Health Insurance Claim Rejected? How to Escalate to the Insurance Ombudsman

The 4-Stage Grievance Process for Rejected Health Insurance Claims

A rejected health insurance claim rarely comes with a clear roadmap. Instead, you’re likely to receive a rejection letter quoting a policy clause, a settlement that falls well short of your hospital bill, or, in some cases, no meaningful response even after weeks of follow-up. What many policyholders don’t realise is that India has a structured, free, four-stage grievance process designed specifically for situations like this. Missing a step in that process is one of the most common reasons even legitimate complaints fail to move forward.

This guide explains the escalation process in the same order regulators expect you to follow it. You’ll start by understanding exactly why your claim was rejected, then raise the matter with your insurer’s Grievance Redressal Officer (GRO). If that doesn’t resolve the issue, the next step is to register your complaint on IRDAI’s Bima Bharosa portal before approaching the Insurance Ombudsman. The Ombudsman functions as a quasi-judicial authority and can award compensation of up to ₹50 lakh, without charging any fee. Each stage has its own documentation requirements, timelines, and eligibility rules. Missing even one of them can send your complaint back to the beginning.

The good news is that none of these four stages requires you to hire a lawyer or pay a filing fee. The framework exists because disputes over health insurance claims shouldn’t force policyholders into expensive and time-consuming litigation. What it does demand, however, is careful attention to procedure. Filing the right documents, approaching the correct authority, and staying within the prescribed timelines can make the difference between a rejected claim remaining closed and one that is ultimately settled in your favour.

At A Glance: Health Insurance Claim Rejected?

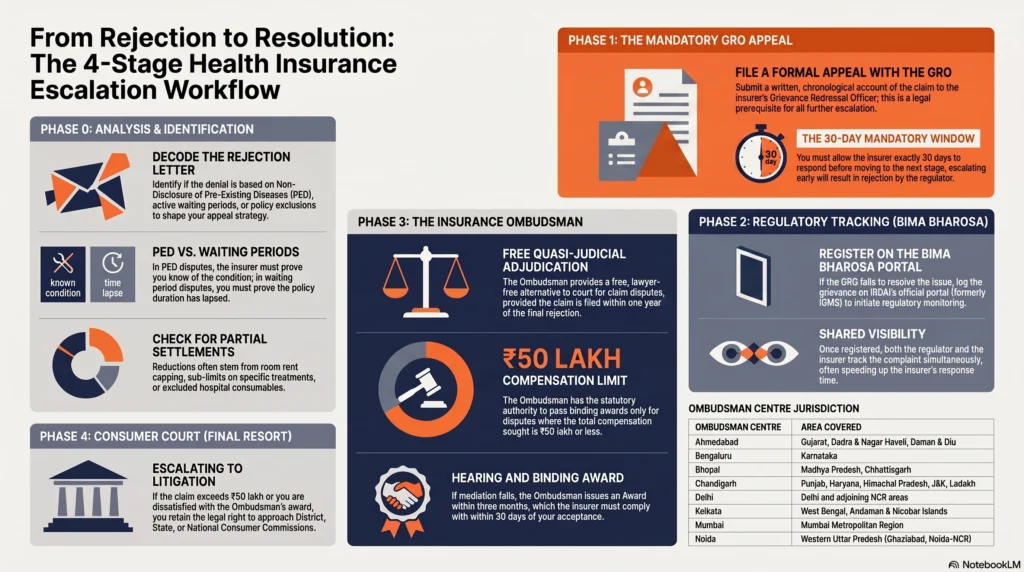

Identify the Rejection Reason: Carefully review your denial letter to determine if the claim was rejected due to non-disclosure of pre-existing diseases (PED), active waiting periods, or policy sub-limits.

Step 1: Contact the GRO: Submit a formal, chronological appeal to your insurer’s Grievance Redressal Officer (GRO) and observe the mandatory 30-day response window.

Step 2: Register on Bima Bharosa: If the GRO fails to resolve the issue, log your grievance on the official IRDAI Bima Bharosa portal to initiate regulatory tracking.

Step 3: Approach the Insurance Ombudsman: File a 100% free online complaint for claim disputes up to ₹50 lakh, ensuring you apply within one year of the insurer’s final rejection.

Step 4: Escalate to Consumer Courts: If you are dissatisfied with the Ombudsman’s binding award, you retain the legal right to challenge the decision in a Consumer Court.

Understanding Why Your Health Insurance Claim Was Rejected

Before you draft an appeal, take the time to understand exactly why your claim was turned down. That reason will shape every step that follows. A successful escalation isn’t built on the belief that the insurer acted unfairly. It’s built on addressing the specific grounds on which the claim was rejected.

Analyzing the Rejection Letter and Standard Clauses

Your rejection or repudiation letter is the foundation of your case. Insurers are required to provide a written reason for denying a claim, and that explanation tells you where to focus your response. As Axis Max Life advises, your first step should be to read the letter carefully and identify whether the issue stems from missing documents, a disagreement over policy coverage, or a genuine policy exclusion. Each scenario calls for a different approach, as explained in this guide.

It’s equally important to understand the kinds of disputes that can be formally challenged. According to the Council for Insurance Ombudsmen’s FAQs, complaints can relate to delays in claim settlement beyond the timelines prescribed by IRDAI, partial or complete claim repudiation, premium disputes, misrepresentation of policy terms, disagreements over how policy provisions should be interpreted, policy servicing issues, policies issued differently from what was originally proposed, or cases where a policy wasn’t issued despite payment of the premium.

As soon as you receive the rejection letter, check these two points carefully:

- Does the letter mention a specific policy clause? If it cites an exact clause number, you’ll have a clear basis for your response. If it simply refers to “terms and conditions” without identifying the relevant provision, that lack of specificity may itself become part of your appeal.

- Is the communication a final rejection or only an interim response? This distinction matters because the one-year deadline for approaching the Insurance Ombudsman starts from the insurer’s final rejection, not from an earlier query or provisional communication. Consumer advocate Jehangir Gai highlighted this during a Moneylife Foundation programme, noting that many policyholders unintentionally lose valuable time by calculating the limitation period from the wrong date. More details are available here.

Also Read: The 2026 Guide to 100% FDI in the Indian Insurance Sector: A Complete Policyholder Impact Analysis

Non-Disclosure of Pre-Existing Diseases (PED) vs. Waiting Periods

These two reasons for claim rejection are often confused, even though they involve very different issues and require different responses.

| Non-Disclosure of PED | Claim During Waiting Period |

| What the insurer is saying: “You knew about this condition before buying the policy but didn’t disclose it.” | What the insurer is saying: “You disclosed the condition, but the waiting period under your policy hadn’t ended.” |

| What decides the outcome: Whether the insurer can establish that the condition existed and was known before the policy was purchased. | What decides the outcome: The waiting period specified in your policy schedule. |

| Where the burden lies: The insurer must support its allegation of non-disclosure with evidence. | Where the burden lies: You need to demonstrate that the applicable waiting period had already expired. |

| Your first step: Ask the insurer to provide the medical records or evidence supporting its allegation. | Your first step: Check your policy dates and verify whether the waiting period had actually lapsed before hospitalisation. |

Among the two, non-disclosure disputes tend to be more contentious. Moneylife highlighted one such case involving a bank-linked group health insurance policy, where the disagreement centred on how the insurer interpreted IRDAI’s definition of a pre-existing disease. According to the report, some insurers have relied on stricter interpretations than the regulator’s standard definition, resulting in claims being rejected even where the medical condition had been resolved years earlier and the policy itself contained no clear exclusion.

Jehangir Gai also points out that insurers sometimes reject claims over technical or procedural issues, including relatively minor documentation delays. He notes that once a policy has been issued and renewed, its terms cannot be changed unilaterally by the insurer. Any modification requires the policyholder’s consent. His observations are available here.

In practical terms, your appeal should reflect the reason for rejection. If the insurer alleges non-disclosure, ask it to provide the medical evidence and dates supporting that allegation. If the rejection is based on a waiting period, focus on the policy commencement date, the relevant waiting-period clause, and the date of hospitalisation. Often, the timeline itself resolves the dispute.

Partial Settlements: Sub-limits, Consumables, and Room Rent Capping

Not every disagreement involves a complete rejection. In many cases, the insurer approves the claim but settles it for significantly less than the hospital bill. When that happens, your policy schedule becomes just as important as the settlement letter. Three of the most common reasons for reduced payouts are:

Room rent capping

If your policy limits the daily room rent and you choose a room that exceeds that limit, the insurer may apply proportionate deductions across several parts of the bill, including surgeon’s fees and procedure charges, rather than deducting only the excess room rent.

Sub-limits

Certain treatments or expenses, such as cataract surgery, specific implants, or ambulance charges, may have individual caps regardless of your overall sum insured. These limits can significantly reduce the final payout even when your coverage amount has not been exhausted.

Consumables

Items such as gloves, syringes, masks, and other disposable hospital supplies are commonly excluded unless your policy specifically includes consumables coverage through a rider or additional benefit.

Axis Max Life recommends obtaining the insurer’s reasoning in writing and comparing each deduction with the wording of your policy before deciding whether to challenge it. A deduction based on a correctly applied policy limit is very different from one resulting from an incorrect interpretation of the policy terms. More guidance is available in this guide.

Also Read: Ayushman Bharat for Gig Workers 2026: Enrolment Guide

Step 1: The Mandatory First Escalation to the Grievance Redressal Officer (GRO)

Everything that follows in the escalation process, whether it’s Bima Bharosa, the Insurance Ombudsman, or even a consumer court, depends on this first formal complaint. Think of it as the foundation of your case. It shows that you gave your insurer a fair opportunity to review and resolve the dispute before taking it to an external authority. If you skip this step or rely only on phone calls with no written record, you’ll almost certainly be asked to return here before your complaint can move forward.

Why You Cannot Bypass the Insurer’s Internal Grievance Cell

It’s understandable to want to approach the regulator or the Insurance Ombudsman immediately after receiving what feels like an unfair rejection. Unfortunately, the process doesn’t work that way. The Council for Insurance Ombudsmen requires policyholders to first raise the issue with the insurer itself. You become eligible to approach the Ombudsman only if the insurer either fails to respond within the prescribed period or provides a response that you find unsatisfactory, as explained by the Ombudsmen.

This requirement exists because every insurer is legally required to maintain an internal grievance redressal mechanism. The General Insurance Council explains that IRDAI mandates all insurers to have a board-approved grievance redressal policy and appoint a designated Grievance Redressal Officer (GRO). The GRO’s contact details must appear in policy-related communications, and complaints are tracked through the regulator’s grievance management system .

In other words, this isn’t a procedural formality you need to complete before the “real” escalation begins. It’s a mandatory step that opens the door to every remedy that follows.

How to Find Your Insurer’s GRO Contact Information

In most cases, your insurer has already provided the information you need. The GRO’s name, email address, and contact details are usually printed in your policy document, often on the first page or in the claims section. They should also appear in the claim rejection letter.

If you can’t find them, don’t worry. According to the General Insurance Council, the official email addresses of every insurer’s Grievance Redressal Officer are also available through IRDAI’s consumer portal, policyholder.gov.in.

One important point to remember is that IRDAI expects this initial complaint to come directly from the policyholder or claimant. Complaints submitted at this stage through an agent, advocate, or another third party generally aren’t entertained.

If you’ve misplaced your policy documents, visit your insurer’s website and look for sections titled “Grievance Redressal” or “Contact Us.” Insurers are required to keep this information accessible and up to date. You can also email customer support requesting that your grievance be forwarded to the GRO. Doing so not only reaches the right department but also creates a written record of your communication, which you’ll need if the dispute escalates later.

Drafting a Factual, Chronological Appeal Letter

The appeal you send to the GRO becomes the cornerstone of your entire case. Every subsequent authority, whether it’s Bima Bharosa or the Insurance Ombudsman, may refer back to this document. That makes clarity far more important than emotion.

Axis Max Life recommends explaining why you believe the claim was wrongly rejected, mentioning your policy number and claim ID, attaching all relevant supporting documents, and maintaining a courteous but firm tone throughout.

You can make your appeal even stronger by following a few practical principles:

- Start with a timeline. List the key dates, including when you purchased the policy, the date of hospitalisation, when you informed the insurer, when you submitted the claim, and when you received the rejection. Establishing the sequence of events first makes the rest of your case easier to follow.

- Address the insurer’s reasoning directly. If the rejection refers to a particular policy clause, respond specifically to that clause instead of making broad statements about unfair treatment.

- Clearly state the outcome you’re seeking. Whether you’re requesting full settlement, reconsideration of a deduction, or recalculation of a partial payout, spell it out. A precise request gives the insurer a clear opportunity to resolve the dispute.

- Keep copies of everything. Save your appeal, all supporting documents, email acknowledgements, courier receipts, and any proof showing when your complaint was submitted. These records become mandatory supporting documents if you later register your complaint with Bima Bharosa or the Insurance Ombudsman.

The Strict 30-Day Mandatory Waiting Period

Once you’ve submitted your written complaint to the GRO, the next step is simply to wait. The insurer must be given an opportunity to respond before you can move the dispute to the next level.

The Council for Insurance Ombudsmen makes this requirement explicit. You can escalate your complaint only if the insurer either does not respond within one month of receiving your complaint or sends a response that you consider unsatisfactory.

As soon as you send your complaint, record the submission date and calculate the 30-day deadline. That date effectively determines when the rest of the escalation process becomes available. Missing it won’t usually hurt your case, but trying to escalate before it arrives almost certainly will.

Step 2: Registering the Dispute on the Bima Bharosa (IGMS) Portal

If your insurer doesn’t resolve the complaint within 30 days, or responds in a way that doesn’t address your concerns, it’s time to move to the next stage. Rather than approaching the Insurance Ombudsman immediately, you should first register your grievance on IRDAI’s Bima Bharosa portal. This allows the regulator to monitor how your insurer is handling the complaint before the matter progresses to a formal adjudication.

What is the Bima Bharosa Portal?

Bima Bharosa is IRDAI’s official online grievance management platform. If you’ve come across references to IGMS (Integrated Grievance Management System), don’t be confused. Bima Bharosa is simply the updated version of the same system. According to the portal itself, it was introduced to monitor insurers’ compliance with policyholder protection timelines while creating a central database of insurance-related grievances across the industry.

Bimabazaar’s explanation of the platform also highlights an important point. Policyholders are expected to first use the insurer’s own grievance mechanism before turning to Bima Bharosa. The portal is intended to strengthen the existing complaint process, not replace it.

In practical terms, Step 1 and Step 2 work together. Your complaint to the GRO creates the formal record, while Bima Bharosa gives IRDAI visibility into how the insurer is responding.

Transitioning Your Complaint to the IRDAI Dashboard

Once your complaint is registered on Bima Bharosa, it doesn’t remain with the regulator alone. As Bimabazaar explains, the complaint is also routed to the insurer’s grievance system, allowing both IRDAI and the insurer to track the same case simultaneously.

This shared visibility encourages insurers to address complaints more promptly because the regulator can monitor response times and progress throughout the process.

In many cases, policyholders receive the first substantive update within about two weeks of registering the complaint. If the issue still isn’t resolved, or the insurer’s response remains unsatisfactory, you can proceed to the next stage by approaching the Insurance Ombudsman.

One important warning is worth remembering. The official Bima Bharosa portal never asks policyholders to make payments, scan QR codes, or click links to receive settlements. Anyone claiming otherwise is attempting to defraud you. Compensation is never released through unofficial payment requests or third-party links.

Tracking the Status of Your Grievance Online

After registering your complaint, you’ll receive a reference or token number by email. Keep this number safely. You’ll use it to track your complaint, communicate with IRDAI, and support any future escalation to the Insurance Ombudsman.

If you prefer not to rely solely on the online portal, IRDAI’s Grievance Call Centre (IGCC) can also provide updates and answer questions about your complaint. You can contact the helpline on 155255 or 1800 4254 732, or email complaints@irdai.gov.in for assistance.

Finally, be cautious when searching online. Several unofficial websites closely resemble the official Bima Bharosa portal and use similar wording, but they are not operated by IRDAI. Always verify that you’re using the official bimabharosa.irdai.gov.in website before entering your personal information, policy details, or KYC documents. If the web address is different, leave the site and access the official portal directly.

Step 3: Approaching the Insurance Ombudsman

For many policyholders, this is the stage they associate with formally challenging a rejected insurance claim. Unlike the earlier stages, which focus on resolving the issue directly with the insurer and the regulator, the Insurance Ombudsman functions as an independent, quasi-judicial authority. Before you begin preparing your documents, however, it’s important to make sure your complaint meets all the eligibility requirements. A well-prepared application can save you from unnecessary delays later.

What is the Insurance Ombudsman and What is Their Authority?

If your complaint remains unresolved after going through Bima Bharosa, the Insurance Ombudsman becomes the next avenue for redress. The Ombudsman operates under the administrative control of the Council for Insurance Ombudsmen (CIO) and functions under the Insurance Ombudsman Rules. Its purpose is to provide policyholders with a faster, simpler, and more affordable alternative to court proceedings for resolving disputes with insurers, agents, and intermediaries.

The current framework is governed by the Insurance Ombudsman Rules, 2017, which replaced the earlier system established under the Redressal of Public Grievances Rules, 1998. The General Insurance Council explains that these rules define how Ombudsman offices operate and how complaints are handled.

Although many people approach the Ombudsman after a claim rejection, its jurisdiction extends well beyond outright denials. According to the Council for Insurance Ombudsmen, the Ombudsman can also hear complaints involving delays in claim settlement, partial settlements, premium disputes, incorrect interpretation of policy terms, deficiencies in policy servicing, and cases where the policy issued differs from what the customer originally applied for.

Mandatory Eligibility: The 1-Year Time Limit and ₹50 Lakh Cap

Before you file your complaint, take a few minutes to confirm that you satisfy all the eligibility conditions. According to the Council for Insurance Ombudsmen, your complaint must meet each of the following requirements:

- You have already submitted a formal complaint to the insurer or broker.

- The insurer either failed to respond within one month or provided a response that you consider unsatisfactory.

- You are filing your complaint within one year from either the insurer’s final rejection or the expiry of the one-month response period if no reply was received.

- The total compensation you’re seeking, including any associated expenses, does not exceed ₹50 lakh.

- The same dispute is not already pending before, or decided by, a court, consumer commission, or arbitrator.

You can review the complete eligibility criteria here.

One condition deserves particular attention. The Ombudsman cannot entertain claims exceeding ₹50 lakh. If the value of your dispute is higher than this limit, you’ll need to pursue the matter through the appropriate consumer commission or another legal forum instead.

It’s also worth noting that filing a complaint with the Insurance Ombudsman is completely free. The Council clearly states that policyholders are not required to pay any fee at any stage of the process.

Determining Territorial Jurisdiction Across the 17 Centres

Your complaint must be filed with the Ombudsman office that has jurisdiction over either your residential address or the insurer’s branch office involved in the dispute. Before filing, the Council for Insurance Ombudsmen recommends checking the official jurisdiction list to identify the correct office.

The Department of Financial Services lists 17 Insurance Ombudsman Centres across India, covering different states and union territories. A separate desk in Thane handles part of the Mumbai Metropolitan Region, which is why some sources occasionally refer to 18 offices.

| Ombudsman Centre | Broad area typically covered |

| Ahmedabad | Gujarat, Dadra & Nagar Haveli, Daman & Diu |

| Bengaluru | Karnataka |

| Bhopal | Madhya Pradesh, Chhattisgarh |

| Bhubaneswar | Odisha |

| Chandigarh | Punjab, Haryana, Himachal Pradesh, Jammu & Kashmir, Ladakh, Chandigarh |

| Chennai | Tamil Nadu, Puducherry (excluding Mahe) |

| Delhi | Delhi and adjoining NCR areas |

| Guwahati | Assam and the North-Eastern states |

| Hyderabad | Telangana, Andhra Pradesh |

| Jaipur | Rajasthan |

| Kochi | Kerala, Lakshadweep and Mahe (Puducherry) |

| Kolkata | West Bengal and the Andaman & Nicobar Islands |

| Lucknow | Central and Eastern Uttar Pradesh, including Lucknow, Kanpur and Varanasi |

| Mumbai | Mumbai and the wider Mumbai Metropolitan Region |

| Noida | Western Uttar Pradesh, including Ghaziabad and the Noida-NCR region |

| Patna | Bihar and Jharkhand |

| Pune | Maharashtra, excluding the Mumbai Metropolitan Region |

This table serves as a general guide. District-level jurisdiction can occasionally change, so it’s always a good idea to verify the correct office on the CIO website before submitting your complaint.

If you’re still unsure which office has jurisdiction, file with the one closest to your residential address. Complaints submitted to the wrong office are generally transferred internally instead of being rejected outright.

The Exact Process to File an Ombudsman Complaint Online

Once you’ve confirmed that you’re eligible and identified the correct Ombudsman office, the actual filing process is fairly straightforward. If you’ve already organised your documents, most people can complete the online application in less than 30 minutes.

Preparing Mandatory Documents (Policy, Rejection Letter, KYC)

Before opening the online form, gather all the required documents. According to the Council for Insurance Ombudsmen, you’ll typically need:

- A copy of the complaint you submitted to the insurer or broker.

- The insurer’s rejection letter or email.

- Valid KYC documents such as your Aadhaar card, PAN card, driving licence, or another accepted identity proof.

- A copy of your insurance policy.

- A recent passport-sized photograph.

- Any additional correspondence or documents that support your complaint.

The complete checklist is available here.

If your claim was rejected because of alleged non-disclosure or a waiting-period issue, it’s also helpful to keep copies of any earlier health insurance policies covering the same insured person. These documents may help establish continuity of coverage if questions arise during the proceedings.

One simple habit can save considerable time later. Scan or photograph each document separately and give every file a clear name, such as Policy Copy, Claim Rejection Letter, KYC, or Hospital Records. Organised files make the upload process much smoother.

Navigating the CIOINS Website for Online Registration

The online filing process involves four basic steps:

- Visit www.cioins.co.in and select “Register Complaint” under the “Complaint Online” section.

- Complete the online form with your personal details, policy information, claim details, and a clear description of your grievance. You’ll also need to select the Ombudsman office that has jurisdiction over your complaint.

- Upload the required supporting documents.

- Review the information carefully before submitting your application.

The Council outlines this process in detail.

If online filing isn’t convenient, you can also submit your complaint by post, email, or by visiting the appropriate Ombudsman office in person. The online route is simply the quickest and most convenient option for most policyholders.

Verifying the Complaint via OTP and Generating the Application Number

After you submit the form, you’ll receive a one-time password (OTP) on your registered mobile number. Once you enter the OTP successfully, the system generates a complaint reference number immediately.

Keep this application number safe. You’ll need it to monitor the status of your complaint and for any future communication with the Ombudsman’s office.

It’s worth storing this reference alongside your Bima Bharosa token number and your insurer’s claim reference. Having all three numbers readily available makes future correspondence much easier.

What to Expect During the Ombudsman Hearing and Resolution

Once your complaint has been registered, the focus shifts from filing documents to resolving the dispute. In most cases, the process follows one of two paths. The Ombudsman may first try to help both parties reach a mutually acceptable settlement. If that doesn’t happen, or if no agreement is possible, the matter proceeds to a formal decision. Both stages are governed by specific timelines, giving policyholders a clearer idea of what to expect.

Presenting Your Case: Why You Do Not Need a Lawyer

One of the biggest advantages of the Insurance Ombudsman process is that you don’t need legal representation to pursue your complaint. In fact, the Council for Insurance Ombudsmen states that the Insurance Ombudsman Rules, 2017 do not provide for engaging a lawyer during these proceedings.

The system is designed to be accessible to ordinary policyholders. Your case is built primarily on the documents you’ve already gathered, including your complaint to the GRO, the insurer’s response, your policy document, medical records, and any supporting correspondence.

If the Ombudsman decides that a hearing is necessary, it may be conducted either in person or through video conferencing. Depending on the circumstances, hearings can also be held at locations other than the Ombudsman’s main office, provided they fall within that office’s territorial jurisdiction.

The emphasis throughout the process is on facts and documentation rather than legal arguments. A clear timeline and well-organised records usually carry far more weight than lengthy submissions.

Stage 1: Attempting Mutual Agreement and Recommendations

Before issuing a formal decision, the Ombudsman generally tries to resolve the dispute through conciliation or mediation. The objective is to help both the policyholder and the insurer reach a mutually acceptable settlement without the need for a formal award.

If both parties agree to this approach, the Ombudsman is required to issue a Recommendation within one month of receiving written consent from both sides to participate in mediation.

This stage is often quicker and less adversarial than a formal adjudication. It also gives both parties an opportunity to settle the dispute without extending the process further.

That said, mediation is voluntary. Neither you nor the insurer can be compelled to participate or accept a proposed settlement. If mediation isn’t attempted, or if it fails to resolve the issue, the Ombudsman moves on to the next stage and issues a formal decision.

Stage 2: The Formal Issuance of the Binding Award

If the dispute cannot be settled through mediation, the Ombudsman delivers a formal Award.

According to the Council for Insurance Ombudsmen, this Award must generally be issued within three months of receiving all the necessary documents and information from the complainant.

Once issued, the Award is binding on the insurer. The General Insurance Council also confirms that insurance companies are required to comply with the Ombudsman’s decision within the prescribed framework.

There are, however, two important limitations to keep in mind:

- The Ombudsman cannot direct insurers to make purely discretionary ex gratia payments that aren’t supported by the policy terms or the facts of the case.

- The total compensation awarded cannot exceed the Ombudsman’s statutory limit of ₹50 lakh.

In other words, the Award is based on the policy, applicable regulations, and the evidence presented. It isn’t intended to provide compensation outside those boundaries.

Timelines for Insurer Compliance and Final Payout

Once the Award has been issued, responsibility shifts back to the insurer.

The General Insurance Council states that insurers are expected to comply with the Award within 30 days of receiving it and must confirm their compliance to the Ombudsman.

IRDAI’s policyholder education portal adds another important step. After receiving the Award, the policyholder must communicate their acceptance if they agree to treat it as a full and final settlement. Once that acceptance is received, the Ombudsman informs the insurer, which is expected to comply with the accepted Award within 15 days.

From a practical perspective, it’s reasonable to expect the payment process to conclude within about 30 days of the Award, assuming there are no outstanding procedural requirements.

Post-Hearing Scenarios and Final Alternatives

Receiving an Ombudsman’s Award doesn’t necessarily bring your options to an end. What happens next depends on whether you’re satisfied with the outcome. If you accept the decision, the matter is concluded. If you don’t, there are still legal avenues available. Understanding those options helps you decide whether to close the dispute or take it further.

What Happens if You Reject the Ombudsman’s Award?

One of the biggest advantages of approaching the Insurance Ombudsman is that it doesn’t prevent you from pursuing other legal remedies later. If you’re satisfied with the Award and accept it as a full and final settlement, the dispute comes to an end. If you’re not, you still have the right to approach a consumer court or a civil court.

Ditto’s guide to the Ombudsman process explains that using this mechanism doesn’t take away your underlying legal rights. It simply gives you an opportunity to resolve the dispute through a faster and cost-free forum before considering litigation.

That said, you can’t pursue the same dispute before multiple forums at the same time. The Council for Insurance Ombudsmen makes it clear that it won’t entertain complaints that are already pending before, or have been decided by, a court, consumer commission, or arbitrator. The reverse principle also applies in practice. It’s generally advisable to complete one process before moving to another.

For most policyholders, this makes the Ombudsman an attractive first option. Filing a complaint costs nothing, requires relatively limited paperwork compared to court proceedings, and leaves your legal rights intact if the outcome isn’t satisfactory.

Frequently Asked Questions: Health Insurance Claim Rejected?

Before approaching any external regulatory authorities, you must first file a formal, written grievance directly with your insurer’s designated Grievance Redressal Officer (GRO). You cannot approach the Ombudsman without completing this mandatory internal step and allowing the standard 30-day response window to expire.

Policyholders must file their online complaint within a strict one-year time limit starting from the date of the insurer’s final rejection letter. If your insurance company entirely ignored your GRO complaint, this one-year countdown automatically begins immediately after your initial 30-day waiting period concludes.

The Insurance Ombudsman currently possesses the statutory authority to pass binding financial awards for claim disputes up to a maximum of ₹50 lakh. If your contested medical bill or settlement deficit exceeds this specific limit, you must escalate the matter directly to a Consumer Disputes Redressal Commission (Consumer Court).

No, the entire escalation process is 100% free of cost, and the rules explicitly state that you do not need a lawyer to represent you. The platform is designed specifically for everyday policyholders to present their own cases relying purely on factual documentation, such as the original policy schedule, hospital medical records, and the official repudiation letter.

Formerly known as the Integrated Grievance Management System (IGMS), Bima Bharosa is the official, centralized grievance tracking dashboard operated by the Insurance Regulatory and Development Authority of India (IRDAI). Registering your dispute on this platform forces the regulator to actively monitor your insurer’s response time before you escalate to the Ombudsman.

Escalating to Consumer Courts as a Last Resort

Many insurance disputes are resolved before they ever reach a consumer commission. However, there are situations where litigation becomes the more appropriate course of action.

You should consider approaching a consumer court if:

- Your claim exceeds ₹50 lakh, making it ineligible for the Insurance Ombudsman.

- You’re dissatisfied with the Ombudsman’s Award and want to pursue the matter further.

- You prefer a judicial process that allows appeals and results in a court order.

Consumer advocate Jehangir Gai has pointed out that while the Ombudsman process is generally quicker than litigation, proceedings before consumer commissions can take considerably longer, particularly after changes introduced under the Consumer Protection Act, 2019 (https://www.moneylife.in/article/insurance-claim-rejection-truth-jehangir-gai-explains-unfair-practices-and-what-policyholders-can-do/76179.html).

He also makes an encouraging observation. Many insurers expect policyholders to abandon their claims after an initial rejection. Simply following the prescribed grievance process and pursuing the available remedies often leads to disputes being resolved without the need for prolonged litigation.

India’s consumer dispute resolution system operates through multiple levels based on the value of the claim, beginning with the District Consumer Disputes Redressal Commission and progressing to the State and National Commissions for higher-value matters. Unlike the Ombudsman process, these proceedings involve formal pleadings, the possibility of appeals, and, if you choose, legal representation.

If your case ultimately reaches this stage, keep every document you’ve collected throughout the process. Your complaint to the GRO, the Bima Bharosa reference number, the Ombudsman application, the Award, and all supporting correspondence together form the documentary record that a consumer commission will expect to review.

Taken together, these four stages aren’t separate battles but successive steps in a single process. The complaint you submit to the Grievance Redressal Officer becomes supporting evidence on the Bima Bharosa portal. That same correspondence forms part of your Ombudsman application, and if the matter eventually reaches a consumer commission, the entire paper trail becomes part of your case. Treat every document as something you’ll need later, not just for the stage you’re currently in.

One final point deserves emphasis. The Council for Insurance Ombudsmen clearly states that it never charges policyholders any fee for filing complaints, never promises bonuses or special settlements, and never asks anyone to transfer money or scan QR codes to receive compensation. If someone claiming to represent the Ombudsman’s office asks you for payment or directs you to an unofficial payment link, treat it as a fraud attempt and report it rather than engaging further.

Disclaimer:

This article is for general informational purposes and reflects the escalation process as publicly described by the Council for Insurance Ombudsmen, IRDAI, and the General Insurance Council at the time of writing. It is not legal or financial advice. Monetary limits, timelines, and procedural rules are set by regulation and can change. Always confirm the current position on the official cioins.co.in and bimabharosa.irdai.gov.in portals, or with a qualified professional, before filing a complaint.

Discussion (1)

Leave a Reply