ₹15,000 to ₹25,000, you will directly notice the impact on your next payslip. Furthermore, the calculation base itself is shifting; under Section 2(y) of the Code on Wages, 2019, excluded allowances (such as HRA and special allowances) cannot exceed 50% of total remuneration. If they do, the excess is forcibly added back to the basic wage, meaning the new 12% PF deduction will be calculated on a significantly wider, restructured wage base up to the ₹25,000 ceiling.

For others—especially those who track every deduction—it could be the first number their eyes go to.

So let’s break down the actual math.

The Formula: Calculating 12% on ₹25,000 vs. ₹15,000

EPF calculations are fairly straightforward once you understand how the contribution gets split—but this is exactly where many employees get confused.

Under the EPF framework, both the employee and employer contribute 12% of Basic Salary + Dearness Allowance, subject to the statutory wage ceiling.

From the employer’s 12% contribution:

• 3.67% goes to EPF

• 8.33% goes to EPS (Employee Pension Scheme)

Under the current ₹15,000 ceiling, contributions are capped there, even if your actual basic salary is much higher.

That means:

Current Ceiling (₹15,000)

Employee contribution:

12% × ₹15,000 = ₹1,800/month

Employer contribution:

• EPF portion = ₹550.50/month

• EPS portion = ₹1,249.50/month

Total monthly flow into your PF ecosystem: ₹3,600

Now compare that with the proposed ₹25,000 ceiling. The following math illustrates how the PF ceiling limit for 2026 fundamentally alters your monthly contribution structure:

Proposed Ceiling (₹25,000)

Employee contribution:

12% × ₹25,000 = ₹3,000/month

Employer contribution:

• EPF portion = ₹917.50/month

• EPS portion = ₹2,082.50/month

Total monthly flow: ₹6,000

That’s an increase of ₹2,400 every month.

Not small.

Not theoretical.

Actual money moving into long-term retirement savings.

Here’s the comparison side by side:

| Component | Current (₹15,000 ceiling) | Proposed (₹25,000 ceiling) | Change |

| Employee EPF Contribution | ₹1,800/month | ₹3,000/month | +₹1,200/month |

| Employer EPF Contribution (3.67%) | ₹550.50/month | ₹917.50/month | +₹367/month |

| Employer EPS Contribution (8.33%) | ₹1,249.50/month | ₹2,082.50/month | +₹832/month |

| Total monthly flow into PF ecosystem | ₹3,600/month | ₹6,000/month | +₹2,400/month |

| Annual accumulation (combined) | ₹43,200/year | ₹72,000/year | +₹28,800/year |

And this is where things get interesting.

An extra ₹2,400 a month may not feel life-changing on its own. But retirement planning rarely works in monthly snapshots. It works through compounding.

Assuming EPFO’s current long-term interest rate of 8.25% per annum, the long-term difference becomes much harder to ignore.

Illustrative 30-year corpus projection:

| Ceiling | Monthly Combined Contribution | Approx. 30-Year Corpus |

| ₹15,000 | ₹3,600 | ~₹58.5 lakhs |

| ₹25,000 | ₹6,000 | ~₹97.5 lakhs |

| Gain | — | ~₹39 lakhs |

That’s nearly ₹39 lakhs of additional retirement accumulation, driven largely by a single ceiling revision.

Of course, real life rarely follows perfect spreadsheets.

Salaries increase. People switch jobs. Interest rates change. Careers take detours.

Still, the larger point doesn’t change.

A higher EPF ceiling doesn’t just increase monthly deductions.

Over time, it can reshape what retirement actually looks like.

The Take-Home Pay Hit: Short-Term Pain, Long-Term Gain

Now for the part most employees actually care about first:

Will my in-hand salary drop?

In many cases—yes.

And there’s no point pretending otherwise.

Let’s say your basic salary is ₹25,000.

Under the current ceiling, your employee EPF deduction is ₹1,800 per month.

Under the proposed ceiling, that becomes ₹3,000.

That’s an extra ₹1,200 deducted from your monthly salary.

Or ₹14,400 per year.

If your company doesn’t restructure your compensation, that money comes straight out of your take-home pay.

That’s the short-term hit.

But there’s another side to this.

EPF contributions remain eligible for tax deduction under Section 80C under the old tax regime.

So if you fall in a higher tax bracket, part of that extra contribution may come back indirectly through lower taxable income.

For example:

An employee in the 30% tax bracket contributing an extra ₹14,400 annually could save roughly ₹4,320 in taxes.

Not enough to erase the impact completely—but enough to soften it.

And as noted in this guide, the 2026 tax framework has broadly retained existing EPF tax treatment:

- Employee contributions remain eligible under 80C (old regime)

- Employer contributions up to statutory limits remain tax-efficient

- Withdrawals after 5 years of continuous service remain tax-free

For broader income tax changes affecting salaried employees, see this guide.

So yes, cash in hand may shrink.

But retirement security improves.

And for some people, that trade-off is worth it.

For others… maybe not. Especially if monthly liquidity is already tight.

That’s where salary structure starts to matter.

Will my employer reduce my in-hand salary?

This is probably the question HR teams are hearing most right now.

And the answer is frustratingly simple:

It depends on how your compensation is structured.

Here’s how it usually plays out:

Scenario A — Fixed Gross Salary

If your offer letter says you earn a fixed monthly gross salary, say ₹50,000, then higher EPF deductions usually mean lower take-home pay.

Your employer isn’t automatically required to increase your gross salary to offset the deduction.

So yes, your in-hand salary could fall.

Scenario B — Fixed CTC Model

If your company uses a Cost to Company structure, things get trickier.

Because your employer’s EPF contribution often forms part of your CTC.

So if their contribution rises, they may adjust other salary components to keep the total CTC unchanged.

Result?

Your cash payout could shrink—even if your official salary package stays exactly the same.

A little corporate math. Very common.

Scenario C — Employer Absorbs the Cost

Some larger companies may choose to absorb the extra contribution themselves.

That means:

- Your take-home pay stays largely unchanged

- Your employer increases the total compensation cost instead

Not every company will do this. But some will, especially in competitive hiring sectors.

As stated in this report, many employers are expected to wait until the final government notification before making any compensation changes.

So, for now, there’s a lot of watching, modelling, and quiet spreadsheet panic happening inside payroll teams.

Pretty standard.

The Employer Perspective: CTC Restructuring and Compliance Costs

For employees, the proposed EPF ceiling hike usually starts with one question:

“How much less am I taking home?”

For employers, the question is very different:

“How much more is this going to cost us—and how fast do we need to adapt?”

And honestly, that’s where the real operational pressure begins.

A jump from ₹15,000 to ₹25,000 may sound manageable when you’re thinking about one employee. But multiply that across hundreds—or thousands—of workers, and suddenly finance teams are looking at a very different payroll bill.

This isn’t just about higher provident fund contributions either.

It affects insurance contributions, administrative charges, payroll software settings, compliance filings, employee communication… the whole machinery.

And if your organisation still runs salary structures built around older compliance assumptions, things can get messy fast.

Increased Employer Matching and EDLI Contributions

When most people think of employer PF contributions, they think of the employer’s 12% match.

Fair enough, but that’s only part of the picture.

Under the EPF framework, employers also contribute toward EDLI—the Employees’ Deposit Linked Insurance scheme. This gives EPF members a life insurance cover linked to employment.

The EDLI contribution is currently calculated at 0.5% of wages, subject to the statutory ceiling.

So, under today’s ₹15,000 ceiling:

Employer EDLI contribution:

0.5% × ₹15,000 = ₹75 per employee per month

Simple enough.

Now apply the proposed ₹25,000 ceiling:

0.5% × ₹25,000 = ₹125 per employee per month

That’s ₹50 extra per employee, every month.

On its own? Doesn’t sound dramatic.

But scale changes everything.

A company with 1,000 employees covered under this ceiling would see:

₹50 × 1,000 = ₹50,000 extra every month

Just from EDLI.

And that’s before factoring in higher EPF, EPS, and admin charges.

Employers also pay administrative charges to EPFO, currently calculated at 0.5% of wages.

Which means:

- At ₹15,000 ceiling → ₹75/month

- At ₹25,000 ceiling → ₹125/month

Again, another ₹50 increase per employee.

Now combine the cascading statutory costs:

- Higher employer EPF contributions

- Higher EPS diversions

- Increased administrative charges

- Elevated liabilities under the Employees’ Deposit Linked Insurance (EDLI) Scheme, 1976: Because the EDLI premium mandates a 0.5% employer contribution mapped directly to the wage ceiling, raising the cap to ₹25,000 proportionally increases the employer’s insurance outlay while simultaneously enhancing the maximum statutory death benefit cover for the workforce

And suddenly, for mid-sized or large organisations, payroll costs start climbing by several lakhs every month.

That’s why finance teams aren’t treating this as a routine update.

How to Update Payroll Systems for the New Ceiling

Once the government formally notifies the new ceiling, HR and payroll teams won’t have much breathing room.

Because statutory changes like this don’t just live in policy memos—they hit real salary cycles.

Miss a payroll update, and suddenly employees start flooding inboxes asking why deductions look wrong.

So what actually needs to happen?

Here’s the typical compliance checklist:

Update the statutory ceiling inside payroll software

Sounds obvious. Still gets missed.

Every payroll engine—whether it’s SAP, Zoho Payroll, Darwinbox, GreytHR, or a custom ERP—will need the ceiling changed from ₹15,000 to ₹25,000.

Many systems may push updates automatically.

Still… trusting automation blindly in payroll? Risky move.

Manual verification matters.

Recalculate impacted employees

The biggest impact usually hits employees earning between ₹15,001 and ₹25,000 in basic wages.

This group often sees the sharpest change in both:

- Employee deductions

- Employer contributions

They’re the first batch payroll teams will need to audit carefully.

Review CTC structures

Some employers may choose to absorb the added cost.

Others may restructure salaries to keep overall CTC constant.

That could mean:

- Revised salary breakups

- Addendums to offer letters

- Fresh compensation communication

Not fun paperwork—but often unavoidable.

Update statutory filings

The Electronic Challan cum Return (ECR) on the EPFO Unified Portal will need updated wage and contribution data.

Missed or incorrect filings can create compliance headaches later—sometimes months later, when reconciliation starts.

And by then nobody remembers who changed what.

Classic payroll problem.

Communicate with employees early

This part gets ignored far too often.

If salary deductions suddenly increase and nobody explains why, employees usually assume one of two things:

- Payroll made a mistake

- The company quietly cut take-home pay

Neither creates a healthy Monday morning.

A clear communication from HR—before the first revised payslip lands—can prevent a lot of confusion.

Review exempted PF trusts

Companies operating their own exempted PF trusts need to align internal trust rules with the revised statutory ceiling.

That may require legal review, actuarial recalculations, or board approvals depending on the structure.

Definitely not something to leave for the last week of implementation.

For official guidance, employers should monitor the EPFO Unified Portal, the EPFO FAQ page, and reform communications such as this.

Because when a statutory change goes live, payroll doesn’t get grace periods.

It just gets deadlines.

The EPS Pension Revolution: From ₹1,000 to ₹7,500?

When most employees think about EPF, they usually think about the provident fund balance—the lump sum they’ll eventually withdraw, maybe at retirement, maybe during a job transition, maybe for a home purchase somewhere in between.

Fair.

But tucked inside the EPF ecosystem is another piece that often gets ignored until much later:

EPS — the Employees’ Pension Scheme.

And if the EPF wage ceiling really moves to ₹25,000, EPS may end up seeing one of the biggest ripple effects of all.

In fact, for some employees, the pension impact could matter more than the PF balance itself.

That sounds dramatic. But once you look at the numbers… it starts making sense.

How a Higher Wage Ceiling Expands Pension Coverage

Under the current EPF structure, a part of your employer’s contribution doesn’t actually go into your provident fund.

Instead, 8.33% of the employer’s contribution is diverted into EPS.

But here’s the limitation:

That EPS contribution is capped based on the existing wage ceiling of ₹15,000.

So the maximum EPS contribution today works out to:

8.33% × ₹15,000 = ₹1,250 per month

That means even if your salary is significantly higher, your pensionable salary is still being calculated using that ₹15,000 ceiling.

And that ceiling hasn’t moved since 2014.

That’s a long time in wage terms.

Now imagine the ceiling shifts to ₹25,000.

Suddenly the math changes:

8.33% × ₹25,000 = ₹2,082.50 per month

That’s an increase of more than ₹800 per employee, every month, flowing toward pension contributions.

Quietly. Automatically. Without the employee doing anything extra.

And over decades? That’s not small.

EPS pensions are calculated using this formula:

Monthly Pension = (Pensionable Salary × Pensionable Service) ÷ 70

For employees who complete long service periods, that formula becomes very meaningful.

For example:

An employee with 35 years of pensionable service under the current ceiling:

(₹15,000 × 35) ÷ 70 = ₹7,500/month

Under the proposed ₹25,000 ceiling:

(₹25,000 × 35) ÷ 70 = ₹12,500/month

That’s a 67% increase in the maximum pension potential.

Not a cosmetic policy tweak.

A real retirement difference.

For official EPS calculation guidance, see here.

And for workers approaching retirement age, this may be one of the most important numbers in the entire reform package.

The Minimum Pension Hike Debate

While contribution ceilings are getting attention, there’s another conversation running alongside it—one that’s far more emotional for pensioners.

The minimum EPS pension.

Right now, many EPS pensioners receive just ₹1,000 per month.

Read that again.

₹1,000.

Even in 2014, people argued it wasn’t enough.

In 2026? For many retirees, it barely covers a utility bill.

Which is why pensioner associations, labour unions, and worker advocacy groups have been pushing hard for a revised minimum pension of ₹7,500 per month.

And the momentum is building.

According to this guide, demands for a higher EPS pension floor have gained serious traction in 2026, with multiple policy discussions and parliamentary recommendations keeping the issue alive.

That doesn’t mean approval is guaranteed.

Far from it.

Because increasing the minimum pension has a direct fiscal cost for the government, which already supports the EPS framework through budgetary subsidies.

And once pension commitments rise, they don’t quietly shrink later.

So while the demand for ₹7,500 is gaining visibility, the Ministry of Labour hasn’t formally locked in a number yet.

Still, if the wage ceiling moves higher first, it creates the financial and policy foundation for a future pension revision.

Which may be exactly where this is headed.

For pension eligibility details and related application processes, see this.

How much EPS pension will I get after 10 years?

This is one of the most searched EPS questions—and understandably so.

Under EPS rules, 10 years of pensionable service is the minimum threshold to qualify for monthly pension benefits.

So, let’s say an employee completes exactly 10 years under the proposed ₹25,000 ceiling.

The pension formula becomes:

(₹25,000 × 10) ÷ 70 = ₹3,571/month

Now compare that with the current ceiling:

(₹15,000 × 10) ÷ 70 = ₹2,143/month

That’s a monthly increase of:

₹1,428

Maybe that doesn’t sound life-changing at first glance.

But retirement math is funny.

Stretch that over 20 years of retirement:

₹1,428 × 12 × 20 = roughly ₹3.43 lakhs

And that’s money the employee didn’t actively invest, trade, or manage.

It simply comes from being inside the system longer—and under a higher pensionable salary cap.

That’s why this reform matters more than many people realise.

Also worth remembering:

If an employee leaves service before completing 10 years, they typically don’t qualify for a monthly EPS pension. Instead, they may receive a withdrawal benefit, calculated under EPS rules.

And yes—the higher ceiling improves that calculation too.

Quietly. But meaningfully.

Strategic Opt-Outs: Can You Avoid the EPF Deduction?

Once employees hear that PF deductions could rise under the new ₹25,000 ceiling, the next question usually comes fast:

“Can I just opt out?”

And honestly… it’s not a bad question.

Not everyone sees EPF the same way.

Some people love the forced discipline. Money goes in, compounds quietly, and one day it becomes a decent retirement cushion.

Others, especially higher earners, see it differently. They’d rather keep more liquidity, invest in equity funds, build their own retirement corpus, maybe chase better returns elsewhere.

So where does the law stand?

Can you actually avoid EPF if the ceiling moves to ₹25,000?

The answer is yes… but only in very specific situations.

And once you’re inside the system, getting out is a whole different story.

The ₹25,000 Threshold and Mandatory vs. Voluntary Coverage

Under current EPF rules, membership depends largely on your salary at the time you join employment, not what happens later.

That distinction matters more than most people realise.

As things stand today:

If your basic salary is ₹15,000 or below at the time of joining an EPF-covered establishment, EPF membership is generally mandatory.

If your salary exceeds the wage ceiling at the time of joining, you may qualify as an “excluded employee” and can choose not to join.

Now if the ceiling officially moves to ₹25,000, that threshold rises too.

Meaning:

Employees joining a new EPF-covered company with a basic salary above ₹25,000 may have the option to remain outside the EPF system.

That’s where strategic decisions start creeping in.

Some employees may choose to opt out and invest that money elsewhere.

Others may still join voluntarily because, frankly, walking away from an employer match often feels like leaving money on the table.

And there’s another catch people often miss:

Once you become an EPF member, you generally cannot simply exit later while continuing employment in a covered establishment.

Salary increases don’t automatically remove you.

Promotions don’t remove you.

Crossing the ceiling doesn’t remove you.

Once you’re in… you’re usually in.

As explained here, employees earning above the statutory ceiling at the time of joining may have a choice regarding EPF membership, but that choice usually becomes effectively irreversible during that employment.

Which makes the joining decision more important than many employees realise.

Understanding Section 26(6) of the EPF Act

This is where the law gets a little more technical.

Section 26(6) of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 governs voluntary EPF membership for employees who would otherwise fall outside mandatory coverage.

In simple terms:

If your salary exceeds the wage ceiling and you qualify as an excluded employee, you can still choose to join EPF—provided your employer agrees.

That’s what Section 26(6) allows.

So an employee earning above ₹25,000 under the proposed ceiling could still voluntarily participate in EPF.

Why would someone do that?

A few reasons:

- Employer matching contributions

- Stable, government-backed returns

- Tax advantages

- Long-term retirement discipline

Not flashy benefits. But powerful over time.

There’s also the pension angle.

If you voluntarily contribute on higher wages, your EPF contributions may rise—but your EPS pensionable salary may still remain subject to the statutory ceiling unless additional higher pension options apply.

And that’s where things get… nuanced.

Especially after the Supreme Court’s November 2022 higher pension judgment and the EPFO circulars that followed.

Employees who contributed on higher salaries before September 2014 may have rights or options that newer members don’t automatically have.

It’s one of those areas where the law, payroll practice, and litigation history all intersect.

Messy. But important.

For updated circulars and notifications on this subject, see here .

What happens if my basic salary crosses the limit?

This one creates a lot of confusion.

Here’s the short version:

Nothing happens automatically.

If you’re already an EPF member and your basic salary later rises beyond ₹25,000…

You stay an EPF member.

You don’t get auto-exited.

You don’t suddenly become exempt.

You don’t get a refund or an opt-out form.

Your EPF membership continues.

Your contributions are typically calculated using the statutory ceiling (₹25,000, if the proposal becomes law), unless you and your employer choose to contribute on actual higher wages voluntarily.

So:

Salary goes up.

Membership stays.

Simple.

Now if you’re not yet an EPF member, and you join a company with a basic salary above ₹25,000…

That’s where the choice comes in.

You may be able to decline EPF membership at joining.

But before doing that, it’s worth thinking carefully.

Because opting out doesn’t just reduce deductions.

It may also mean walking away from:

- Employer matching contributions

- Pension accumulation

- Tax-efficient retirement savings

Sometimes flexibility wins.

Sometimes guaranteed compounding wins.

Depends on the person. Depends on the stage of life.

And honestly, that’s what makes this one of the most strategic decisions in the entire EPF conversation.

High Earners’ Dilemma: EPF vs. NPS in 2026

For employees earning well above the proposed ₹25,000 EPF ceiling, the conversation eventually shifts.

It stops being about mandatory deduction and starts becoming about strategy.

Because once your salary moves into higher brackets—₹50,000 basic, ₹80,000, ₹1 lakh or more—the statutory EPF contribution becomes a relatively small slice of your overall income.

At that point, the real question isn’t:

“How much PF am I paying?”

It becomes:

“Where should the rest of my retirement money go?”

And in 2026, for a lot of salaried professionals, that decision usually comes down to two familiar options:

EPF (and optionally VPF)

vs.

NPS (National Pension System)

Both offer tax benefits. Both are designed for retirement. Both have loyal supporters.

But they work very differently once you get into the details.

And for high earners, those differences matter—a lot.

Tax Efficiency: Section 80C vs. Section 80CCD(1B)

This is usually where people start comparing the two.

Not returns. Not flexibility.

Taxes.

Fair enough.

Because for many salaried employees, tax efficiency is what pushes retirement planning from “I’ll do it later” to “Okay, let’s actually set this up.”

According to this guide, the 2026 tax framework largely keeps existing retirement tax benefits intact.

So, let’s break it down.

EPF (Under the Old Tax Regime)

EPF continues to offer what’s often called EEE treatment—Exempt, Exempt, Exempt.

Meaning:

- Contributions qualify for deduction under Section 80C (within the ₹1.5 lakh cap)

- Interest earned remains tax-efficient, subject to existing limits

- Withdrawals after 5 years of continuous service generally remain tax-free

Employer contributions up to statutory limits also continue to enjoy favorable tax treatment.

And if you contribute extra through VPF, that too generally falls within the same 80C umbrella.

Solid. Predictable. Familiar.

But there’s a limitation.

For most higher earners, the ₹1.5 lakh 80C limit gets exhausted fast.

PF, life insurance, ELSS, principal repayment, tuition fees… it all piles into the same bucket.

Which means extra EPF contributions don’t always create extra tax advantage.

NPS (National Pension System)

This is where NPS gets interesting.

NPS offers:

- Deduction under Section 80CCD(1) within the broader 80C framework

- Plus an additional ₹50,000 exclusive deduction under Section 80CCD(1B)

That second benefit is what grabs attention.

Because it sits outside the normal 80C cap.

Meaning even if your entire ₹1.5 lakh 80C bucket is already full, NPS still gives you another tax-saving window.

That’s a big deal for higher-income professionals.

At a 30% tax bracket, a ₹50,000 NPS contribution could save roughly ₹15,000 in taxes annually.

No complicated hacks. Just clean tax efficiency.

As reported here, the government has retained this structure in 2026, making NPS one of the more underutilised retirement tax tools for salaried employees.

And honestly, a lot of people still ignore it.

Fixed Returns (EPF) vs. Market-Linked Growth (NPS)

This is where numbers stop being purely tax-driven and start becoming personal.

Because EPF and NPS are built on completely different philosophies.

EPF: Stability First

EPF is built for people who value predictability.

Its biggest strengths:

- Government-backed framework

- Historically stable returns (currently around 8.25%, as per EPFO)

- No market volatility

- Full capital protection

- Tax-efficient maturity

There’s also something quietly powerful about forced investing.

Money leaves your salary before you can spend it.

No temptation.

No timing the market.

No checking NAVs at midnight.

For many people, that discipline alone makes EPF incredibly effective.

Especially in your 40s and 50s, when preserving capital often matters more than chasing aggressive growth.

NPS: Growth Potential

NPS plays a different game.

Instead of fixed declared returns, it gives exposure to:

- Equity markets

- Corporate bonds

- Government securities

That means:

More upside.

More volatility.

More uncertainty.

Historically, equity-heavy NPS allocations have delivered higher long-term returns than EPF in many periods—sometimes in the 12–14% range over long horizons.

But of course…

Markets don’t move in straight lines.

Some years feel brilliant.

Some years feel… less brilliant.

That’s the tradeoff.

NPS also comes with withdrawal restrictions:

- Up to 60% can typically be withdrawn as a lump sum at maturity (tax-efficient)

- The remaining 40% usually goes toward annuity purchase

So yes, you get growth potential.

But you also give up some flexibility.

So Which Makes More Sense in 2026?

For most high earners, it’s probably not an EPF or NPS decision.

It’s usually EPF and NPS.

That combination often works better than picking sides.

A practical pattern many financial planners lean toward:

If you’re under 35:

You probably have time on your side.

That often makes NPS—especially equity-oriented allocation—more attractive alongside mandatory EPF.

You can afford volatility.

You can recover from bad market years.

You can let compounding do its thing.

If you’re above 50:

The equation changes.

Retirement gets closer.

Capital protection starts feeling less theoretical and more… important.

That’s where EPF’s stability often becomes more valuable.

Less excitement.

More predictability.

Sometimes boring wins.

There’s also another layer to watch in 2026.

The new labour code’s 50% wage rule—which requires at least half of total remuneration to qualify as wages for social security calculations—could independently increase EPF contributions for many employees.

That means some high earners may see PF contributions rise from two directions at once:

- Higher wage ceiling

- Higher wage base

As discussed here, the combined impact could materially alter salary structuring across sectors.

And for employees also managing professional tax obligations across states, this reference remains useful:

Because at higher income levels, retirement planning is rarely about just one deduction.

It’s about how the whole system fits together.

Messy spreadsheets and all.

Frequently Asked Questions (FAQ): PF ceiling limit for 2026

The government is moving to revise the PF ceiling limit for 2026, shifting the statutory wage threshold from ₹15,000 to ₹25,000 per month. This policy update, driven by Supreme Court directives and inflation adjustments, marks the first major expansion of mandatory social security coverage since 2014.

If your basic salary is above ₹15,000, the revised PF ceiling limit for 2026 will likely increase your mandatory monthly PF deduction, which directly reduces your take-home pay. For example, calculating the 12% employee contribution on ₹25,000 instead of ₹15,000 results in an additional ₹1,200 deducted from your monthly in-hand salary, unless your employer restructures your CTC.

The PF ceiling limit for 2026 acts as an entry threshold. If your basic salary exceeds ₹25,000 at the exact time you join a new company, you can legally opt out as an “excluded employee.” However, if you are already an active EPF member, you cannot exit the system, even if your salary subsequently crosses the new ceiling.

While short-term liquidity drops, the new PF ceiling limit for 2026 significantly boosts your retirement benefits. Because the Employer’s Pension Scheme (EPS) contribution is capped at the statutory limit, raising it to ₹25,000 allows for a higher pensionable salary base, which can increase your maximum monthly pension calculation by over 60% upon retirement.

Yes. For employers, the PF ceiling limit for 2026 means higher compliance costs across the board. Because EDLI (0.5%) and administrative charges (0.5%) are calculated on the wage ceiling, an increase to ₹25,000 means companies will pay a higher absolute amount per employee, every month, requiring immediate payroll budget recalculations.

PF Ceiling Impact Analysis

| Component | Current Scenario (₹15,000 Ceiling) | Proposed 2026 Scenario (₹25,000 Ceiling) | Change / Delta |

| Statutory Wage Ceiling | ₹15,000 | ₹25,000 | +₹10,000 |

| Employee Contribution (12%) | ₹1,800 | ₹3,000 | +₹1,200 |

| Employer EPF (3.67%) | ₹550.50 | ₹917.50 | +₹367.00 |

| Employer EPS (8.33%) | ₹1,249.50 | ₹2,082.50 | +₹833.00 |

| Total Monthly Contribution | ₹3,600 | ₹6,000 | +₹2,400 |

| Annual Accumulation | ₹43,200 | ₹72,000 | +₹28,800 |

| EDLI & Admin Charges (1%) | ₹150 (75+75) | ₹250 (125+125) | +₹100 |

| Estimated 30-Year Corpus* | ~₹58.5 Lakhs | ~₹97.5 Lakhs | +₹39 Lakhs |

*Assumes an illustrative 8.25% average interest rate and continuous service.

What You Should Do Right Now

The proposed jump from a ₹15,000 EPF wage ceiling to ₹25,000 isn’t just another compliance update buried in a policy circular.

If this gets formally notified—and all signs suggest that it eventually will—it could become one of the biggest shifts in India’s retirement savings framework in over a decade.

And like most financial policy changes, the impact won’t be evenly felt.

For some employees, it’ll show up as a slightly smaller salary credit every month.

For others, it could mean a significantly stronger retirement corpus, better pension potential, and a more meaningful long-term safety net.

For employers? It means higher contribution costs, payroll restructuring, and compliance work that probably nobody was excited to inherit.

Still… whether you like the change or not, the direction seems pretty clear.

India’s social security framework is moving toward broader coverage, higher wage recognition, and stronger retirement contributions.

The real question now isn’t whether the change matters.

It’s whether you’re prepared before it lands.

For Employees

If you’re salaried, this is a good moment to stop treating PF as that deduction you glance at once a month and ignore.

Actually run the numbers.

Ask:

- How much will your monthly EPF deduction increase if the ceiling moves to ₹25,000?

- How much does that affect your take-home salary?

- If you’re under the old tax regime, how much of that gets offset through Section 80C tax savings?

- If you’re already maxing out 80C, should you start looking at NPS to use the additional ₹50,000 deduction under Section 80CCD(1B)?

And if retirement is less than 10 years away, don’t ignore the EPS side of this.

That pension uplift may matter more than you think.

For HR and Payroll Teams

This is not something to react to after the notification hits your inbox.

Preparation now saves chaos later.

Practical steps:

- Review whether your payroll platform is ready for a statutory ceiling change

- Identify employees in the ₹15,001–₹25,000 salary band—they’re likely to be affected first

- Model the employer cost impact across your workforce

- Prepare internal communication templates before revised payslips create confusion

- Audit existing CTC structures to see whether salary redesign becomes necessary

And keep watching the EPFO Unified Portal and Ministry of Labour notifications for the final gazette announcement.

Because when payroll changes hit, employees don’t usually wait quietly for explanations.

They notice.

Fast.

For Employers (Strategic Planning)

If you’re running workforce planning or finance strategy, the ceiling hike shouldn’t be treated as just a payroll event.

It’s a compensation strategy event.

Questions worth asking now:

- Will your organisation absorb the increased employer contribution—or restructure CTC?

- Do existing salary models still make sense under both the higher wage ceiling and potential labour code wage definitions?

- Does your current employee benefits strategy still hold up if EDLI and PF costs increase?

- Should voluntary retirement options like VPF or NPS education be offered more actively to employees?

And for companies managing large employee populations, even small per-head increases can quietly turn into major annual budget shifts.

A few hundred rupees per employee doesn’t sound like much…

Until you multiply it by 2,000.

Then finance notices.

Very quickly.

The ₹25,000 EPF shift feels less like a new policy, and more like a correction that probably should have happened years ago.

Its real effects won’t play out overnight.

They’ll unfold gradually in salary slips, pension calculations, employer budgets, and retirement balances built over decades.

Which means the smartest move right now isn’t panic.

It’s preparation.

For continuing updates and official guidance, keep an eye on here

and the official EPFO website.

Disclaimer

This article is intended for informational purposes only and does not constitute financial or legal advice. Readers should consult a qualified financial advisor or legal professional for guidance specific to their situation. All figures relating to the proposed ₹25,000 ceiling are based on publicly reported proposals as of mid-2026 and are subject to official government notification.

Discussion (4)

Leave a Reply