NPS Tier 1 vs Tier 2 (2026): Maximize Your Retirement Corpus & Section 80CCD(1B) Tax Benefits

NPS in 2026: Navigating Tier 1 vs Tier 2 for Maximum Tax Benefits

Retirement planning in India has become both more important and more complex than ever before. People are living longer, traditional pension coverage remains limited for many private-sector employees, and inflation continues to chip away at the purchasing power of savings. Against this backdrop, the National Pension System (NPS) has emerged as one of the country’s most effective long-term retirement and wealth-building solutions. Herein comes the issue of NPS Tier 1 vs Tier 2.

Even so, many investors still struggle with a basic but important question: what is the difference between an NPS Tier 1 account and a Tier 2 account, and how do they affect your taxes?

This guide breaks down the answer in simple terms. We’ll compare both account types, explain how the Section 80CCD(1B) deduction can help eligible taxpayers save up to ₹15,600 annually, and explore practical strategies that can help you build a stronger retirement corpus in 2026 and the years ahead.

At A Glance: NPS Tier 1 vs Tier 2

- Core Objective: A comprehensive keyword research and SEO strategy for NPS Tier 1 vs Tier 2 (2026), focusing on maximizing retirement corpus and 80CCD(1B) tax benefits.

- Target Audience: Salaried professionals, self-employed individuals, and high-tax-bracket earners in India seeking wealth creation, tax deductions, and clarity on 2026 tax regime changes.

- Key 2026 Regulatory Updates Addressed: Incorporates the new ₹8 Lakh 100% lump-sum withdrawal limit, the Multiple Scheme Framework, and the nuances of the New Tax Regime (Section 115BAC) where 80CCD(1B) is abolished but 80CCD(2) survives.

- Strategic Deliverable: Uncovers high-intent long-tail keywords, maps them to logical content clusters, and provides advanced AI search (SGE) and voice search optimization tactics to dominate the SERPs.

Understanding the National Pension System (NPS) in 2026

The Evolution of India’s Primary Retirement Framework

The National Pension System (NPS) began in January 2004 as a retirement scheme for newly recruited Central Government employees. A few years later, in 2009, it was opened to all Indian citizens, transforming it from a government-focused initiative into a widely accessible retirement planning tool. Today, it is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and serves millions of subscribers nationwide.

One of the major turning points in NPS’s growth came in 2013, when corporate participation was formally introduced through an employer-employee contribution framework. Since then, a series of budget announcements have steadily enhanced its appeal. Among the most significant was the introduction of Section 80CCD(1B) in 2015, which created an exclusive additional tax deduction of ₹50,000 over and above the standard ₹1.5 lakh limit available under Section 80C. This distinction makes NPS one of the few investment options in India with a dedicated tax-saving benefit of its own. Official circulars, regulatory updates, and operational guidelines are available here.

By 2026, the system will become far more digital and user-friendly than it was in its early years. Subscribers can now open accounts, make contributions, switch pension fund managers, update details, and even initiate withdrawals online without paperwork through the eNPS portal. Behind the scenes, Central Record Keeping Agencies (CRAs) such as Protean (formerly NSDL) and KFintech/CAMS manage account administration and recordkeeping.

Decoding the Dual-Account Structure

When you join NPS, you’re assigned a Permanent Retirement Account Number (PRAN), a unique 12-digit identifier that remains with you throughout your working life, regardless of where you live or work. Under this single PRAN, you have access to two separate account types: Tier 1 and Tier 2.

A simple way to think about them is as two compartments serving different purposes. Tier 1 is your dedicated retirement account, designed to keep your savings invested until retirement. Tier 2, on the other hand, offers much greater flexibility and functions as an open-ended investment account. While it generally lacks the tax benefits of Tier 1, Central Government employees may claim deductions under Section 80C for Tier 2 contributions, provided the funds are maintained through a mandatory three-year lock-in period.

As explained by Value Research Online in its overview of the NPS structure, Tier 1 forms the foundation of the system. Tier 2 can only be opened if you already have an active Tier 1 account. This requirement reflects the original purpose of NPS: encouraging long-term retirement savings first, while providing additional investment flexibility through the optional Tier 2 account.

Both accounts can invest in the same broad asset classes, including equity (Scheme E), government securities (Scheme G), and corporate bonds (Scheme C). They can also be managed by the same Pension Fund Managers. The real differences emerge when you look at taxation, withdrawal rules, and liquidity.

What Happens to NPS Account After Death of Subscriber?

In the event of a subscriber’s death, the accumulated corpus in both Tier 1 and Tier 2 accounts is transferred to the registered nominee or legal heir. Unlike certain exit scenarios where annuity purchase is mandatory, death claims are treated differently. The nominee is not required to buy an annuity and can receive the entire corpus as a lump sum.

An additional advantage is the tax treatment. The amount received by the nominee is fully exempt from income tax, ensuring that the accumulated retirement savings pass to the beneficiary without creating an additional tax burden.

To avoid delays during claim settlement, subscribers should periodically review and update their nomination details. It is equally important to ensure that nominee KYC information remains accurate and current within the CRA records. Detailed guidance on claim procedures and documentation requirements can be found in the PFRDA circulars.

NPS Tier 1 Account: The Mandatory Retirement Shield

Primary Objectives and Lock-in Period Rules

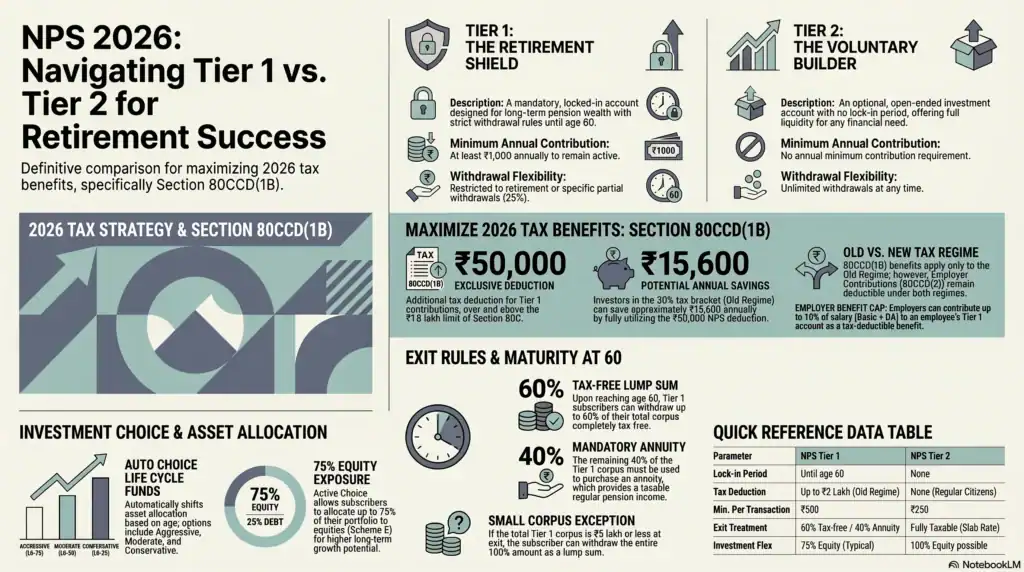

Tier 1 is the core account within the National Pension System and the one that truly drives its retirement-focused structure. Its purpose is straightforward: to help subscribers build a sizeable retirement corpus over several decades and convert part of that corpus into a regular income stream after retirement.

To ensure that retirement savings are not withdrawn prematurely, Tier 1 comes with a strict lock-in period. In most cases, contributions remain invested until the subscriber reaches the age of 60 or attains superannuation. While certain partial withdrawals are allowed under specific circumstances, the account is intentionally designed to discourage frequent access to funds.

At maturity, under Section 10(12A) of the Income Tax Act, subscribers can withdraw up to 60% of the accumulated corpus as a tax-free lump sum. The remaining 40% is required to be used for purchasing an annuity, which is exempt from taxation at the time of purchase under Section 80CCD(5), although subsequent annuity payouts remain taxable according to the subscriber’s applicable income slab.

NPS also offers flexibility at the exit stage. Subscribers may defer both lump sum withdrawal and annuity purchase if they prefer to stay invested for longer. Depending on the subscriber category, the account can continue beyond age 60 and, in some cases, remain active up to age 85. Updated exit provisions and continuation rules are available here.

In simple terms, Tier 1 is less about accessibility and more about discipline. The restrictions can sometimes feel limiting, but they exist for a reason. Retirement planning often succeeds because money is difficult to access, not because it is easy to withdraw.

Minimum Contribution Requirements for 2026

As of 2026, Tier 1 accounts continue to maintain relatively modest contribution requirements, making the scheme accessible to a wide range of investors.

Current contribution rules include:

• Minimum contribution per transaction: ₹500

• Minimum annual contribution: ₹1,000 across all contributions during the financial year

• No upper contribution limit, although tax deductions remain subject to the limits prescribed under the Income Tax Act

For tax purposes under the Old Tax Regime, salaried employees can generally claim deductions under Section 80CCD(1) based on up to 10% of their salary (basic pay plus dearness allowance), while self-employed individuals can claim deductions based on up to 20% of their gross total income. It is critical to note that these individual deductions operate strictly within the overarching ₹1.5 lakh statutory ceiling mandated by Section 80CCE.

To maximize total tax relief beyond this ceiling, subscribers utilize the supplementary ₹50,000 deduction available under Section 80CCD(1B). However, taxpayers filing under the default New Tax Regime governed by Section 115BAC forfeit both of these individual exemptions entirely. In such scenarios, Section 80CCD(2) serves as the primary surviving statutory carve-out, allowing employees under the default regime to claim tax relief on employer-routed Corporate NPS contributions up to 10% of their salary (14% for government personnel).

Beyond these precise tax frameworks, one point regarding account maintenance that often surprises new subscribers is that there is no minimum balance requirement. As long as the annual contribution threshold is met, the account remains active.”e. If the minimum annual contribution is not made, the account may be marked as frozen. Fortunately, reactivation is usually straightforward and can be completed by contributing the required shortfall along with the prescribed penalty.

For operational details and account maintenance guidelines, subscribers can refer here.

Does NPS Tier 1 Have a Guaranteed Return?

No, NPS Tier 1 does not provide guaranteed returns.

Unlike products such as the Public Provident Fund (PPF) or the Senior Citizens Savings Scheme (SCSS), NPS is a market-linked investment. The value of your retirement corpus depends on several factors, including your contribution amount, investment duration, asset allocation, and the performance of the underlying markets.

That said, long-term investors have historically benefited from the structure of the scheme. Equity allocations under Scheme E have delivered competitive returns over extended periods, particularly for investors who remained invested through multiple market cycles. Debt-oriented schemes have also played an important role by providing stability and diversification within the portfolio.

The PFRDA’s PRIDE DISHA calculator allows subscribers to estimate potential retirement outcomes under different contribution and return assumptions. Investors interested in comparing historical fund performance can also review the Value Research NPS tracker.

While past performance should never be treated as a guarantee of future returns, the long investment horizon associated with retirement planning allows compounding to work in a way that shorter-term investments often cannot replicate.

Premature, Partial, and Superannuation Withdrawal Guidelines

Understanding withdrawal rules is essential before committing significant amounts to Tier 1, because liquidity is intentionally restricted.

At retirement (age 60 or superannuation)

Under Section 10(12A) of the Income Tax Act, subscribers can withdraw up to 60% of the corpus as a tax-free lump sum. The remaining 40% must generally be utilized to purchase an annuity, which is exempt from taxation at the time of purchase under Section 80CCD(5), though subsequent annuity payouts remain taxable according to the subscriber’s applicable income slab.

Premature exit before age 60

Early exit is allowed, but the rules are far more restrictive. Only 20% of the accumulated corpus can be taken as a lump sum, while 80% must be used to purchase an annuity. This framework is designed to preserve retirement income even when a subscriber leaves the scheme early.

Partial withdrawals

NPS does provide limited access to funds during the accumulation phase. After completing three years in the scheme, subscribers may withdraw up to 25% of their own contributions—which remains entirely tax-exempt under Section 10(12B) of the Income Tax Act—for specific purposes such as:

• Higher education of children

• Marriage of children

• Purchase or construction of a first residential property

• Treatment of specified critical illnesses

• Disability or incapacitation-related needs

A maximum of three such partial withdrawals is permitted during the subscriber’s lifetime under NPS. Detailed rules are available through the master circular and the NPS Trust portal.

Small corpus exception

If the total Tier 1 corpus at the time of exit is ₹5 lakh or less, subscribers may choose to withdraw the entire amount as a lump sum without purchasing an annuity. This provision helps avoid situations where very small retirement balances are converted into negligible monthly pension payments. The applicable regulations are available here.

The overall message is clear: Tier 1 rewards patience. It is built for retirement first and liquidity second. Investors who understand this from the beginning are far less likely to be frustrated by the withdrawal restrictions later on.

NPS Tier 2 Account: The Voluntary Wealth Builder

Eligibility Requirements and Account Activation Process

A Tier 2 account is available only to individuals who already have an active NPS Tier 1 account linked to a valid PRAN. Unlike Tier 1, which is mandatory when enrolling in NPS, Tier 2 is entirely optional. You can choose to open it, ignore it, or activate it later depending on your financial needs.

In practice, Tier 2 works much like a flexible investment account attached to your NPS profile. As Zerodha Varsity explains in its detailed guide, it functions similarly to an open-ended investment vehicle, giving subscribers access to the same professionally managed NPS investment ecosystem without the strict retirement lock-in.

Opening a Tier 2 account is straightforward. Subscribers can activate it online through the eNPS platform or through an authorised Point of Presence (PoP). The minimum opening contribution is ₹1,000, and unlike Tier 1, there is no requirement to make annual contributions to keep the account active. Even if you stop investing for a long period, the account does not get frozen.

Another advantage is flexibility in fund management. Investors are not required to use the same Pension Fund Manager for both accounts. This means you can maintain one investment strategy in Tier 1 and a completely different one in Tier 2, depending on your goals and risk tolerance.

Is NPS Tier 2 Tax-Free?

This is where many investors get caught off guard.

Despite being part of the NPS framework, Tier 2 does not enjoy the same tax benefits as Tier 1. For most investors, contributions made to a Tier 2 account do not qualify for deductions under Section 80C, Section 80CCD(1), or Section 80CCD(1B). The only notable exception applies to certain Central Government employees investing through the notified Tier 2 default scheme and complying with the prescribed lock-in requirements.

For everyone else, Tier 2 contributions are made from post-tax income without any immediate tax relief.

Tax treatment on withdrawal is also less favourable than many investors expect. Gains from Tier 2 investments are generally taxed according to the investor’s applicable income tax slab, unlike equity mutual funds that benefit from a separate capital gains taxation framework. This difference can have a meaningful impact on post-tax returns over time.

As highlighted in Cleartax’s comparison of Tier 1 and Tier 2 accounts, the absence of meaningful tax incentives is one of the biggest reasons Tier 2 remains a supplementary investment option rather than a primary wealth-building vehicle for most subscribers.

That does not mean Tier 2 lacks value. It simply means its appeal comes from flexibility and cost efficiency rather than tax savings.

Liquidity Advantages and Zero Lock-in Periods

If Tier 1 is designed to lock your money away for retirement, Tier 2 sits at the opposite end of the spectrum.

There is no lock-in period, no minimum holding requirement, and no restriction on withdrawals. Investors can contribute whenever they wish and withdraw whenever they need funds. Whether the money remains invested for ten years or ten days is entirely the subscriber’s decision.

This flexibility makes Tier 2 particularly attractive for people who appreciate the NPS investment framework but are uncomfortable committing all their savings to a retirement-focused account. It can serve as a place for medium-term goals, surplus cash, or investments that may need to be accessed before retirement.

Another useful feature is the ability to transfer funds from Tier 2 to Tier 1. This one-way transfer can be valuable in years when you want to increase your retirement savings or maximise tax-related opportunities within Tier 1.

According to Zerodha Varsity, Tier 2 equity allocations have historically produced results comparable to large-cap equity mutual funds. The debt-oriented options under Schemes C and G have also delivered competitive outcomes relative to similar debt products. However, investors should remember that debt portfolios can experience fluctuations when interest rates rise, particularly because some NPS debt schemes maintain higher duration exposure.

The biggest takeaway is simple: Tier 2 offers freedom. Whether that freedom is valuable depends on how much liquidity you want in your overall investment portfolio.

Transaction Costs, Fees, and Minimum Investment Thresholds

One of the strongest arguments in favour of NPS, regardless of tier, is its exceptionally low cost structure.

Compared with many actively managed investment products, NPS charges remain remarkably modest. Pension Fund Managers operate under fee limits prescribed by PFRDA, helping subscribers retain more of their investment returns over the long run. The latest fee framework effective from April 1, 2026, is available here.

In addition to fund management fees, subscribers may incur small charges related to CRA maintenance and transaction processing through Points of Presence. These costs are generally minimal when compared with many traditional investment products.

For Tier 2 specifically:

• Minimum contribution per transaction: ₹250

• No minimum annual contribution requirement

• No minimum balance requirement

• No separate annual maintenance fee exclusively for holding a Tier 2 account beyond standard PRAN-related charges

Low costs might not seem exciting at first glance, but over a 20- or 30-year investment horizon they can have a surprisingly large impact. Every rupee saved on fees remains invested and continues compounding, which is exactly what long-term investors want.

Direct Comparison: NPS Tier 1 vs Tier 2

Purpose: Long-Term Pension vs. Flexible Investing

Although both Tier 1 and Tier 2 operate under the same NPS umbrella and invest in similar asset classes, they are built for very different objectives.

Tier 1 is fundamentally a retirement account. Its structure encourages long-term investing by restricting access to funds and rewarding disciplined contributions through tax benefits. If your goal is to build a pension corpus that supports you after retirement, Tier 1 is the account designed for that purpose.

Tier 2, on the other hand, offers much greater flexibility and functions as an open-ended investment account. While it generally lacks the tax benefits of Tier 1, Central Government employees may claim deductions under Section 80C for Tier 2 contributions, provided the funds are maintained through a mandatory three-year lock-in period.

Here’s a simplified comparison:

| Parameter | NPS Tier 1 | NPS Tier 2 |

| Primary objective | Retirement corpus and pension planning | Flexible investing and wealth creation |

| Account status | Mandatory when joining NPS | Optional |

| Lock-in period | Until age 60, subject to limited exceptions | None |

| Minimum annual contribution | ₹1,000 | No annual requirement |

| Tax benefits on contribution | Available under applicable sections | Generally unavailable |

| Withdrawal flexibility | Restricted | Fully flexible |

| Best suited for | Long-term retirement planning | Investors seeking liquidity and flexibility |

Rather than viewing them as competing options, it is often more useful to think of them as serving different jobs within the same financial plan. Tier 1 helps secure your future retirement needs. Tier 2 gives you easier access to your money when life demands flexibility.

Withdrawal Flexibility and Emergency Access

The difference in withdrawal rules is arguably the single biggest distinction between the two accounts.

Tier 1 is intentionally restrictive. Outside specific partial withdrawal provisions, investors generally cannot access their money until retirement. Even when partial withdrawals are allowed, they are subject to limits and must satisfy prescribed conditions.

This lack of liquidity can feel inconvenient in the short term, but it is also one of the reasons NPS works so well as a retirement vehicle. Many investors underestimate how tempting it can be to dip into long-term savings when money remains easily accessible.

Tier 2 takes the opposite approach. There are no restrictions on withdrawals, no waiting period, and no limits on the number of redemption requests. Funds can be withdrawn whenever required, whether for an emergency, a planned expense, or simply a change in investment strategy.

As noted in Scripbox’s Tier 1 versus Tier 2 comparison, combining both accounts can create a practical two-layer structure. Tier 1 serves as the protected retirement bucket, while Tier 2 provides liquidity for medium-term goals and unexpected expenses.

For investors who struggle to balance long-term discipline with short-term flexibility, that combination can work remarkably well.

Tax Exemptions on Contributions

When it comes to tax benefits, Tier 1 has a clear and significant advantage.

Contributions made to Tier 1 may qualify for deductions under Section 80CCD (1), the additional Section 80CCD(1B) deduction of up to ₹50,000, and employer contribution benefits under Section 80CCD (2), depending on the subscriber’s circumstances and tax regime.

Tier 2 generally offers none of these benefits for regular subscribers.

This distinction matters because tax savings can substantially improve the effective return on an investment. A ₹50,000 contribution that also reduces your tax liability creates value in two ways: through investment growth and through immediate tax savings.

For many investors, particularly those following the old tax regime, the availability of Section 80CCD(1B) is one of the strongest reasons to prioritise Tier 1 contributions before allocating additional money elsewhere.

Annual Maintenance Rules and Cost Efficiency

One area where both accounts are surprisingly similar is cost.

NPS has built a reputation as one of India’s most cost-efficient long-term investment platforms, and that advantage extends across both tiers. Since Tier 1 and Tier 2 are linked to the same PRAN, administrative expenses are streamlined and relatively low.

The annual CRA maintenance charges apply at the PRAN level rather than being duplicated separately for each account. As a result, simply opening a Tier 2 account does not create a significant additional cost burden.

Detailed fee schedules and operational charges can be reviewed here.

From a cost perspective, both accounts remain highly competitive compared with many other investment products available to retail investors. Over long periods, lower expenses can translate into noticeably better net returns, especially when compounded over decades.

Deep Dive into Section 80CCD(1B) Tax Benefits

What is the Section 80CCD(1B) Tax Exemption?

Section 80CCD(1B) is one of the most valuable tax benefits available to retirement-focused investors in India. Introduced to encourage long-term pension savings, it allows individuals to claim an additional deduction of up to ₹50,000 for contributions made to their NPS Tier 1 account.

What makes this deduction particularly attractive is that it sits outside the standard ₹1.5 lakh limit applicable to Section 80C and Section 80CCD(1). In other words, even if you have already exhausted your entire Section 80C limit through investments such as EPF, PPF, ELSS, life insurance premiums, or home loan principal repayments, you can still claim an extra ₹50,000 deduction through NPS.

Further details can be found in this guide and the official Income Tax India resource.

The real-world impact can be significant. For an investor in the 30% tax bracket, a ₹50,000 contribution under Section 80CCD(1B) can reduce the tax bill by approximately ₹15,600 after accounting for cess. Taxpayers in lower brackets also benefit, although the savings naturally vary according to their applicable tax rate.

Few tax-saving provisions offer such a straightforward combination of immediate tax relief and long-term retirement growth.

How Do I Claim the Extra ₹50,000 Deduction in NPS?

Claiming the additional deduction is relatively simple, provided the contribution is made to a Tier 1 account during the relevant financial year.

To utilise the full benefit, you need to contribute at least ₹50,000 to your NPS Tier 1 account. While filing your income tax return, this amount is reported separately under Section 80CCD(1B) in Schedule VI-A. The maximum deduction available under this section remains capped at ₹50,000, even if your actual contribution exceeds that amount.

It is important to retain supporting documents for record-keeping and verification purposes. These typically include:

• NPS account statement showing the contribution details

• Contribution receipt or transaction statement downloaded from the CRA portal

• PRAN details for reference

According to HDFC Bank’s NPS tax guide, salaried employees should also verify whether contributions have been reflected in Form 16. If contributions were made directly rather than through payroll, they may need to be entered manually while filing the return.

A small administrative step, perhaps. But one that can result in meaningful tax savings year after year.

Salaried Employees vs. Self-Employed: Claiming the Benefit

The Section 80CCD(1B) benefit is available to both salaried individuals and self-employed taxpayers, although the way contributions are made often differs.

For salaried employees, NPS contributions may be routed through payroll, in which case the relevant deductions are often reflected automatically in Form 16. However, many employees choose to make additional voluntary contributions directly into their PRAN account. These top-up contributions can also qualify for the additional deduction, provided they are correctly disclosed while filing the income tax return.

Self-employed individuals follow a slightly different path because there is no employer contribution component involved. Every eligible deduction comes from their own contributions to the scheme.

One advantage for self-employed professionals is the broader deduction framework available under Section 80CCD(1), combined with the separate ₹50,000 deduction available through Section 80CCD(1B). Detailed examples illustrating both scenarios are available in Cleartax’s guide.

Regardless of employment status, the principle remains the same: contributions made to Tier 1 can potentially reduce current tax liability while simultaneously building long-term retirement wealth.

NPS Tax Benefit for Self-Employed 2026

For self-employed professionals, NPS often remains one of the most underappreciated retirement planning tools available.

Doctors, consultants, architects, freelancers, lawyers, and business owners frequently focus on business growth and tax management while postponing structured retirement planning. NPS offers a way to address both objectives at the same time.

Consider a self-employed professional earning ₹20 lakh annually during FY 2025-26. Subject to applicable tax rules and overall deduction limits, NPS contributions may allow the individual to utilise:

• Deductions under Section 80CCD(1) within the broader Section 80C framework

• An additional exclusive deduction of up to ₹50,000 under Section 80CCD(1B)

In practical terms, this means taxable income can potentially be reduced by up to ₹2 lakh annually under the old tax regime when both deduction buckets are fully utilised.

For professionals who do not have access to employer-sponsored retirement benefits, this combination of tax efficiency and long-term wealth accumulation can be particularly valuable. The challenge is not whether the benefit exists. More often, it is that many eligible taxpayers never take full advantage of it.

That said, these benefits apply primarily under the old tax regime. The picture changes considerably under the new regime, which is why understanding the next section is essential before making contribution decisions.

NPS Taxation: Old Tax Regime vs. New Tax Regime (2026)

The Validity of Section 80CCD(1B) Under the Old Regime

For taxpayers who continue to opt for the old tax regime, Section 80CCD(1B) remains one of the strongest arguments in favour of investing through NPS.

The additional ₹50,000 deduction is fully available and can be claimed over and above the standard ₹1.5 lakh deduction limit under Section 80C and Section 80CCD(1). This creates an opportunity to lower taxable income while simultaneously strengthening long-term retirement savings.

For many taxpayers, especially those already claiming deductions for EPF contributions, life insurance premiums, home loan principal repayments, children’s tuition fees, or other eligible investments, the separate nature of Section 80CCD(1B) is what makes it so valuable. It does not compete for space within the already crowded Section 80C bucket.

As highlighted in Kotak Bank’s detailed guide on Section 80CCD, NPS remains one of the few financial products that offers access to an exclusive deduction category. For investors focused on tax efficiency, that distinction matters.

In practical terms, the old regime continues to reward disciplined savers. The more effectively you utilise available deductions, the greater the potential reduction in your tax liability.

How the New Tax Regime (Section 115BAC) Eliminates Self-Contribution Benefits

The shift to the new tax regime fundamentally changes how many investors should evaluate NPS contributions.

Under Section 115BAC, deductions available under provisions such as Section 80C, Section 80D, and Section 80CCD(1B) are generally not permitted. As a result, self-contributions made to an NPS Tier 1 account no longer generate the upfront tax savings that have traditionally been one of the scheme’s biggest attractions.

This point is often misunderstood.

Many investors continue making additional NPS contributions assuming they will automatically receive the familiar ₹50,000 deduction. If they are filing under the new tax regime, that benefit simply does not apply.

That does not mean NPS loses all value. Contributions still participate in market-linked growth. The retirement corpus continues to benefit from long-term compounding. The 60% tax-free lump sum withdrawal at maturity also remains available. What disappears is the immediate deduction that once improved the investment’s overall tax-adjusted return.

For investors who have adopted the new regime, contribution decisions should therefore be based primarily on retirement planning goals rather than tax-saving expectations.

Maximizing Employer Contributions Under Section 80CCD(2) Across Both Regimes

This is where NPS becomes particularly interesting from a tax planning perspective.

While self-contribution deductions largely disappear under the new tax regime, employer contributions under Section 80CCD(2) continue to enjoy favourable treatment under both tax regimes.

Employer contributions made to an employee’s Tier 1 account can be deducted from taxable income, subject to the prescribed limits. Currently, the ceiling is generally 10% of basic salary plus dearness allowance for private-sector and PSU employees, while Central Government employees enjoy a higher permissible limit.

This benefit sits outside the usual Section 80C framework and remains available even when an employee chooses the new tax regime.

As a result, many salaried professionals are increasingly exploring salary restructuring options that incorporate higher employer NPS contributions. In some cases, this can create meaningful tax savings without increasing the employer’s overall compensation cost.

ICICI Bank’s NPS FAQ page (https://www.icici.bank.in/personal-banking/investments/government-schemes/nps-national-pension-system/new-pension-system-faqs) discusses this strategy in greater detail and explains how employer contributions are treated under current tax rules.

For employees who have already migrated to the new regime, Section 80CCD(2) is often the most important NPS-related tax benefit still available.

Should I Invest in NPS if I am in the 30% Tax Bracket?

The answer depends largely on which tax regime you follow.

For investors in the 30% tax bracket who continue to use the old tax regime, NPS remains highly attractive. The additional ₹50,000 deduction available through Section 80CCD(1B) alone can generate tax savings of approximately ₹15,600 annually after accounting for cess. When combined with tax-efficient compounding and the 60% tax-free withdrawal at retirement, the overall proposition becomes difficult to ignore.

The calculation changes under the new tax regime.

Without access to deductions on self-contributions, NPS no longer delivers the same immediate tax advantage. Investors must evaluate it more as a retirement product than a tax-saving tool. In that context, factors such as long-term investment discipline, professional fund management, low costs, and retirement income planning become more important.

Employer contributions under Section 80CCD(2) continue to strengthen the case for NPS even under the new regime. Investors with access to this benefit often find that NPS still deserves a place in their retirement portfolio, particularly when retirement is decades away and compounding has ample time to work.

As discussed in Taxmann’s analysis, the decision is no longer purely about deductions. It is about balancing tax efficiency, retirement security, and long-term wealth creation within the framework of your chosen tax regime.

For many high-income earners, NPS remains worthwhile. The reasons simply become more nuanced once the new tax regime enters the conversation.

Taxation Rules on NPS Returns and Withdrawals

Tax-Free 60% Lump Sum Payout at Maturity (Tier 1)

One of the most attractive features of NPS Tier 1 is the tax treatment available at retirement.

When you reach age 60 or superannuation and choose to exit the scheme, you can withdraw up to 60% of your accumulated corpus as a lump sum. This amount is completely tax-free. No income tax, capital gains tax, or TDS applies to this portion of the withdrawal, regardless of how large the corpus has grown over the years.

This benefit can have a substantial impact on retirement planning. After decades of contributions and compounding, being able to access a majority of the corpus without an additional tax burden significantly improves the effective value of your retirement savings.

Scripbox’s NPS withdrawal guide provides a detailed explanation of the withdrawal process, required documentation, and timelines for subscribers approaching retirement.

For many investors, this tax-free exit provision is one of the key reasons NPS remains competitive even when compared with other long-term investment options.

Taxation on the 40% Mandatory Annuity Income

While the 60% lump sum enjoys complete tax exemption, the remaining 40% of the corpus follows a different path.

Under current NPS rules, this portion must generally be used to purchase an annuity from an approved provider. The annuity then generates a regular pension income, usually paid monthly, quarterly, half-yearly, or annually depending on the option selected.

Here’s the important part: the purchase of the annuity itself is not taxed, but the pension income received from that annuity is fully taxable according to your applicable income tax slab.

This distinction often surprises first-time NPS investors. Many assume that because NPS offers tax benefits during accumulation and a tax-free lump sum at retirement, the pension income will also be exempt. That is not the case.

As a result, retirement planning should not focus solely on building the largest possible corpus. Investors should also think about how much taxable annuity income they are likely to receive and how that income fits into their broader retirement cash flow needs.

The PRIDE DISHA calculator can help subscribers model different corpus sizes and estimate potential retirement outcomes under various scenarios.

Can I Withdraw 100% From NPS if Corpus is Below ₹8 Lakh?

This is one of the most frequently misunderstood NPS withdrawal rules.

Many investors refer to an ₹8 lakh threshold, but the current provision actually applies to a corpus of ₹5 lakh or less.

According to the PFRDA (Exit and Withdrawals under the NPS) (Amendment) Regulations, 2025, subscribers whose total corpus at the time of normal exit is ₹5 lakh or below can withdraw the entire amount as a lump sum.

In such cases, there is no requirement to purchase an annuity.

This rule exists for a practical reason. Forcing a subscriber with a relatively small corpus to convert a portion of it into an annuity would often result in extremely low pension payouts that offer limited financial value.

The full withdrawal remains tax-free under normal exit conditions, making the provision particularly beneficial for subscribers with smaller retirement balances.

For premature exits, however, different rules apply. In most situations, only 20% of the corpus can be withdrawn as a lump sum while 80% must be used to purchase an annuity, subject to the applicable exceptions and thresholds.

NPS Withdrawal Rules Before 60 Years 2026

NPS was designed primarily as a retirement vehicle, so early withdrawal rules are intentionally restrictive.

If you’re considering exiting the scheme before age 60, it’s important to understand the limits that apply.

Before completing three years of membership

Generally, voluntary exit is not permitted during the initial three-year period, except in the event of the subscriber’s death.

After three years but before age 60

Subscribers can opt for a premature exit. However, only 20% of the corpus can typically be withdrawn as a lump sum. The remaining 80% must be used to purchase an annuity.

Partial withdrawals

After completing three years in the scheme, subscribers may access up to 25% of their own contributions for specified purposes such as higher education, marriage, purchase of a first house, treatment of critical illnesses, or disability-related requirements. A maximum of three such withdrawals is permitted during the entire NPS tenure.

Death of the subscriber

In the unfortunate event of the subscriber’s death, the entire corpus is paid to the nominee. No annuity purchase is required, and the amount received remains fully tax-free for the beneficiary.

Official exit guidelines can be reviewed here, while a detailed practical overview is available in this guide.

The broader theme running through all these rules is consistency. NPS rewards investors who stay invested for the long haul, while making early exits possible only under controlled circumstances. That structure may feel restrictive at times, but it is also what helps preserve the retirement focus of the scheme.

Advanced Strategies to Maximize Your Retirement Corpus

Utilizing the “Auto Choice” Life Cycle Funds Based on Age

One of the most useful features within NPS is the Auto Choice option, particularly for investors who do not want to actively manage their asset allocation throughout their careers.

Rather than requiring you to manually adjust your equity and debt exposure over time, Auto Choice automatically rebalances your portfolio as you age. The idea is simple: take more risk when you’re young and gradually reduce that risk as retirement approaches.

NPS currently offers three life cycle options:

Aggressive Life Cycle Fund (LC-75)

Starts with up to 75% equity exposure and gradually reduces equity allocation from age 35 onward.

Moderate Life Cycle Fund (LC-50)

Begins with a more balanced approach, allocating up to 50% to equities.

Conservative Life Cycle Fund (LC-25)

Designed for risk-averse investors, with a starting equity allocation of up to 25%.

For younger investors, especially those in their 20s and 30s, the Aggressive Life Cycle Fund often makes the most sense because it allows a larger portion of the portfolio to benefit from long-term equity growth. As retirement gets closer, the automatic shift toward debt instruments helps reduce portfolio volatility without requiring constant monitoring.

Zerodha Varsity’s investment options guide offers a helpful illustration of how these allocations evolve over time.

For many investors, Auto Choice removes one of the biggest challenges in retirement planning: knowing when and how to adjust risk exposure.

Capitalizing on the 75% Maximum Equity Exposure Limit

Equity has historically been one of the most powerful drivers of long-term wealth creation, which is why understanding NPS equity limits is important.

Under the traditional Active Choice framework, non-government subscribers can allocate up to 75% of their portfolio to Scheme E (equities). The remaining allocation is typically spread across government securities and corporate debt.

While some investors view the cap as restrictive, it was originally introduced to balance growth potential with retirement-focused risk management. After all, NPS is designed to provide retirement security, not encourage excessive speculation.

However, the landscape has evolved.

Beginning October 1, 2025, certain eligible subscribers under the Multi-Scheme Framework (MSF) gained access to equity allocations of up to 100%, as detailed in this report.

This change is particularly relevant for younger investors with investment horizons stretching 25, 30, or even 40 years into the future. Over such long periods, the ability to maintain higher equity exposure can significantly increase wealth accumulation potential, though it naturally comes with greater short-term volatility.

Tier 2 investors also enjoy additional flexibility, as 100% equity allocation is generally available regardless of the MSF framework.

The key is not simply choosing the highest possible equity allocation. It is choosing an allocation that you can comfortably stick with during both bull markets and market downturns. Long-term success often depends less on chasing returns and more on staying invested when markets become uncomfortable.

Which is Better: NPS or Mutual Funds?

This question comes up almost every time retirement planning is discussed, and the honest answer is that there is no universal winner.

NPS and mutual funds solve different problems.

For investors following the old tax regime, NPS enjoys advantages that mutual funds simply cannot replicate. The additional Section 80CCD(1B) deduction, employer contribution benefits under Section 80CCD(2), and tax-free treatment of the 60% retirement lump sum create a compelling tax-efficient package.

Mutual funds, meanwhile, offer greater flexibility. There is no mandatory annuity requirement, no retirement lock-in, and investors retain complete control over when and how they access their money.

For investors using the new tax regime, the comparison becomes much closer. Without the additional deduction benefits, mutual funds often gain ground because of their flexibility and favourable long-term capital gains framework.

In reality, most successful retirement plans do not force a choice between the two.

As discussed in Zerodha Varsity’s retirement planning content, the strongest approach is often to combine both. NPS can serve as the disciplined retirement bucket, while mutual funds provide flexibility for goals that may arise long before retirement.

Viewed this way, the question shifts from “Which is better?” to “How much of each should I own?”

EPF vs NPS Comparison Chart

EPF and NPS are often compared because both are widely used retirement savings vehicles. However, they are built on very different foundations.

| Parameter | EPF | NPS Tier 1 |

| Regulator | EPFO | PFRDA |

| Contribution structure | Mandatory for eligible employees, with employer contribution | Flexible contributions with minimum annual requirement |

| Return profile | Interest rate declared periodically | Market-linked returns |

| Tax benefits | Eligible under Section 80C | Eligible under Section 80C, 80CCD(1), 80CCD(1B), and 80CCD(2) where applicable |

| Equity exposure | None | Up to 75% under Active Choice, with higher exposure possible under certain frameworks |

| Maturity treatment | Generally tax-free subject to applicable conditions | 60% tax-free lump sum, balance typically used for annuity purchase |

| Flexibility | Limited | Higher contribution flexibility |

| Best suited for | Investors seeking stability and predictable accumulation | Investors seeking long-term growth and retirement-focused investing |

Rather than viewing EPF and NPS as alternatives, many financial planners see them as complementary tools.

EPF provides stability and predictable accumulation through fixed-interest crediting. NPS introduces equity exposure, diversification, and additional tax planning opportunities. Together, they can create a more balanced retirement portfolio than either product can provide on its own.

For salaried employees with access to both, the goal is often not choosing between EPF and NPS. The goal is learning how to use each for the role it performs best.

Managing Your NPS Portfolio in 2026

Evaluating and Selecting Top-Performing Pension Fund Managers (PFMs)

Choosing the right Pension Fund Manager (PFM) is one of the few decisions within NPS that can meaningfully impact long-term outcomes.

As of 2026, subscribers in the non-government sector can choose from several PFRDA-licensed fund managers, including SBI Pension Funds, LIC Pension Fund, UTI Retirement Solutions, HDFC Pension Management, ICICI Prudential Pension Funds, Kotak Mahindra Pension Fund, Aditya Birla Sun Life Pension Management, and Tata Pension Management.

With so many options available, investors often focus solely on recent returns. That can be tempting, but it rarely tells the full story.

A more balanced evaluation should include:

• Long-term performance across 5- and 10-year periods

• Consistency during different market cycles

• Performance across equity (Scheme E), corporate debt (Scheme C), and government securities (Scheme G)

• Assets under management and operational track record

• Risk-adjusted returns rather than headline returns alone

Retirement investing is a marathon, not a sprint. A fund manager that consistently performs well across market conditions is often more valuable than one that tops the charts for a single year.

The goal isn’t necessarily to find the highest return. It’s to find a manager capable of delivering competitive results over decades.

Best NPS Fund Manager 2026 Performance

The question “Which NPS fund manager is the best?” doesn’t have a permanent answer because rankings change over time.

Performance varies across asset classes, time periods, and market conditions. A fund manager who leads in equity returns over three years may not hold the same position over ten years. That’s why investors should look beyond short-term performance snapshots.

For the most current comparisons, Value Research Online maintains a detailed NPS performance tracker.

Historically, fund managers such as SBI Pension Funds and HDFC Pension Management have often featured among the stronger long-term performers in Scheme E. However, leadership positions shift as market conditions evolve.

Investors interested in more recent trends can also review Livemint’s performance analysis, which examines annualised returns across major pension fund managers.

One often-overlooked feature of NPS is the ability to diversify fund manager risk. Subscribers can allocate investments across more than one fund manager within the same PRAN structure, reducing dependence on the decisions of any single institution.

Past performance remains a useful reference point. It should never be mistaken for a forecast.

Guidelines for Switching PFMs and Investment Schemes

NPS provides flexibility not only in choosing a fund manager but also in changing that choice when circumstances warrant it.

Subscribers can generally switch their Pension Fund Manager once during a financial year without any charge. Additional switches may attract a nominal fee, depending on the applicable rules at the time.

The process itself is straightforward. A subscriber simply logs into the CRA portal, selects the fund manager change option, and submits the request online. In most cases, the change is processed within a few working days.

Asset allocation changes are also permitted. Investors can modify their exposure between Scheme E (equity), Scheme C (corporate bonds), and Scheme G (government securities), or move between Active Choice and Auto Choice, subject to the limits prescribed by PFRDA.

This flexibility is particularly useful because financial goals evolve over time. A 30-year-old investor seeking growth may prefer aggressive equity exposure, while someone approaching retirement may choose to gradually reduce risk.

The official investment guideline circular detailing these processes is available here.

The ability to adapt is one of the reasons NPS remains relevant across different stages of an investor’s life.

NPS Login NSDL Portal Registration

Managing an NPS account has become considerably easier over the past few years, thanks to the expansion of digital services and online account management tools.

Subscribers can access their accounts through the following official platforms:

• Protean (formerly NSDL) CRA Portal

• CAMS NPS Subscriber Portal

• KFintech Subscriber Portal

These portals allow subscribers to:

• Make contributions

• Update personal information

• Change pension fund managers

• Modify investment preferences

• Track portfolio performance

• Initiate withdrawal and exit requests

To register or log in, subscribers generally need their PRAN, PAN, and registered mobile number for OTP verification. First-time users may also need to complete FATCA-related declarations.

Modern NPS platforms support contributions through net banking, UPI, and D-Remit facilities, making account funding considerably more convenient than it was in the scheme’s earlier years.

The introduction of the multiple NAV framework from April 1, 2026, further improves transaction processing efficiency and operational flexibility. Details are available here.

For most subscribers today, managing an NPS account requires little more than a smartphone and a few minutes of attention each year.

Securing Your Financial Future with NPS

Aligning NPS with Broader Financial Goals

NPS works best when it is viewed as part of a larger financial strategy rather than a standalone investment.

Retirement planning rarely succeeds because of a single product. More often, it is the result of several financial tools working together. For salaried employees, that might include EPF for stable retirement accumulation, PPF for long-term tax-efficient savings, mutual funds for growth and liquidity, and health insurance for protection against unexpected medical expenses. NPS fits into this ecosystem by providing disciplined retirement-focused investing backed by tax advantages and professional fund management.

The most effective approach is to use each product for what it does best.

Tier 1 is designed for long-term retirement accumulation. Its lock-in structure helps prevent impulsive withdrawals and encourages consistency over decades. Other instruments can then be used for shorter-term goals such as buying a home, funding education, building an emergency reserve, or creating additional investment flexibility.

If you continue to follow the old tax regime, making a ₹50,000 contribution to Tier 1 each financial year to fully utilise Section 80CCD(1B) should be high on your tax-planning checklist. Few deductions provide such a direct and measurable reduction in tax liability.

For taxpayers who have moved to the new tax regime, the focus shifts. In that case, exploring employer contributions under Section 80CCD(2) may offer a more meaningful tax-saving opportunity than additional voluntary contributions.

The HDFC Bank guide on important NPS rules provides a useful account review checklist covering nominations, contact details, account maintenance, and other administrative essentials that are easy to overlook but important to keep updated.

Frequently Asked Questions (FAQs): NPS Tier 1 vs Tier 2

No, the additional ₹50,000 deduction under Section 80CCD(1B) for personal contributions is abolished in the New Tax Regime. This benefit is exclusively available under the Old Tax Regime. However, employer contributions remain tax-deductible up to 14% of your basic salary under Section 80CCD(2) across both tax regimes.

An NPS Tier 1 account is designed for retirement and has a mandatory lock-in period until the age of 60, though partial withdrawals (up to 25% of self-contribution) are permitted for specific emergencies after three years. Conversely, an NPS Tier 2 account functions as a flexible voluntary investment vehicle with zero lock-in period, allowing unrestricted withdrawals at any time.

Under updated rules, if your total NPS corpus is below ₹8 lakh, you are permitted to make a 100% tax-free lump sum withdrawal. If the corpus exceeds ₹8 lakh, you can withdraw a maximum of 60% as a tax-free lump sum, while the remaining 40% must be utilized to purchase an annuity, which will provide a taxable monthly pension.

Generally, NPS Tier 2 accounts offer no tax benefits for private sector employees or self-employed individuals. Capital gains on withdrawals are taxed according to your applicable income slab. The only exception is for Central Government employees, who can claim a deduction under Section 80C if they agree to a three-year lock-in period on their Tier 2 funds.

If the subscriber passes away before age 60, the entire accumulated corpus is paid to the registered nominee or legal heir, and this payout is completely exempt from income tax.

| Parameter | NPS Tier 1 | NPS Tier 2 |

| Primary Objective | Retirement corpus and pension planning | Flexible investing and wealth creation |

| Account Status | Mandatory when joining NPS | Optional (requires active Tier 1 PRAN) |

| Lock-in Period | Until age 60 (subject to limited exceptions) | None (functions as an open-ended fund) |

| Minimum Contribution | ₹500 per transaction / ₹1,000 annually | ₹250 per transaction / No annual minimum |

| Tax Benefits | Deductions under 80C, 80CCD(1), 80CCD(1B), 80CCD(2) | Generally none (contributions made from post-tax income) |

| Withdrawal Flexibility | Restricted; 60% tax-free lump sum and 40% annuity at 60 | Fully flexible; unrestricted withdrawals at any time |

| Tax on Gains | 60% lump sum is tax-free; annuity pension is taxable | Gains are taxed according to user’s income tax slab |

Final Assessment: Optimizing Tier 1 and Tier 2 Utilization

After comparing Tier 1 and Tier 2 across taxation, liquidity, investment flexibility, withdrawal rules, and long-term retirement planning objectives, a fairly clear picture emerges.

The strongest NPS strategies do not treat the two accounts as interchangeable. Instead, they assign a specific role to each.

For investors using the old tax regime and planning for retirement over the long term

• Contribute at least ₹50,000 annually to Tier 1 to fully utilise the Section 80CCD(1B) deduction

• Take advantage of employer contributions under Section 80CCD(2) whenever available

• Maintain higher equity exposure during the accumulation years through Active Choice or an aggressive Auto Choice option, then gradually reduce risk closer to retirement

• Use Tier 2 selectively for medium-term savings and low-cost market exposure when additional liquidity is desirable

For investors using the new tax regime

• Focus on employer NPS contributions that qualify under Section 80CCD(2)

• Continue using Tier 1 as a retirement planning tool even without self-contribution deductions, particularly if retirement remains many years away

• Compare Tier 2 with debt and liquid mutual funds before allocating surplus capital, using current performance data from

For self-employed professionals

• NPS remains one of the most tax-efficient retirement vehicles available under the old tax regime

• Contributions can help build retirement wealth while reducing taxable income through Sections 80CCD(1) and 80CCD(1B)

• Regularly review whether the old or new tax regime offers the better overall outcome based on your deduction profile and income structure

At its core, NPS offers something increasingly valuable in modern financial planning: structure.

Whether you are a salaried employee, a government worker, a freelancer, a consultant, or a business owner, the system combines regulated oversight, professional fund management, retirement-focused discipline, and potentially meaningful tax advantages in a single framework.

The biggest mistake many investors make is assuming Tier 1 and Tier 2 serve the same purpose. They do not.

Tier 1 is built to secure your retirement. Tier 2 is built to provide flexibility.

Understanding that distinction, and using each account intentionally, is what ultimately unlocks the full value of the National Pension System.

Disclaimer

This article is for informational purposes only and does not constitute financial or tax advice. Tax laws and NPS regulations are subject to change. Please consult a qualified financial advisor or tax consultant before making investment or tax planning decisions.

Leave a Reply