Women’s Business Loans in India (2026): Deconstructing MSME Credit Frameworks and Zero-Collateral Leverage

Women Entrepreneurs Driving India’s Economic Growth

India right now feels like it’s standing on the edge of something big; it’s one of those moments economists like to label with round numbers and ambition. The $5 trillion economy goal gets tossed around a lot. But somewhere beneath that headline figure sits a quieter, more stubborn reality: we’re still not fully tapping into the economic force of women entrepreneurs. Herein lies the need to explore the topic of business loans for women in India.

It’s a strange imbalance when you pause and think about it. Women make up nearly half the population, yet their visible footprint in formal business, and by extension, GDP, remains surprisingly small. Closing that gap isn’t just about fairness or representation anymore. It’s about growth. Plain and simple.

And the data doesn’t really let us look away. The Mastercard Index of Women Entrepreneurship (MIWE) ranked India 57th out of 65 nations, a number that lands a bit heavier than you’d expect. It captures something deeper than rankings usually do: the distance between intent and execution.

But here’s the flip side, and it’s a big one. There’s enormous upside still sitting on the table. Estimates suggest that if women-led enterprises are supported and scaled properly, they could generate anywhere between 150 and 170 million jobs. It’s not incremental, but it’s the kind of shift that quietly rewires an entire economy.

So the question isn’t whether women’s entrepreneurship matters. It’s what kind of entrepreneurship we’re actually building.

At a Glance: Women’s Business Credit in India (2025–26)

- The Goal: Empowering women-led enterprises (51%+ stake) with low-cost, collateral-free credit and end-to-end digital approval.

- Funding Spectrum: From ₹50,000 (Mudra Shishu) up to ₹10 Crore (CGTMSE-backed SME loans).

- Top Picks for 2025 (By Business Stage):

- Micro & Small (Existing): PMMY (Mudra) – Best for working capital. New: “Tarun Plus” category covers ₹10L – ₹20L for growing businesses.

- Greenfield (New Projects): Stand-Up India – Loans from ₹10 Lakh to ₹1 Crore for SC/ST or Women entrepreneurs setting up their first manufacturing, service, or trading unit.

- Expansion (SMEs): CGTMSE – Collateral-free guarantee cover now expanded up to ₹10 Crore (formerly ₹5 Cr) with reduced guarantee fees for women.

- Zero Collateral: Most schemes leverage CGTMSE or CGFMU, meaning no property or third-party guarantee is required for eligible loans.

- The ‘2025 Edge’:

- Single Window: Apply via the JanSamarth Portal to check eligibility for 13+ schemes instantly.

- Digital Speed: End-to-end digital processing uses your Udyam Registration and GST data for faster disbursals.

- First Step: Register on Udyam to unlock MSME status and ensure your CIBIL score is healthy (750+ recommended).

Quick Verdict:

- Need quick cash (<₹20L) for an existing shop? Go for Mudra.

- Building a new factory or service center (>₹10L)? Stand-Up India is your best bet.

- Scaling a tech or export business (>₹2Cr)? Use CGTMSE for collateral-free leverage.

SAFE Framework for Sustainable Women-Led Businesses

That’s where the “SAFE” framework comes in, something policymakers and analysts have started leaning on as a way to define what good looks like at scale. Not just more businesses, but better ones. SAFE breaks down into four ideas that sound simple, but aren’t always easy to achieve in practice:

- Sustainable — businesses that don’t disappear after a year or two

- Autonomous — where women actually make decisions, not just hold names on paper

- Formal — registered, visible, able to access credit and systems

- Employment-generating — ventures that create jobs beyond the founder

What’s interesting about SAFE is that it quietly shifts the goalpost. Instead of asking, “How many loans did we give?” it asks something more uncomfortable: Did those loans actually turn into durable businesses?

Because that’s where things often blur. A scheme might look successful on paper, thousands of accounts opened, crores disbursed, but that doesn’t automatically translate into enterprises that grow, hire, and stick around long enough to matter.

This guide, then, isn’t just a catalogue of schemes. There are already too many lists floating around. Think of it more as a map, one that tries to show not just what exists, but how it fits together (and where it doesn’t). The idea is to help women entrepreneurs move through this landscape with a bit more clarity, maybe even a sense of strategy instead of guesswork.

MSME Classification 2025 and Budget 2026 Updates Explained

Before getting into schemes and funding options, there’s a quieter but essential step that often gets overlooked: figuring out where your business actually sits in the system, not emotionally, but formally.

Because in India, eligibility starts with classification.

The MSME sector, Micro, Small, and Medium Enterprises, is often called the backbone of the economy. It’s one of those phrases that gets repeated so often it risks sounding hollow. But when you dig in, it’s not entirely exaggerated. A huge chunk of jobs, production, and local economic activity flows through this segment.

And in 2025, the government quietly redrew the boundaries of that ecosystem.

Revised MSME Classification Criteria in India (2025 Update)

- Micro Enterprises: Investment up to Rs 2.5 crore; annual turnover up to Rs 10 crore

- Small Enterprises: Investment up to Rs 25 crore; annual turnover up to Rs 100 crore

- Medium Enterprises: Investment up to Rs 125 crore; annual turnover up to Rs 500 crore

At first glance, this might look like a routine update, numbers adjusted and categories expanded. But it’s not just administrative housekeeping. These thresholds quietly determine who gets access to what: priority sector lending, subsidised interest rates, government procurement opportunities.

For some businesses, especially women-led ones that were sitting awkwardly just outside older limits, this change can feel like being let back into the room. A manufacturing unit that had “outgrown” micro status earlier might now qualify again for support it genuinely still needs.

And that matters more than it sounds on paper.

Importance of Udyam Registration and Formalisation for Women Entrepreneurs

If there’s one friction point that keeps coming up, again and again, it’s this: informality.

Not lack of ambition, not even lack of access, always, but just not being formally visible.

An estimated 95.6% of women-owned enterprises in India operate outside the formal system. There is no Udyam registration, no GST filings, and often no consistent banking trail.

And once you’re in that space, everything else gets harder.

No registration means no access to collateral-free loans backed by CGTMSE. No credit history means higher interest rates—if credit is approved at all. Cash-based operations make working capital unpredictable. It becomes a loop and a frustrating one.

Which is why Udyam registration isn’t just a checkbox. It’s more like a gateway. Slightly bureaucratic, yes, but once you’re through, a lot more doors actually open.

Key Budget 2026 Updates Impacting MSMEs and Women Entrepreneurs

Now, zooming out a bit, the Union Budget 2026 introduced a couple of changes that are worth paying attention to, even if they didn’t make splashy headlines.

The first is a Rs 10,000 crore SME Growth Fund, aimed at improving access to equity capital.

That’s important because most support structures so far have leaned heavily toward debt. Loans, loans, and more loans. But not every business needs more borrowing; sometimes it needs breathing room, risk capital, and time to grow without immediate repayment pressure.

The second is an initiative targeting 5 lakh first-time entrepreneurs, with an added emphasis on handholding. Not just funding, but guidance alongside it.

And that shift, subtle as it may seem, signals something. A move away from simply pushing credit into the system, towards actually thinking about whether businesses can survive and grow after receiving it.

Because access alone isn’t the full story. What happens after access is where things usually get decided.

Top Government Schemes for Women Business Loans in India

Pradhan Mantri Mudra Yojana (PMMY) Loan Details, Eligibility and Limits

If you talk to almost any small business owner in India, especially at the early stages, there’s a good chance PMMY comes up sooner or later. It’s not just another scheme; it’s the scheme most people have actually heard of, sometimes even before they fully understand what it does.

Launched back in 2015, the Pradhan Mantri Mudra Yojana has grown into the largest credit programme for micro-enterprises in the country. The scale is hard to ignore: over Rs 40.07 lakh crore disbursed across more than 50 crore loan accounts. And interestingly, maybe tellingly, women consistently make up more than 65% of the beneficiaries.

That’s not a small skew. It says something about where demand actually exists.

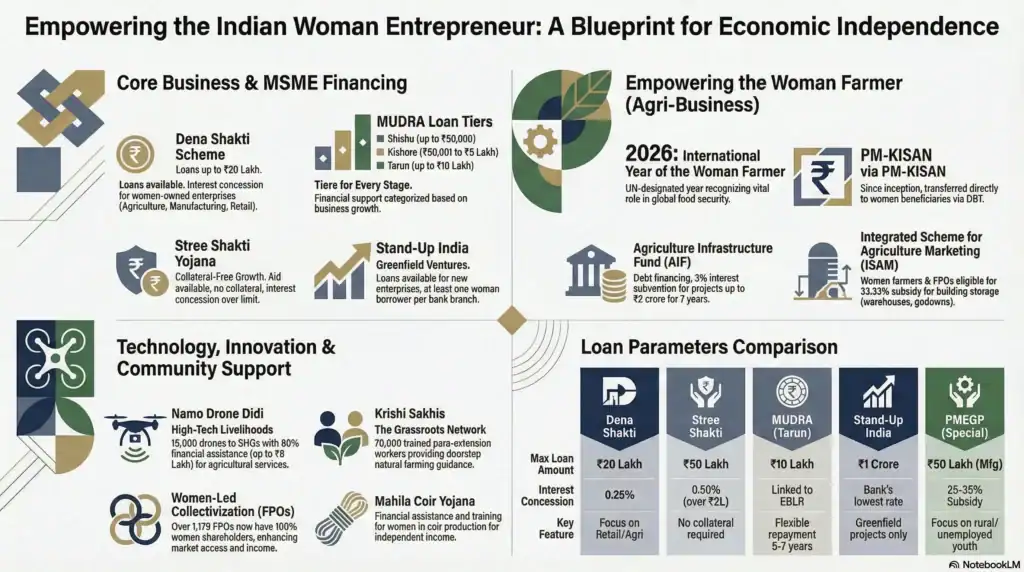

The 2025 update quietly made the scheme more relevant for businesses that are trying to grow, not just survive. The loan ceiling was increased from Rs 10 lakh to Rs 20 lakh.

Doubling the limit might sound like a technical tweak, but for someone running a small manufacturing unit or scaling a service business, it changes the conversation. Earlier, many businesses would hit that Rs 10 lakh ceiling and stall, too big for microcredit, too small (or too risky) for formal SME loans. This expansion tries to bridge that awkward middle.

The scheme now works across four tiers:

- Shishu: up to Rs 50,000

- Kishore: Rs 50,001 to Rs 5 lakh

- Tarun: Rs 5 lakh to Rs 10 lakh

- Tarun Plus: Rs 10 lakh to Rs 20 lakh

That last category, Tarun Plus, is clearly aimed at businesses that have already proven they can handle credit responsibly and are ready to push further.

Another detail that often gets overlooked but is actually quite practical: the Mudra Card. It works like a business credit card linked to your loan account, so you don’t have to withdraw the entire sanctioned amount at once. You draw what you need and when you need it.

It sounds simple, but it solves a very real problem. Taking a lump sum loan and paying interest on unused capital? That’s how small businesses quietly bleed.

And then there’s the biggest draw—no collateral, no guarantor, and no prior credit history required. For many women entrepreneurs, especially first-time ones, this isn’t just helpful. It’s the difference between starting and not starting at all.

Stand-Up India Scheme for Women Entrepreneurs: Loans from Rs 10 Lakh to Rs 1 Crore

Where PMMY supports small, incremental growth, Stand-Up India plays a different game altogether. It’s less about sustaining an existing business and more about starting something from scratch, and doing it at a scale that actually moves the needle.

The scheme is built around a simple but ambitious mandate: every scheduled commercial bank branch should support at least one woman entrepreneur with a loan between Rs 10 lakh and Rs 1 crore.

That’s not microfinance territory anymore. That’s serious project funding.

But there’s a condition and it’s an important one. The business must be at least 51% owned by a woman.

On paper, that sounds straightforward. In practice, it’s meant to prevent a common workaround where women are listed as nominal owners while control sits elsewhere. This clause tries, imperfectly, but intentionally, to ensure that the opportunity reaches actual decision-makers.

Another defining feature: Stand-Up India is strictly for greenfield projects. That means new ventures in manufacturing, services, or trading. Not working capital and not expansion of an existing setup.

And honestly, that makes it both powerful and slightly intimidating. Starting something new at that scale requires not just funding, but planning, confidence, and usually a bit of handholding.

Which is where the Stand-Up Mitra Portal comes in. It’s more than just an application gateway, it connects applicants with support systems: credit counsellors, DPR (Detailed Project Report) guidance and financial literacy tools.

Because here’s the thing, access to Rs 1 crore doesn’t mean much if you don’t know how to structure a business plan that justifies it.

Institutional Loan Schemes for Women Entrepreneurs in India

Mahila Udyam Nidhi Scheme Benefits, Eligibility and Repayment Terms

There’s a quiet problem in India’s business financing ecosystem that doesn’t get talked about enough. It sits somewhere between debt and equity, and most small businesses, especially women-led ones, get stuck right there.

Banks are comfortable giving loans as they have fixed terms, clear repayment schedules and predictable risk. But when it comes to something softer- longer timelines, flexible repayment, funding that behaves a bit like equity- they hesitate.

That’s exactly the space the Mahila Udyam Nidhi scheme was designed to fill.

It offers soft loans to women entrepreneurs in the tiny and small-scale sectors, but what really sets it apart isn’t just access—it’s time. Repayment periods can stretch up to 10 years, with a moratorium of up to 5 years on principal repayment.

And that changes the pressure dynamics completely.

Because early-stage businesses don’t fail only due to lack of revenue, they fail because revenue doesn’t arrive fast enough. A longer runway can mean the difference between stabilising and shutting down quietly.

MUN, in a way, acknowledges that reality. It doesn’t rush the business into repayment before it’s ready.

SIDBI SMILE Scheme for MSME Modernisation and Technology Upgrades

Then there’s another kind of constraint—less visible, but just as limiting: outdated technology.

A lot of small enterprises, especially in sectors like garments, food processing, or handicrafts, operate with equipment that’s functional, but far from efficient. Productivity suffers, quality fluctuates, and scaling becomes difficult.

SIDBI SMILE steps into this space. It provides soft loans covering up to 75% of the project cost for modernisation—upgrading machinery, expanding capacity, improving processes.

And this isn’t just about better machines. It’s about competitiveness.

A small shift in technology can ripple outward. This includes faster production, better consistency, and access to new markets. Small units can transform almost overnight after upgrading equipment. Same people, same product line, but suddenly, margins improve, rejection rates drop, and buyers take them more seriously.

That’s the kind of shift SMILE is trying to enable.

TREAD Scheme for Women Entrepreneurs: Grant-Based Credit Support

Not every entrepreneur starts from the same place. Some don’t just lack capital, but they lack access, documentation, and sometimes even the confidence to walk into a bank and ask for a loan.

The TREAD scheme takes a very different approach compared to most others.

Instead of lending directly to women entrepreneurs, it works through NGOs. The government provides a grant, up to 30% of the total loan amount, to these organisations, which then facilitate credit and support for women beneficiaries.

It’s a layered model. Slightly indirect, but intentional.

Because for women who are illiterate or semi-literate, or who don’t have the paperwork or familiarity with formal systems, direct lending often just doesn’t work. The friction is too high.

TREAD tries to reduce that friction by inserting a support layer—someone to guide, translate, simplify.

It’s not perfect. It depends heavily on the quality of the NGO involved. But when it works, it reaches people; most schemes simply don’t.

CGTMSE Scheme Explained: Collateral-Free Loans for Women Entrepreneurs

And then there’s the elephant in the room: collateral.

Most banks still want it. Property, typically, land, basically something tangible they can fall back on.

But here’s the reality: many women don’t own property in their own name. So even if they have a viable business idea, even if they’re capable of running it, they hit a wall almost immediately.

CGTMSE is designed to remove that wall.

Instead of asking the borrower for collateral, the scheme provides a guarantee to the bank. In simple terms, the government shares the risk.

The guarantee ceiling has been increased to Rs 10 crore, which is not trivial. It pushes collateral-free lending well beyond micro-scale into small enterprise territory.

What’s interesting is that most entrepreneurs don’t even realise they’re benefiting from CGTMSE. It works in the background. If you’re taking a loan under PMMY or Stand-Up India, chances are this guarantee structure is already supporting your application.

It’s invisible, but critical.

Bank Loan Schemes for Women Entrepreneurs in India

SBI Women Business Loan Schemes: Stree Shakti and SBI Asmita Details

If there’s one institution that shows up everywhere in India’s financial ecosystem, it’s SBI. And over time, they’ve built a couple of offerings specifically for women entrepreneurs—though, like most bank products, the real experience often depends on the branch and the manager.

The Stree Shakti Package is probably the more accessible of the two. It offers a 0.50% interest rate concession on loans above Rs 2 lakh, provided the business is majority-owned by a woman and she’s completed an Entrepreneurship Development Programme (EDP).

Now, half a percent might not sound like much at first. But over a multi-year loan, that reduction adds up. Quietly. It’s the kind of benefit you don’t feel immediately, but you notice over time—like a slightly lighter weight you’ve been carrying.

Then there’s SBI Asmita, which sits at the other end of the spectrum.

This one is aimed at more established businesses, offering credit up to Rs 5 crore. And that’s significant, because there aren’t many women-focused products operating at that scale. It’s essentially trying to bridge a gap between small business lending and full-fledged corporate financing.

And that gap? That’s where a lot of women-led businesses stall.

Bank of Baroda Women Loan Schemes: Dena Shakti and Shakti Samriddhi

Bank of Baroda takes a slightly different approach. It’s less about large flagship products, more about broad accessibility across sectors.

The Dena Shakti Scheme offers a 0.25% interest rate concession for women entrepreneurs across multiple sectors—agriculture, manufacturing, retail, and micro-credit.

Yes, the concession is smaller compared to SBI’s offering, but the wider coverage makes it easier for more women to actually qualify.

Sometimes, accessibility beats generosity.

What’s more interesting, though, is their Shakti Samriddhi programme.

Because this one steps outside of credit.

It focuses on mentorship, market linkage, business development support, the things that don’t show up in loan agreements but often determine whether a business survives past its early stages.

And honestly, this shift is long overdue. Capital alone doesn’t fix everything. Sometimes it just amplifies existing gaps.

Canara Bank Women Loan Schemes: Mahila Vikas and Stree Shakti

Canara Bank’s offerings feel a bit more practical, almost asset-focused.

The Mahila Vikas Scheme is designed for women entrepreneurs who need to invest in tangible business assets—premises, machinery, equipment.

This is especially relevant in manufacturing or production-heavy businesses, where growth isn’t about working capital alone; it’s about what you own and can produce.

Then there’s the Canara Stree Shakti scheme, which—like its counterparts—offers concessional rates and simpler documentation.

Nothing radically different on paper. But sometimes, simplification itself is the differentiator.

What Actually Impacts Loan Approval and Borrower Experience

Here’s the part that rarely makes it into official descriptions.

The interest rate concession? Helpful, yes. But rarely decisive.

What actually shapes a woman entrepreneur’s experience with bank credit tends to be far more human:

- Does the relationship manager understand the business model?

- Are documentation requirements realistic, or quietly overwhelming?

- Is the process explained clearly—or left for the applicant to figure out?

- How long does approval actually take, not theoretically?

These are the things people remember. These are the stories that get shared.

Two entrepreneurs can apply for the same scheme and walk away with completely different experiences-one smooth, one frustrating-based purely on how it’s implemented on the ground.

And that’s the uncomfortable truth running through all of this: design matters, but delivery matters more.

Agriculture Schemes for Women Entrepreneurs in India

International Year of the Woman Farmer 2026: Policy Impact and Opportunities

There’s something quietly significant about 2026 being declared the International Year of the Woman Farmer. It’s not just symbolic, though it might look that way at first glance. It shifts attention. And in policy, attention tends to pull funding, programmes, and urgency along with it.

India, for its part, seems to be leaning into that moment.

Because the reality has been sitting in plain sight for years: rural women contribute somewhere between 60% to 80% of agricultural labour, yet control very little of the resources—land, credit, technology. There’s a kind of imbalance there that’s so normalized it almost disappears into the background.

Until you look directly at it.

The policy push around 2026 tries to correct some of that, not all at once, not perfectly, but through a mix of financial support, access to technology, and collective models that give women a bit more negotiating power.

Namo Drone Didi Scheme: Subsidy, Training and Income Opportunities

Now, this one feels almost unexpected when you first hear about it.

Drones. In agriculture. Operated by women’s self-help groups.

And yet it works.

The Namo Drone Didi programme provides agricultural drones to SHGs, with up to 80% of the cost subsidised (capped at Rs 8 lakh).

But what makes it interesting isn’t the subsidy. It’s the model.

Instead of owning the drone as a tool for personal farming, SHGs use it as a service business. Members are trained, becoming “Drone Didis”-and then offer services like crop spraying, seeding, crop monitoring to other farmers in the area.

So the drone stops being an expense and becomes an income-generating asset.

It’s a small shift in framing, but a powerful one.

And there’s something else here, too—less tangible. Technology, when placed in the hands of women who haven’t traditionally had access to it, tends to ripple outward. Confidence changes. Roles shift, even if subtly.

The programme aims to distribute 15,000 drones. On paper, that’s a number. On the ground, it’s thousands of small enterprises taking shape in places that don’t usually get described as “entrepreneurial hubs.”

Farmer Producer Organisations (FPOs): Collective Growth for Women Farmers

If you’ve ever looked at small-scale farming economics, you’ll know the problem: individually, farmers don’t have much leverage. Not in buying inputs, not in selling produce, not in accessing credit.

FPOs try to solve that by changing the unit of participation.

Instead of one farmer negotiating alone, you have a collective.

For women, this model becomes even more important. Because beyond economics, it addresses something more structural—decision-making power.

The push toward 100% women-shareholder FPOs is particularly interesting. It creates spaces where women aren’t just participants but actual decision-makers. No dilution, no silent sidelining.

That directly tackles a recurring issue, the “nominal ownership” problem, where women are listed as owners, but control sits elsewhere.

In women-led FPOs, that dynamic shifts. Not perfectly, not overnight—but enough to matter.

MKSP Scheme: Skill Development and Capacity Building for Women Farmers

Then there’s MKSP, which takes a step back from credit entirely and focuses on something more foundational: capability.

The programme has trained over 4.62 crore women in areas like agro-ecology, livestock management, organic farming, post-harvest processing.

That’s a massive number. Almost hard to visualise.

But the philosophy behind it is what stands out.

Credit without capability can backfire.

A loan given without the knowledge to use it effectively can create pressure instead of progress. I’ve seen this in small farming setups—money comes in, but without the right techniques or market access, returns don’t follow. And repayment becomes a burden.

MKSP tries to flip that sequence. Build skills first. Then let financial support layer on top of something stable.

It’s slower. Less flashy. But arguably more durable.

Challenges in Scaling Women-Owned Businesses in India

The “Missing Middle” Problem in Women Entrepreneurship in India

For all the schemes, subsidies, portals, and policy announcements, there’s one stubborn pattern that refuses to shift.

Most women-led businesses stay small.

In fact, less than 1% of women-led firms in India ever make it to the “medium enterprise” category, the stage where businesses start plugging into exports, supply chains, and the impact can’t be negligible.

That drop-off, that gap between micro and scalable, is what people call the “missing middle.”

And it’s not just a statistic. It’s a pattern you start noticing once you look for it.

Plenty of women access microcredit. PMMY, SHGs, small-ticket loans—they’re working, at least at the entry level. But then something happens. Or rather, it doesn’t happen.

Growth stalls.

The jump from:

• micro → small

• small → medium

That’s where the pipeline breaks.

And it’s not because ambition disappears. It’s because the support system thins out right when the stakes get higher.

Socio-Cultural Barriers Affecting Women Entrepreneurs in India

Some of the barriers aren’t financial at all. They’re woven into everyday life.

Take time poverty, for instance.

Women in India perform about 76% of all unpaid care work—childcare, elder care, and household management.

That’s not just a statistic you nod at and move on from. It translates into fewer hours for business, less flexibility to travel, and limited ability to attend training programmes or networking events.

I remember speaking to a small business owner who ran a tailoring unit from home. Her biggest constraint wasn’t capital; it was time. Orders would pile up, but between household responsibilities and business, something always had to give, usually, the business.

No scheme really accounts for that kind of friction.

Then there’s credit aversion.

It’s easy to label it as hesitation, but that’s too simplistic. For many first-generation women entrepreneurs, debt carries a different weight. It’s not just financial risk but a social risk.

Failure isn’t isolated. It spills into family reputation, community perception, and even future prospects for children.

So the caution isn’t irrational, but it’s calibrated.

But it does mean that even when credit is available, it’s not always taken. Or it’s taken in smaller amounts than what the business actually needs to grow.

The Informality Trap and Credit Access Challenges for Women Entrepreneurs

And then we circle back to something we touched on earlier: informality.

It doesn’t just block entry, but it blocks growth.

No registration → no credit history

No credit history → higher interest rates

Higher rates → limited borrowing

Limited borrowing → limited growth

Limited growth → continued informality

It loops. Quietly, but persistently.

Breaking out of that cycle isn’t a single-step fix. It requires things happening together:

- formal registration

- financial literacy

- accessible credit

- trust in the system

Miss one piece, and the cycle tends to rebuild itself.

Platforms Supporting Women Entrepreneurs: Mentorship and Market Access in India

NITI Aayog Women Entrepreneurship Platform (WEP 3.0): Features and Benefits

At some point, you start noticing a pattern: access to capital gets a lot of attention, but it’s rarely the whole story.

A business can get funded and still feel stuck. No clear direction, no network, no idea which opportunity to chase next. That’s where platforms like WEP start to matter.

The Women Entrepreneurship Platform, now in its 3.0 version, has evolved quite a bit from what it originally was. It used to feel more like a directory, useful, but static. Now it’s trying to behave more like an ecosystem.

One of the more interesting additions is the “Smart Match” feature. Instead of expecting entrepreneurs to sift through dozens of schemes (which, honestly, can feel overwhelming), it suggests options based on your business profile—sector, stage, and needs.

It’s a small shift in design, but a meaningful one. Less searching, more guided discovery.

Then there’s the “Award to Reward” mentorship network, which, despite the slightly formal name, is essentially about connecting women entrepreneurs with people who’ve already walked the path. And that kind of access is hard to quantify, but it changes things.

Because sometimes, one conversation can save months of trial and error.

The platform also hosts the “Financing Women Collaborative,” bringing together financial institutions that are (at least in principle) committed to expanding credit access for women-led enterprises.

Underlying all of this is a broader idea, spelled out in NITI Aayog’s “From Borrowers to Builders” report, that support shouldn’t come in isolated pieces. Finance, mentorship, skills, and market access they need to connect. Otherwise, gaps start showing up right where businesses are trying to grow.

GeM and TReDS Platforms: Improving Market Access and Cash Flow for MSMEs

If WEP is about guidance and connections, platforms like GeM and TReDS are about something more concrete: actual business flow.

Let’s start with GeM, the Government e-Marketplace.

For many small businesses, getting reliable buyers is harder than getting funding. Demand is unpredictable, negotiations are uneven, and access to large clients is limited.

GeM tries to level that, at least partially, by opening up government procurement to MSMEs, including women-owned ones. And since CPSEs (Central Public Sector Enterprises) are mandated to procure a portion from MSMEs, it creates a kind of built-in demand pipeline.

Not guaranteed success, but definitely a more structured opportunity than chasing private contracts blindly.

Then there’s TReDS which solves a very different problem: delayed payments.

It’s one of those issues that doesn’t get enough attention until you’re in it. You deliver goods or services, invoices are raised and then you wait. Sometimes 30 days. Sometimes 90. Sometimes longer.

For a small business, that gap can choke cash flow.

TReDS allows MSMEs to discount their receivables, basically get paid earlier by selling those invoices to financiers at competitive rates.

Budget 2026 pushed this further by mandating faster payment settlement through TReDS for CPSEs.

And that matters. Because liquidity, steady, predictable cash flow, is what keeps businesses alive between growth spurts.

How to Apply for Women Business Loans in India: Step-by-Step Guide

Documents Required for Women Business Loan Applications in India

No matter which scheme you’re applying for-PMMY, Stand-Up India, or a bank-specific product- there’s a core set of documents that keeps showing up. It’s not always communicated clearly upfront, which is where a lot of frustration begins.

At the base of everything is identity and address proof—most commonly Aadhaar.

That part is usually straightforward.

Where things get slightly more layered is proof of business ownership. Depending on how your business is set up, this could be:

- a partnership deed

- a company incorporation certificate

- or, in many small cases, a self-declaration for a sole proprietorship

Then comes the Detailed Project Report (DPR), which, for many applicants, is the first real hurdle.

It’s not just paperwork. It’s your business translated into numbers and narrative:

- what you plan to do

- how you’ll earn

- what it will cost

- how you’ll repay

For schemes like Stand-Up India or larger-term loans, this document carries weight. And if you’ve never made one before, it can feel intimidating. Not impossible, but just unfamiliar.

Add to that:

- last six months of bank statements

- income tax returns (if applicable)

- Udyam registration certificate

And you’ve got the standard bundle most banks expect.

Nothing here is individually complex. But together, it can feel like a lot, especially if you’re assembling it for the first time.

Online Application Portals for Women Business Loans: JanSamarth and Udyami Mitra

One thing that has improved, quietly but meaningfully, is the shift toward digital applications.

The JanSamarth Portal is now a central entry point for several government-linked schemes.

In theory, you can:

• apply online

• upload documents

• complete Aadhaar-based verification

• track your application

All without stepping into a bank branch.

And for many people, especially in semi-urban or rural areas where bank visits can be time-consuming or intimidating, that’s a real advantage.

The platform is also multilingual, which sounds like a small feature until you realise how often language becomes an invisible barrier in financial processes.

Alongside this, there’s the Udyami Mitra portal, which connects applicants to SIDBI-linked schemes and support agencies.

Both platforms can be used in parallel. You’re not locked into one pathway, which is useful, because eligibility often overlaps across schemes.

Offline Support for Loan Applications: DICs and LDM Assistance

That said, digital isn’t always comfortable for everyone.

And this is where offline channels still matter more than people assume.

District Industries Centres (DICs) are one of those under-discussed resources. They exist in almost every district and are staffed with officers who can help with:

- identifying relevant schemes

- preparing documentation

- guiding applications

Similarly, Lead District Managers (LDMs), appointed by the RBI, play a coordinating role between banks and government schemes at the district level.

If walking into a bank branch feels overwhelming (and for many first-time applicants, it does), approaching a DIC or LDM first can make the process smoother. They act like intermediaries, in a way. Translators between policy and practice.

FAQs: Women Business Loans & Government Schemes (2025–2026)

The “best” loan depends on your business stage. For new ventures, Stand-Up India offers the highest funding (up to ₹1 crore). For existing small businesses, PMMY (Mudra) is the go-to for quick working capital. For large-scale expansion, CGTMSE-backed loans are ideal for collateral-free funding up to ₹10 crore.

Absolutely. Under the 2025–2026 guidelines, schemes like PMMY, Stand-Up India, and CGTMSE are specifically designed to eliminate the need for property or gold as security. The government acts as your “guarantor” to the bank.

To qualify, you generally need:

Ownership: Minimum 51% stake held by a woman.

Credit Score: A CIBIL score of 700+ is preferred (though some Mudra loans are more flexible).

Registration: Valid Udyam Registration (MSME).

Project Report: A clear plan showing how you will use the funds and repay them.

The Stand-Up India Scheme remains the gold standard for “Greenfield” (new) projects. It provides between ₹10 lakh and ₹1 crore. Pro-Tip: Ensure your business is in manufacturing, services, or the trading sector to qualify.

The PMMY offers four tiers of funding based on your need:

Shishu: Up to ₹50,000 (Ideal for home-businesses).

Kishore: ₹50,000 to ₹5 lakh.

Tarun: ₹5 lakh to ₹10 lakh.

Tarun Plus: ₹10 lakh to ₹20 lakh (Expanded for 2025).

Note: Interest rates are typically 1–2% lower for women borrowers at most PSU banks.

Avoid the queues by using these official portals:

JanSamarth Portal: The one-stop shop for all 13+ government credit schemes.

Udyami Mitra: Best for SIDBI-linked loans and finding hand-holding agencies to help with your application.

Keep digital copies of these ready:

Identity: Aadhaar and PAN Card.

Business Proof: Udyam Certificate and GST registration (if turnover exceeds threshold).

Financials: Last 6–12 months’ bank statements and IT Returns (for loans above ₹5 lakh).

The “Deal Closer”: A Detailed Project Report (DPR) explaining your business model.

CGTMSE is a trust that provides credit guarantees to lenders. It is vital for women who have outgrown small loans and need up to ₹10 crore to scale but do not have commercial property to pledge as collateral.

Yes, many banks have “Women-Only” desks with reduced processing fees:

SBI Stree Shakti: Offers interest concessions for tiny-sector units.

Bank of Baroda (Mahila Shakti): Specialized credit for women entrepreneurs.

Canara Bank (Mahila Vikas): Tailored for women in the MSME sector.

The “Missing Middle” and informality. Many women-owned businesses operate without formal registration (Udyam) or proper bookkeeping. To ensure approval in 2025, ensure your business is registered and all transactions are routed through a business bank account.

Quick Match: Finding the Right Business Loan for Your Stage

| Business Stage | Best Scheme | Max Loan Amount | Key Benefit |

| Micro / Home-based | Mudra (Shishu) | Up to ₹50,000 | Minimal docs; No collateral |

| Small / Growing | Mudra (Kishore/Tarun) | ₹50,000 – ₹20 Lakh | Working capital & equipment |

| New Venture (Greenfield) | Stand-Up India | ₹10 Lakh – ₹1 Crore | High funding for first-timers |

| Scaling / Industrial | CGTMSE | Up to ₹10 Crore | Collateral-free large-scale credit |

| Bank-Specific | SBI Stree Shakti / BoB | Varies by Bank | Lower interest rates for women |

From Women Borrowers to Scalable Business Builders in India

If you step back and look at the full picture, something becomes clear, India doesn’t lack schemes for women entrepreneurs.

In fact, the architecture is surprisingly dense.

There’s collateral-free credit through PMMY and CGTMSE. Long-tenor support through MUN. Greenfield funding via Stand-Up India. Rural enterprise models like Namo Drone Didi. Platforms like WEP trying to stitch everything together.

On paper, it’s all there. A layered system. Thought through, at least in design.

But the gap isn’t really about availability anymore.

It’s about coherence.

Too many women entrepreneurs still don’t know these schemes exist. And even when they do, the process of navigating them can feel fragmented—like trying to assemble something without a clear instruction manual.

And then there’s the last mile problem.

Accessing credit is one thing. What happens after that—whether mentorship shows up, whether market linkages actually materialise, whether the support system holds—that’s far less consistent.

Which is why the conversation is slowly shifting.

From:

“How much did we lend?”

To:

“What did that lending actually build?”

The idea of Viksit Bharat 2047 often gets framed in big, sweeping terms. But if it’s going to mean anything on the ground, it will likely come down to something more specific: whether women-led businesses can move beyond survival and become part of larger economic systems.

Supply chains. Public procurement. Export networks.

That’s where platforms like GeM, TReDS, and cluster-based initiatives like SFURTI and Coir Vikas Yojana start to matter, not as standalone schemes, but as connectors.

Because growth doesn’t happen in isolation. It happens when businesses are plugged into something bigger than themselves.

If there’s one practical takeaway from all of this, it’s not to chase a single scheme.

That’s a common instinct, find the best loan, apply, done.

But the businesses that tend to last don’t rely on just one lever. They build a kind of ecosystem around themselves:

- • credit for capital

- • mentorship for direction

- • platforms for market access

- • peer networks for support

- • ongoing skill development

And that combination… it compounds over time.

India already has the pieces.

The real challenge now is how well those pieces connect—on the ground, in real businesses, in real lives.

Because policy intent is one thing.

But what ultimately matters is whether that intent translates into enterprises that grow, hire, sustain and stick around long enough to matter.

Disclaimer

The content on this page is intended for informational and educational purposes only and should not be construed as professional financial, tax, or legal advice. India Policy Hub and its authors are not certified financial planners, registered investment advisors, or practicing Chartered Accountants (CAs). Tax laws, particularly regarding international assets and compliance, are complex and subject to change. Always consult a qualified professional or Chartered Accountant regarding your specific financial situation, tax liabilities, or legal compliance before making any financial decisions or submitting tax declarations.

Discussion (1)

Leave a Reply